HBAN - Truist Financial: Bargain Hunting For Value And Yield In Financial Institutions

2023-11-24 09:00:00 ET

Summary

- Truist Financial Corporation is undervalued and represents a long-term investment opportunity.

- The financial sector may face challenges in 2024 due to potential interest rate cuts and a possible recession.

- TFC is adapting to the digital banking trend and has seen increased engagement in its mobile app and digital transactions.

While the S&P 500 has increased by 19.14% and the Nasdaq has climbed 46.40% YTD, the financial sector hasn't contributed much to the rally. We're ending a Fed tightening cycle, which has allowed financial institutions to generate larger amounts of interest income while loaning capital at higher rates, yet many in the financial space have seen better years. The Financial Select Sector SPDR Fund ETF ( XLF ) has appreciated by 2.77%, while the SPDR S&P Regional Banking ETF ( KRE ) has declined by -23.98%. Despite the Silicon Valley Bank fiasco being in the rearview, many regional banks are still dealing with the ramifications. The first question I asked myself was whether the regional banking sector would get rolled up into large financial institutions. Since I don't believe that will occur, my next question was where potential value could exist in the regional banking sector. After looking through many of the regional banks, Truist Financial Corporation ( TFC ) looks undervalued. I am trying to position myself ahead of the curve, and while it could take years, not months, for my investment thesis to play out, I think there is an opportunity in shares of TFC, and the 6.59% yield is large enough for me to patiently wait.

{kind=link}

Following up on my previous article about TFC

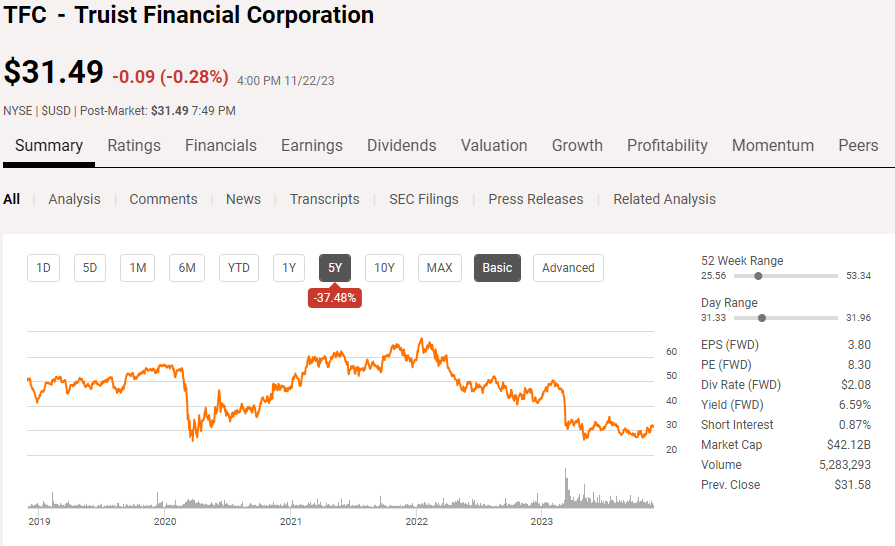

After the regional banking crisis started to die down, I wrote an article on TFC on 5/9/23 ( can be read here ). Since then, shares of TFC have appreciated by 11.15% compared to the S&P, climbing 10.51%, and when TFC's dividends are factored in, the total return has been 17.17%. In that article, I discussed why I didn't feel regionals would get rolled up into the large money centers, why TFC looked interesting, the dividend profile, and how TFC stacked up against its peer group. While TFC has outperformed the market since then, it's still in the negative for 2023, and well off its 5-year highs. I am following up on my previous article because I feel that TFC still represents significant value, and there could be further upside on the horizon.

Regional banks and other segments of financials could experience a tough 2024

While I see long-term value in shares of TFC, there is certainly a bear case for investing in the financial sector at this point in time. The CME Group is projecting that there is a 94.8% chance the Fed is done hiking rates and that there is a 28.4% chance we will see our first rate cut in March of 2024. Looking out to the end of 2024, CME Group is projecting that there is a 96% chance that rates could be somewhere between 350-500 bps, with the most likely level for the target rate to finish the year between 425-450 bps. While individual investors are eagerly awaiting a Fed pivot, it's a double-edged sword for financials. On one hand, the cost of capital will decline so the likelihood of defaults should decline, and borrowing should increase, driving volumes higher. The negative is that banks such as TFC will not be generating the same returns on interest generated. The rising rate environment has helped TFC grow its total interest income and net interest income to all-time highs on an annual basis, and lower rates could significantly impact these line items. We will need to see what occurs and if volumes can increase on borrowings enough to offset the loss of income made on interest.

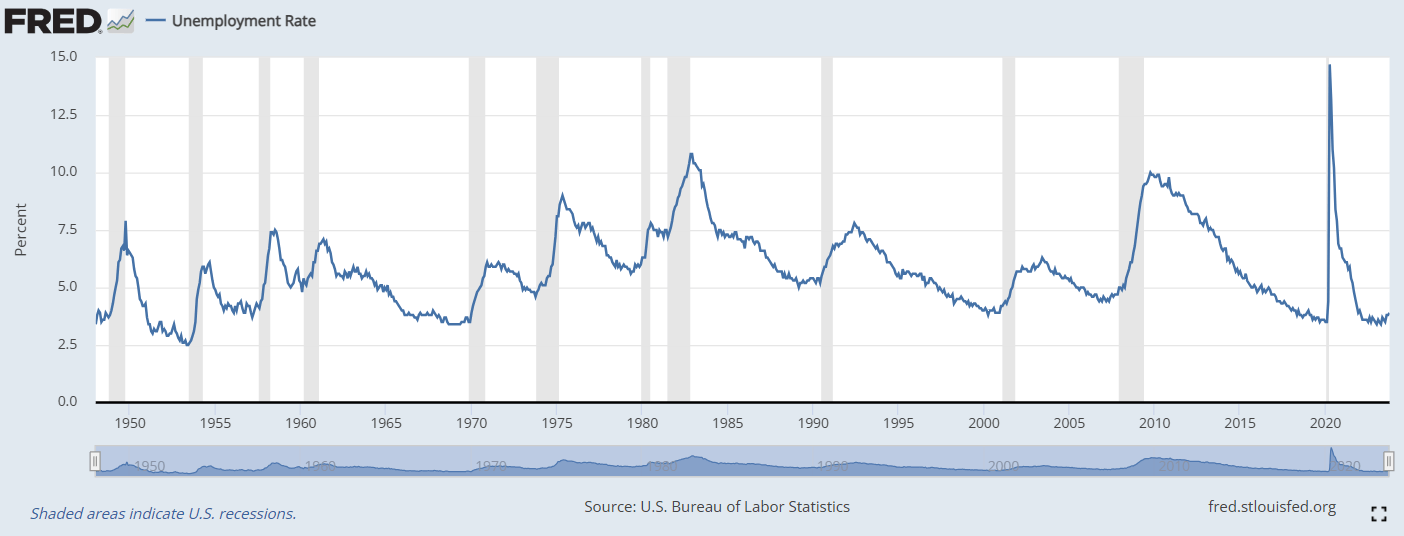

I was previously in the camp that a recession would be as the economic data changes, so does my opinion. Financials don't typically do well during periods of recession, and if we head into one next year, it could be another unattractive year for the sector. Since the early 1970's an inverted yield curve for more than 3 months has been followed by a recession, excluding the pandemic. While I don't feel this is the best indicator to look at, the inverted yield curve does have a high probability of indicating that a recession is looming. The indicator I pay more attention to is unemployment. Since 1948, the past 12 recessions have all occurred as unemployment increased by more than 1%. Unemployment has increased from 3.4% in April to 3.9%, while corporate bankruptcies have also increased QoQ for the past 5 quarters. If unemployment continues on this trajectory, we're almost certain to enter a recession. If we do the Fed could be forced to lower rates quicker than they want, and the probability of defaults will increase. This will add additional negative exposure to banks as a portion of their loans could be impacted, and they will not generate as much income from interest generated. This is why I think TFC is a long-term investment for me, as I can't predict the future. There is a growing bear case for financials in the short term, and we will need to wait and see how things play out on a macroeconomic level.

{kind=link}

TFC may be the oldest bank headquartered in North Carolina but that hasn't deterred it from changing with the times

Prior to diving into TFC's financials, I wanted to discuss a different aspect, which is digital banking. Some of those who read this article already know that I am very bullish on SoFi Technologies, Inc. ( SOFI ) because I think financial institutions are undergoing a large shift to meet their customer's needs. The demands from customers have evolved as new technological capabilities have emerged. Banking before the smartphone renaissance and banking today looks completely different.

One of the fears I have with smaller financial institutions is their ability to keep up with technology. The days of being confined to the banks within a specific distance of your primary residence are long gone. Someone living in a small town doesn't have to use a community or regional bank as they can open accounts at a large money center such as JPMorgan Chase & Co. ( JPM ) or a digital bank such as SOFI from their couch. Just about all your financial needs can be established and utilized from anywhere you are without stepping foot inside a physical location. One of my biggest fears with smaller banks, in particular, was the unknown of how they would deal with the changing landscape.

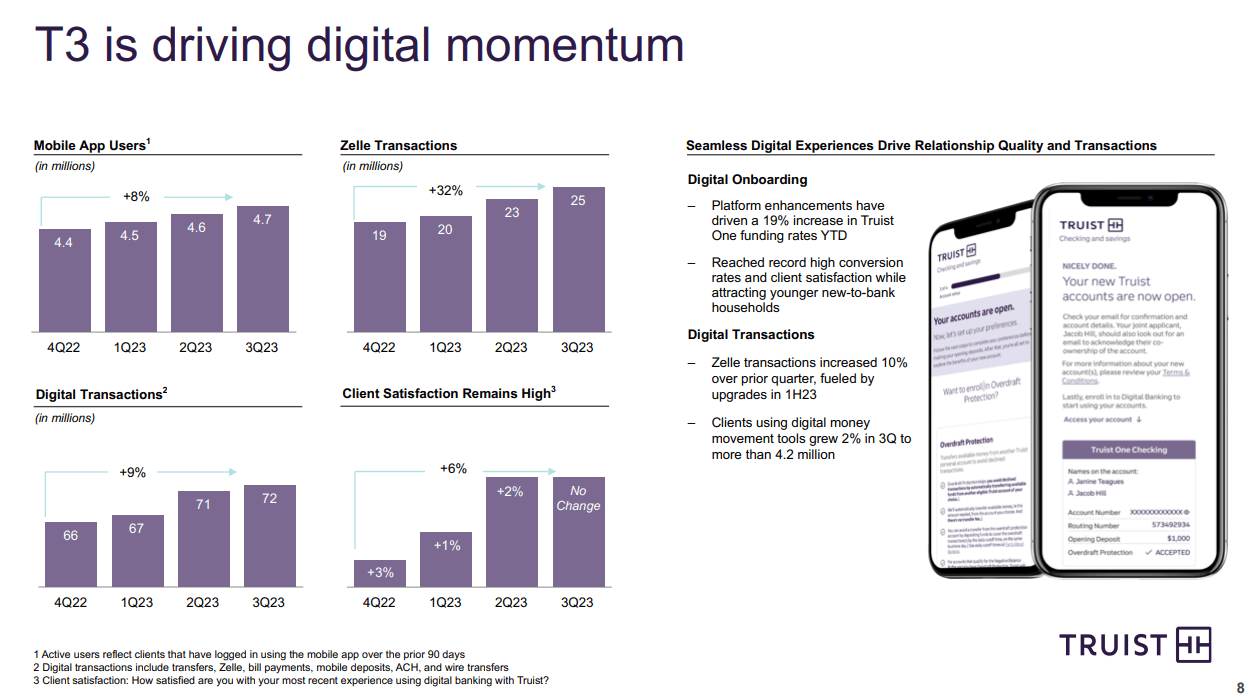

TFC answered many of these questions for me in Q3. For me to allocate capital toward traditional financial institutions, the digital trends have to be headed up and to the right. TFC continues to see additional engagement as mobile app users and digital transactions continue to increase. Digital transactions now account for more than 60% of TFC's total banking transactions. This is why digital is so important for all banks, as there is less of a need to continuously visit a brick-and-mortar location when most of a person's financial needs are conducted digitally. Since the end of 2022, TFC has gained 3 million mobile users as its mobile app users have grown by 8% to 4.7 million. TFC's quarterly digital transactions have increased by 6 million or 9% as their users conducted 72 million digital transactions in Q3. One of the hottest functions for digital banking is utilizing Zelle, and TFC saw its Zelle utilization grow by 32% to 25 million transactions since the end of 2022.

TFC is allocating a tremendous amount of resources to its TC initiative, which is their concept that touch and technology work together to create trust. TFC isn't letting the technological revolution pass by, and it's making sure that it can enhance its customer experience and drive further adoption and efficiency as banking goes further into the digital space. I am happy with the digital metrics, as this is critical for any financial institution's future success.

{kind=link}

Truist's underlying business and the dividend continue to thrive

A big negative for regional banks was that they had underwritten a large portion of commercial real estate loans, and the narrative had turned negative. Unibail-Rodamco-Westfield and Brookfield Properties were preparing to hand the keys to the Westfield San Francisco Centre, which is a 1.2-million-square-foot shopping center in downtown San Francisco's Union Square, back to its lenders. According to the San Francisco Business Times, payments on its $588 million loan were halted. The large fear had been that banks would be sitting on unwanted assets as more entities handed the keys back and large losses would occur due to banks having to sell these assets well below their previous fair values.

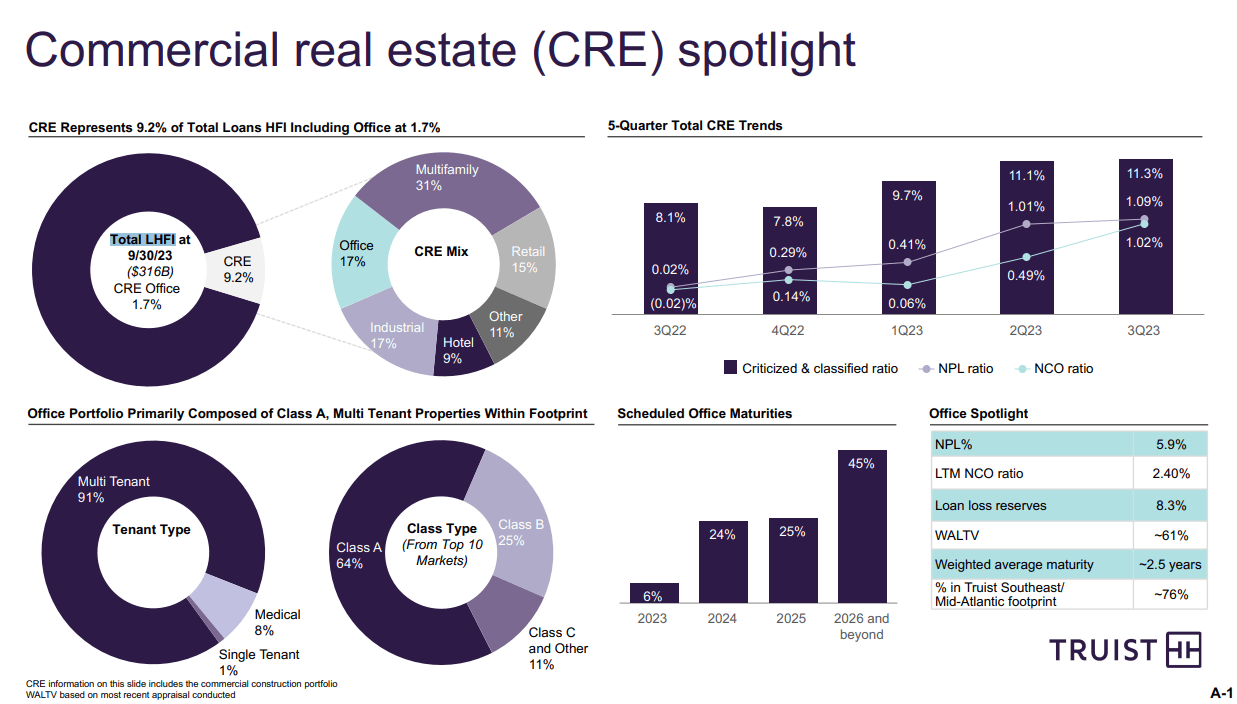

TFC has done a great job of highlighting its exposure to the sector in its quarterly presentation . TFC had $316 billion worth of loans held for investment on its balance sheet at the end of Q3 and offices only represented 1,7% of this portfolio. TFC's exposure to commercial real estate is 9.2% of their total loans held for their investment portfolio. Within its commercial real estate subset, the office is 17% of the asset mix. TFC has a well-diversified loan portfolio, and 45% of the loan maturities from the office segment term will be in 2026 or later. TFC has done a fantastic job at not getting overly exposed to any segment in the commercial real estate space and is positioned to do well if the Fed does in fact, keep rates higher for longer.

{kind=link}

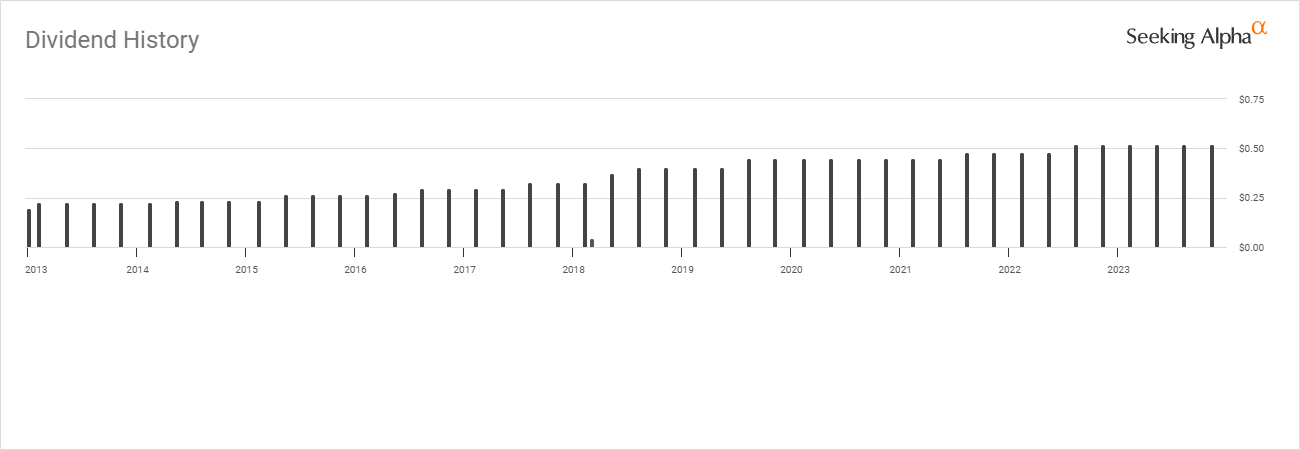

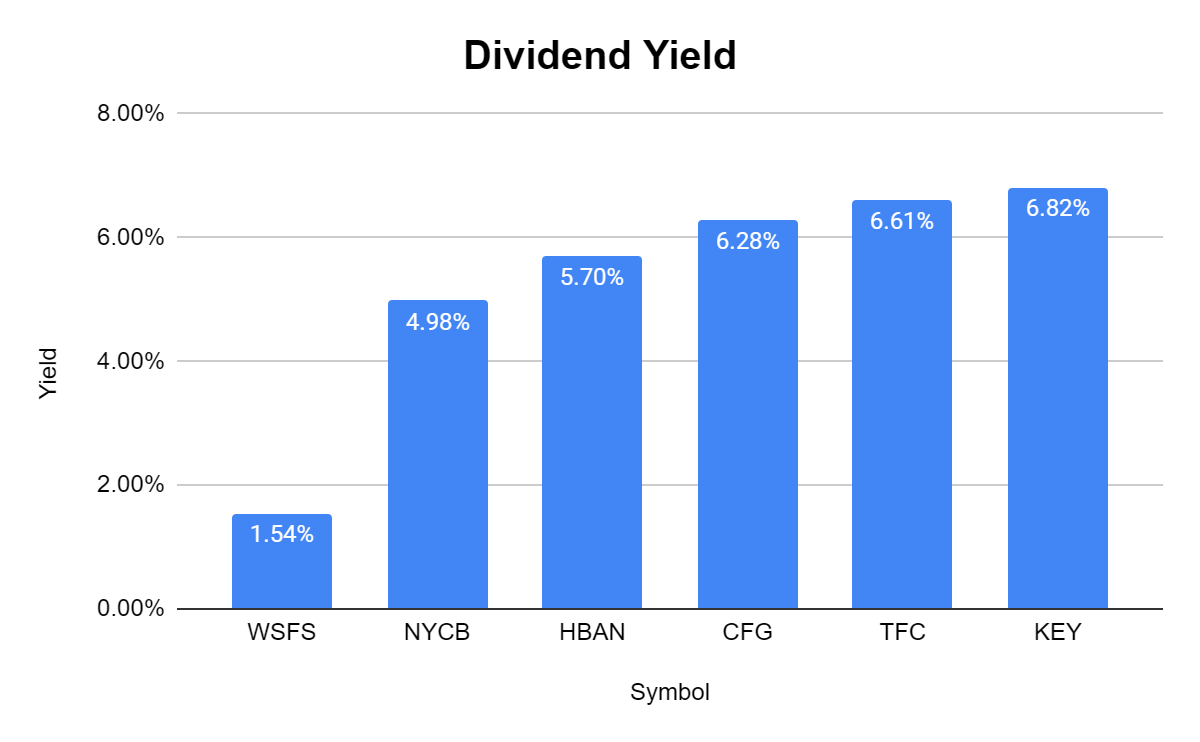

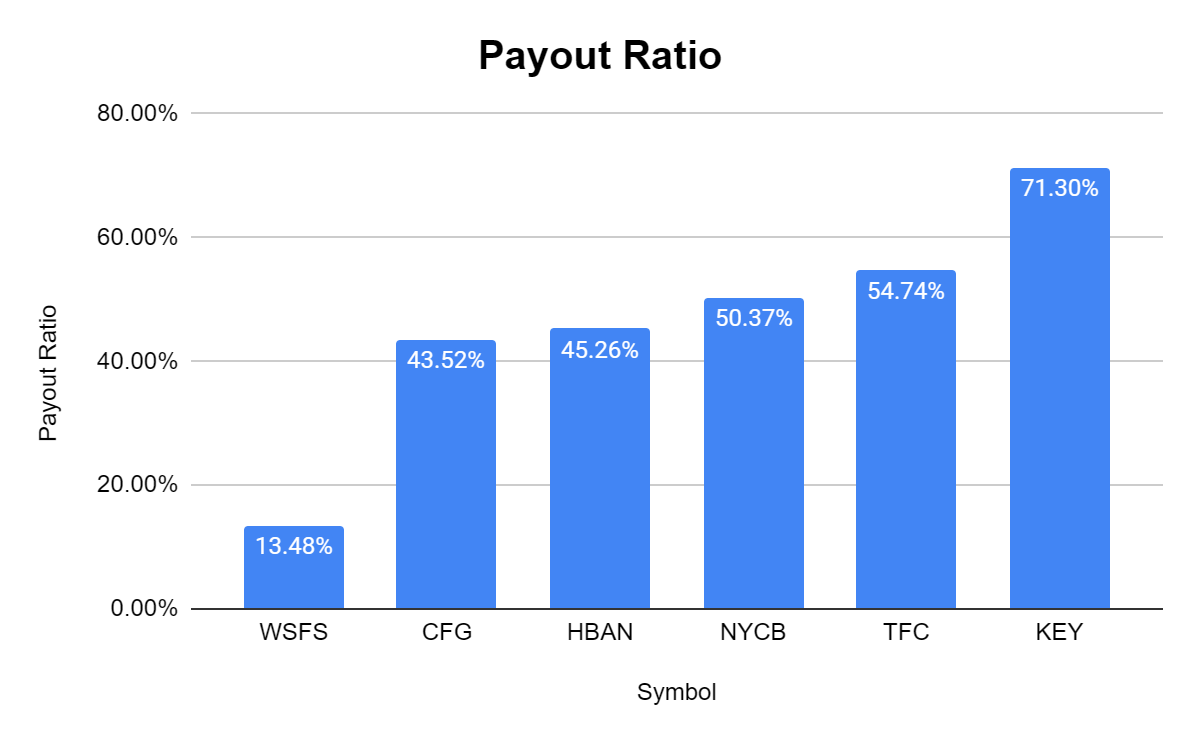

TFC continues to generate billions in profits and return a lot of capital to shareholders. Shares of TFC come with a $2.08 dividend, which is a 6.61% yield on its current share price. The dividend is also well covered, with a 54.74% payout ratio. TFC has grown the dividend for 9 consecutive years at a 6.54% growth rate over the past 5 years. This is a large reason why I am willing to allocate capital toward TFC, as the chances of a recession increase in my eyes. I can't time the markets, and I would rather invest in strong companies when there is mass fear rather than when they are rising. TFC fits within my risk profile for investments, and I am comfortable adding at these levels. I can generate a large yield while I wait for financials to return to favor and reinvest the quarterly dividends to accumulate more shares and increase my future income.

{kind=link}

Over the next 12-18 months, TFC will implement a gross cost-saving plan that will amount to $750 million in savings. This includes $300 million from reductions in force, $250 million from organizational realignment and simplification, and $200 million from technology expense reductions. TFC is also managing third-party spending and reducing its corporate real estate footprint. While they expect one-time costs to range from 25% to 30% of gross cost saves, TFC is forecasting that this will help them manage their future adjusted expense growth from 0% to 1% in 2024. The street could be spooked by TFC's guidance as their net charge-off ratio is to come in around 50 bps compared to 27 bps YoY, and their adjusted expense is to increase 7% YoY. These could impact margins a bit as revenue is only expected to grow by 1.5% YoY.

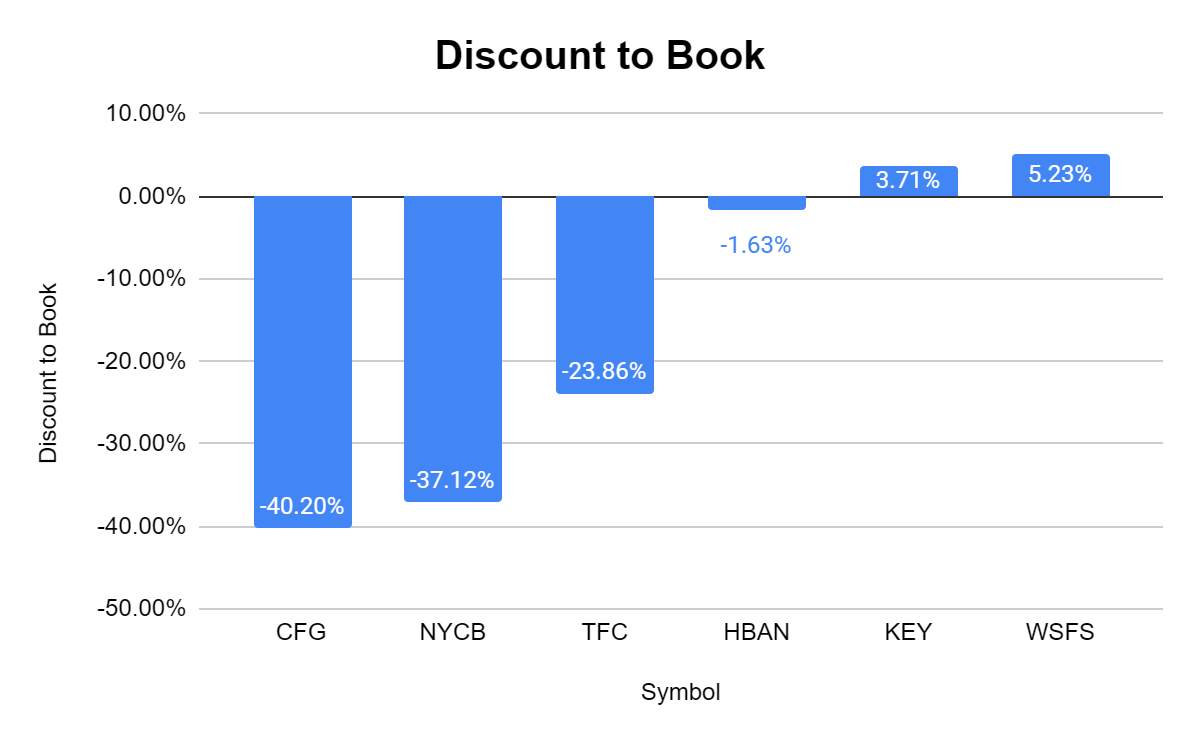

I am not necessarily worried because TFC is still a cash flow machine that is making progress on its digital initiatives. In the TTM, TFC has generated $21.9 billion in total revenue and produced $5.68 billion of net income. TFC is operating at a 25.94% profit margin and generates over $1 billion in profitability each quarter. TFC has a book value of $41.36, and shares trade at a -23.86% discount. Even if the economy slows, it won't be forever, and I think a recession will be short-lived. TFC is one of the strongest regionals in my opinion, and I think its financials are solid and there is a long-term opportunity as the market is currently discounting shares.

How TFC compares to its peers

I will compare TFC to the following banks to see how it's being valued:

- WSFS Financial Corporation ( WSFS ).

- KeyCorp ( KEY ).

- Huntington Bancshares Incorporated ( HBAN ).

- Citizens Financial Group, Inc. ( CFG ).

- New York Community Bancorp, Inc. ( NYCB ).

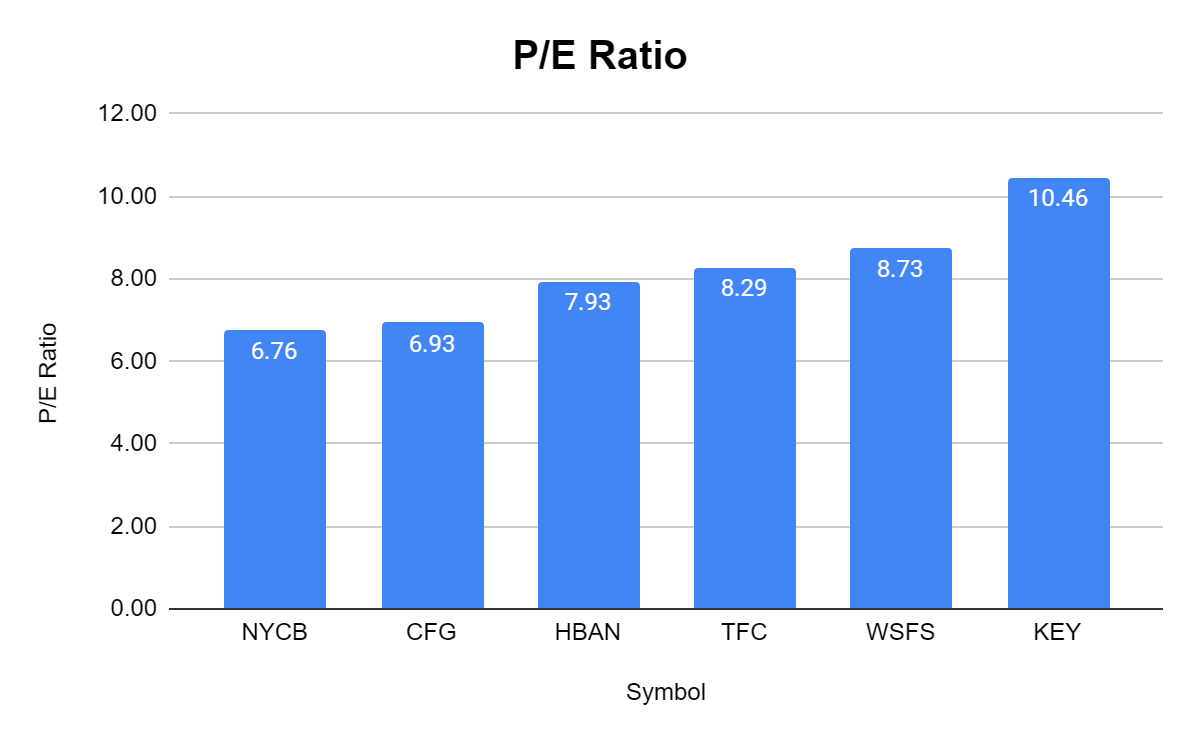

TFC is trading around the peer group average on a P/E basis. TFC has a P/E of 8.29, while the peer group average is 8.19. Financials typically trade at low P/E ratios, and I am fine paying just above the peer group average for TFC's earnings.

{kind=link}

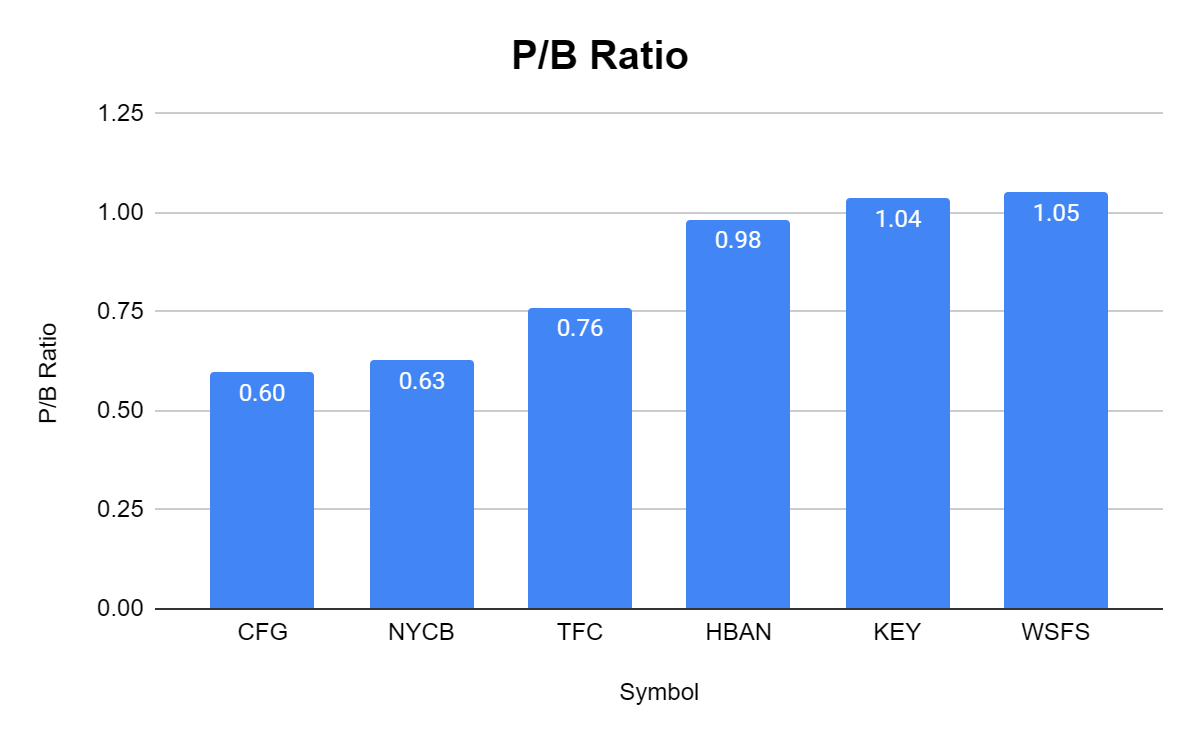

On a price-to-book ratio methodology, TFC trades at a P/B of 0.76. The peer group average is 0.84 as 4 of the 6 banks trade at a discount to book value. TFC may not be the cheapest on a P/B level, but getting shares at a -23.86% discount to book is enticing. I am more than willing to pay a discount for TFC's assets and profitability.

{kind=link}

{kind=link}

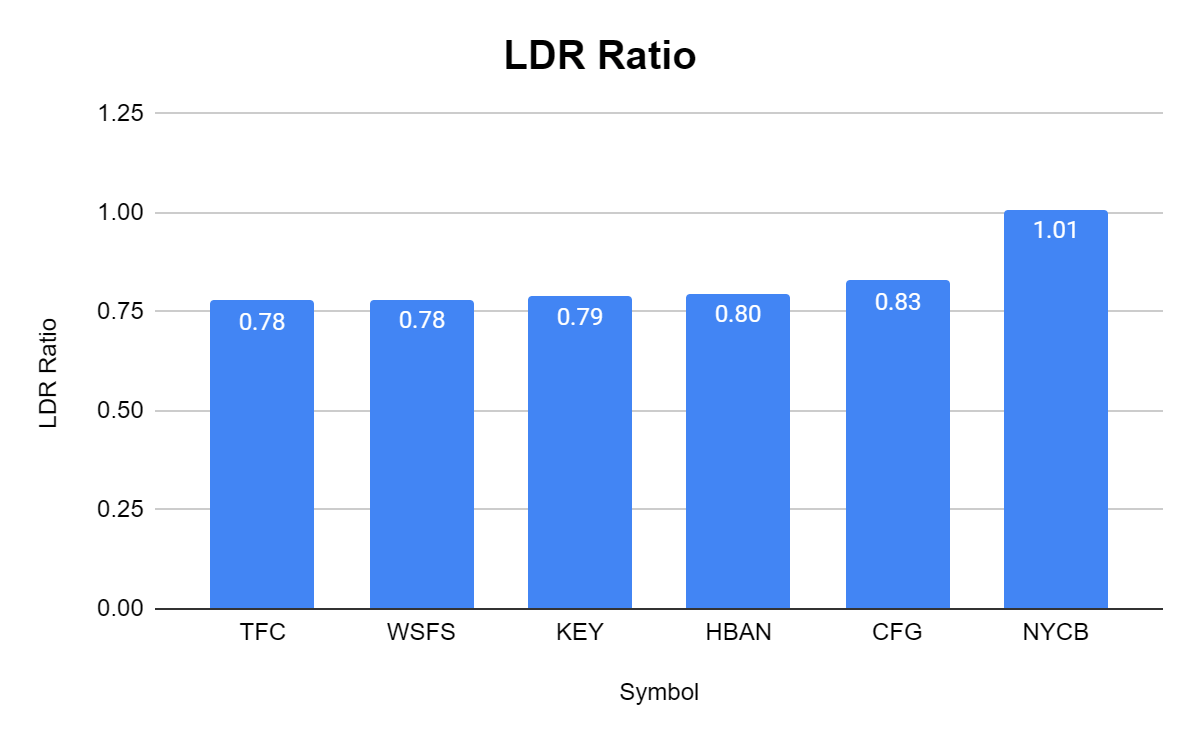

In my opinion, the loan-to-deposit ratio is one of the most important aspects of looking at a bank. I want to see that the bank hasn't over-extended itself, especially in the current macroeconomic environment. The LDR shows how much of a bank's loan portfolio is covered by the deposits on its balance sheet. TFC and WSFS have the lowest LDR ratios, which is compelling. An LDR of 0.78 is very attractive to me, and I feel much better about TFC's commitment to mitigating risk when seeing an LDR of 0.78.

{kind=link}

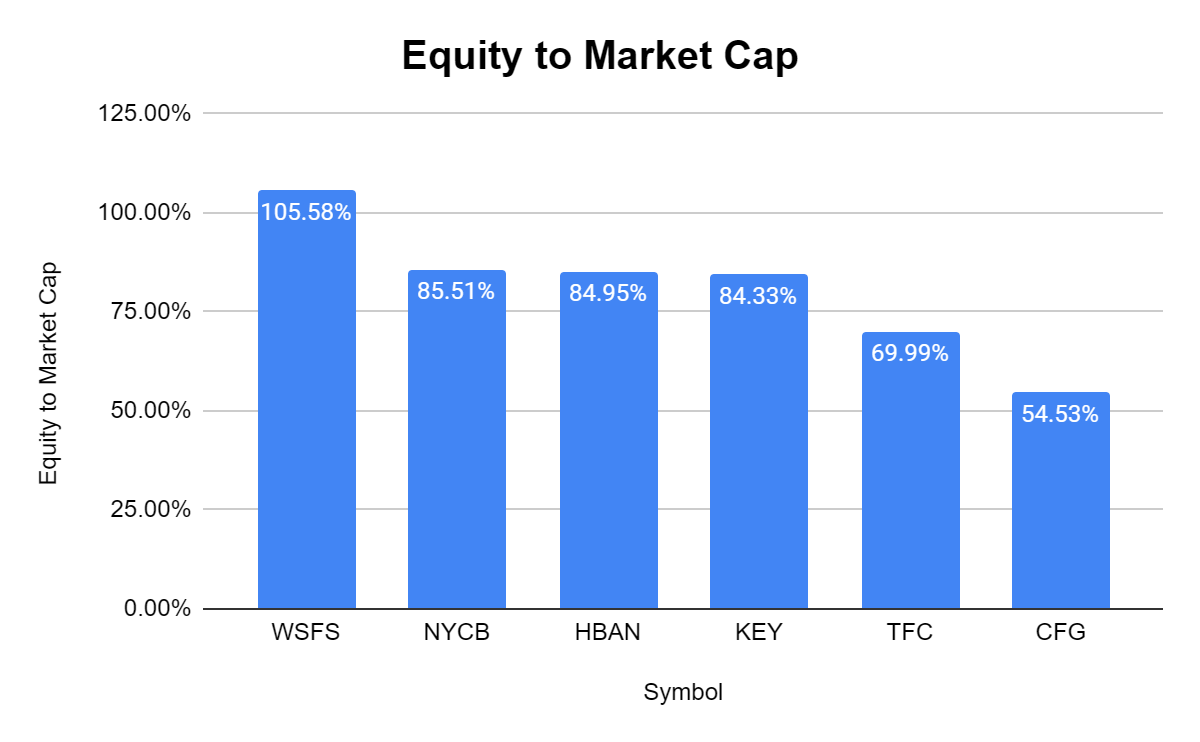

I also look at the equity to market cap ratio because I want to see if the bank's total equity on the balance sheet is trading at a discount or a premium. TFC's equity on the books is being significantly discounted as its market cap is 69.99% of its total equity.

{kind=link}

TFC is paying a $2.08 per share dividend, which has a yield of 6.61%. This is the 2nd largest yield in its peer group, as the peer group average has a dividend yield of 5.32%. TFC also has a payout ratio on its EPS of 54.74%, which is slightly above the 46.45% peer group average. The combination of a 6.61% yield with a 54.74% payout ratio is well within my parameters, and there is still significant room for future dividend growth.

{kind=link}

{kind=link}

Conclusion000

TFC is progressing on its digital transition, and its customer base is showing increased engagement. While the macroeconomic environment is a concern, how a financial institution's customer base utilizes digital offerings could be a bigger concern for the future. This is critical to retaining customers, especially when the younger generation has an increasing demand for immediate gratification for simple tasks. I think TFC has established a bottom, and while it may take some time for shares to get back to the $40s I am happy to add shares at a -23.86% discount to book and get paid a dividend that yields 6.61%. While 2024 could be a rough year, I believe TFC is one of the best-positioned regional banks for the long term, and I plan on building out my position over the next year. Financials could experience further pain, but TFC is doing all the right things to mitigate risk, as shown by their limited commercial real estate exposure and 0.78 LDR ratio. I think TFC represents an opportunity for long-term capital appreciation and income generation.

For further details see:

Truist Financial: Bargain Hunting For Value And Yield In Financial Institutions