TFC - Truist Financial Q3: Cracks Are Appearing

2023-10-23 14:30:00 ET

Summary

- Truist Financial reported better than expected earnings for Q3, but deposit trends are poor, and the credit provision situation is not great either.

- The bank saw a 30% Y/Y drop in earnings, credit provisions remained elevated.

- Truist Financial did see a small increase in average deposits in the third quarter.

- While the dividend is covered by earnings and shares trade at a large discount to BV, the decline in Q3'23 earnings and BV is not convincing.

Truist Financial ( TFC ) reported slightly better than expected earnings for the third quarter last week, but shares nonetheless dropped following the earnings release. While Truist Financial beat expectations with regard to adjusted EPS, I believe the bank's deposit and credit provision trends are not great and investors have better regional banks to choose from. The 7.7% yield is supported by the bank's earnings, but risks are growing, in my opinion. Therefore, despite a large 34% discount to book value, I believe investors may want to continue to stay on the sidelines as the third quarter earnings report was not very convincing!

Previous Rating

I rated Truist Financial stock a hold after Q2'23 due to the bank faring not especially great in the Fed's latest stress test and because the deposit situation following the regional banking crisis in the first quarter was concerning. Deposit headwinds persisted in the third quarter and the bank reported an earnings decline, in part due to higher credit provisions (reflecting worsening quality of the loan portfolio). I believe that the risk profile is not favorable, but the 7.7% yield should be sustainable. If it weren't for the 7.7% dividend yield and high discount to book value, I would likely rate Truist Financial a sell.

Earnings performance and credit provisions

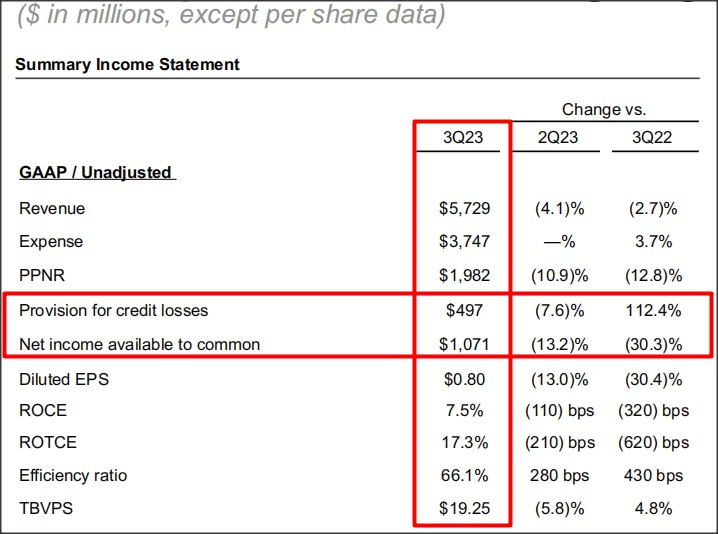

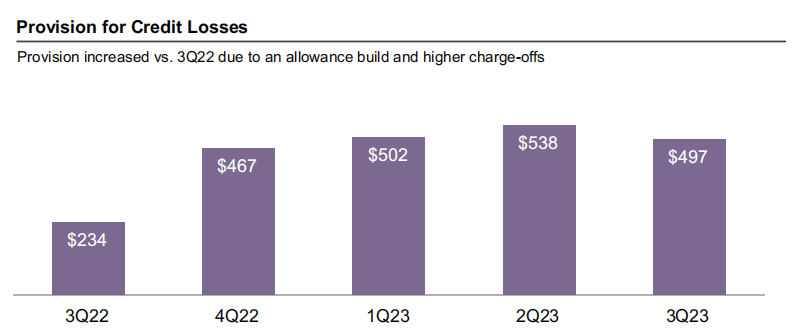

It was not a great quarter for Truist Financial: the bank reported a massive 30% decline in earnings, lower revenues Q/Q, and elevated credit provisions. Truist Financial disclosed $1.07B in earnings for the third quarter, showing a steep year-over-year decline and higher expenses as well as a drastic year-over-year increase in credit provisions which are to blame for the significant drop in earnings. The lender did confirm that it continues to plan with a $750M cost reduction program, including tech optimization and personnel cuts, but unless earnings growth resumes and credit provisions decline significantly, I don't see any catalyst for the gap between the bank's book value and its share price to diminish.

{kind=link}

A look at Truist Financial's credit provision trend

It was not the first quarter of significant credit loss provisions for Truist Financial. Provisions have been elevated since the fourth quarter of FY 2022 and although Truist Financial's credit provisions fell $41M in the third quarter, Q/Q, they nonetheless remained elevated over the year-earlier period... which indicates growing problems with asset quality. With $497M in credit provisions in Q3'23, Truist Financial's credit quality is now a drag on the bank's earnings.

{kind=link}

Deposit situation

Truist Financial's deposit situation continued to disappoint in the third quarter as well. The financial institution reported $401B in average deposits at the end of the third- quarter, showing a 0.3% increase quarter-over-quarter. For comparison, Western Alliance Bancorporation ( WAL ) saw a 6.4% quarter-over-quarter increase in period-ending deposits. Truist Financial also saw a strong uptick in its deposit costs, as expected, in the third quarter to 1.81% which is weighing on profitability as well.

Source: Truist Financial

One good thing about Truist Financial

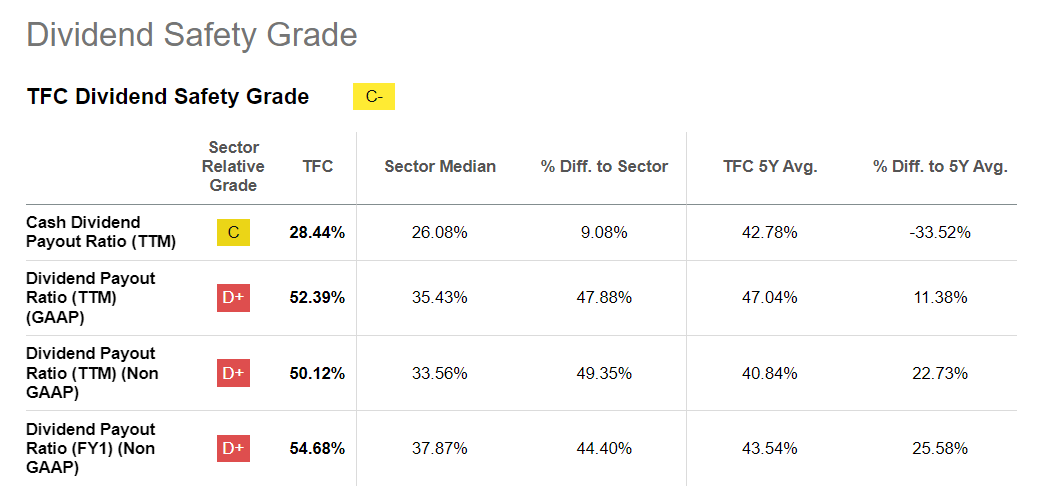

Truist Financial pays a 7.7% yield which results in TFC ranking at the near top of its industry group. Only KeyCorp ( KEY ) currently has a higher dividend yield with an 8.3% yield.

However, Truist Financial covers its dividend payout with earnings and the bank has had an LTM payout ratio of about 52%. Although the payout ratio is higher than the industry median (35%), the dividend is well-supported and I expect Truist Financial will keep paying its dividend.

{kind=link}

Truist Financial's valuation reflects concerns over business trajectory

Truist Financial trades at a very large discount to a book value which, in my opinion, results from the bank's underwhelming performance in deposits and loan quality/credit provisions. The large 34% discount to book value might actually turn out to be a trap if Truist Financial's loan portfolio degrades in quality heading into a recession.

Higher credit provisions have not only resulted in declining earnings, but also in a drop-off in book value in the third quarter. Truist Financial's tangible book value skidded from $20.44 per share to $19.25 per share, showing a total decline of 5.8%. For comparison, Western Alliance's tangible book value per share increased 1.3% to $43.66 per share.

The large discount to book value relative to other regional banking rivals as well as the high yield of 7.7% indicate higher-than-average risks. The large discount also reflects concerns about Truist Financial's credit quality as well as declining book value.

Risks with Truist Financial

Given the rather steep increase in credit provisions, I am starting to be concerned about the regional banks' balance sheet and asset quality. The Q3'23 decline in earnings and book value is also a potentially troubling sign and a recession would likely see an even larger jump in credit provisions... resulting in growing pressure on the bank's earnings trajectory and tangible book value.

Closing thoughts

I am actually leaning towards rating Truist Financial a sell, but I am refraining from it because the regional bank's earnings still cover the 7.7% dividend yield and shares trade at a large discount to book value. But cracks are emerging in the investment thesis: the lender is not making a strong case for itself by reporting elevated credit provisions and a steep drop-off in earnings. A recession would make the asset quality situation undoubtedly a lot worse, in my opinion. Although shares of Truist Financial sell at a large discount to book value and thereby reflect problematic loan and asset quality trends, I believe Truist Financial is not a great buy. Western Alliance produced a much better earnings sheet for the third quarter and the regional bank's deposits are growing and the book value is growing!

For further details see:

Truist Financial Q3: Cracks Are Appearing