HBANM - Truist Financial's 7% Yield - A Table-Pounding Buy

2023-05-08 06:30:00 ET

Summary

- The banking crisis is doing a number on regional bank stocks, causing a sell-off of more than 30% since the start of this year.

- Truist Financial's stock price is among the victims, although its business remains in great shape.

- Not only does TFC have a 7% yield, but it also comes with a strong business, steady deposits, satisfying loan quality, and an attractive valuation.

Introduction

I'm not mentioning anything new when I say that banking stocks are in a tough place. The regional banking ETF ( KRE ) has lost a third of its value since the start of this year, making it the worst sell-off since the pandemic hit the markets in 2020.

While this sell-off isn't fun for existing positions like my investment in Huntington Bancshares ( HBAN ), which I bought dirt-cheap in 2020, it's one of the many opportunities to add high-quality regional banks - if that's what investors are looking for.

I have often made the case that there is no need to own regional banks. Investors can get good yields in other areas. Buying regional banks is a bit like picking up pennies in front of a steam roller: regional banks tend to sell off rather violently every time the economy enters a recession.

The good news is that the market tends to throw out the baby with the bathwater, which opens up new opportunities for income-seeking investors looking for undervalued banking exposure.

Hence, in this article, I'm focusing on Truist Financial Corp. ( TFC ) , one of the best regional banks on the market. While its stock price is suffering, its core business remains strong. Given its yield and its valuation, I believe that TFC is one of the banks that warrants new investments in times of distress.

Zero Confidence

I bought Huntington Bancshares, my only bank holding, in 2020, close to $9 per share. I had always planned to take advantage of market downturns to acquire additional shares in case of a recession. However, I did not anticipate having the opportunity to purchase more shares at the same price point again.

As perfectly summarized by the Wall Street Journal , banks are in the grips of investor confidence, which has completely evaporated.

{kind=link}

Wall Street Journal

Essentially, the recent decline in the stock prices of US regional banks has raised concerns over the soundness of the banking system. The crisis began to gain momentum with the seizure and sale of First Republic Bank to JPMorgan ( JPM ), which was expected to be a cathartic moment for American banks, signaling the end of the latest crisis of confidence in the financial system. However, the relief was short-lived, with shares of regional banks plummeting and the KBW Nasdaq Regional Banking Index dropping 15% from the prior week at one point.

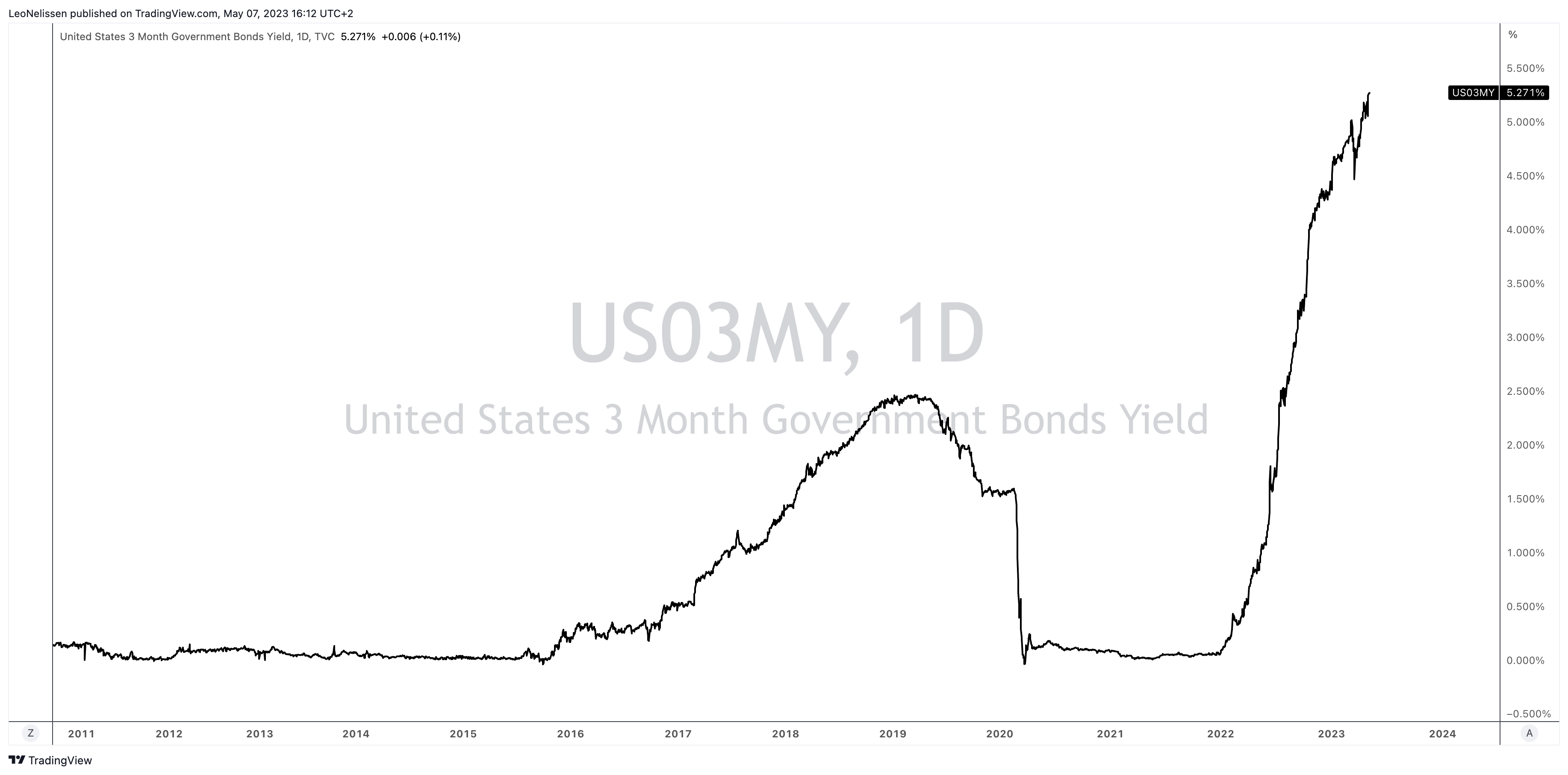

The problem is a mix of headwinds, including an aggressive hiking cycle, which has raised the yields of short-term bonds to levels that make it unattractive to leave money at the bank.

The 3-month annualized treasury yield is now at 5.3%.

{kind=link}

TradingView (US 3M Yield)

This was also noted by the aforementioned WSJ article, which makes the case that the optimism about the recovery of banks' portfolios does not account for the inherent fragility of deposits. If a bank, such as Silicon Valley Bank or First Republic, can face a lethal tidal wave of withdrawals from accounts that lack deposit insurance, it can quickly become a dangerous trend.

Controlling the vicious cycle that follows can be a challenging task. Investors are concerned about banks for several reasons, including the tendency of vehicles like money-market funds to transfer high-interest rates to customers, as well as the regulatory reforms enacted after the 2008 financial crisis that primarily targeted the risk of megabank failures, making other banks appear weaker by comparison.

In this case, it also doesn't help that the banks that got into trouble were horribly mismanaged, which was highlighted by Warren Buffett :

Buffett pointed to First Republic Bank, the beleaguered lender which JPMorgan Chase & Co. just rescued. First Republic’s filings showed the lender was offering jumbo, non-government-backed mortgages at fixed rates that were interest-only for 10 years in some cases — which Buffett called “a crazy proposition.”

That said, I do believe that strong banks offer opportunities, although I do not expect a sudden and steep recovery. The Fed is forced to keep rates high, which will continue to weigh on deposits. Even if the market calms down, I would not make banks a high-conviction investment.

Based on this context, North Carolina-based Truist Financial is on my watchlist, as I believe it's a no-nonsense bank with good management and the ability to deliver tremendous long-term shareholder value - especially given the current sell-off.

Truist Financial Remains Rock-Solid

With a market cap of roughly $35 billion, Truist Financial is America's third-largest regional bank. The company has more than $570 billion in assets, more than 2,100 branches, more than 50,000 employees, and 15 million clients in the Midwest, Northeast, and South.

{kind=link}

Truist Financial Corp.

While the company's stock price has suffered, it seems to be a case of a falling tide that sinks all ships.

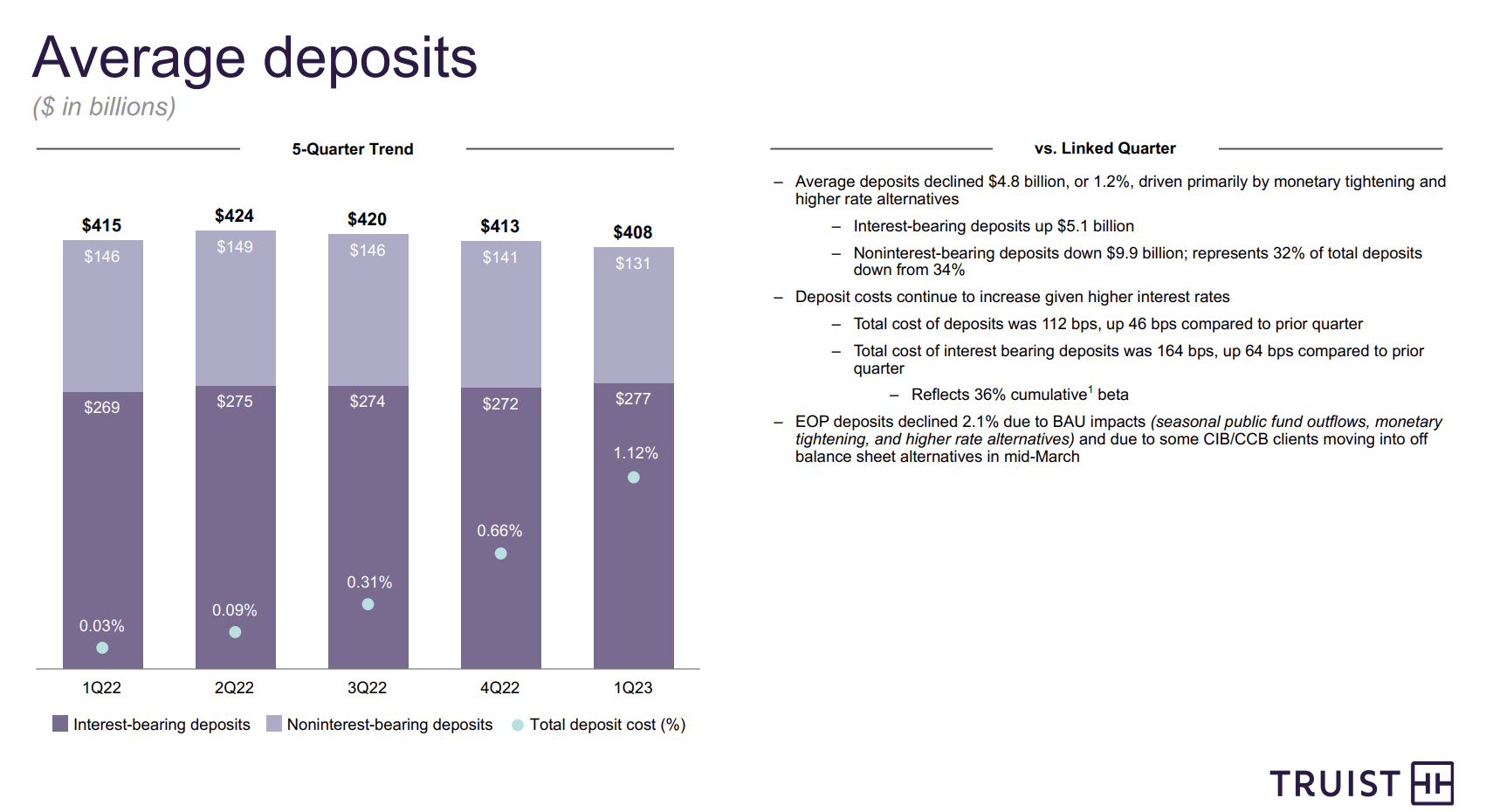

The fact is that Truist has done very well. As reported by Bloomberg , regional banks such as Truist Financial Corp., Fifth Third Bancorp ( FITB ), and Huntington Bancshares reported steady deposits during the first quarter of this year despite the impact of the collapse of three lenders in March.

Truist's deposits were recorded at $408 billion as of March 31, which is slightly lower than the predicted $411 billion by analysts tracked by Bloomberg.

{kind=link}

Truist Financial Corp.

However, this is stable and not at all indicative of trouble.

“In a challenging and unique quarter for the banking industry, Truist demonstrated strength,” Truist Chief Executive Officer Bill Rogers said in the statement.

Bloomberg

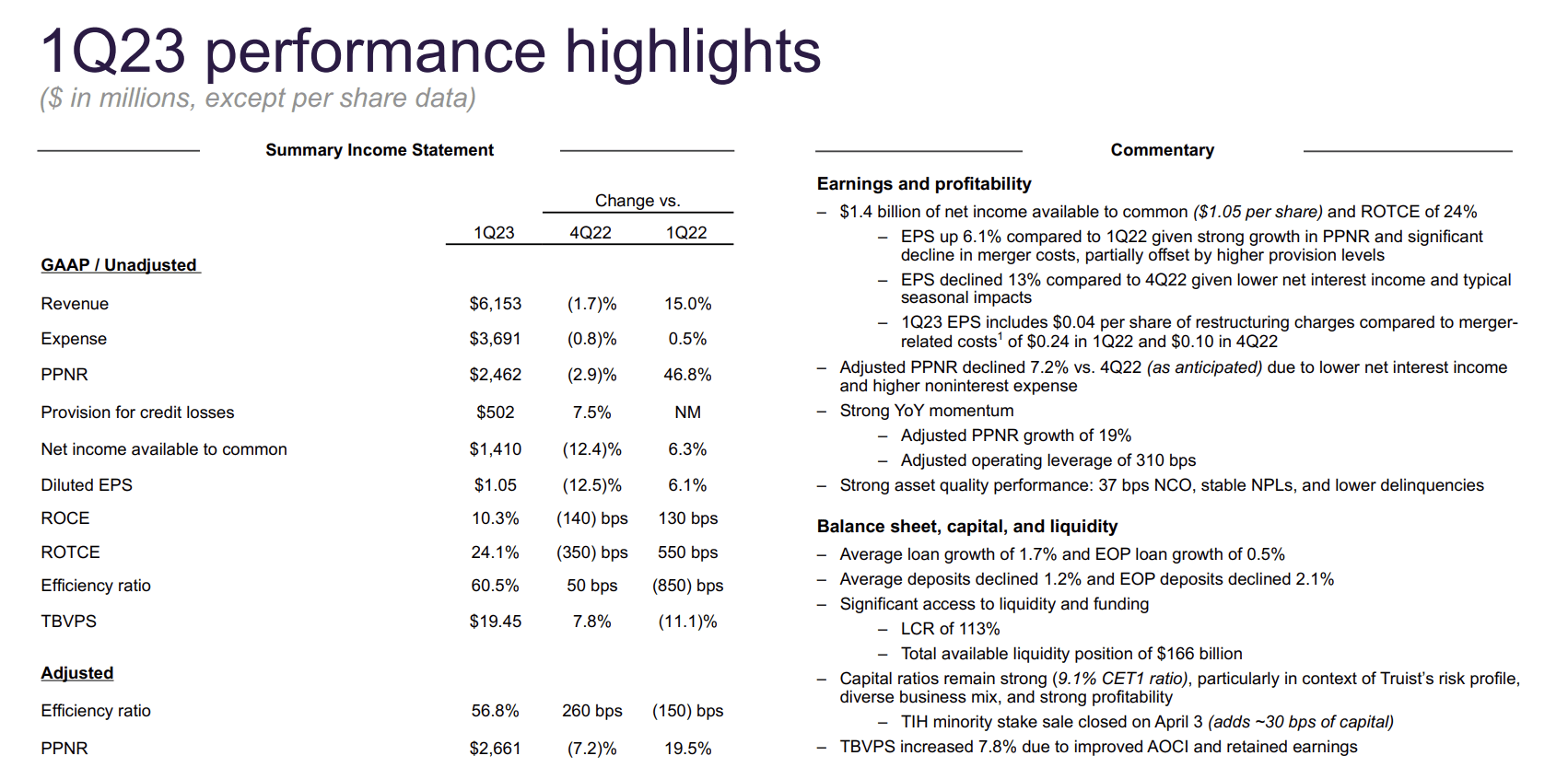

In the first quarter, Truist reported a 6% increase in net income year on year, but EPS decreased 13% quarter on quarter, primarily due to lower net interest income and seasonality. Adjusted PPNR (pre-provision net revenue) decreased 7% sequentially due to lower net interest income and somewhat higher than expected expenses, but relative to 1Q22, adjusted PPNR grew 19%.

{kind=link}

Truist Financial Corp.

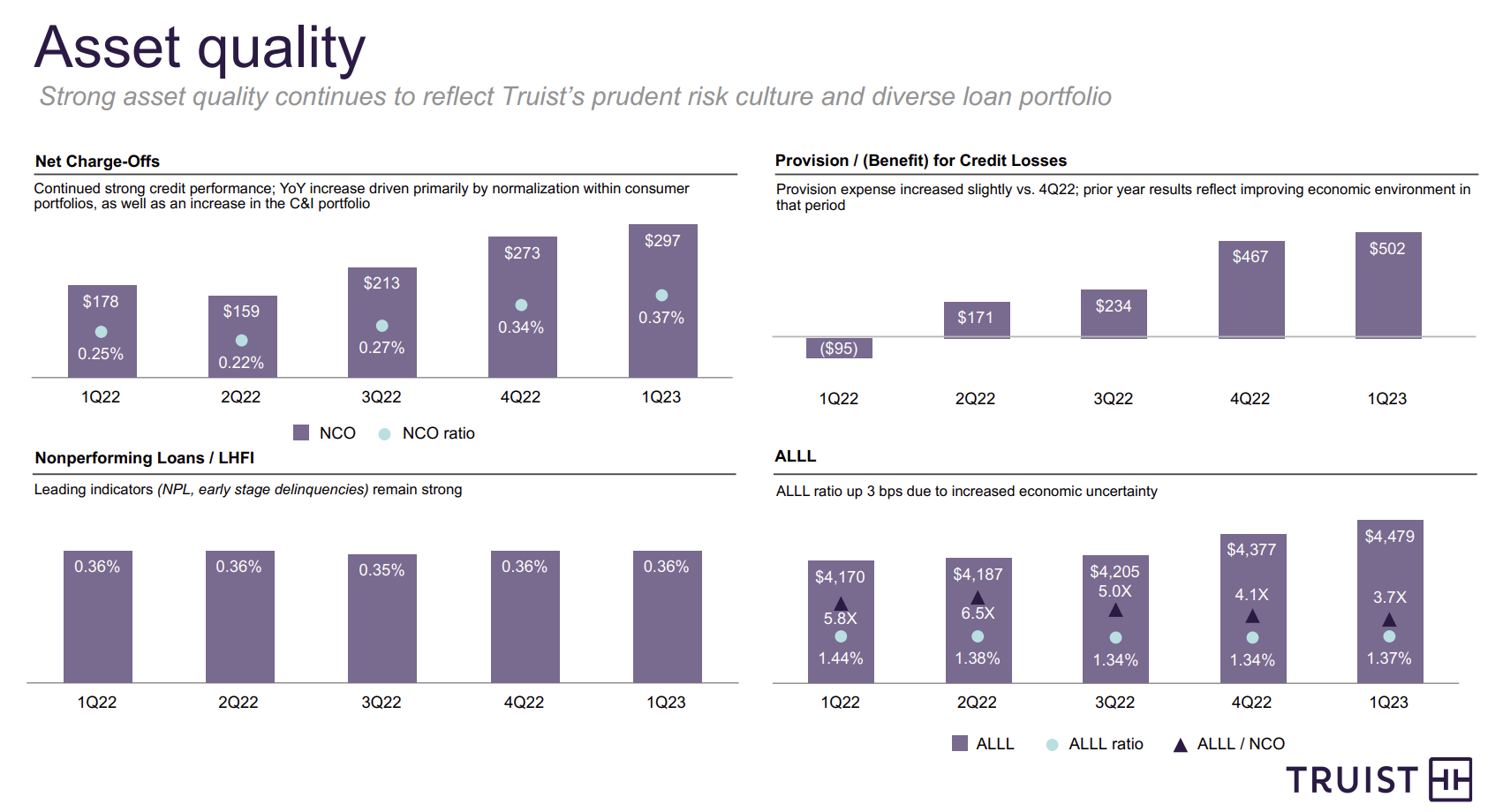

Furthermore, asset quality remained strong, and net charge-offs continued to normalize. The bank's ALLL (allowance for loan and lease losses) ratio was increased by three basis points to reflect a more uncertain economic environment. While it makes sense to incorporate higher economic uncertainty, there is no evidence that loan quality is in a bad spot. Nonperforming loans remain subdued at 0.36% of total loans held for investment.

{kind=link}

Truist Financial Corp.

Moreover, the company became even more cautious in its outlook regarding CRE (commercial real estate) fundamentals and is tightening credit and reducing its risk appetite in selected areas while maintaining its through-the-cycle approach in anticipation of an increasing risk environment.

On a side note, if you want to know more about commercial real estate risks, feel free to read the article I wrote on this last month.

Furthermore, with regard to CRE, the company reported a 2.2% decrease in its CRE portfolio from 2019 to 2022 due to its focus on diversification and disciplined risk management. The company carefully evaluated its various portfolios during the integration process to become Truist to ensure it understood the combined risk profile and to establish how it would manage them going forward.

Truist's disciplined approach to CRE is reflected in its asset quality metrics, which remain solid, and it maintains a high-quality CRE portfolio through prudent client selection. The office segment accounted for 1.6% of Truist's loan book, which tends to be weighted towards Class A properties within its footprint. The company's exposure tends to be large CRE with strong institutional sponsorship, and it has reduced its exposure to smaller CRE.

{kind=link}

Truist Financial Corp.

Furthermore, the company's own CET1 ratio improved to 9.1%, as the company maintains a satisfying capital position.

What About The Dividend & Valuation?

Truist pays a $0.52 per share per quarter dividend. This translates to $2.08 per year. The dividend yield is 7.2%.

On July 26, management hiked this dividend by 8.3% from $0.48.

The dividend has a payout ratio of 45%, which is safe but a bit above the sector median of 34%.

During its earnings call , management briefly commented on its dividend after it was asked what its plans were for dividend growth (emphasis added):

[...] we're in a capital build mode right now until we're not. So we want to really understand the landscape, understand the regulatory landscape, be prepared. We've got 20 basis points or so of sort of organic capital accretion that comes into play. That's post our dividend. Our dividend will continue to be important to us, and we'll continue to support our dividend .

While it's hard to estimate what dividend growth will look like this year, the fact that TFC is yielding more than 7% makes the risk/reward very attractive. I do not anticipate a dividend cut unless the economy implodes, similar to what we witnessed during the Great Financial Crisis.

Not only is its 7.2% yield attractive, but the company is also trading at an attractive price.

The company is trading at 1.7x its tangible book value, which is the lowest valuation since the early pandemic recovery and the 2016 manufacturing recession lows.

While none of this guarantees that TFC is bottoming (the market can stay irrational longer than reckless investors can stay liquid), we are dealing with a good risk/reward - I think.

The consensus price target is $42. The most recent analyst ratings were all upgrades, with price targets between $45 and $53.

FINVIZ

Especially when the economy starts to grow again, I am sure that TFC will work its way up to new highs.

Nonetheless, investors interested in buying TFC need to be careful. If I were adding banking exposure (besides expanding my HBAN position), I would be a gradual buyer. If the stock falls further, I would be able to average down. If the stock were to suddenly take off, I would have my foot in the door.

Takeaway

In this article, we discussed the banking crisis and one of the best regional banks on the market. While TFC is being pressured by high short-term rates and a rapid decline in confidence, its business continues to do well. It has minimal exposure to commercial real estate, its deposits remain strong, and its loan quality remains highly satisfactory.

While uncertainty continues to hold a tight grip on the market, I believe that TFC is offering tremendous long-term potential. It has a juicy 7% dividend yield, an attractive valuation, and a business model that makes a quick recovery likely the moment economic demand bottoms.

Needless to say, as the economy is not out of the woods yet, investors need to remain careful when dealing with banks.

For further details see:

Truist Financial's 7% Yield - A Table-Pounding Buy