TFC - Truist Financial Stock: Downgraded To Hold Despite Powell Pivot

2023-12-19 11:30:54 ET

Summary

- Truist Financial stock has rallied 30% in just two months, largely due to recently emerged rate cut fantasies.

- In this update, I share my thoughts on the latest trends in deposits, loans and credit quality.

- I provide an update on Truist's HTM securities portfolio and explain what to make of the unrealized loss, which recently reached a new high ($12.4 billion, 36% of tangible equity).

- I also explain why I have downgraded TFC stock to "hold" and decided not to lock in profits.

Introduction

I turned bullish on Truist Financial Corporation (TFC) stock in mid-March, shortly after the collapse of Silicon Valley Bank (SIVBQ) marked the beginning of a new crisis in the banking sector. I thought the fears regarding the bank's comparatively large unrealized losses in its held-to-maturity ((HTM)) securities portfolio were largely unfounded, especially in light of the Bank Term Funding Program ((BTFP)) and the bank's size ( currently ranked 8th in terms of total assets), which makes it one of the comparatively more trustworthy among depositors. Because of this and the still largely unrealized merger synergies (recall the BB&T/SunTrust merger in late 2019) and the associated uncertainty, I considered TFC stock to be one of the best bets in this sector from a risk/reward perspective.

However, as the year progressed, I had to realize that Truist's management apparently has issues delivering on its efficiency targets. Considering that BB&T and SunTrust merged four years ago, and although I acknowledge that the consolidation works took place at an unfortunate time (in the middle of the pandemic), the result is disappointing. However, having worked in the banking sector myself, I know how complex mergers can be, and so I remained patient , also considering that higher interest rates (and hence still high unrealized losses) weighed on sentiment.

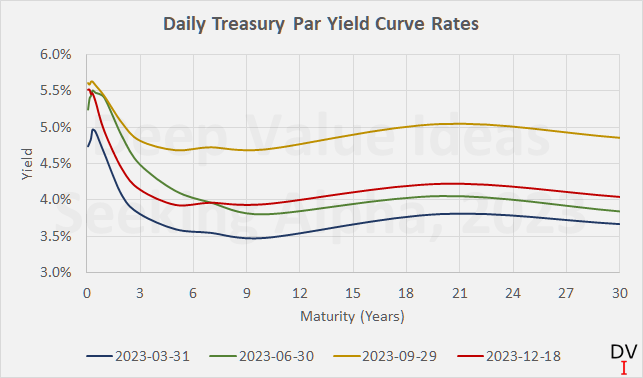

With the Federal Reserve having signaled the end of its latest rate hike cycle, long-term interest rates have fallen significantly (Figure 1), and with them discount rates on future earnings, as well as fears related to the unrealized losses on Truist's balance sheet . All else being equal, the Fed's expected policy change should result in fewer bankruptcies due to cheaper refinancing and also to an uptick in mortgage lending (the 30-year mortgage rate has declined 80 basis points from its October peak). But, of course, it's important to keep in mind the prime reason for rate cuts - to stimulate economic growth in a downturn.

Figure 1: Daily Treasury par yield curve rates from March 31, June 30, September 29, and December 18, 2023 (own work, based on data from home.treasury.gov)

{kind=link}

Taken together, it is, therefore, no wonder that sentiment for bank stocks has improved. Truist shares have risen by 30% since my last article - in just two months. I think it's worth examining the reasons for the rally and whether the gains are justified. In this article, alongside an updated valuation, I share my thoughts on the latest trends in deposits, loans and credit quality. And while the unrealized losses in banks' securities portfolios are no longer a frequent topic of discussion, I still think it's worth taking a fresh look at Truist's HTM portfolio and the (still high) utilization of the BTFP.

An Update On Truist's Deposits And Its HTM Securities Portfolio

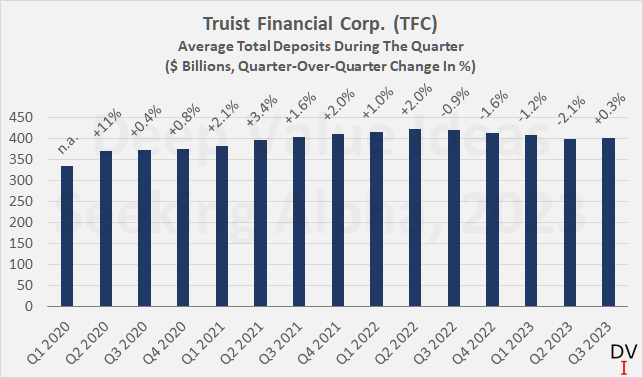

As mentioned in my last article, Truist deposits continued to decrease in the second quarter of 2023 , with the decline accelerating sequentially. However, the trend reversed in the third quarter and the level of deposits stabilized (Figure 2). I would attribute only a small part of the decline in 2023 to actual, fear-induced deposit flight. It is worth remembering that the Federal Reserve has been aggressively raising interest rates since early 2022. As a result, depositors have been increasingly looking for a better deal, but I think it can be argued that Truist maintains a solid deposit base even against this backdrop. Obviously, Truist is giving depositors a good deal on their savings, but as one of the largest banks in the U.S., it can actually afford to pay a little less than its - likely perceived less trustworthy - smaller competitors. In any case, it was reassuring to see that the sequential decline did not accelerate further in the second quarter of 2023 and that average deposits in the third quarter were actually slightly higher than in the previous quarter.

Figure 2: Truist Financial Corporation (TFC): Average total deposits during the quarter (own work, based on company filings)

{kind=link}

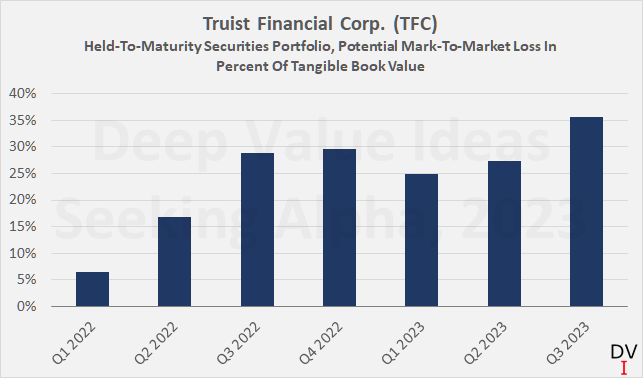

In addition to the development of deposits, it is worth taking a fresh look at the value of Truist's HTM securities portfolio and putting it in proper perspective. After all, a forced sale of the portfolio's assets would trigger a significant mark-to-market loss, which in turn would put severe pressure on the company's capitalization (Figure 3). Although the potential loss in market value has reached a new high in both absolute ($12.4 billion) and relative terms (36% of tangible book value) due to the rise in long-term interest rates going into the fourth quarter, the market no longer appears to be concerned (or at least less concerned than at the beginning of the year). I believe this is due to the fact that the market no longer expects the Fed to keep interest rates at current levels through 2024 and, therefore, also expects a reduction in the unrealized losses in Truist's HTM securities portfolio (lower rates result in an appreciation of high duration assets).

Figure 3: Truist Financial Corporation (TFC): Impact of the sale of all HTM assets on tangible equity (own work, based on company filings)

{kind=link}

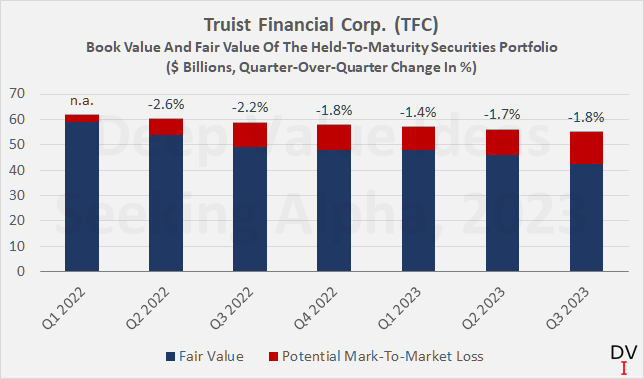

The value of the entire portfolio (excluding the potential loss) has fallen steadily over the last two years - from $61.7 billion at the end of the first quarter of 2022 to $54.9 billion at the end of the third quarter of 2023 (-11%, Figure 4). This is an indication that Truist is not replacing securities that have matured off the balance sheet. And indeed, the bank's most recent cash flow statement shows that no securities were purchased for the HTM portfolio in the first nine months of 2023. However, Truist did purchase $2.3 billion worth of available-for-sale ((AFS)) securities that could be transferred to the HTM portfolio at some point ( see this article ). However, these purchases were more than offset by maturities, calls and paydowns of AFS securities ($6.3 billion).

Figure 4: Truist Financial Corporation (TFC): Book value of the HTM assets and potential mark-to-market loss at quarter end (own work, based on company filings)

{kind=link}

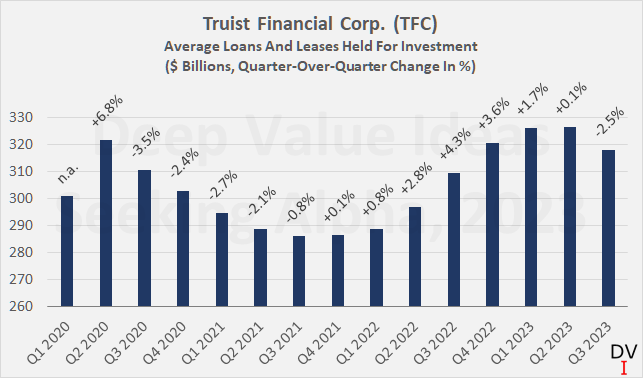

Overall, Truist's investment portfolios shrank over the course of 2023 (not only due to lower valuation), and the bank also recorded a slight decline in its loan and leases portfolio in the third quarter (Figure 5) - a feeble sign of a slowdown in economic activity.

Figure 5: Truist Financial Corporation (TFC): Average loans and leases held for investment during the quarter (own work, based on company filings)

{kind=link}

A Fresh Look At the Utilization Of The BTFP

As a quick response to the collapse of Silicon Valley Bank in March 2023, the Federal Reserve announced the Bank Term Funding Program, which grants short-term loans to banks and other financial institutions. It is important to note that the assets deposited as collateral (e.g., currently underwater government bonds) are valued at par. With this program, the Federal Reserve has acted wisely by boosting depositor confidence (and thus reducing the risk of further bank runs) by offering a form of emergency liquidity to banks with significant unrealized losses in their held-to-maturity portfolios.

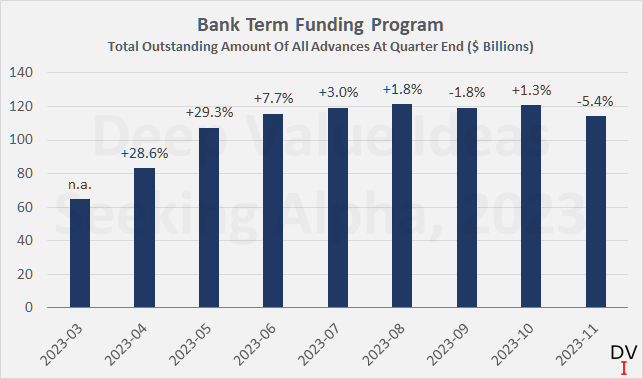

The topic is no longer frequently covered, but as it is still relevant (see above), I continue to monitor the drawdown of the BTFP very closely as I consider it a direct indicator of the overall situation. The Federal Reserve publishes the utilization of the BTFP on a monthly basis (Figure 6).

Figure 6: Bank Term Funding Program: Total outstanding amount of all advances at quarter end (own work, based on data from federalreserve.gov)

{kind=link}

While the recent decline (-5.4%) is reassuring, the still high utilization is a cause for concern. However, it should be borne in mind that interest rates are still comparatively high and high duration bonds have the highest unrealized losses. Naturally, they will take the longest to mature off the balance sheet. At the same time, investors should appreciate the fact that banks are currently able to improve their portfolio yield by reinvesting the proceeds from maturities. Of course, this means that refinancing costs have also risen, but banks generally - and quite obviously - operate more profitably above a certain interest rate threshold. Time heals all wounds in the truest sense of the word - including those inflicted by the zero interest rate environment and the subsequent rate hike cycle.

Was The Rally Justified? - And An Updated Valuation Of TFC Stock

I admit that selling a position for a quick 30% gain is tempting, knowing that it will probably only take a rebound in the rate of inflation, some hawkish statements from the Federal Reserve, and consequently a weak bid for long-term Treasuries for bank stocks like Truist to change course.

However, I did not buy my position in Truist (and U.S. Bancorp (USB) for that matter) to speculate on a short-term rally. I consider both to be solid banks that have been largely unjustly punished for their large unrealized losses in their HTM portfolios. Truist is certainly weaker due to still prevalent profitability concerns, but, therefore, has more upside potential if management is finally able to deliver on its targets.

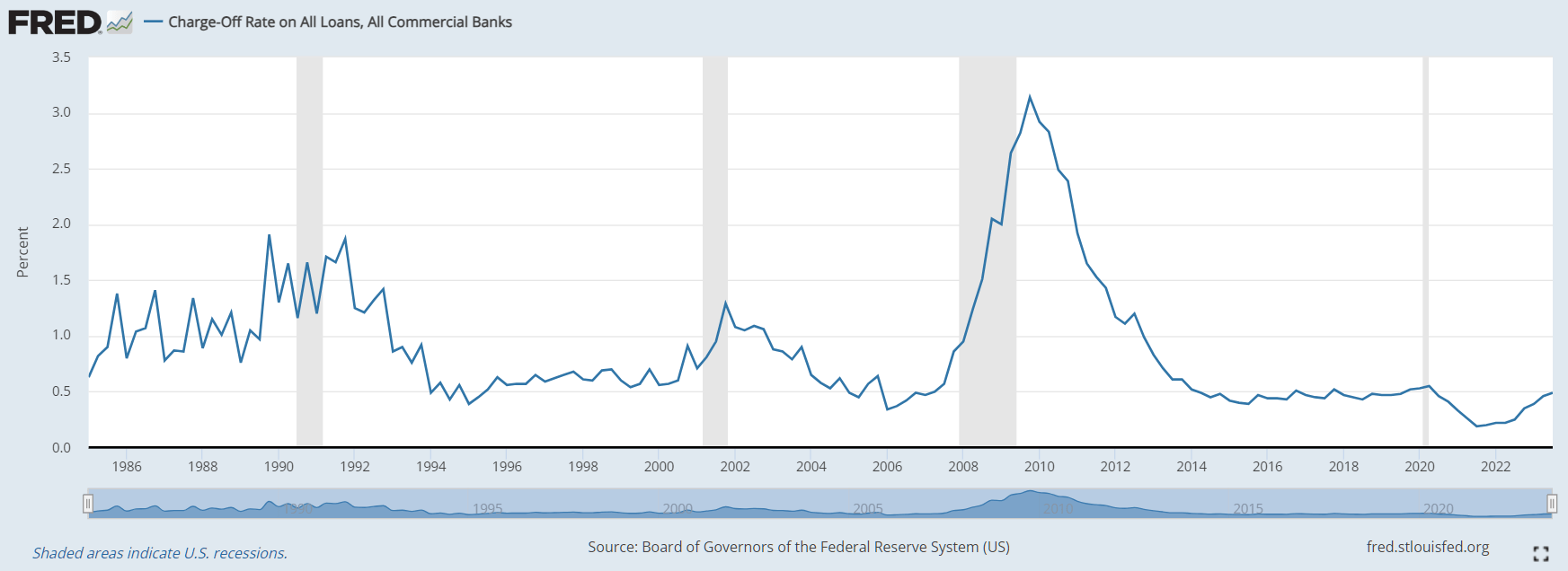

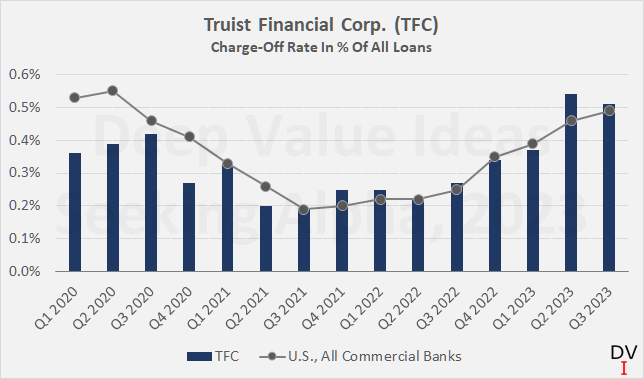

In my view, Truist stock rallied largely on rate cut fantasies - as underlined by the fact that the rebound was not bank-specific. It should also be borne in mind that lower expected long-term rates lead to an increase in the time value of money and thus to multiple expansion. A cut in the Fed Funds Rate would eventually lead to a normalization of the shape of the still inverted yield curve (recall Figure 1), improving banks' ability to engage in maturity transformation ( explanation here ). At the same time, lower interest rates mean better refinancing conditions for borrowers and thus lower charge-offs. In this context, however, it is important to note that charge-offs are still extremely low by historical comparison (Figure 7), so a recession would certainly lead to a sharp increase and thus temporarily weaker bank earnings. Nonetheless, Truist's latest figure - 0.51% of average loans and leases, down 3 bps sequentially (Figure 8) - was definitely encouraging to see.

Figure 7: Charge-off rate on all loans - CORALACBN - Board of Governors of the Federal Reserve System (U.S.) (retrieved from FRED, Federal Reserve Bank of St. Louis) Figure 8: Truist Financial Corp. (TFC): Charge-off rate as a percentage of all loans, compared with the average for all commercial banks in the U.S. (own work, based on company filings and FRED, Federal Reserve Bank of St. Louis)

{kind=link}

{kind=link}

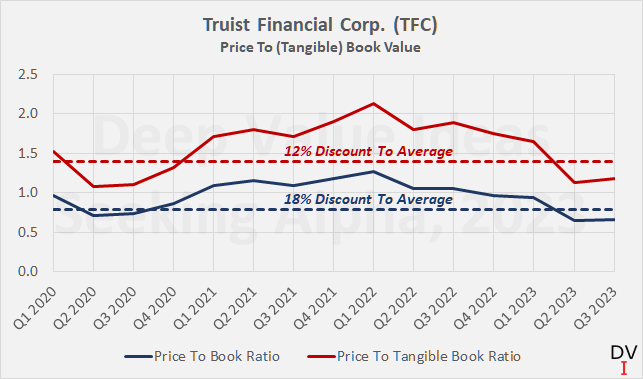

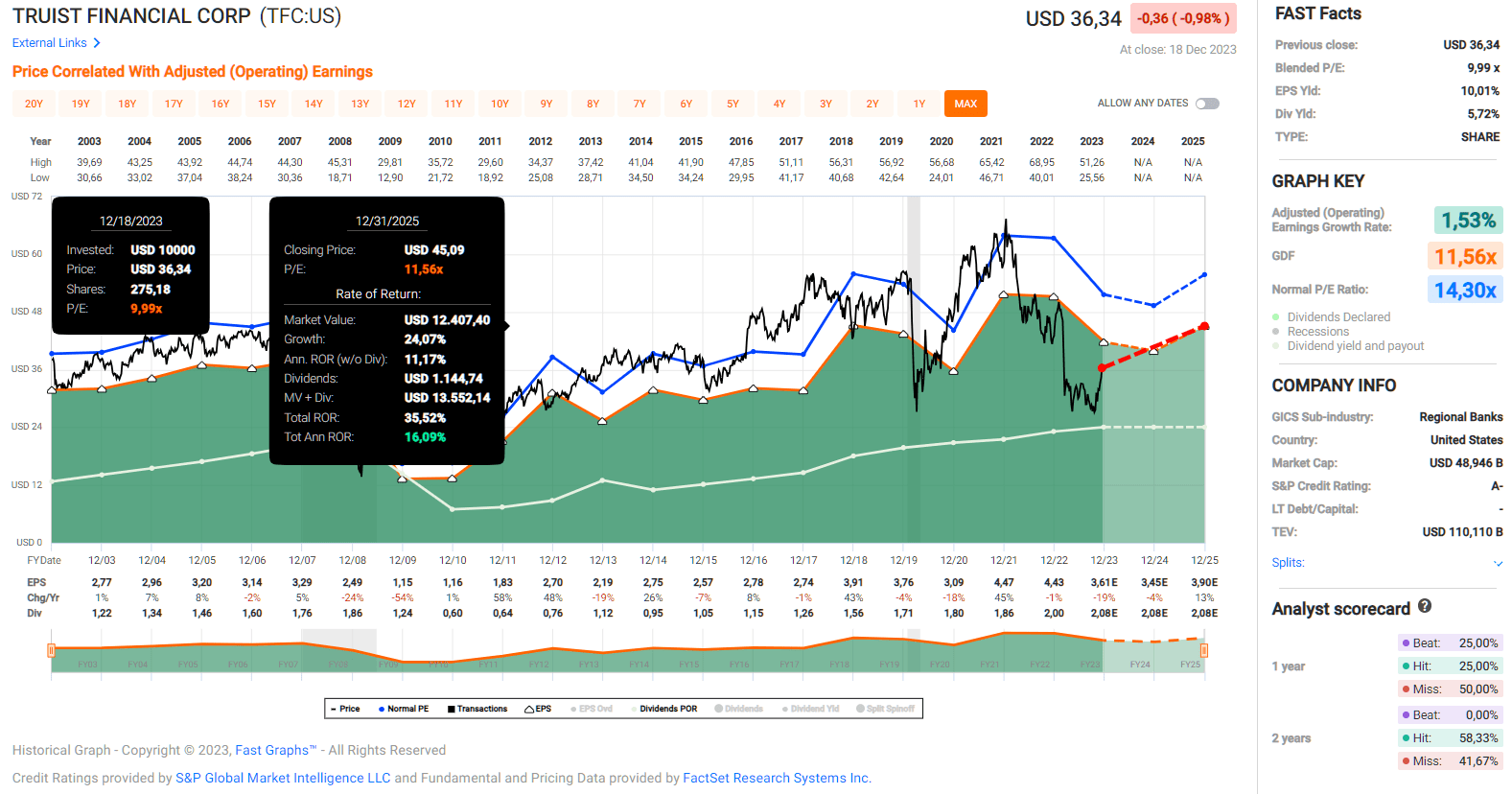

Compared to the three-year average valuation in terms of price to (tangible) book value, Truist remains comparatively cheap (Figure 9). Compared to the averages, Truist stock is undervalued by a mid single-digit percentage, although it should be noted that the period since the beginning of 2020 has de facto been characterized by crises rather than normality. If we take the ten year average price to book value of Truist (or its predecessor) as a comparison, the stock would be almost 30% undervalued. From the perspective of the historical price/earnings ratio (Figure 10), TFC stock also remains comparatively cheap with a discount of 13% to the long-term average value. Truist shares also remain favorable from a dividend perspective (current yield of 5.7% versus the five-year average of 4.2% ), although it should be noted that the bank's short-term dividend growth prospects are fairly poor due to capital building efforts.

Figure 9: Truist Financial Corp. (TFC): Price to (tangible) book value) on a quarterly basis ((own work, based on company filings and the daily closing price of TFC stock) Figure 10: Truist Financial Corp. (TFC): FAST Graphs chart, based on adjusted operating earnings (FAST Graphs)

{kind=link}

{kind=link}

Conclusion

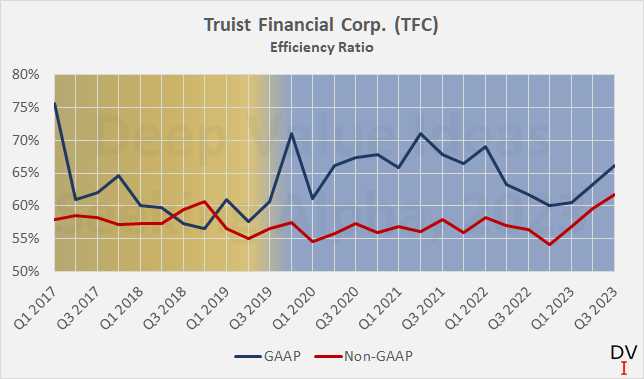

Truist Financial stock has definitely been one of the more deeply discounted names of the 2023 banking crisis. The main reasons for the market's skepticism lie in the - still largely unaddressed - profitability concerns (Figure 11) and of course the HTM assets issue. As I have explained in this update and in my previous articles, I believe the c securities portfolio-related concerns are largely unfounded. The BTFP is serving its purpose, and Truist deposit trends do not suggest any material impact from fear-induced deposit flight.

Figure 11: Truist Financial Corp. (TFC): GAAP and adjusted efficiency ratio; the yellow and blue colors illustrate the pre- and post-merger period, respectively (own work, based on company filings)

{kind=link}

With the Fed having recently signaled rate cuts for 2024, it is no wonder that the market is taking a slightly less critical view of the HTM issue. After all, lower interest rates will lead to an increase in the market value of high duration bonds. However, investors need to be aware that resolving the HTM issue will take time - at the end of 2022, the effective duration of Truist's securities portfolio was 6.7 years. In addition, Truist has not purchased any long-term government bonds for its HTM portfolio so far in 2023. Such investments would gain in value if interest rates were to fall, thereby partially offsetting the currently still high unrealized losses.

The market, which is increasingly anticipating rate cuts, is probably also starting to factor in a profit contribution from improved maturity transformation as the yield curve eventually normalizes. However, it is also important to keep in mind the prime reason for rate cuts - to stimulate a weakening economy, which is usually accompanied by temporarily weaker earnings for banks and higher charge-offs.

Taken together, I think the Truist Financial Corporation stock rebound was justified, but with the market looking ahead, I do not see much more upside potential for TFC stock in the near term, as the bank's deeper issues will take time to be resolved. For a return to long-term average multiples, the bank's operating fundamentals would need to show signs of sustained improvement.

However, with the stock still trading well below its long-term average multiples, I am not thinking of selling my position, knowing full well that TFC could come under renewed downward pressure if long-term interest rates rise again, or in a recession. Knowing how difficult it is to time the market reliably, I have downgraded Truist to Hold and remain patient while watching management's progress closely.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Truist Financial Stock: Downgraded To Hold Despite Powell Pivot