TFC - Truist: Solid As A Rock And Potentially Returning 8.4% Annualized

2023-12-29 14:17:29 ET

Summary

- Truist Financial Corporation has proven to be a profitable investment for us, with previous trade recommendations earning annualized returns of 15% and 12.5%, respectively.

- TFC is a bank holding company formed from the merger of BB&T and SunTrust Banks, ranking 9th in size in the US with $542 billion in assets.

- Despite its solid position and cost-cutting campaign, TFC's valuation remains cheap, making it an attractive option for selling put options.

- We outline a trade that stands to out-earn the dividend on an income basis, while simultaneously reducing risk in the name.

So far in 2023, we have written two separate articles about Truist Financial Corporation ( TFC ).

In April, we wrote: " Truist: Following Earnings, We're Ready To Start Buying ", which talked about how the stock had been unfairly discounted by the market due to the regional banking panic that had occurred only a month prior.

In June, we wrote: " Truist: Don't Forget About This Deep Value Gem ", which covered the recent earnings and how the stock was still well positioned for gains throughout 2024.

In both articles, we advocated a "put selling" strategy, where keen investors could earn higher-than-average rates of annualized return by selling put options on the stock, thus earning a premium and locking in a chance to buy shares of the company at a lower price.

Fast forward to today, and both of these trade recommendations have proven profitable, earning a 15% annualized return and a 12.5% annualized return respectively.

After a solid rally, strengthening business conditions, and 2 new earnings reports, we wanted to revisit the stock, break down what has been going on with the company, and pitch a similar trade to the one we have historically - a trade that we believe has a chance to potentially earn investors an 8.4% annualized yield over the next few months.

This represents a return more than 300 basis points higher than the dividend, and is accompanied by significantly less risk in our view.

Sound good? Let's jump in.

Getting Up To Speed

Here's some quick facts about TFC in case you're new to the stock.

What it is :

- Truist is bank holding company formed in 2019 from the merger of BB&T and SunTrust Banks.

- Truist is one of the largest banks in the US, ranking 9th in size as of October 2023, with $542 billion in assets.

- The company is headquartered in Charlotte, North Carolina.

Where it operates :

- 2,781 branches across 15 states and Washington, D.C., mainly concentrated in the Southeast and Mid-Atlantic regions.

What it does :

Truist offers a wide range of financial services for individuals, businesses, and municipalities, including;

- Consumer banking : Checking and savings accounts, credit cards, mortgages, loans, etc.

- Commercial banking : Lending, payments, treasury management, etc.

- Capital markets : Investment banking, trading, underwriting, etc.

- Wealth management : Investment advice, portfolio management, trust services, etc.

These core services are in addition to a few other miscellaneous offerings like owned and partnered insurance, partnered employee benefit management, and more.

Financial Results

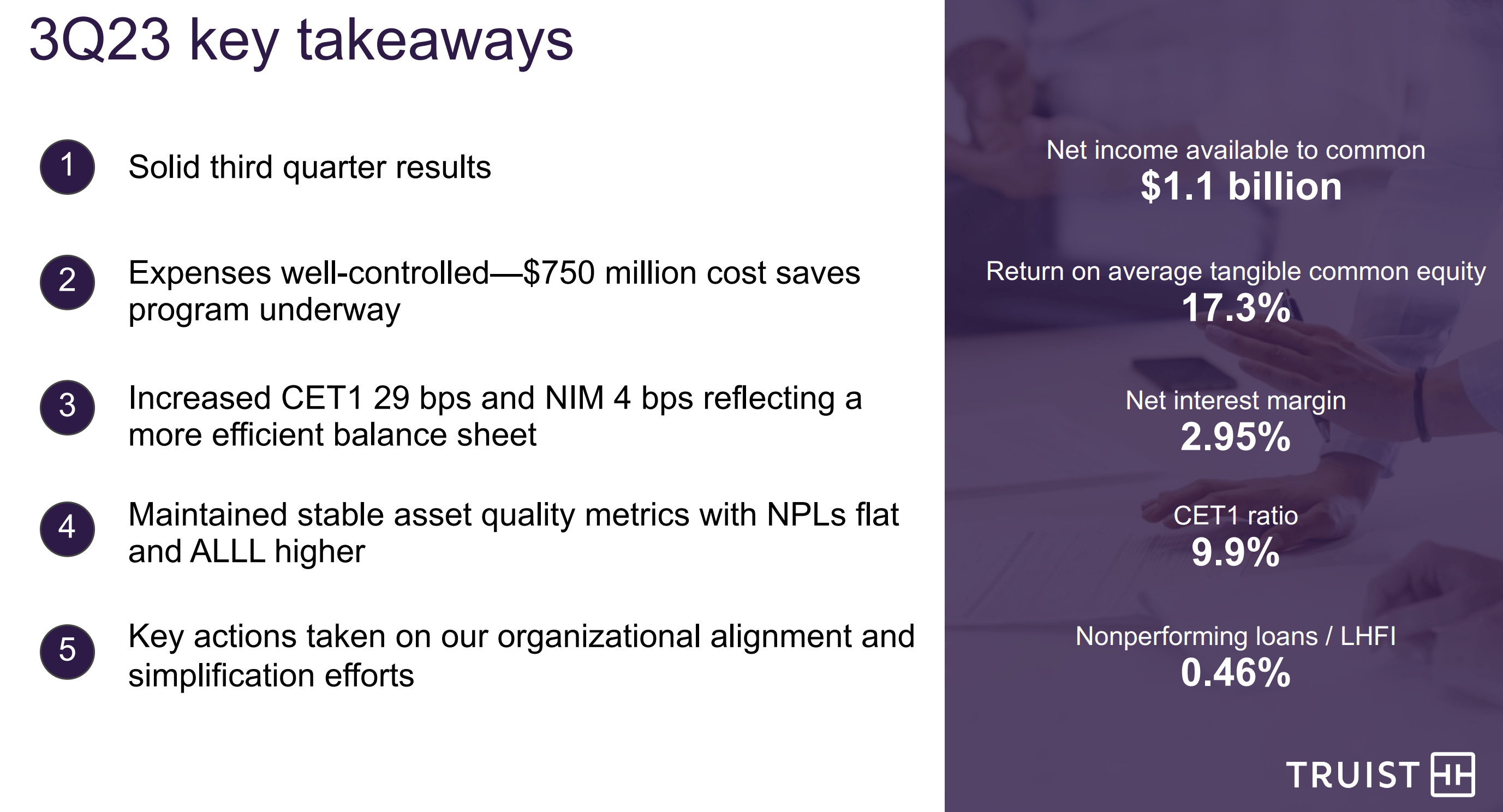

When we last published on TFC, we were mainly focused on the company's level of stability following the regional banking crisis in March of this year.

In our view , the bank's position was stable and improving:

Before, during and after the recent merger, Truist has demonstrated consistent and impressive financial performance. TTM Revenue is up over 136% to ~$28 Billion over the last 5 years, and Free Cash Flow has almost doubled in that same span to more than $8.5 Billion.

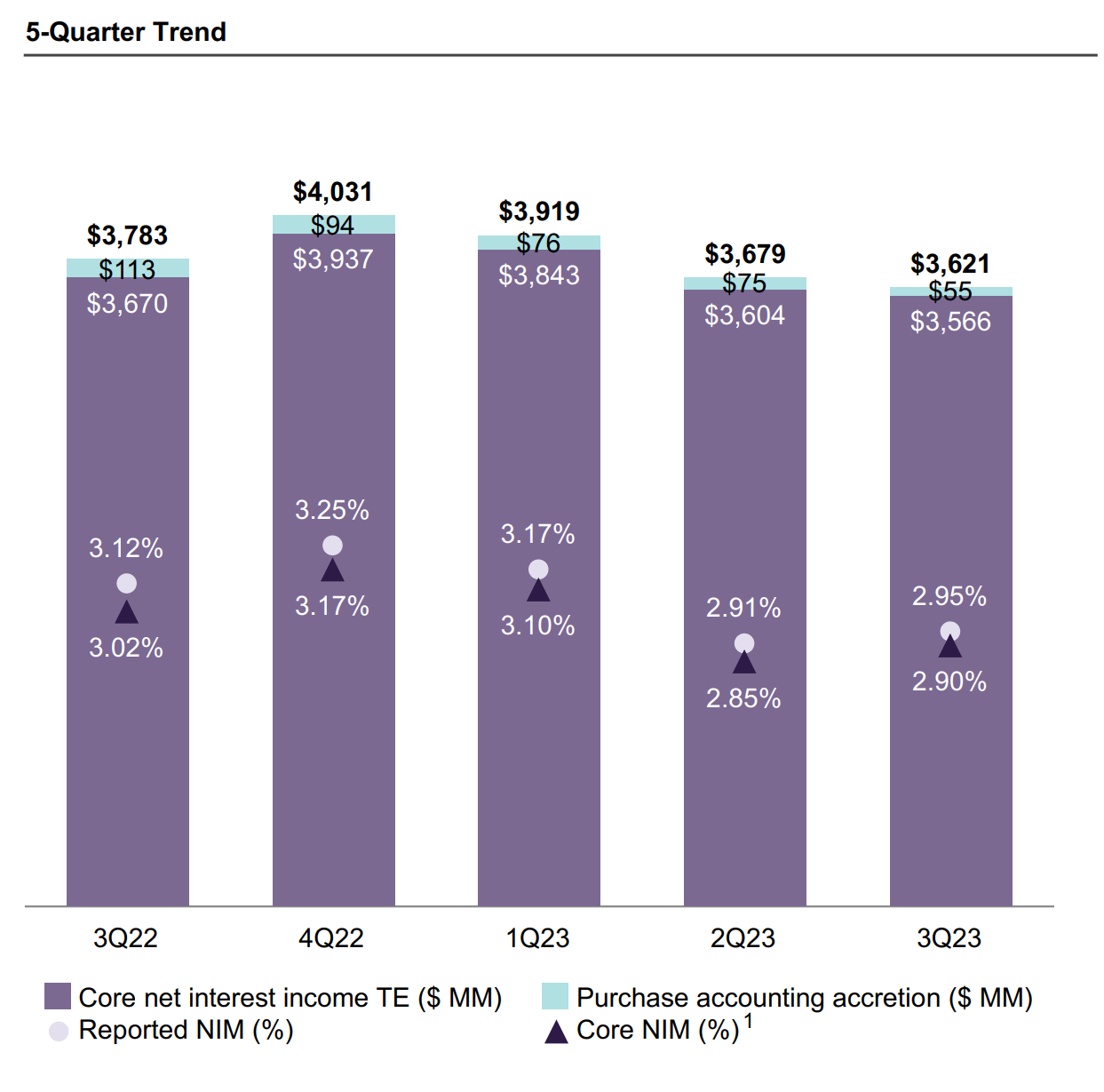

These strong results have been driven by economies of scale, new digital product launches (Digital Account opening increased by more than 50% QoQ), and a solid, diverse loan book. Core Net Interest Margins were strong up 41 bps YoY to 3.10%.

When it comes to liquidity, the bank also stands on solid ground. Throughout the recent banking crisis / bank run scare, Truist only saw deposit declines of 1.2%. [Additionally], in terms of the balance sheet, the bank maintains $166 Billion in liquidity, and a $63 Billion difference between assets and liabilities.

Over its recent earnings reports, things have remained stable.

Revenues and net interest income has come under pressure somewhat as TFC has had to increase deposit rates, something that we viewed as inevitable to prevent deposit bleed.

Consequently, net income is down on an absolute basis relative to 2022.

However, NIM's were actually up 4 basis points in the most recent quarter on a QoQ basis, which reflects the company's new cost saving program in action :

We are driving swift and meaningful actions to simplify our organization and reduce expenses. Our continued focus on core clients, paring back non-core and lower-return portfolios, and paying down higher-cost borrowings has made our balance sheet more efficient and helped drive a modest improvement in our net interest margin.

{kind=link}

{kind=link}

These recent results from recent quarters highlight the wood that management still needs to chop in terms of cutting costs amid restructuring and a novel rate environment.

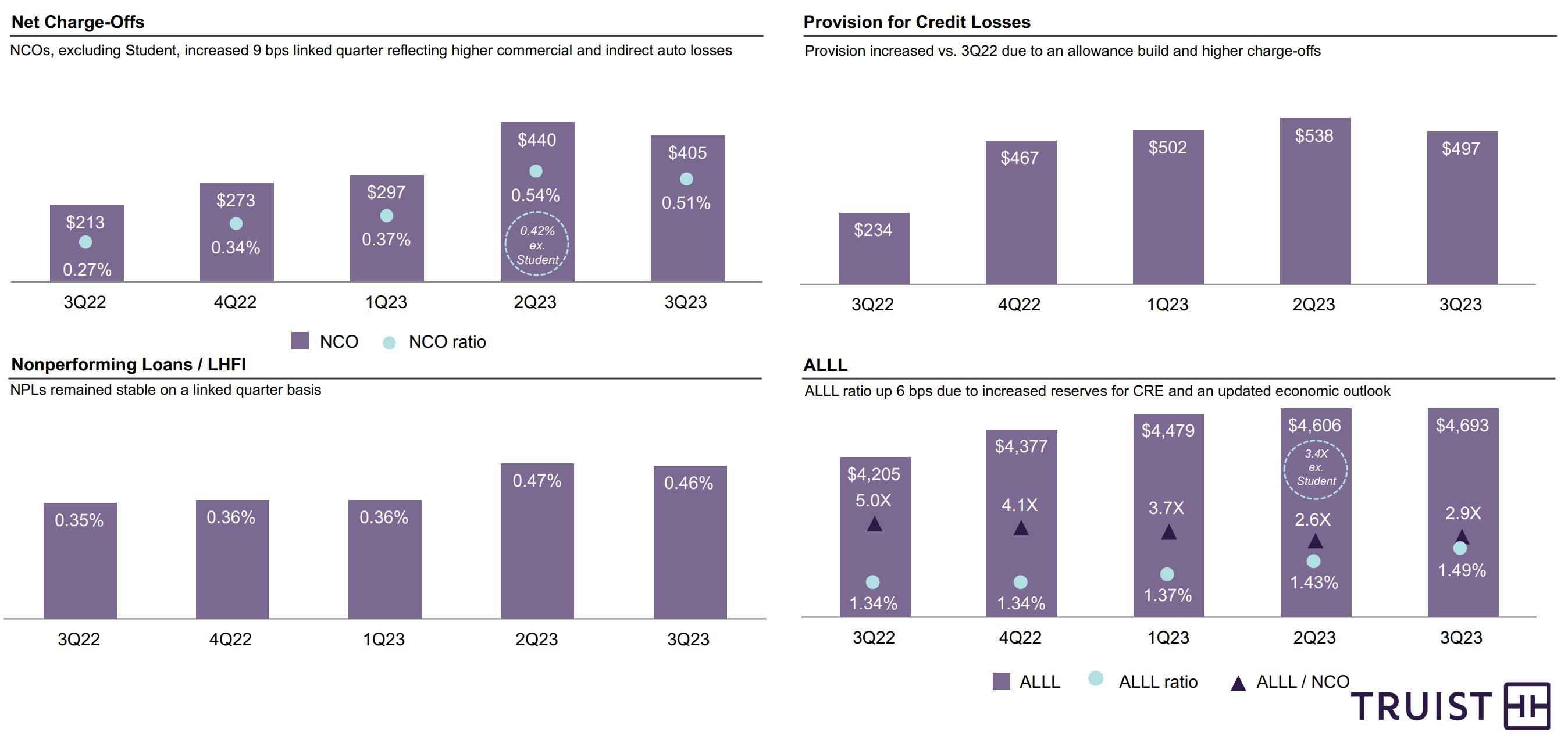

However, asset quality is improving, and provisions for losses in light of economic uncertainty appear to have peaked over the two recent reports, which bodes well for future earnings growth:

{kind=link}

All in all, after a banner 2022, TFC seems to be managing the increased competitiveness and cyclicality well. Part of this is due to the bank's size and deposit stickiness, with the bank's average customer relationship length stretching out more than a decade.

The balance sheet also appears to be in good shape, with a $62 billion gap between assets and liabilities - almost exactly where things sat directly following the banking crisis.

Solvency concerns, there are not.

The Valuation

Despite the stable competitive position of TFC and the ongoing cost savings program which looks to save $750 million over the next 4-6 quarters (which should have a solid impact on the bottom line), TFC's valuation is still rather cheap, especially compared with the bank's historical multiple, as well as the financial sector as a whole.

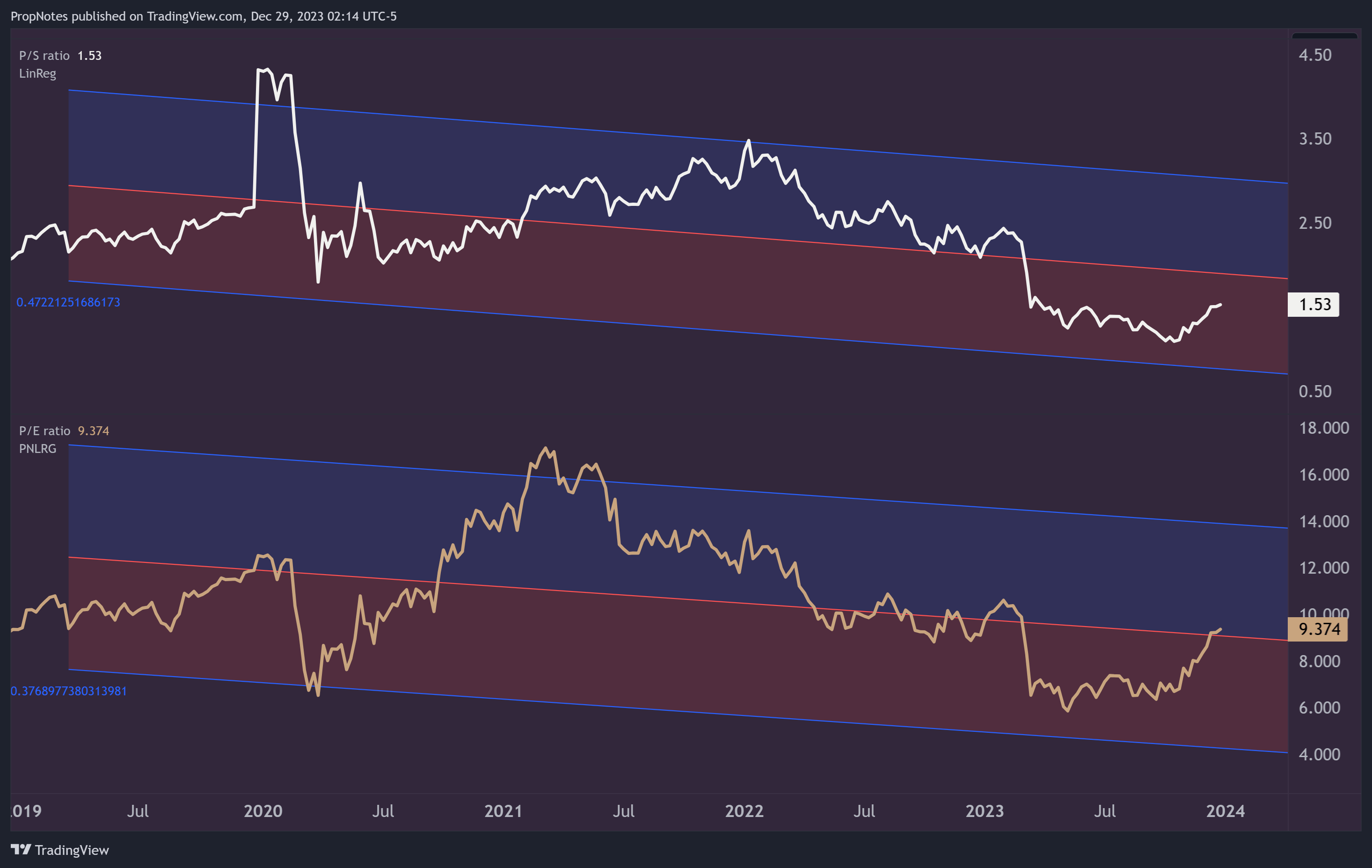

On top line revenue, TFC continues to trade below its long-term trend:

{kind=link}

As you can see, the sales multiple is well into the 'red' zone, which indicates that it's experiencing a lower than average multiple when measured on a 5-year linear regression.

The net income multiple is a little richer, around 9.3x, although that too was trading below the historical mean for some time until the recent rally. Any amount of earnings growth in the next report should knock this back into the 'red' undervalued territory as well.

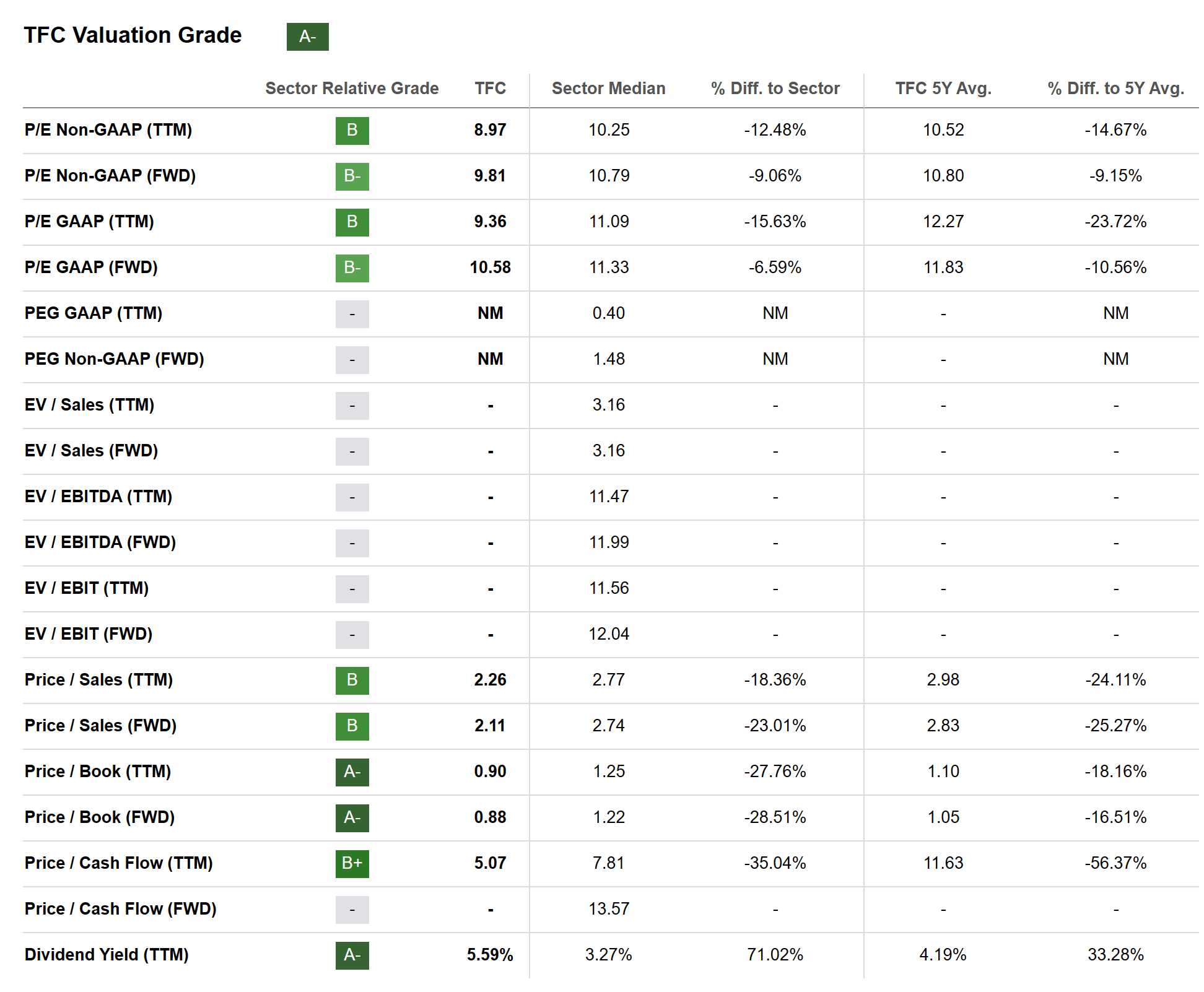

Additionally, when zooming out and measuring against the sector, TFC also appears undervalued, with the Seeking Alpha Quant Rating System giving the stock an "A-":

{kind=link}

The bank's valuation metrics across the board trade at a discount to the sector, which indicates that shares may be undervalued, especially in light of the bank's strong net income margins that stand above 25%.

But is buying the best way to take advantage of the relative discount and stable performance? We don't think so.

The Trade

Instead, consider selling put options on TFC stock. In case you're new to options, here's what that means:

- Selling a put option means you're granting the buyer of the option the right to sell you 100 shares of TFC at a specific price (strike price) by a certain date (expiration date).

- In return, you receive a premium upfront, which is your immediate profit regardless of what happens to the stock price.

Plus, if you sell options below where the stock is currently trading, then you 'get' to buy in at a lower price vs. where things are at the present moment.

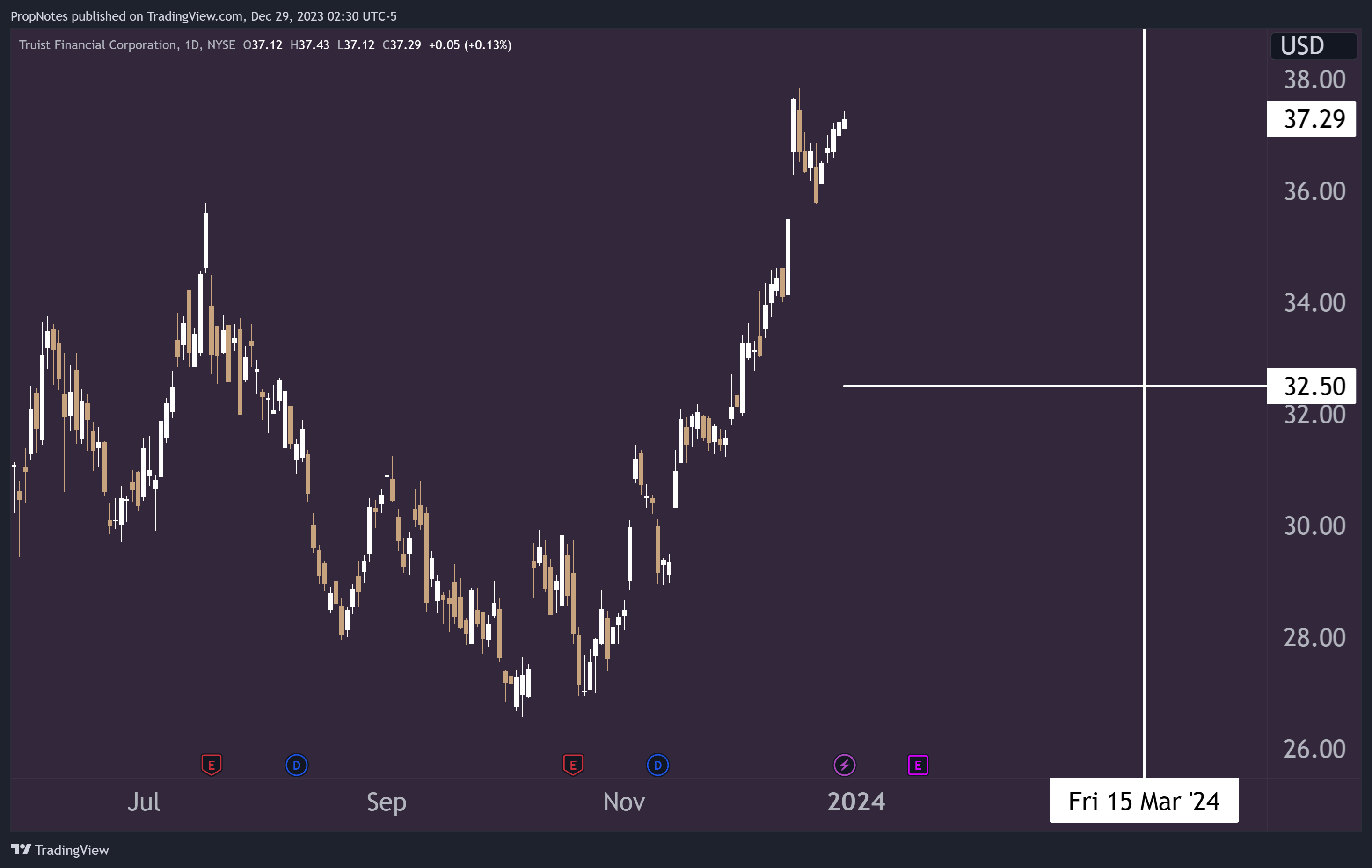

In this case, we like the idea of selling the $32.5 strike price options that expire on 3/15/2024:

{kind=link}

These options are currently going for 0.57 cents per share, or $57 per contract.

Here's what this means:

- If the stock finishes above $32.50 on March 15th of next year, then you get to keep the 57c per share free and clear. This represents a 1.4% cash-on-cash return, which annualizes to 8.4%. This is higher than the 5.5% dividend the stock currently pays.

- If the stock finishes below $32.50 on March 15th, then you still get to keep the 8.4% yield, but you are also obligated to buy the stock at $32.50. This price represents a 13% discount to the most recent price traded in the market.

Thus, selling put options on a solid stock like TFC looks like a win-win scenario; either outpace the dividend and inflation, or earn a better-than expected yield at a better price than is currently available in the market.

As we mentioned in the intro, we've done this successfully twice before this year. With an 83% chance of max profit by expiry, the odds continue to look good for this strategic opportunity.

Risks

While we like TFC stock and this strategy looks like a lower-risk way to play the stock, there are some risks that we should mention.

First off, if you sell a put, you're obligated to buy shares at the strike price, even if the stock completely collapses or goes to zero.

This isn't necessarily any different than the risk of holding the stock over the same time horizon, but it's important to know regardless.

Additionally, the underlying stock could face risks as well, like a repeat of this year's bank run, a falling rate environment which could hurt NIM's, or a worse-than-expected economic scenario which could cause further provisions for losses and pressure on net income.

These are all factors that could cause losses in our trade idea.

That said, we feel comfortable taking this risk in this stock as previously outlined.

Summary

TFC continues to be a steady banking franchise, with good NIM's, solid cost cutting momentum, and an attractive valuation. Using it as a platform for selling puts seems like the best way to play the stock, generating returns in the process while hedging out some downside risk.

All in all, selling puts here seems like a win-win trade for investors looking to get involved in TFC in a lower-risk way. Stay safe out there.

Cheers!

For further details see:

Truist: Solid As A Rock And Potentially Returning 8.4% Annualized