TRMK - Trustmark Corporation: An Opportunity To Be Cautious About

2023-09-21 14:40:13 ET

Summary

- Trustmark Corporation has seen its deposits grow, but its share price has not recovered significantly.

- The company offers a wide array of banking services, including commercial and consumer banking, mortgages, insurance, and wealth management.

- Trustmark's financial performance has improved, with net interest income and net profits rising compared to the previous year.

- Shares offer upside potential, but investors should be cautious if they do decide to pull the trigger.

Earlier this year, a banking crisis sent shares of many financial institutions tumbling lower. Although many of those companies have since posted significant partial share price recoveries, some have barely improved. Of those, most have failed to improve because deposits remain depressed.

But one player in the space that has seen its deposits grow, and yet has not seen a meaningful share price recovery, is Trustmark Corporation ( TRMK ). This is in spite of the fact that shares are cheap relative to both earnings and book value per share. The reason for this, I believe, largely stems from the elevated uninsured deposit exposure that the company has. While this has improved over the past couple of quarters, it is still higher than what I would like to see. But because it is the only significant metric that gives me concern and because deposits do continue to grow, I have decided to rate the bank a soft "buy" for now.

Checking in on Trustmark

Founded in 1968 and headquartered in Jackson, Mississippi, Trustmark is a bank holding company that provides its customers with a wide array of financial services . As of the end of its 2022 fiscal year, the company had 169 offices spread across the markets in which it operates. These markets include parts of Alabama, Florida, Mississippi, Tennessee, and Texas. Through these locations, the firm offers a variety of commercial banking services. Examples here include the provision of loans for commercial and industrial projects, loans for various types of commercial real estate, loans for construction and land development, and more.

Naturally, Trustmark also engages in consumer banking services. For both consumers and commercial enterprises, it offers up checking and savings accounts. Money market accounts are also provided. It offers its consumers mortgages, and it even engages in the secondary marketing and servicing of mortgages. Insurance solutions are also an area that the company engages in, with examples including, but not limited to, life and health insurance. Other activities consist of wealth management and trust services, on top of other various activities.

{kind=link}

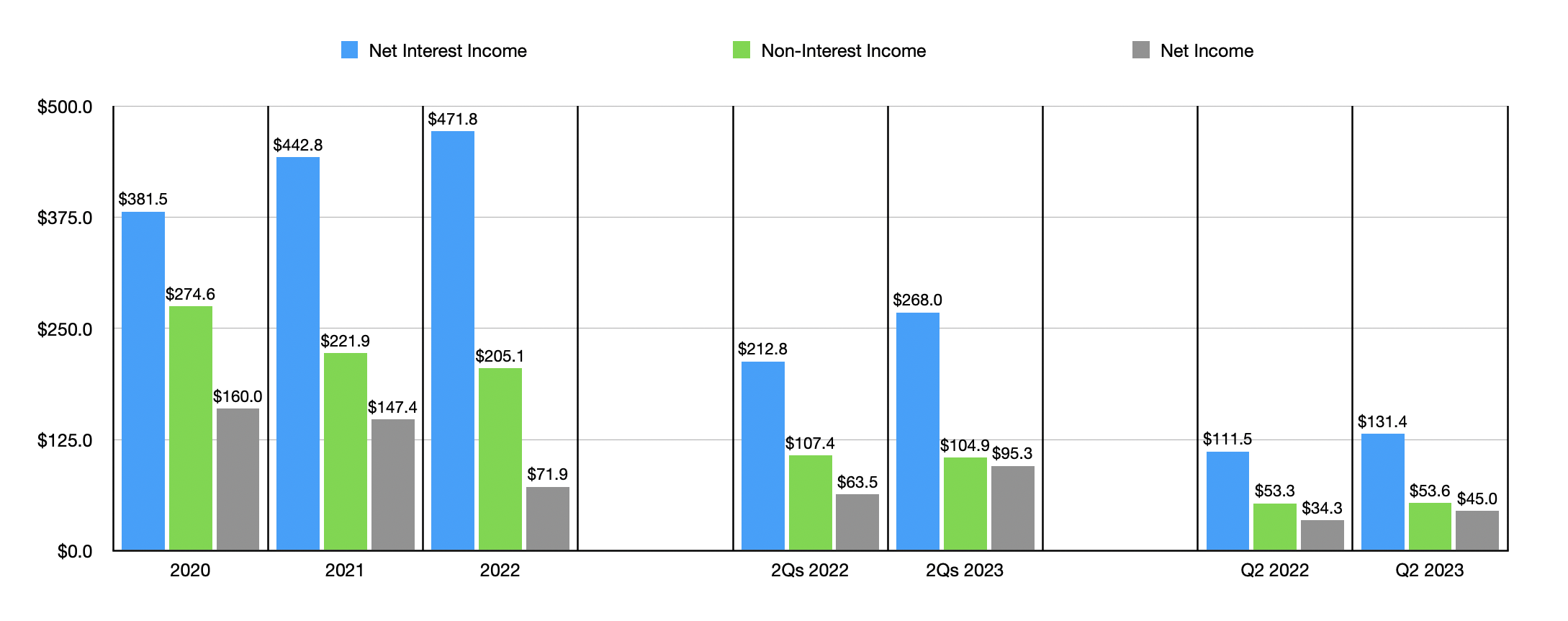

Over the past three fiscal years, Trustmark has done a solid job growing its top line. Net interest income grew from $381.5 million in 2020 to $471.8 million in 2022. Over that same window of time, however, non-interest income dropped from $274.6 million to $205.1 million. All of this decline, however, has been driven by a drop in mortgage banking revenue. This fell from $125.8 million to $28.3 million over this window of time. This drop, according to the firm's financial statements, was driven by a decline in the gain on sales of loans under the company's mortgage unit.

Digging deeper, this drop seems to have been caused by both a reduction in margin on its loan sales in the secondary market and by a fall in overall loan sales. For instance, from 2021 to 2022, loan sales dropped 45.6%, or $1.04 billion. Management said that rising interest rates were the cause of reduced mortgage lending activity during this time. As I have written about in prior articles, the housing market is starting to show signs of a recovery. So I wouldn't be surprised if financial performance starts to improve from this point on.

On the bottom line, the picture for the company was a bit more complicated. Net income has dropped from $160 million in 2020 to $71.9 million in 2022. However, much of that fall was driven by a $100.8 million litigation settlement that the company incurred. If we use the same interest rate applied to pre-tax earnings for 2022 and add back the post interest litigation settlement, which is justifiable considering it is a one-time event, then earnings last year would have been $170.1 million. This ignores the continued decline that I mentioned regarding mortgages in the prior paragraph. As you can see in the first chart in this article, financial performance so far this year has largely improved, with net interest income and net profits rising nicely compared to what the company saw the same time last year.

{kind=link}

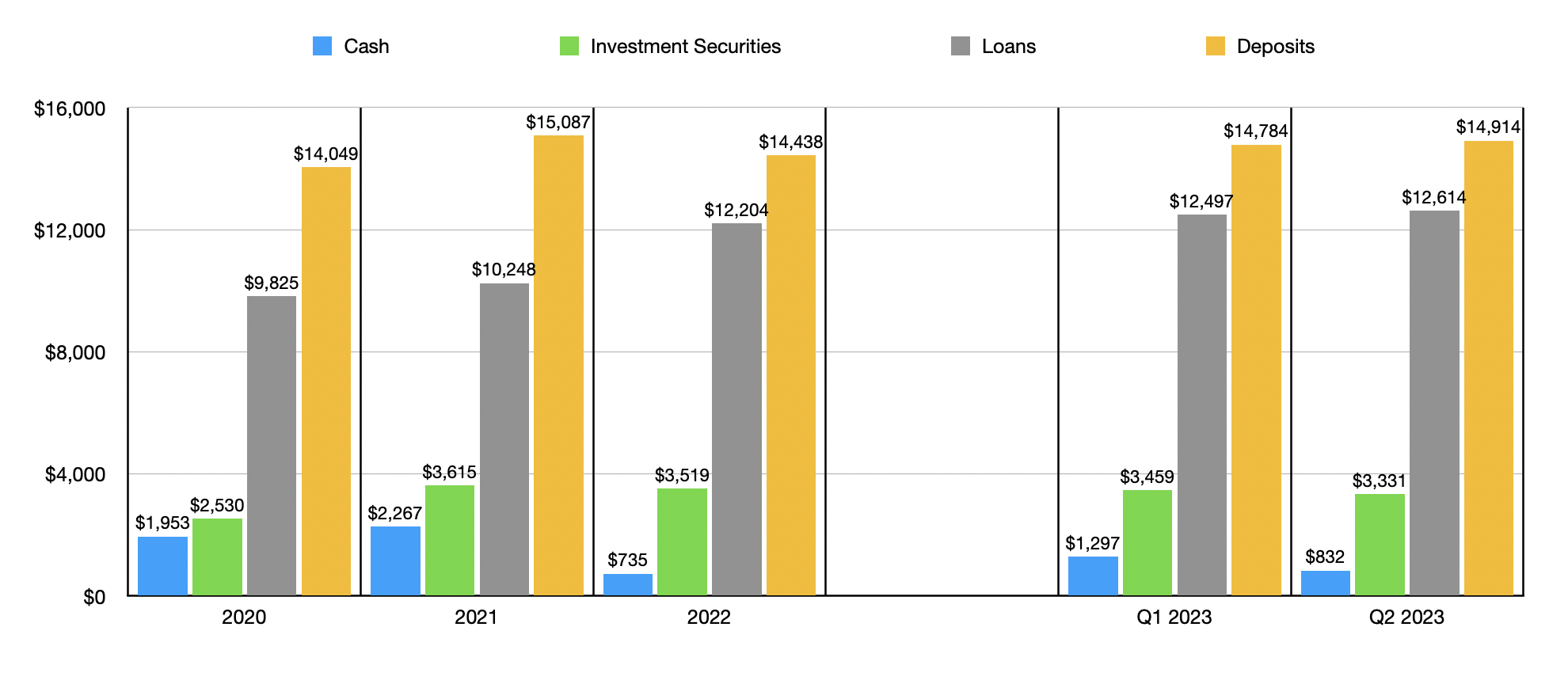

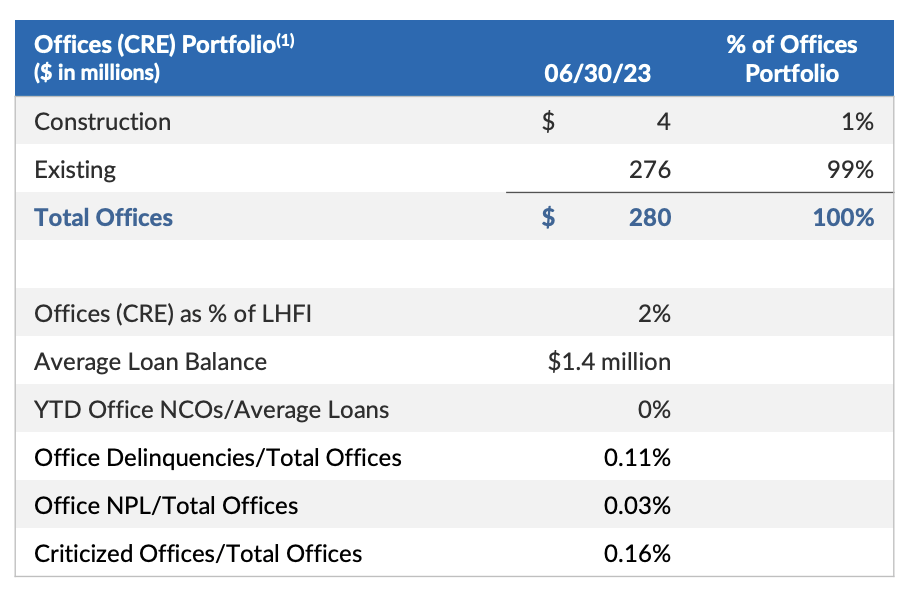

The overall growth in financial performance was only made possible by the continued growth in the company's asset base. The value of loans on its books, for instance, expanded from $9.82 billion in 2020 to $12.20 billion in 2022. By the end of the second quarter of this year, loans had grown to $12.61 billion. I understand that one area that investors have been concerned about recently, and justifiably so, is office exposure. But the good news is that this is very limited when it comes to Trustmark. As of the end of the most recent quarter , only about $280 million, or 2% of the company's loan portfolio, was in the form of office properties.

{kind=link}

As the company's loan portfolio grew, it also saw an increase in the value of investment securities on its books. These expanded from $2.53 billion in 2020 to $3.52 billion in 2022. We have seen a decline since then, with the metric dropping to $3.330 billion. And some of that decline seems to have been in response to management's decision to reduce debt. At the end of the first quarter this year, debt was $1.71 billion. But between the value of investment securities dropping and cash falling from $1.30 billion to $832.1 million, management was able to reduce this to $1.28 billion.

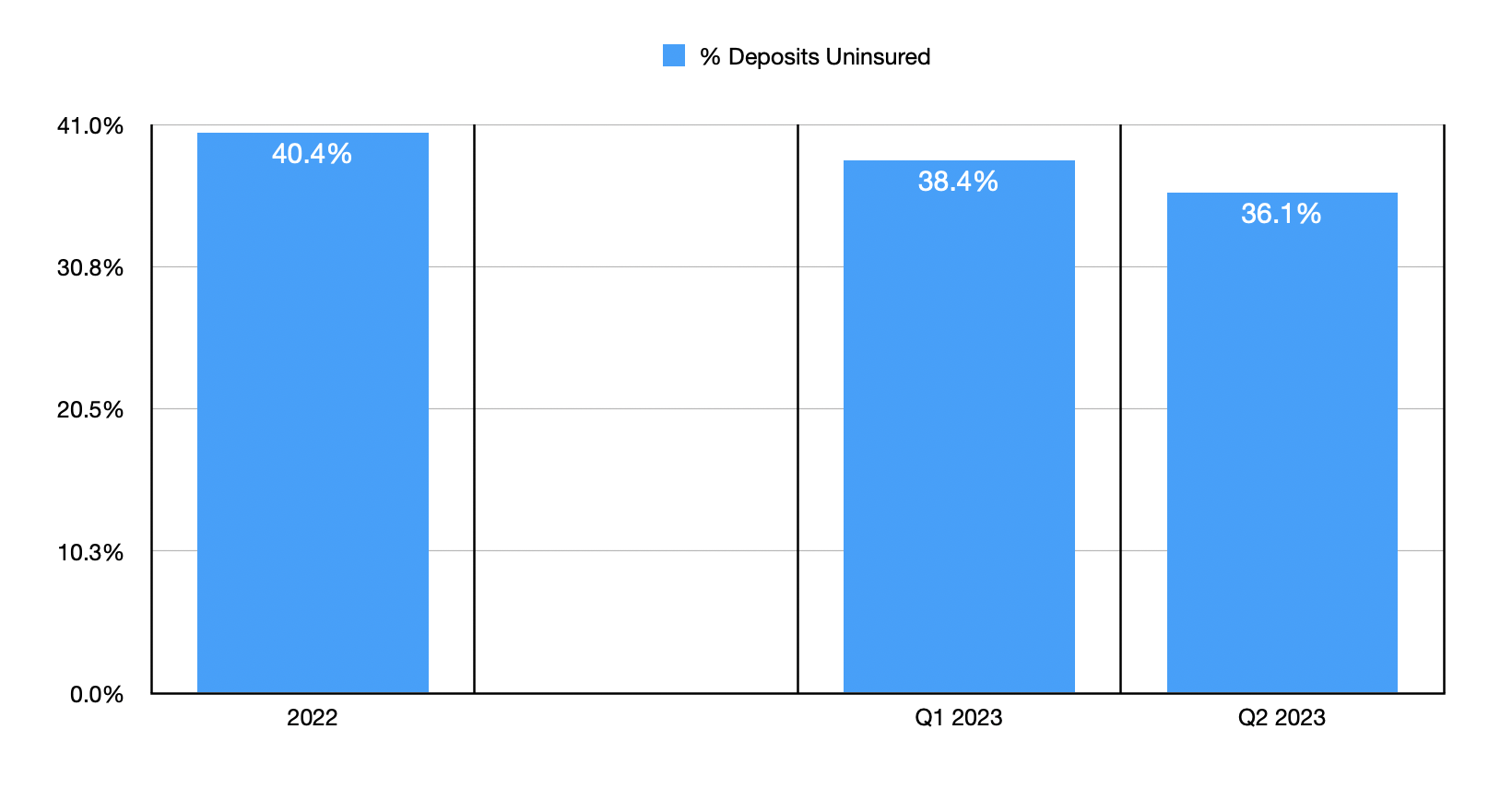

Loan growth is only possible when deposits remain robust. After rising from $14.05 billion in 2020 to $15.09 billion in 2021, deposits did pull back slightly to $14.44 billion. Interestingly, deposits continued to climb even during the banking crisis. At the end of the first quarter, deposits were $14.78 billion. And as of the end of the second quarter, they had grown to $14.91 billion. I don't believe this is the only bank that I have seen post continued growth in deposits during this time. But it definitely is a rarity. Most experienced at least some decline during the past couple of quarters. But one thing that does concern me is that uninsured deposit exposure for the bank remains lofty. At the end of 2022, it totaled 40.4% of overall deposits. By the end of the second quarter of this year, it had dipped only slightly to 36.1%. Ideally, I would like this number to be as low as possible, with a reading under 30% highly preferable.

{kind=link}

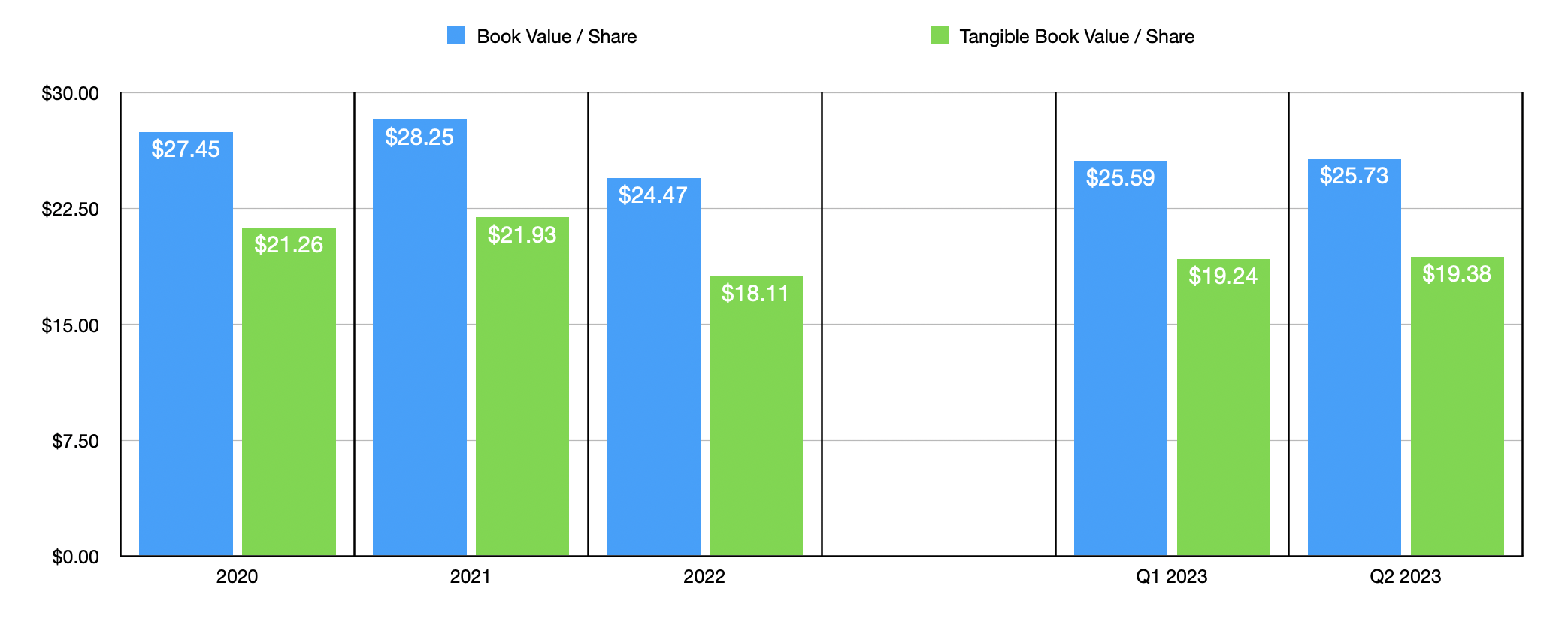

In recent years, the book value per share of the institution has bounced all over the map. After rising from 2020 to 2021, it pulled back in 2022. But since then, it has been on the incline. As of the end of the second quarter of this year, book value per share came in at $25.73. That compares to the $24.47 reported at the end of last year. Meanwhile, tangible book value per share has grown from $18.11 to $19.38. From a valuation perspective, the company seems to be trading at only 86% of its book value, while going for 114% of its tangible book value. This is perfectly fine, with some banks that I’ve seen trading lower and others trading higher. Earnings, meanwhile, have been enough to keep the price to earnings multiple of the bank at 7.9. This is definitely near the lower end of what I have seen so far this year. And the average in the space is around 10.4 at this moment. So relative to the average firm, Trustmark is looking good.

{kind=link}

Takeaway

For the most part, Trustmark is doing quite well for itself. I continue to be impressed with the growth in deposits that the bank has seen. Loan growth is impressive and management has recently reduced debt. Shares are trading at fine levels relative to book value and are cheap on a price to earnings approach.

I am a bit concerned about the uninsured deposit exposure. But on its own, this is not enough to cause me to become bearish about the bank. However, anybody who does decide to buy stock in it should make that a metric that they pay very close attention to moving forward.

For further details see:

Trustmark Corporation: An Opportunity To Be Cautious About