TRX - TRX Gold Is Value And Opportunity At These Prices

2023-03-10 10:24:56 ET

Summary

- The Canadian explorer is generating revenues and positive CFOs and is close to reaching breakeven FCF thanks to its Tanzanian exploitation.

- The company is pursuing a model where the exploitation's cashflows can finance new CAPEX for a sulfide mining project.

- The company's properties are located in a gold rich area with global players. TRX's latest resource assessment was done in 2020 with lower gold prices and less geological evidence.

- I believe TRX could self-finance its sulfide project and significantly increase revenues and profits.

- However, the company trades at a multiple between 6x and 12x of expected FY24 earnings, depending on assumptions of ore quality. The sulfide project and improvements in price are the free opportunity.

TRX Gold ( TRX ) (TNX:CA) is a Canadian mining company with a single gold mining open-pit operation in Northern Tanzania called the Buckreef mine.

The company lost millions for two decades in unsuccessful exploratory processes. However, since 2021, the company has been producing at a small scale in its Tanzanian mine.

The company can bootstrap its operations through self-generated cash flows at the subsidiary level and is close to generating positive net income at the consolidated level.

According to my calculations, the company could produce an annualized P/E ratio of 10 by mid-calendar 2024 compared to the current market cap. That leaves all the upside potential from expanding production as the unpriced opportunity.

Note: Unless otherwise stated, all information has been obtained from TRX's filings with the SEC.

Business description

Striking gold : TRX was an unsuccessful mining explorer for two decades, spending millions in exploration and licenses without generating revenue.

Things changed when the company obtained a pre-feasibility study (Canada's second-highest tier of resource qualification) in 2018 for an open-pit gold mine in northern Tanzania.

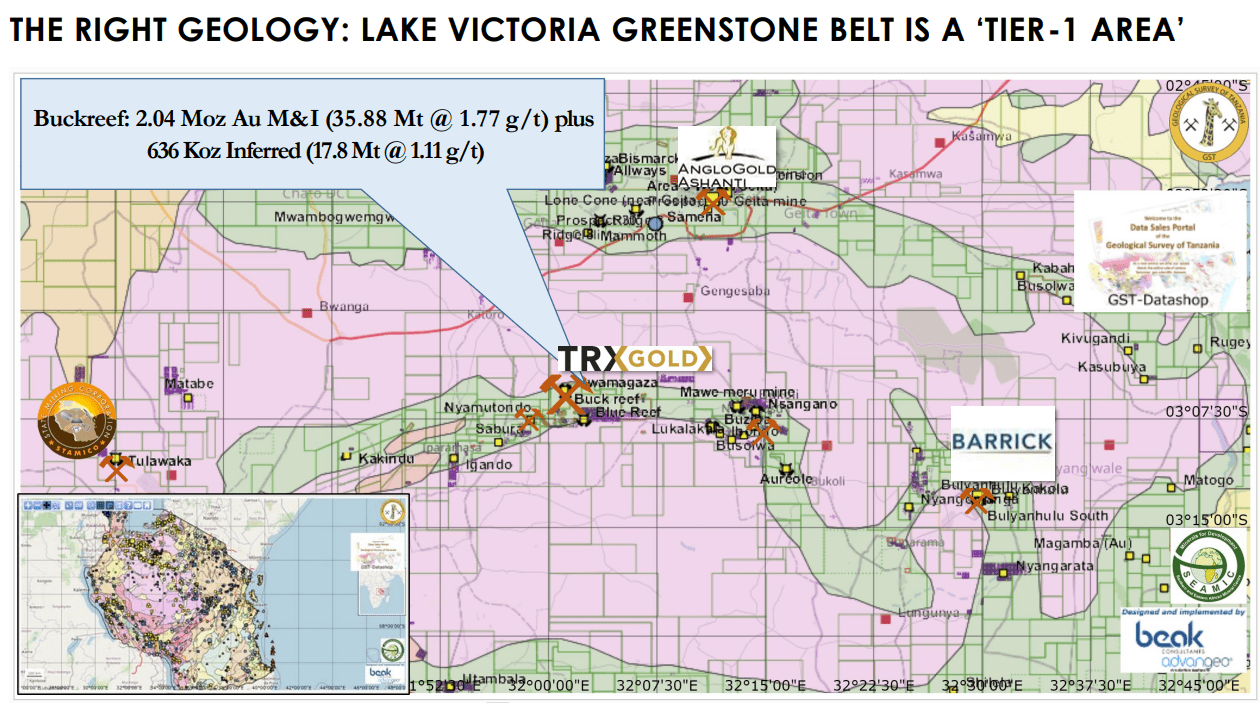

The Buckreef mine : TRX property is located between two important gold mines in Northern Tanzania: the Geita mine from AngloGold Ashanti ( AU ), and the Bulyanhulu mine from Barrick Gold ( GOLD ).

The region south of Victoria lake contains greenstone deposits rich in gold and other minerals.

The region where Buckreef mine is located (TRX's investor presentation)

{kind=link}

The property has measured gold resources for 1.2 million ounces and inferred resources for another 600 thousand ounces from studies published in June 2020 according to Canadian standards. The study was conducted before new discoveries were made , and with a gold price estimate of $1,300 per ounce.

Producing from oxide : The company started producing in an open-pit extracting oxides, which represent approximately 10% of the resources of the mine but are easier to exploit in terms of capital expenses. Mining advanced through two stages, adding 360+ tpd milling capacity first, to increase to 1000+ by the end of calendar 2022. The company's latest result, from 1Q23 (November 2022), includes mining and processing at the 1000+ tpd rate, with realized production of 5,400 ounces and expected yearly ranges between 20 and 25 thousand ounces. However, the company announced a few days ago the commissioning of a new 1000 tpd mill , which could double the mine's capacity for oxides.

Financing itself : The mine is already at the stage where it can finance a significant portion of the capital expenditures required to exploit oxide deposits and continue exploring the property. Reaching the existing 1000+ tpd capacity costs $4 million in capital expenditures so a similar figure could be expected for the additional capacity planned.

TRX has zero debt and is consuming cash reserves from share issuance but should reach breakeven FCF this year.

Sulfide project : The core of the property's value is concentrated in sulfide ores that require a different treatment from oxide ores. The company is in the process of obtaining economic feasibility studies for this project.

According to Canadian regulations, an EFS is the highest level of assurance for a mining project's economic extraction and profitability. It requires evidence of the existence of the resource underground, the feasibility of its metallurgical separation from the ore, and its economic value, under a series of assumptions.

As mentioned, the company had already obtained a pre-feasibility study in 2018. The granting of a feasibility study would estimate the project's CAPEX, returns, and, most importantly, a certification that the resources are there and it is profitable to extract them.

According to the company, the strategy is to use the cash from the exploitation of the oxide deposits to finance the CAPEX required to establish the sulfide exploitation several years into the future.

SG&A, compensation, and insider ownership : The company's SG&A expenses are relatively high for their size, running at $1.75 million in the last quarter, or $7 million annualized. We will later see that high SG&A expenses are the Achilles heel of the company's profitability.

Further, a significant portion of that SG&A comes from managerial compensation. Three executives, the CEO, CFO, and COO, were paid $4 million in FY21, according to the company's proxy statement .

Finally, insider ownership is not super high, at only 3.2% of the company, but this is relatively understandable given that the company's market cap is not small and that it has diluted its shareholder substantially before starting mining operations.

Tanzanian government participation and Tanzanian risk : The Tanzanian State Mining Corporation (STAMICO) has a 45% participation in the Tanzanian subsidiary that runs the mine.

Although Tanzania has been a democratic country free of political conflict for decades and one of the most prospering African countries, it is still a frontier market. There are substantial political risks from operating in Tanzania. Particularly changes to export taxes and buy-local requirements could change the company's economic equation. Much more terrible but also farther away are the risk of expropriation.

Some investors show concern because of the sanctions applied to Barrick Gold's mine (previously known as African Barrick Gold or Acacia Mining). The sanctions led to the delisting of Acacia, and its acquisition by Barrick, after substantial fines and capital losses. However, in this case, the company was found to have avoided millions in taxes, demonstrating not the risk of a change of rules but the application of rules. The same outcome, or even worse, would be expected in a developed country where a company is found falsifying export disclosures.

Valuation

In this valuation, I use an approach similar to the one used for other commodity companies. That is, to estimate profitability at different levels of production and sale prices under specific cost assumptions.

The company is producing at an annualized rate between 20 and 25 thousand ounces annually. However, given that the company already announced a mill expansion that should be online by the beginning of calendar 2024, we will start production at those levels.

In the MD&A for 1Q23 , the company published the table below. We can assume production and mining costs for the new 2,000+ tpd mill from it, applying conservative changes.

Starting at 2,000+ tpd, and capacity utilization of 95%, we arrive at approximately 700 thousand tonnes of ore processed annually. With a strip ratio of 7, this requires moving 4.9 million tons of land for $15.7 million. The processing cost of the ore is $14.5 million (variable * ore mined + fixed). We assume double the current fixed processing costs and the same variable processing costs. So we arrive at mining costs for 4.9 million tons of land and 700 thousand tons of ore, of $30 million.

Then we have to assume the grade. TRX's properties have an average grade of 1.7 g/t, but the mining for the last year has averaged 3 g/t . I prefer to operate with an average, assuming the grade will deteriorate to reach the property's estimated average. With 2.35 g/t, and 700 thousand tonnes of ore mined, we arrive at 1.645 million grams of gold, or 53 thousand troy ounces (58 thousand regular ounces).

Dividing costs by ozt obtained, we get a troy ounce cost of $565.

Operating data of TRX for 1Q23 (TRX's MD&A for 1Q23)

With this, we can calculate profits at the mine level, pay taxes of 30% for Tanzanian corporations , and 55% of those profits correspond to TRX, the other 45% to STAMICO.

Then we move down the income statement.

For SG&A, we assume $7 million, the current annualized expense. Most SG&A expenses are managerial compensation, so there is no way to forecast them based on production. It will depend on managerial decisions, and, for the time being, we give management a vote of confidence that it will not increase its compensation excessively.

Finally, we assume no taxes at the Canadian level, given that Canada recognizes worldwide income for Canadian corporations and allows for using foreign tax credits . We assume that TRX can offset all of its Canadian income taxes with Tanzanian income taxes.

Run the assumptions on an Excel sheet, and we get the net income table below for production and price assumptions.

Net income for TRX according to specific price, quantity, and cost assumptions (Own)

{kind=link}

According to our estimations, with a current price of $1,800 for a troy ounce of gold, TRX should get almost $20 million in net income annualized by the end of FY24 with the new mill operating or an approximate forward expected P/E ratio of 6x for FY24. Further, the scenarios allow for the company to operate profitably at very low prices.

Scenario analysis : I provide a different scenario to moderate the assumptions in the previous calculation. If the ore grade obtained is 1.7 g/t (the property average), production decreases to 38.5 thousand troy ounces with the new mill operating, and the cost per ounce moves up to $790.

The results for net income are shown below. The forward P/E ratio is much higher, and the company has a higher breakeven gold price. Still, the company is profitable at most prices and yields a P/E ratio of 13x at current prices.

{kind=link}

Conclusions

The company declared 2 million ounces of M&I resources. Considering that 10% is oxide deposits, the company has four years of production at the higher mining rate in the first scenario. This is more than enough to finance the sulfide project in terms of time and profits.

Under a lower-grade scenario, the company is profitable at most prices and can increase production by adding more mill capacity. This scenario would probably require external financing to start sulfide exploitation.

Still, in one scenario, the company trades at a risk-neutral (no assumptions about the price of gold) P/E ratio of 6x, and in the other one, 12x.

This would represent fair value for a company with no growth prospects, given that both scenarios could be assigned equal probabilities and that the company operates in a frontier market.

But, this valuation does not include the expansion to sulfide nor the possibility of feasibility studies recognizing more resources, given that the price of gold has been above $1,300 for quite some time, and the company has continued with exploratory work in the area. The closeness to major gold players implies that qualified resources could command a premium in an acquisition scenario.

Therefore, I believe TRX is an opportunity, given that its current market price implies a fair value of currently expected capacity (online in about a year) but leaves room for further improvements in capacity and resources.

For further details see:

TRX Gold Is Value And Opportunity At These Prices