PFIX - TTT: Unlikely To Repeat Stellar 2022 Performance

Summary

- The TTT ETF provides -3x 1-day returns of the ICE U.S. Treasury 20+ Year Bond Index.

- The TTT ETF returned 149% in 2022.

- Although interest rates may still rise in the coming year, TTT will unlikely repeat 2022's stellar performance.

A few weeks ago, I wrote a bearish article on the ProShares UltraPro Short 20+ Year Treasury ( TTT ), warning that it was time to cash out winnings on one of the most profitable trades of 2022. At the time, recession expectations were ratcheting higher, and long-term interest rates were inflecting lower in response.

However, my initial assessment appears to have been premature, as the U.S. 10Yr Treasury yield reversed near important support at 3.50%, and has been widening in the final weeks of 2022 (Figure 1).

Figure 1 - U.S. 10Yr treasury yield bounced at 3.50% support (Author created with price chart from StockCharts.com)

What has been driving this latest reacceleration in interest rates and is this move higher sustainable?

Central Banks Remain Hawkish

Since the Great Financial Crisis in 2008, central banks around the world have erred on the side of dovishness. For example, in 2018, while Chair Powell initially suggested monetary tightening was on autopilot , after a quick 20% selloff in the S&P 500, he quickly changed his tune and the Fed stopped raising interest rates by early 2019. In fact, by mid-2019, the Fed had begun cutting interest rates, helping stock markets rally to new all-time highs.

In contrast, at the most recent FOMC meeting on December 14th, despite stock markets having fallen by a similar 20% in 2022, the Federal Reserve reiterated its hawkish 'higher for longer' message , indicating more interest rate increases were likely in 2023.

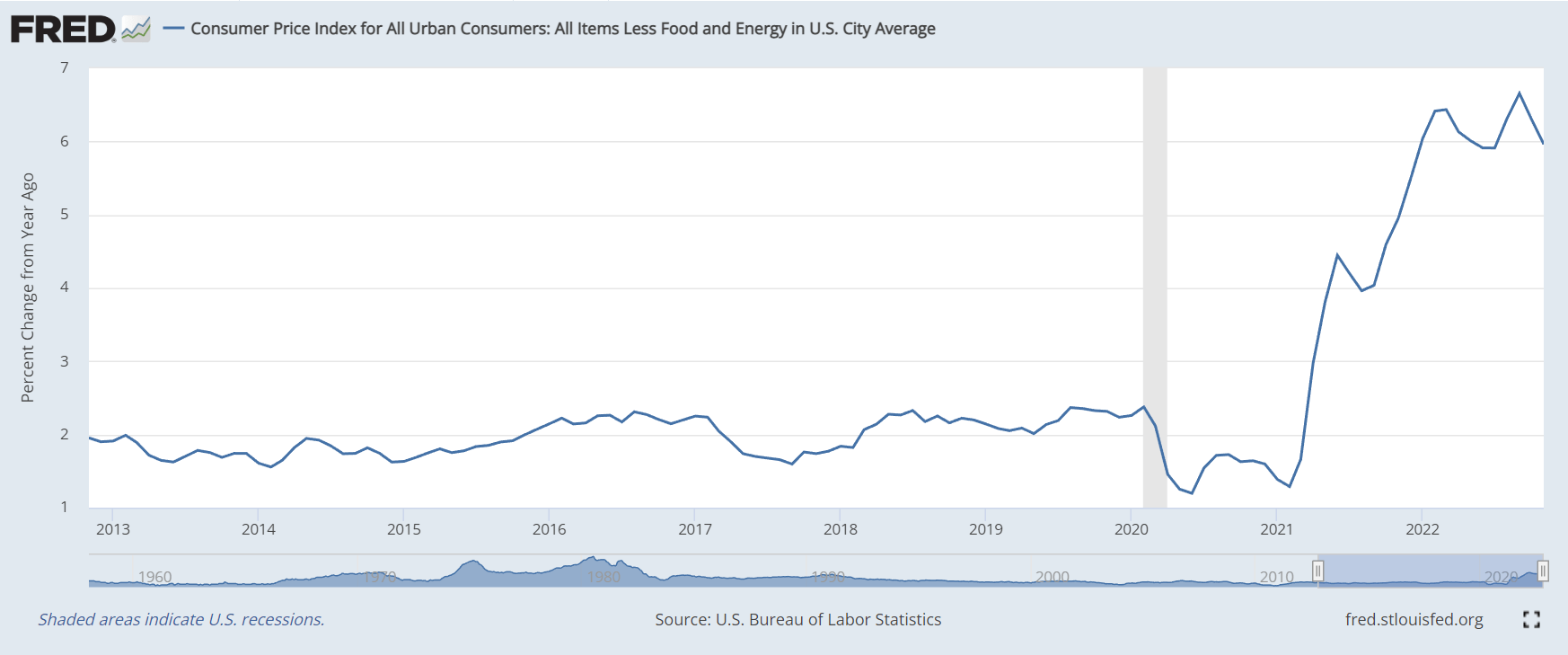

The key difference between 2018 and 2022 is that in 2018, inflation was low and steady, so the Fed had room to cut interest rates. However, in 2022, inflation has been uncomfortably high, with the most recent core inflation reading still at 6%, far above the Fed's target of 2% (Figure 2). This means the Fed must now err on the side of hawkishness, lest inflation becomes entrenched.

Figure 2 - Core CPI inflation (St. Louis Fed)

{kind=link}

Economic Data Still Coming In Strong

Furthermore, while economists have been predicting a pending recession for many months, actual economic data have continued to come in stronger than expected. For example, the most recent U.S. GDP reading showed the U.S. economy grew at a 3.2% annualized rate in Q3/2022, and initial unemployment claims continue to show strength in the U.S. labour market.

Ironically, good economic data is now considered bad, as it gives the Federal Reserve cover to stick to its 'higher for longer' policy. Until data shows that inflation is on trend to return to 2% or the economy starts contracting, the Fed is likely to maintain its restrictive policies.

Carry Trades Unwound On BOJ Surprise

Perhaps the most impactful short-term driver for the rise in interest rates has been the Bank of Japan's ("BOJ") surprise decision to raise the yield limit for 10Yr Japanese Government Bonds ("JGBs") to 0.50%, from a previous limit of 0.25%.

This BOJ move appeared to have caught macro investors off-guard and sparked an unwind of tens, if not hundreds of billions in 'carry trades'. A carry trade is where investors borrow in a low-yielding currency and invest in higher-yielding assets. As the BOJ had been steadfast on its 0.25% yield cap on JGBs, the Japanese Yen was a favourite funding currency for many macro traders engaging in the 'carry trade'.

The BOJ surprise caused the Yen to jump the most in 24 years and likely triggered stop losses for these macro traders. As carry trades are unwound, foreign assets like U.S. treasuries were likely sold off, leading to rising interest rates.

Higher Japanese Yield Means Less Demand For U.S. Treasuries

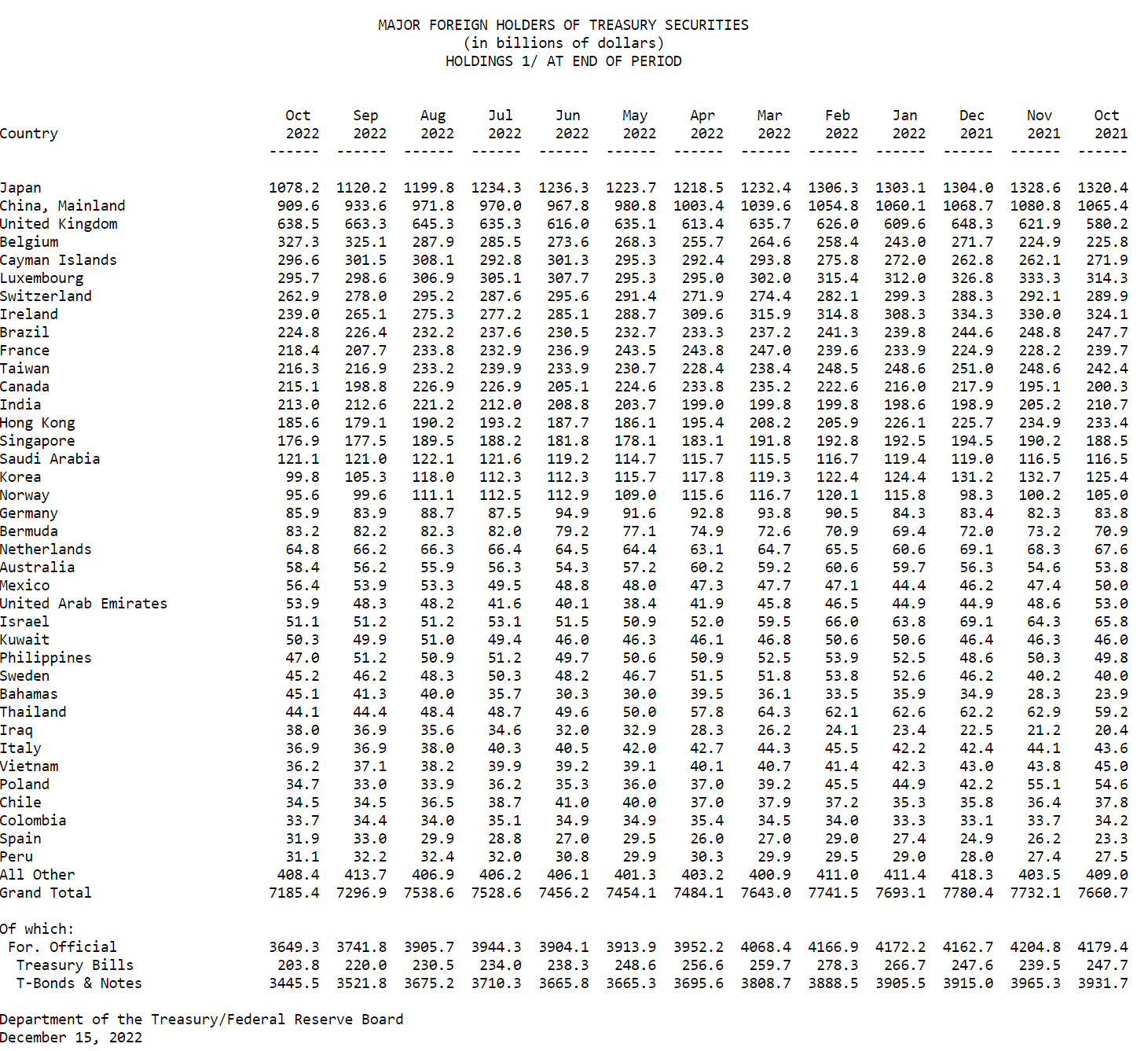

The reversal of the carry trade may remove a key source of demand for U.S. treasuries at a critical time. According to treasury data , Japan is the largest foreign holder of U.S. treasuries. While the impact from the BOJ surprise is likely short-term in nature, with higher domestic interest rates, there will be less Japanese demand for U.S. treasuries going forward (Figure 3).

Figure 3 - Top foreign holders of U.S. treasury securities (treasury.gov)

{kind=link}

Learning from Russia's recent experience with U.S. sanctions, China is also unlikely to add to its hoard of U.S. treasuries, lest it gets frozen/confiscated due to a potential geopolitical confrontation between China and the U.S.

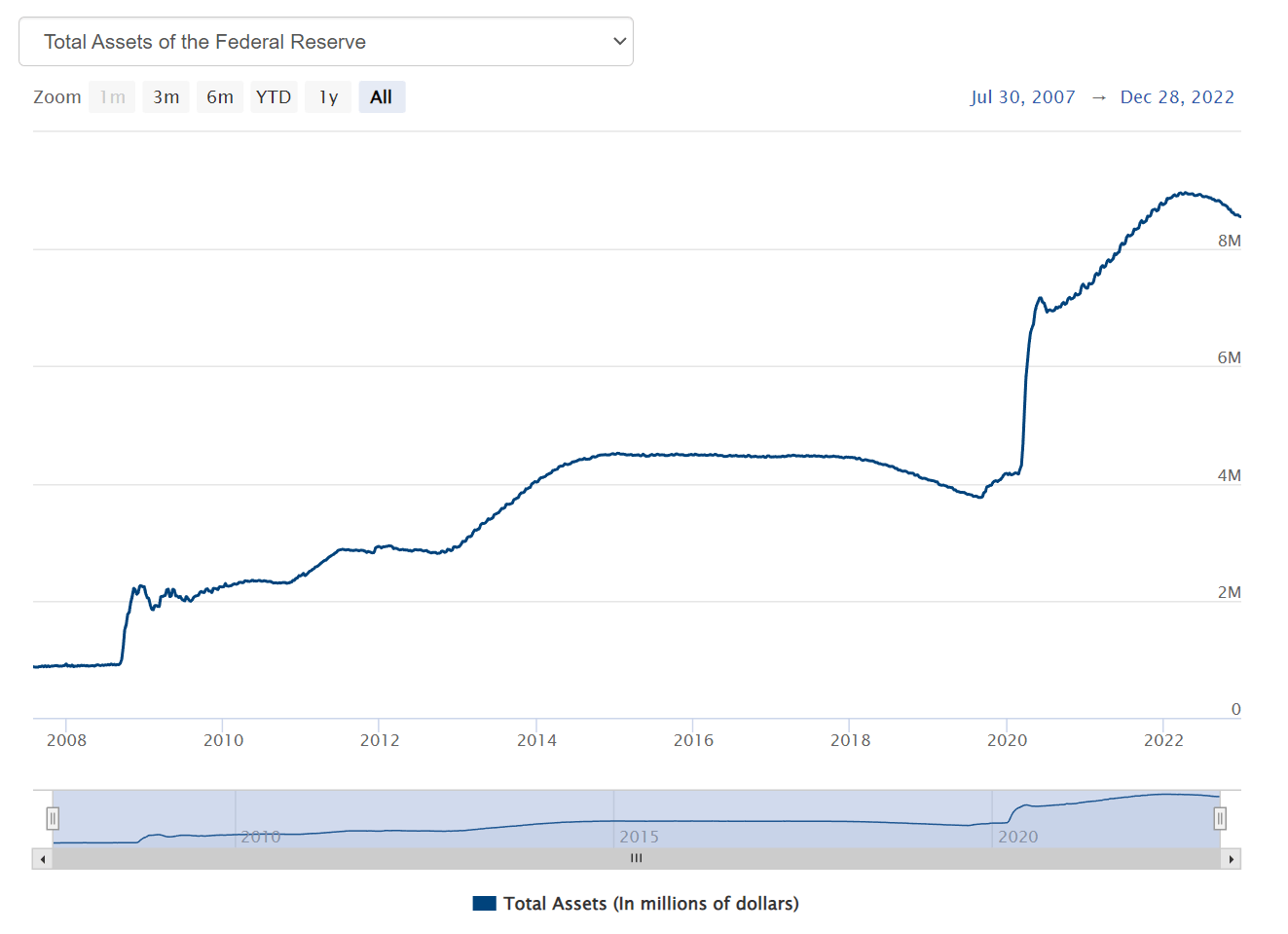

With the U.S. government set to run trillion-dollar deficits for the foreseeable future, it is unclear where the demand for treasury securities will come from, especially as the Federal Reserve engages in Quantitative Tightening ("QT") and allows its balance sheet to run-off at a pace of $95 billion per month (Figure 4).

Figure 4 - Federal Reserve balance sheet running off from QT (U.S. Federal Reserve)

{kind=link}

2022 Unlikely To Repeat; Beware Of 2 Way Volatility

TTT's performance in 2023 is unlikely to repeat its stellar 2022 returns. This is because in early 2022, long-term interest rates were coming off their lowest levels ever due to extraordinary COVID-pandemic monetary policies. Long-term interest rates essentially moved 1-way for many months, leading to TTT's convex returns.

Going forward, as long as economic data continues to come in line or better, I expect the Fed will stick to its 'higher for longer' message, pressuring long-term yields higher. However, every major economic report will also come with increased risk, as the delayed impact from the Fed's 2022 interest rate hikes flow through the real economy. Weak economic data will lead to selloffs in treasury yields, as investors brace for a recession.

The tension between the Fed and incoming economic data will lead to increased volatility in treasury yields, acting as a headwind to inverse levered ETFs like the TTT due to their daily rebalancing volatility decays (please refer to my prior articles on levered ETFs for a more detailed explanation of volatility decay).

Instead of inverse levered ETFs, I recommend investors hedge rising interest rates with a fund like the Simplify Interest Rate Hedge ETF ( PFIX ). The PFIX ETF owns a portfolio of OTC swaptions that is "functionally similar to owning a position in long-dated put options on 20-year US Treasury bonds". However, instead of daily rebalancing decays, the PFIX has a daily theta decay that should be small in comparison, due to its portfolio's long-dated nature. I recently wrote an article about the PFIX here .

Risks To My Call

The rise in long-term interest rates in recent weeks could simply be due to one-time events like the BOJ surprise. Once the carry trade unwind pressure subsides, long-term treasury yields may resume its decline, as investors position for a 2023 recession. This would be negative for the TTT ETF.

On the other hand, if long-term interest rates were to move higher in a straight-line pattern over the coming months like it did in early 2022, the TTT should once again deliver convex returns.

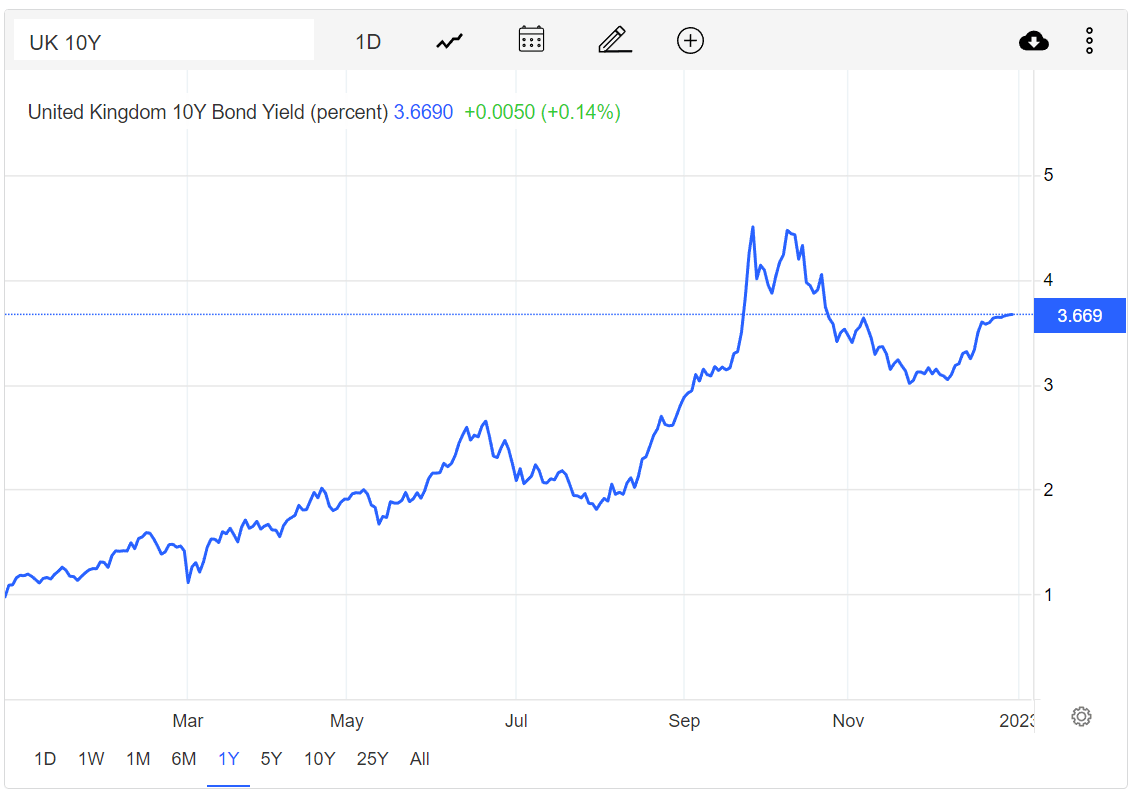

While it is unclear at the moment what could be the driver for such a move higher in long-term treasury yields, weirder things have occurred in the past few years to rule out such a move. For example, U.K. treasuries suffered a massive run in September/October 2022, as investors lost confidence in Theresa May's government (Figure 5).

Figure 5 - U.K. treasuries suffered a run in mid-2022 (tradingeconomics.com)

{kind=link}

Conclusion

In summary, it appears my prior warning on the TTT ETF was premature, as the Fed is sticking to its 'higher for longer' policy and the economy appears more resilient than expected. However, TTT's returns in 2023 are unlikely to repeat its stellar 2022, as I expect increased 2-way volatility in treasury yields.

Instead of inverse levered ETFs like the TTT with daily rebalancing volatility decay, I recommend investors hedge rising interest rates with the PFIX ETF, which acts like a long-term put option on 20-year treasury bonds.

For further details see:

TTT: Unlikely To Repeat Stellar 2022 Performance