FECCF - Tullow Oil: Focus Now On Cash Flow And Profitability

2023-11-16 06:08:38 ET

Summary

- Tullow Oil is shifting its focus from a reserve-based strategy to a focus on low risk-high cash flow projects.

- The company sold its interest in Guyana to Eco Atlantic, indicating the high-risk nature of the project.

- Tullow Oil's management is focusing on Jubilee in an effort to increase cash flow while reducing the debt ratio.

- This management is making good progress but it is probably too early to consider investing. This management should be watched for a better entry point.

- This part of Africa needs the money earned from exporting oil. Therefore, the business atmosphere is helpful even though risk is elevated due to unstable governments.

For quite a while, the previous Tullow Oil (TUWLF)(TUWOY) management focused far more on reserves and finding that offshore "home run". The result was several projects with less than desirable breakeven points and some dry holes. Now management is focused on profitability. Some of the projects like Guyana where cash flow is a speculative future and so is years away at best will be exited or have been already. On the other hand, places like Ghana which have far more certainly and promise relatively steady growth will be the focus as the company delevers. At some point, as management persists with this strategy, the company will become an attractive investment proposition. Right now, the company is likely to be a hold for most investors while watching the progress.

The speed of this deleveraging project is rather uncertain. But its far enough along for investors to see the progress. But the other thing about offshore is there is an occasional large producer that could materially advance the deleveraging progress.

Guyana

Earlier in the year, Tullow sold its holdings in Guyana to Eco Atlantic (ECAOF). This is not a reflection of the quality of the lease but rather an admission by management that they inherited too many high-risk projects for the size of the company.

Tullow had drilled wells that found heavy oil with sulfur. The problem with that is that there is extra processing involved to remove the sulfur while selling a discounted product. The breakeven on the production was estimated at more than $50 BOE which is far too high for an offshore project. Exxon Mobil ( XOM ) was plugging and abandoning these wells whenever they found similar oil.

The fact that Tullow sold its interest after announcing these discoveries tells you all you need to know about those announcements. The second well probably should not have been drilled by previous management. The lease itself could have light oil deposits as well. Clearly Exxon Mobil found light oil. But rather than continue to spend money on a project with speculative upside when the company already has a high debt load, management sold this to Eco Atlantic for about $700,000.

This has implications for Frontera (FECCF) which just announced plans to sell its acreage after finding two light oil discoveries . Light oil discoveries are much more marketable. But two discoveries are hardly enough for any buyer to determine that there is sufficient oil to continue to production. On the other hand, it is two more discoveries than is the case here.

Ghana

This area of operation is further along in that management has established production and is able to drill wells with reduced exploration risk as well as development wells that have a good chance of increasing production. Offshore operations tend to be expensive and there are disappointing wells for one reason or another. Therefore, this type of upstream operation has probably less certainty and more risk than unconventional where the onshore results are fairly certain.

From a political viewpoint, much of this part of Africa earns foreign currency through the production of oil. Therefore, even though there are periodic reports of unrest and a coup from time to time, much of the time oil and gas production continues undisturbed. This is especially true for offshore production which is most of the company production. The business environment would be helpful even if periodic instability in the region elevates business risk because these governments need the money.

{kind=link}

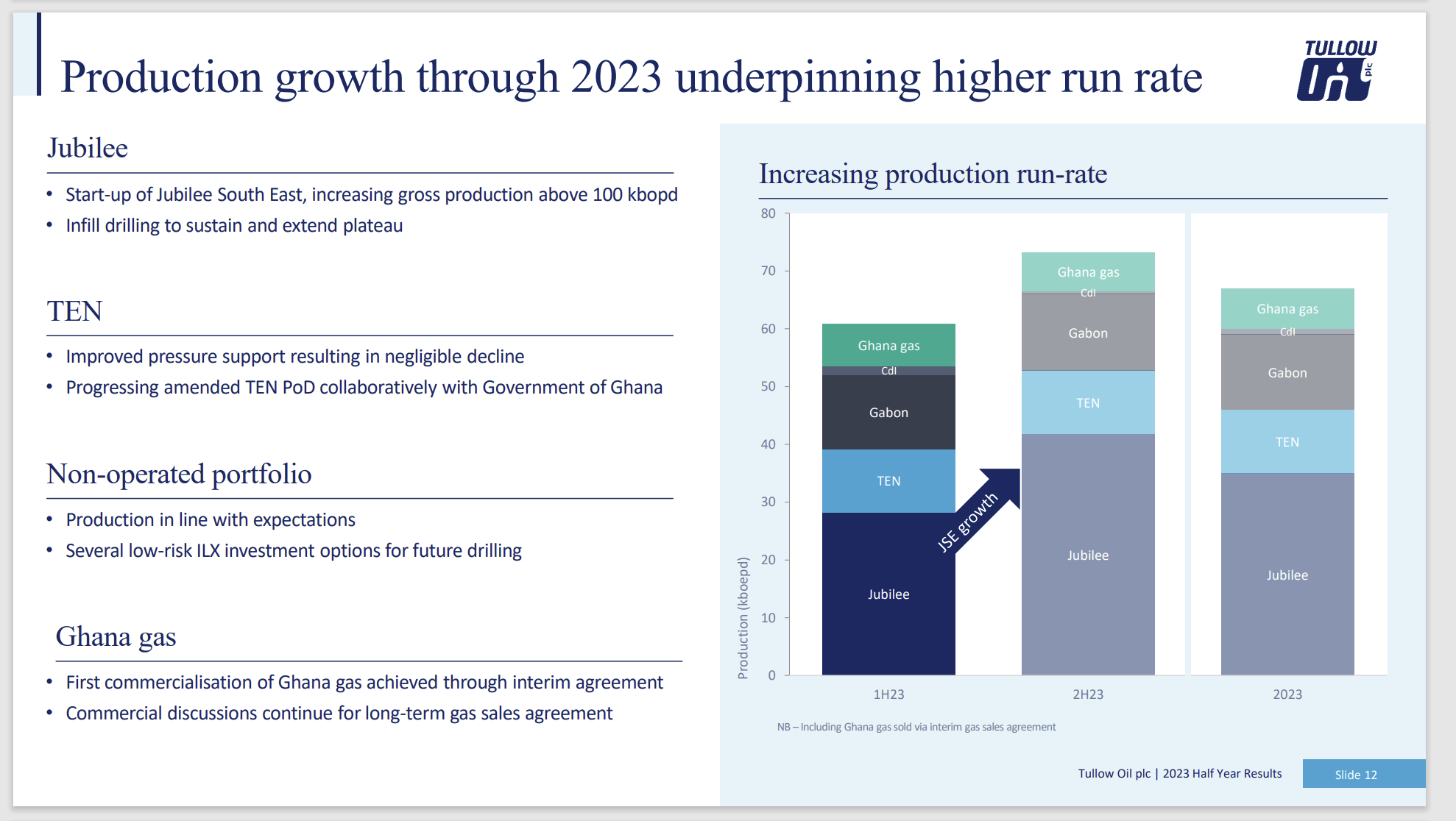

Tullow Ghana Production And Capital Plans (Tullow Corporate Presentation September 2023)

Management has plans to raise production because known areas of oil deposits often allow for some good returns. The company has operated in this area for some time with the Jubilee area producing most of the production. The rate of return on these long-lived wells is attractive. So, management, as shown above sees a way to materially increase production (and hence cash flow) to further improve cash flow and the debt ratio.

What has changed in the last few years is the decision by management to decrease the amount of high-risk exploration. Too much risk has led to about $1.9 billion in debt for the amount of production shown above.

This management has chosen a lot of low-risk projects that should raise production while selling noncore assets (defined as too much risk assets) in an attempt to strengthen the balance sheet (which improves company viability).

Since the current management is relatively new, managing future risk should be a higher priority than in the past. This will eventually lead to a safer investment. Right now, the financial leverage is on the high side. But it should continue to decline as management proceeds with the plan.

Fiscal year 2022 definitely aided anyone that needed to repay debt. Currently prices are still reasonable to aid anyone that needs to reduce debt. That should continue to be the case as there is not a lot of speculative money pouring into the industry that would lead to rampant growth signaling a cyclical downturn.

Now the industry is notoriously volatile and very low future visibility. But that volatility is likely to be between making money and making more money for the time being. Nonetheless it is essential for management to get the leverage down fast because of the volatility and low visibility. Then at least an unfortunate (and unforeseen) future event will not risk the company.

Risks

Long-time readers may remember that Tullow management seemed intent upon risking the company to find that one "home-run" discovery. This left the company in bad financial shape. Fiscal year 2021 saw a new management attempt to dig their way out of the mess the company was in. The term management uses is gearing which was all the way up at 2.6. This is the English version of a debt to equity ratio.

But the latest report in 2023, it was down to 1.7 due to a combination of activities including asset sales, production increases, a stock sale, and more. Fiscal year 2022 had prices that provided an unexpected boost to these efforts.

So, while management has made progress, the "gearing" is still pretty high and provides a financial risk that is absent from a lot of other investment choices, hence the hold rating. This management is accomplishing what few managements can do in turning around a company that was rapidly heading over a financial cliff.

Still, this is a small player in the offshore market where projects are generally large. Financing those projects will always be a challenge until this company gets larger with a far better exploration and development record than is the current case.

Any recovering company has a huge oil price risk. As good as the current recovery has been, the company needs helpful oil prices for at least another year or two. It looks like it will get it as well. But that is not assured.

Similarly, the management talent doing that turnaround is rare. The risk of any of that talent could prove fatal to the turnaround efforts.

Financial Ratings

Moody's has now put the company in its limited default classification because the debt repurchased for a material gain was classified as a distressed exchange. The cash flow for the first six months was less than $200 million with net debt at $1.9 billion. To say that finances are stretched would be an understatement. Another rating is CCC+ for the debt. All of this and more is on the financial statements. It was far worse two years ago.

Still the challenge is debt coming due before the turnaround is far enough along.

To improve the balance sheet and cash flow ratio the company has been selling assets, selling stock, and of course fiscal year 2022 saw unexpectedly robust cash flow (and selling prices for some assets). But the overall situation is between moderate and highly speculative at the current time.

The company is still working on the balance sheet, cash flow, and of course more income through drilling low risk wells. Free cash flow in this situation is negative. The future depends upon the speed of the recovery now underway (heavily).

Key Ideas

This investment is steadily moving from high risk to moderate risk as the debt ratio continues to decline. The next six-month report should continue to show progress if for no other reason than a fair amount of production will be coming online from a successful series of new wells.

This management is pursuing both production increases because they have some low-risk projects available as well as debt repayment. Management can hedge production to protect cash flow in the event that is needed.

This relatively new management is making good progress at reviving a company that was heading in the wrong direction. Nonetheless, it is likely too early to invest at the current time. A company like this has a fairly risky reputation. Therefore, it is very likely to take some time that risk reduction is now a core priority and value.

The new credit facility announced earlier this week is proof of that progress. Management was at the costlier end of credit back in 2021 if it could get it at all. But now it appears that "business as usual" is about to resume. Management needs to prove they won't be so debt happy and "risk-on". This is the beginning of that proof. The next step is to be able to refinance debt as the debt ratio continues to improve rather than having to repay debt as it comes due.

The new credit facility is also one of several parts to handle the fact that oil produced is stored and picked up periodically to get to market. That is different from onshore where oil is often assumed to be sold as soon as it heads into the pipeline. Rarely is onshore production stored for periodic pickup.

The market typically wants evidence and a public track record before giving management credit for the new risk strategy. If current commodity price remain in the range they are at as many predict, then all this company has to do is keep repaying debt while increasing production. Management made a lot of hard decisions early on that got the company in the current situation. The past could have been far worse for shareholders.

But nearly anyone in the industry doing balance sheet repair has a lagging stock price. The choice of offshore production in Africa adds more risk. This management is doing what it can to diversify production sources. But that part is not far along and is likely to be delayed as long as risk reduction is a priority (along with balance sheet repair.

While I like the progress being made, and I like the management as well. This investment idea needs to be watched for a better, less risky investment entry point. The chances of a "homerun" exploration well are nil while the focus on low risk-high return wells are the emphasis. However, that is likely to change once the company is in better shape and able to handle some risk.

For further details see:

Tullow Oil: Focus Now On Cash Flow And Profitability