LOVE - Tupperware Brands: Cheap For A Reason

- Tupperware Brands has been going through a tough time, prompting management to enter into a major turnaround initiative.

- Even with this in play, however, recent performance has been abysmal.

- Shares are cheap enough that they might result in a strong upside, but that's based on the unclear assumption that management can stabilize or improve operations.

Turnaround prospects can be some of the riskiest opportunities on the market. But at the same time, they can also offer some of the greatest upside potential. One interesting turnaround play to consider is Tupperware Brands ( TUP ), a company that focuses on a variety of storage-related products. For years, the company has been working to turn its operations around following declining sales. We have seen some improvement on the company's bottom line, but that has not extended into the current fiscal year. Economic conditions certainly muddy the waters here, but in defense of investors who buy into the stock, shares do look awfully cheap at this time. At the end of the day, this is an incredibly risky prospect that could very well create significant upside for investors. But given the fundamental performance of the company most recently, I do think there's a chance that this is a value trap instead of a great opportunity. And as such, investors should tread very cautiously moving forward.

An iconic brand that is in pain

Odds are, you have heard of Tupperware Brands before. Founded in 1946, the company made a name for itself with the food storage container that it produced. Today, the company has thousands of patents under its belt and it distributes its products into nearly 70 countries through 3.1 million independent sales force members across the globe. In addition to the storage units that it creates, the company also has other offerings such as lines of cookware, knives, microwave products, textiles, water filtration items, and more. Though this space may not seem like one that has a lot of opportunity for innovation, management has done well to invest in research and development activities.

In 2021, for instance, the company received multiple recognitions, such as the Fast Company’s 2021 Innovation by Design Awards and the Green Good Design Award from The Chicago Athenaeum for the creation of its Eco+ Coffee to Go Cup. The firm has also made other interesting products, such as the Universal Cookware set, which is a product line developed for small kitchens and spaces that includes a frying pan and two sizes of stockpots that, combined, take up the space of just one pot. The XtremAqua Freezable Bottle, meanwhile, is a high-impact resistant and freezer-proof solution for consumers on the go. It offers up to 8 hours of fridge fresh cool water when frozen.

{kind=link}

Author - SEC EDGAR Data

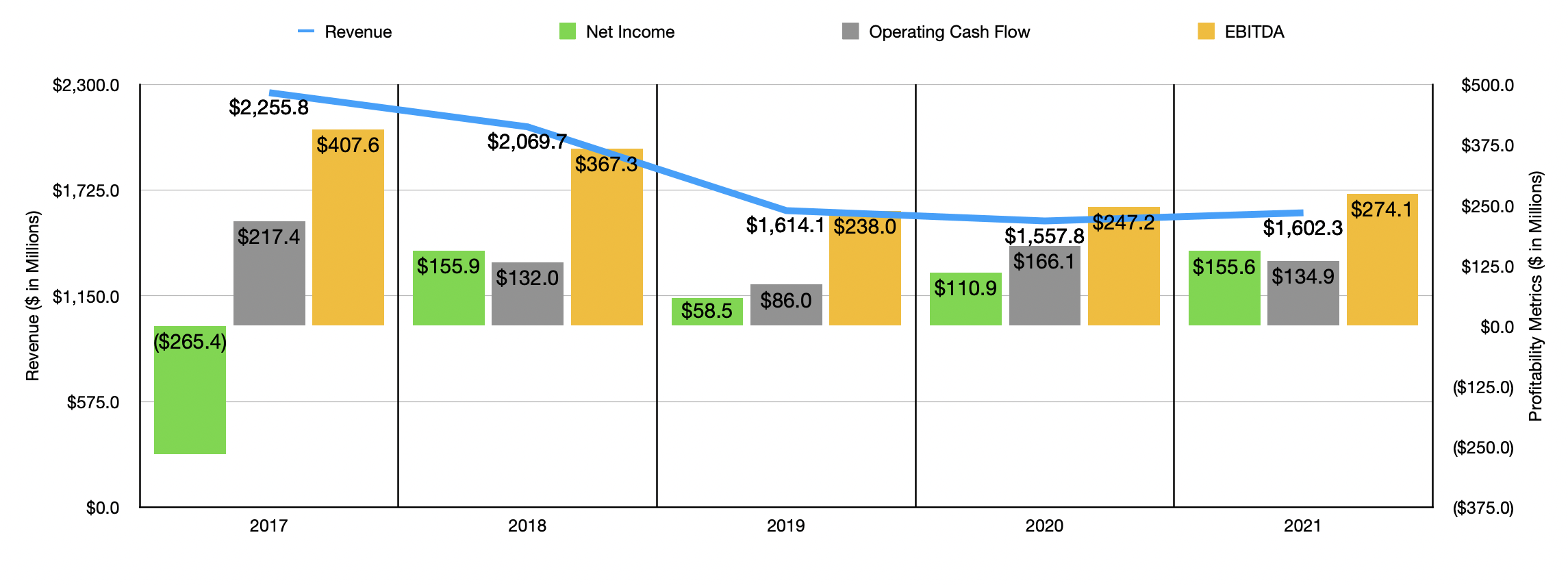

Despite these innovations, the company has struggled in recent years with declining revenue. Sales dropped from $2.26 billion in 2017 to $1.61 billion in 2019. The pandemic pushed sales down further to $1.56 billion in 2020. Many companies experienced a significant rebound in 2021 following the winding down of the pandemic. However, Tupperware Brands experienced only a modest increase in sales to $1.60 billion. Faced with these issues, the company embarked on a multi-year turnaround plan. This plan focused on specific key elements. For starters, the company decided to structurally fix its core business in order to create a more sustainable enterprise. It shifted from a distributor push model to a consumer pool model with the end goal of capturing the needs of today's consumers. It also involved getting its products in channels where today's consumers want to shop and expanding into new product categories, the latter of which plays in well with the company's strategy for innovating.

{kind=link}

Author - SEC EDGAR Data

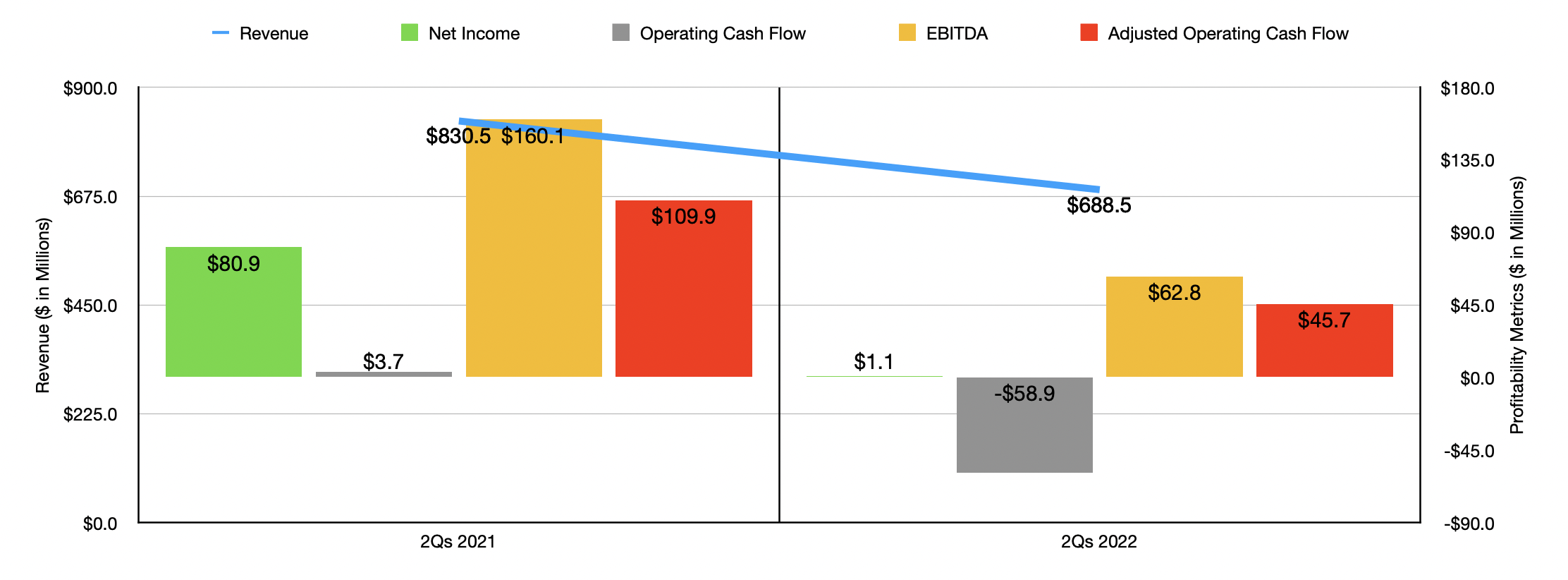

Unfortunately, none of this has stopped weakness in the current fiscal year. Revenue in the first half of 2022 came in at $688.5 million. This compares to the $830.5 million generated the same time last year. Although some of this decline was driven by foreign currency translation, there were larger factors at play. In North America, for instance, the company was negatively affected by lower sales force productivity caused by supply chain challenges and product backlog from the overselling of key promotional offers previously. Lower sales in Europe were driven by, amongst other factors, reduced consumer spending. This, in turn, was caused by higher inflation and higher gas prices. And in the Asia Pacific region, the company was impacted by lower recruiting and overall sales force activity thanks in large part to spikes of COVID-19 and lockdowns related to it.

To call the turnaround plan initiated by the company completely useless, we'd probably be a mistake though. The company went from generating a net loss of $265.4 million in 2017 to a profit of $155.9 million in 2018. Profitability then declined to $58.5 million in 2019 before almost doubling to $110.9 million in 2020. With the rise in sales, we also saw improved profitability in 2021, with net income climbing to $155.6 million. Other profitability metrics, meanwhile, happened to be rather volatile from year to year. But it is worth noting that adjusted operating cash flow rose from $138.2 million in 2020 to $182.3 million in 2021, while EBITDA increased from $288.2 million to a three-year high of $289.5 million last year. But once again, the current fiscal year has proven to be rather painful. Net income in the first half of the year was just $1.1 million. This compares to the $80.9 million generated the same time last year. Operating cash flow plunged from $3.7 million to negative $58.9 million. Even if we adjust for changes in working capital, it would have gone from $109.9 million to $45.7 million, while EBITDA declined from $160.1 million to $62.8 million.

{kind=link}

Author - SEC EDGAR Data

The only real guidance that management gave for the year involved earnings per share. This metric should come in at between $2.60 and $3.20. At the midpoint, that would imply net income of $128.9 million. Estimates I arrived at gave me adjusted operating cash flow of $151 million and EBITDA of $239.8 million. Using these figures, we can see that shares of the business are incredibly cheap at this point in time. The forward price to earnings multiple comes out to 4.2. That's up from a 3.4 using 2021 results. The price to adjusted operating cash flow multiple, meanwhile, should be 3.6. That compares to the 2.9 reading using last year's figures. And when it comes to the EV to EBITDA approach, the multiple is 4.7. If we were to use the data from 2021, it would be slightly lower at 3.9. As part of this analysis, I compared the company to the four firms that were most similar to it that I could identify. But of course, none of these are perfect comparables. On a price-to-earnings basis, these companies range from a low of 5 to a high of 11.4. Using the price to operating cash flow approach, the range was from 6.8 to 23.3. And using the EV to EBITDA approach, the range was from 7.1 to 10. In all three scenarios, Tupperware Brands was the cheapest of the group.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Tupperware Brands |

| 4.2 |

| 3.6 |

| 4.7 |

| Lifetime Brands ( LCUT ) |

| 10.2 |

| N/A |

| 7.7 |

| Newell Brands ( NWL ) |

| 11.2 |

| 13.6 |

| 10.0 |

| The Lovesac Company ( LOVE ) |

| 11.4 |

| 23.3 |

| 7.6 |

| The Container Store Group ( TCS ) |

| 5.0 |

| 6.8 |

| 7.1 |

Takeaway

Over the past few years, Tupperware Brands has struggled from a revenue perspective. Having said that, the company has recently, at least prior to this year, shown some improvement in its bottom line. Unfortunately, that was short-lived because of recent weakness the company has experienced. While it is entirely possible that the business could turn its operations around further and weather this storm, and shares are cheap enough to offer tremendous upside if all goes well, it's also true that the future for the company is uncertain and that investors would be wise to tread carefully since the picture could always worsen from here.

For further details see:

Tupperware Brands: Cheap For A Reason