TUP - Tupperware Brands: No Evidence In Sight Of Turnaround Even At 0.08x Sales

2023-12-28 22:52:35 ET

Summary

- The case for buying Tupperware Brands has emerged once again after renegotiating its credit terms.

- The company has experienced lost 98% of its market value over the past decade after a string of upsets.

- TUP's withholding of financial statements for over 12 months limits the ability to assess its financial position and potential for a turnaround, supporting a neutral stance.

Investment briefing

The scope for rotating capital to beaten down consumer-based companies has broadened into 2024 on the combination of 1) increased market breadth and 2) stretched valuations in mega-cap names that dominate the major indices.

Tupperware Brands ( TUP ) falls under the banner of 'beaten down consumer-based company'. Tupperware is likely a household name and came along just like any other consumer products company, disrupting a relatively stale, yet concentrated industry in plastics. TUP's iconic plastic food storage containers of the same brand changed the face of sales, and lifted the watermark on home food storage. The famous 'Tupperware parties' sold Tupperware plastics under a party plan, multi-level marketing ("MLM") model, a tradition that continues firmly today. After holding an expansive industry position for decades, new technology and immediate competition means TUP's offerings are undifferentiated to an extent and there are arguably even superior offerings out there today based on objective criteria.

Still, TUP presents with an interesting set of investment facts to build a strategy around, having negotiated terms with creditors for the 6th time now, notwithstanding pressure from intense competition, lacklustre earnings and poor capital allocation decisions over the years.

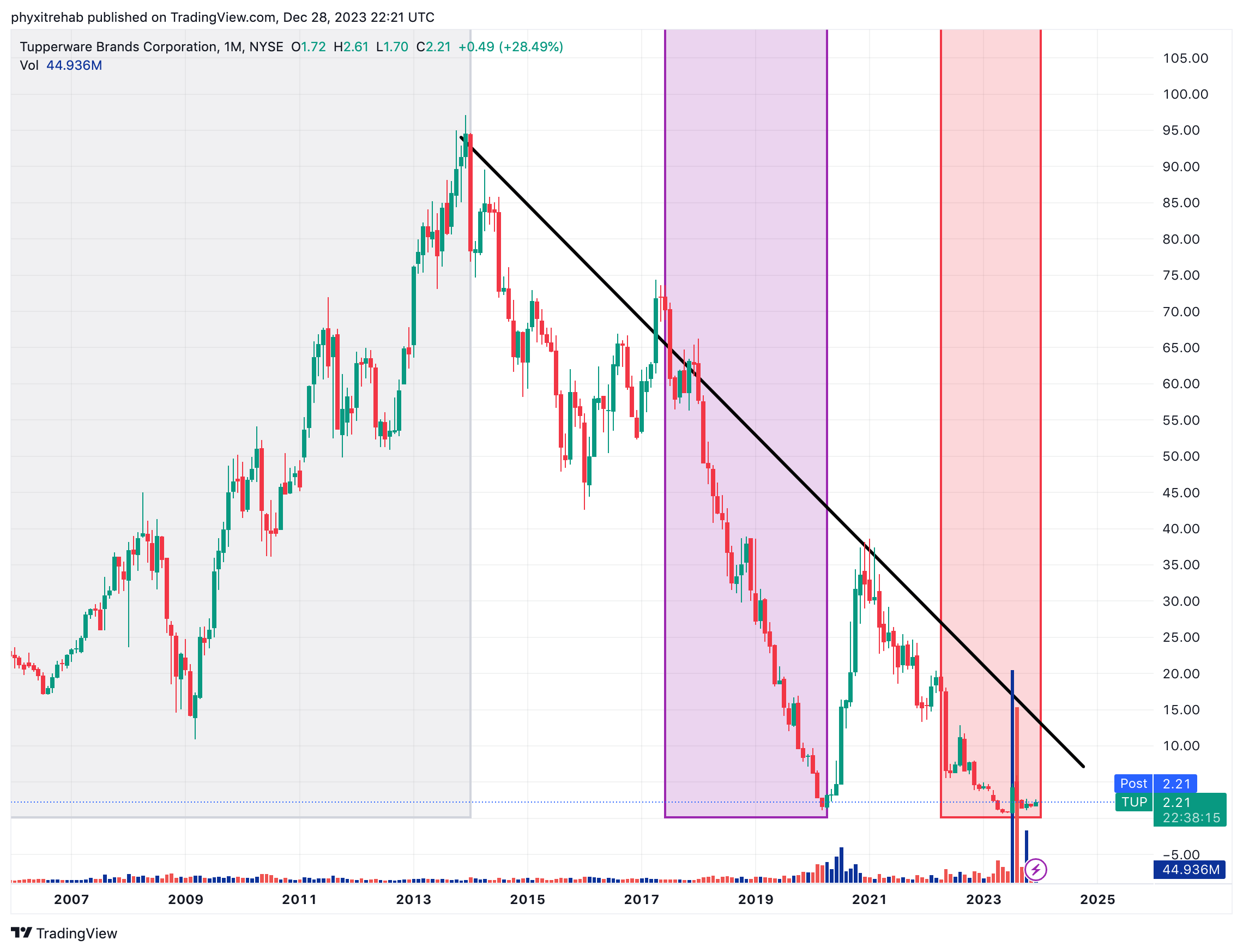

Investment arguments are stacked on both sides of the book, as one could position both long and short here with compelling evidence on either side of the trade. However, one cannot overlook the decline of TUP's market value in the last 10 years— one of simply epic proportions. Figure 1 illustrates the moves over TUP's lifecycle as a public company since the mid 90's. TUP created immense wealth for its owners over the early 00's to mid 10's, advancing from $12 to its top of $96 by January '14. Critically, it has never retaken this high.

In fact, shareholders have been fleeced not once, but twice since then. The market has subsequently wiped out more than 98% of the company's market value off TUP's all time high after a string of uninspiring developments that have weakened the company's balance sheet. The risk now is that TUP is delisted from the NYSE, where its issues will then trade over the counter ("OTC") or even in the 'expert market'. Seeking Alpha analyst WYCO Researcher does an excellent job of explaining this—along with the remainder of the TUP story—in easy to understand terms, paying close attention to the key issues. I would encourage all to read this report as an addition to what's presented here today ( click here to read it).

Recent updates in the TUP investment debate mean a serious and thoughtful appraisal as warranted to understand (i) what the critical risk factors and (ii) what value is on offer. This report will present the key investment findings and make recommendations on positioning based on various risk appetite and return objectives.

Net-net, after weighing in all of the contributing factors, I rate TUP a hold, and do not believe in the notion of a sharp turnaround within the next 12–18 months.

Figure 1. Tremendous revaluation from highs of $96 to the $2s at the time of writing ( arithmetic scale ).

{kind=link}

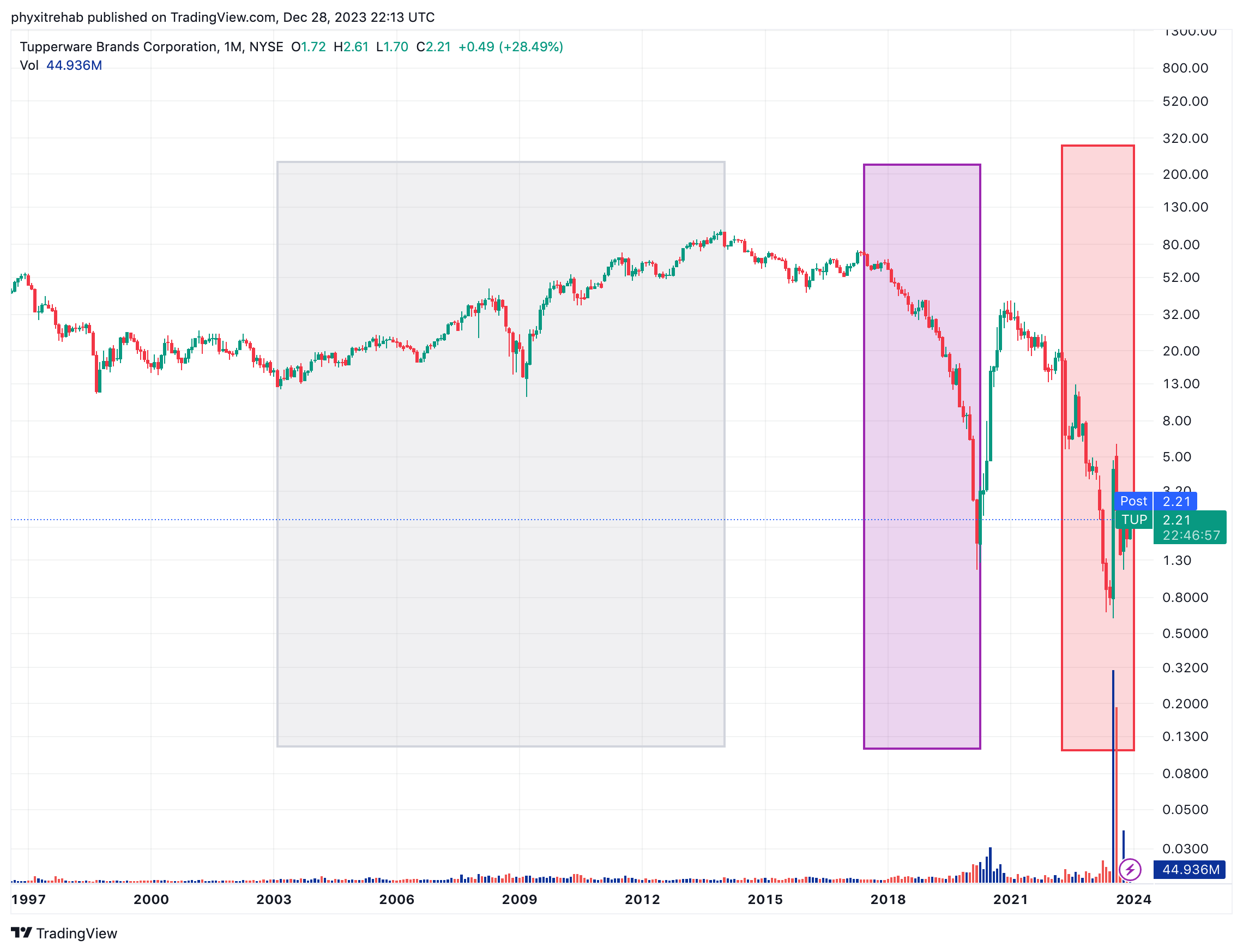

Figure 1a. TUP share price evolution ( Log scale ).

{kind=link}

Critical facts forming hold thesis

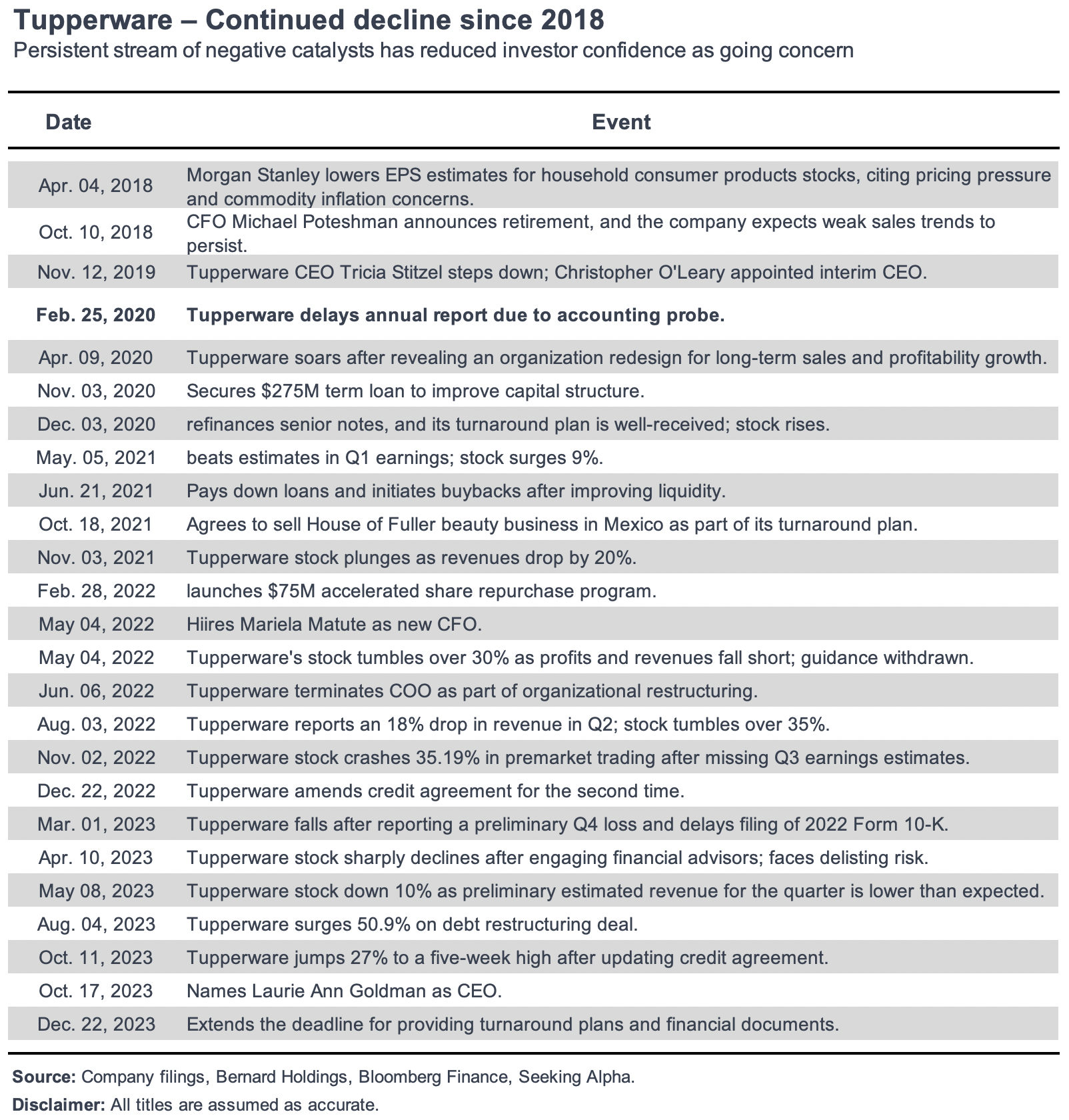

Just like Lemony Snicket in Daniel Handler's novels, it has been a series of unfortunate events for TUP. Dating back to at least 2018 in fact. One simply has to go back to the infamous trade wars of 2018, which reduced international trade by 65% according to the United States International Trade Commission. The market for household consumer goods was disproportionally impacted by the tariffs, as commodity inflation became a concern along with margin pressures from the same. Morgan Stanley (MS) downgraded the sector in '18 as a reflection of this.

In the next 18 months, both TUP's CEO and CFO stepped down, after which an accounting probe is started into its Fuller Mexico beauty business. In my opinion, this opened the can of worms for the company, as a string of challenges emerged in the time since this probe.

According to TUP at the time in 2020:

The Company is conducting an investigation primarily into the accounting for accounts payable and accrued liabilities at its Fuller Mexico beauty business to determine the extent to which these matters may further impact results and to assess and enhance the effectiveness of internal controls at this business.

Immediately afterwards, it was regarding capital structure and operating as a going concern:

Based on the 2020 outlook, the Company is forecasting a need for relief concerning its existing leverage ratio covenant in its $650 million Credit Agreement dated March 29, 2019, to avoid a potential acceleration of the debt, which could have a material adverse impact on the Company.

A full list of relevant events from 2018 to date is noted in Figure 2, below.

Figure 2.

{kind=link}

This is an exhaustive list that points to operational turmoil in my opinion. The company received a lifeline in August this year after is negotiated with creditors to keep itself out of a Chapter 11. bankruptcy filing. This was followed by two more amendments to the credit agreements which potentially strengthened the balance sheet and allowed for working capital and additional liquidity to be obtained.

Normally, you'd see a stock fly on such news, especially if the underlying or core business (in this case, the Tupperware branded business) has some flesh to put on the skeleton, once other assets had been decapitalized for cash to meet the financial obligations.

But TUP's case is unique in two critical ways:

- The company has not filed ANY of its accounts or financial statements since Q3 CY 2022 — over 12 months without any indication of the company's financial position;

- Investors must wait until February 2nd, 2024, for its financials and the status of its turnaround efforts.

Investors are in effect flying blind in buying TUP at this stage as there is literally no evidence of the company's economic record of recent business. Would you buy any asset without being able to scrutinize it in full first? This would be no difference I'd presume.

Furthermore, the notion of withholding accounts for over 12 months is, quite frankly, ridiculous. The market's wisdom posits that it can 'see the wood from the trees' as it were, discounting as much of the known information as possible into a market value. By virtue of withholding financials it will clearly decipher there is something bubbling underneath the lid. This explains in granular detail the extent of TUP's selloff in the last 3 years.

Forensics on Fundamentals

For what numbers we do have up until 2022, the picture is bleak. The company embarked on its 'turnaround' in 2020 and again in 2021, but this has been delayed for what seems indefinitely, especially without any company filings to work from.

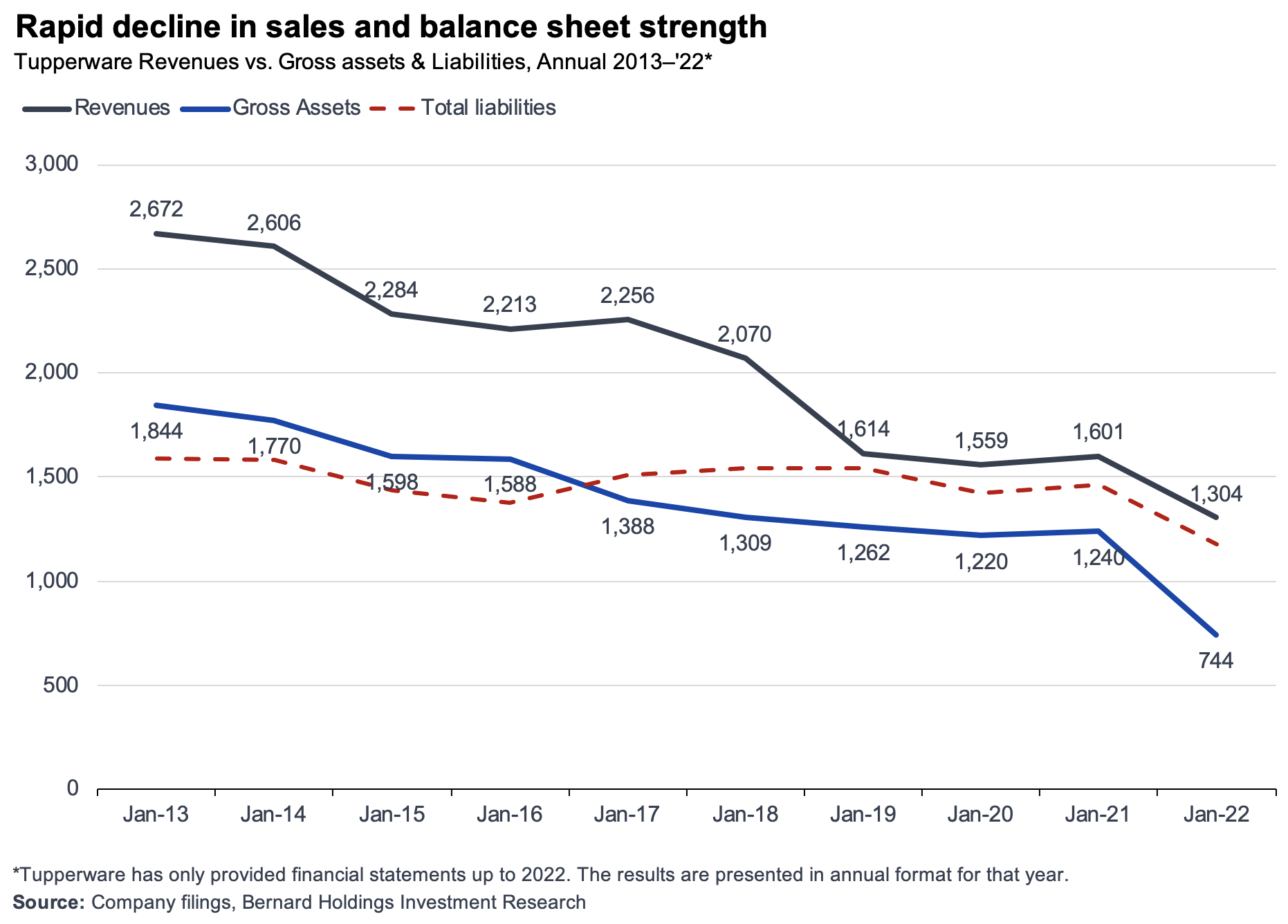

Revenue and asset growth

Both the company's revenues and capitalized asset value has drifted lower at a consistent gradient from 2013–2022, as seen in Figure 4. Total liabilities have been flat in response to this, substantially weakening the balance sheet for both equity holders and creditors. As of late 2022, the company did $1.3Bn in trailing 12 month sales, and held $744mm of assets against $1.17Bn of liabilities, therefore running negative equity of $430mm and therefore would be technically insolvent had it not been for the amendments to its credit terms made across 2023.

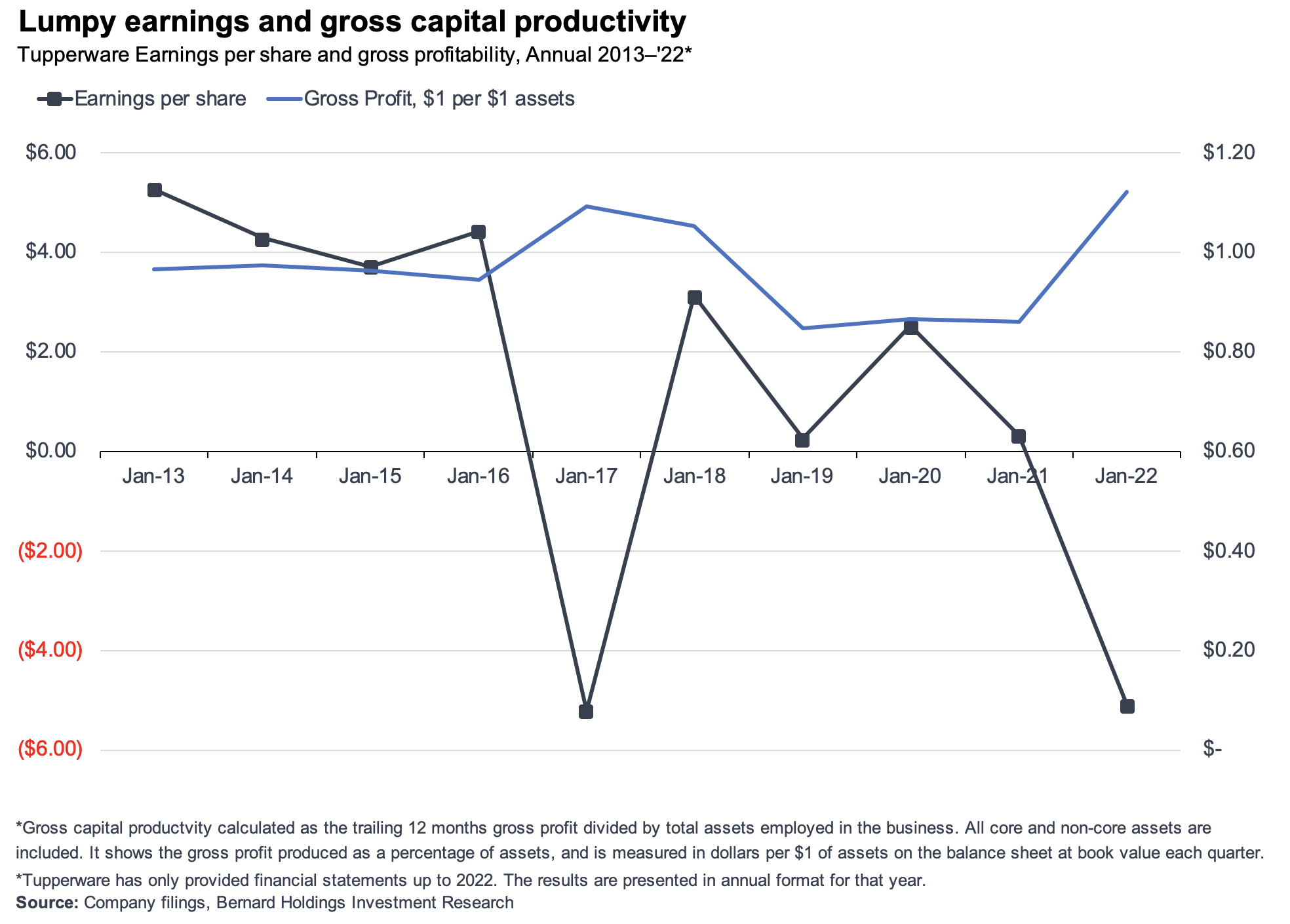

As a positive, the company does typically rotate $0.85–$0.9 on the dollar in gross profit per $1 of assets employed on the balance sheet. For those seeking asset efficiency, this may be the place to look if the fundamentals start to fall into line. February is therefore an absolutely crucial month to observe where TUP stands financially, and what the next moves may be.

Statistical discount?

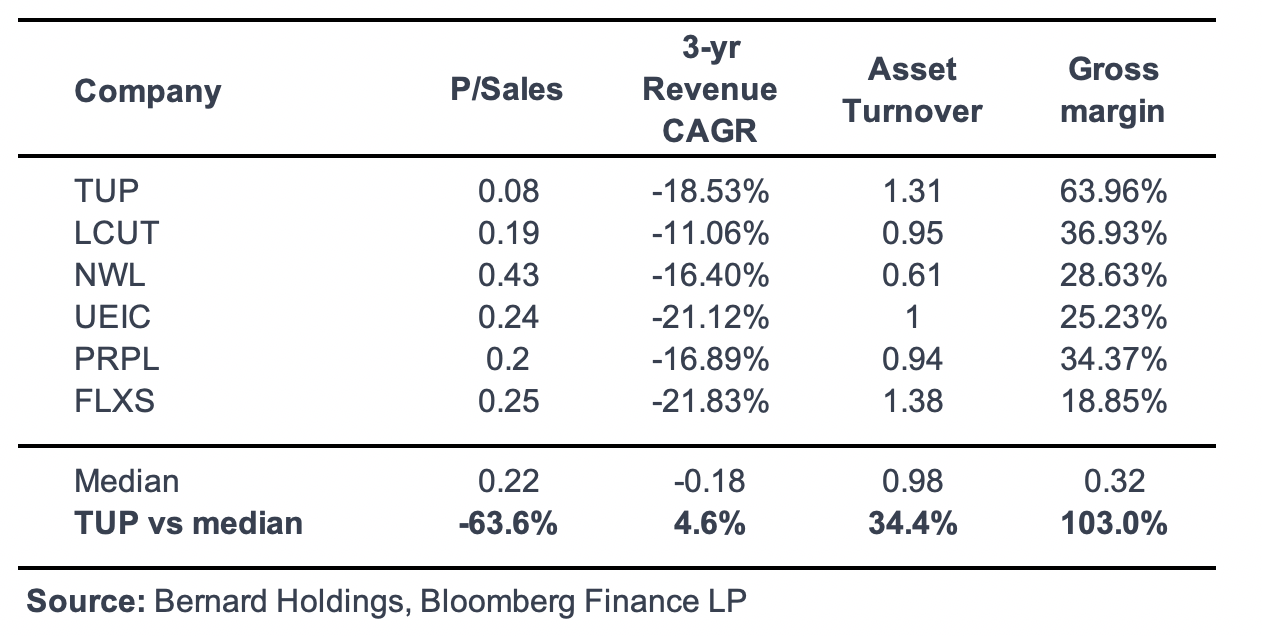

There is also the notion of buying TUP at obscenely compressed valuations and playing a turn in the stock price from renewed investor confidence after its 6th credit amendment. One could have made money this way in buying and selling TUP over the last 18 months. It currently sells at 0.08x trailing sales , and 8x EV/EBIT, about as cheap as it gets in the world of buying and selling investment securities. Buffett's "cigar butt" adage comes to mind here; however, this is not an investment strategy employed by our firm or this channel. We'd rather buy higher growth businesses with excellent growth prospects. Also, consider that for this to work from a risk/reward perspective, you'd need to (i) run this position in size, and (ii) the market to agree with you.

Figure 3.

{kind=link}

My thoughts on this are precisely as follows:

- If the turnaround is deemed to be unsuccessful TUP's will likely be a major takeover candidate. There is an exhaustive list of contenders.

- Another negative equity position could see creditors siphon off key assets to recover the capital that has been provided to this company—more than $1.17Bn of debt capital, and $1.1Bn of equity in pain in capital and retained earnings as of the last filing in 2022.

- Equity holders would likely not be considered a priority given the capital structure and new covenants in place (given we are residual claimants anyway)

- The scope for any business development, growth, or capital allocation elsewhere is therefore severely narrowed outside of reducing debt principle, limiting the scope for long-term capital gains.

Combined these four points misalign with the tenets of buying fantastic companies who are unfortunately mispriced, thereby offering an opportunity. Instead, it would appear the market's pessimism is vindicated on TUP.

Figure 4.

{kind=link}

Figure 5.

{kind=link}

Conclusion

Legendary investors of all creed have made obscene sums of money in identifying incorrectly beaten down companies with excellent underlying business characteristics. There is in fact superb returns to be made in such instances, especially in irrational markets, which, arguably, we are still within right now. The issue for TUP is the quality of the underlying assets forming the business. We measure this in financial terms, typically in sales and earnings growth, but also returns on capital and capital turnover and so forth. We haven't had a set of audited accounts from TUP in over 12 months now, so any judgement on the company's profitability, financial position, let alone forward outlook, is riddled with assumptions vs. tangible evidence.

Consequently, my investment cortex is warning me against this, flashing the lack of asymmetrical risk reward calculus as the primary reasoning before my eyes. There are simply far more selective opportunities with similar risk in the universe at this point in time. Net-net, rate hold.

For further details see:

Tupperware Brands: No Evidence In Sight Of Turnaround, Even At 0.08x Sales