KHOLY - TUR: What Awaits The Best Performing 2022 Country ETF

Summary

- The BIST had an extraordinary performance to the year's end, and the TUR ETF has almost doubled in 2022.

- Despite the stellar stock market gains and relatively stable Lira, the Turkish economy's fundamentals are alarming as inflation hits almost triple digits.

- The current high inflation - low yield environment leave the stock market as the only viable option for ordinary Turks to park their savings.

- Although I expect the current momentum to continue in the short term, I think Erdogan's unorthodox policies are not sustainable and will eventually fail.

In April 2021, I published an article about iShares MSCI Turkey ETF ( TUR ) that took a bearish stance due to fleeing foreign investors, and my bear case held well until the summer of 2022. Despite the Turkish economy severely deteriorating in 2022 with record-breaking, triple-digit inflation figures not seen for over two decades, the Turkish stock market had a stellar year. The TUR ETF significantly outperformed all other country ETFs by a substantial margin, almost doubling in value.

In this article, I will explain Turkey's current economic and political issues and Erdogan's unorthodox solution to economic headwinds to identify if this remarkable bull rally can continue.

TUR began its rally in the summer of 2022 alongside other developed and emerging market countries. However, as these other markets flattened, the Turkish stock market skyrocketed. While there is no fundamental explanation for the positive divergence of Turkish equities from their peers, Erdogan's unorthodox monetary policies created a huge demand that propelled the Turkish stock market. TUR has finally broken its 10-year negative trend and is currently the top-performing country ETF year to date.

Erdogan's Unorthodox Solution

For the past decade, Turkey has been grappling with a persistent issue of currency depreciation. In the past, the central bank has tried to stabilize the currency by enticing foreign investors with high-interest rates. However, Erdogan has long been at odds with these high rates, believing that they are the root cause of inflation and are pushed by the so-called "Interest Lobby". Erdogan's unorthodox economic policy takes a contrarian approach, arguing that countries should actually lower interest rates to combat rising inflation. This theory suggests that lower rates can create a positive feedback loop that helps to curb inflation. While this theory goes against established economic principles, Erdogan has fully implemented these unconventional policies in recent years. Unfortunately, these unorthodox monetary policies don't mesh well with open market policies, and foreign capital tends to flee such regimes.

As a result, foreign capital has been fleeing Turkey, leading to extreme depreciation of the Lira in 2021 and early 2022. The weakening lira has led to the dollarization of the Turkish economy, as both businesses and individuals have held onto foreign cash reserves. The increased demand for foreign currencies has created a vicious cycle for the Lira.

The government had to stop dollarization and stabilize the local currency, but it required dry powder, and Erdogan introduced a solution to fuel his "Lirarization" plan. He secured new credit lines from Qatar , Russia , and Erdogan's former adversaries, the UAE and the Saudi Kingdom , to provide the financial resources for this new strategy. These credit lines would help to kickstart and fuel this unconventional monetary approach.

On the other hand, the government had to limit the influence of the offshore market on the Lira to maximize its control. The severe depreciation of the Lira and lowered interest rates did much of the work, but the government also took various official and unofficial financial measures and regulations. These included increasing cross-currency interest rates, restricting locals' access to supranational bonds, and limiting Turkish banks' issuance and positions of derivative positions to short the Lira. The banking regulations institution, BDDK, played a role in this effort, as did unofficial pressures from the central bank to limit high-volume transactions after 4 pm. These measures made it more difficult for offshore markets and foreign players, but for anyone in general, to take speculative positions against the Lira or short it for prolonged periods.

To limit domestic demand for foreign currencies, Erdogan introduced various new regulations. The most significant measure was the introduction of KKM "FX Linked Deposits". KKM was the first prominent step in the "Lirarization" campaign, which aimed to increase demand for the Lira by incentivizing lira deposits but at a dire cost to the Treasury. Basically, it is a saving deposit with a free option granted to the investor to buy FX at the exercise date at the currency exchange rate of the initiation date. The Central Bank bears the risk of the option, but it has the potential to turn into a vicious cycle if the Lira significantly depreciates. The Central Bank would owe more money, which would create more Lira supply to pay its debt, and that leads to higher currency depreciation due to more supply which leads to higher payouts again.

On the other hand, Turkish corporations were "incentivized" (or, in some cases, forced) to exchange their foreign deposits for "FX Linked Deposits", further advancing the "Lirarization" movement. Finally, new banking regulations required Turkish banks to hold higher lira deposits, further strengthening demand for the currency. While doing all the other interventions, the Central Bank used the cash they obtained from the countries via credit to fuel all these operations and hold the currency stable via direct market interventions. Overall, the "Lirarization" campaign has been successful for now, as the Lira remained stable in the second half of 2022.

Stocks - The Only Option For Ordinary Turks

Despite the stability of the Lira with the "Lirarization" campaign, inflation soared to extreme levels due to the severely depreciated currency and global inflation in the past year. According to official figures, YoY inflation was 84.4% in November, but reputable sources such as ENAG estimate that it was much higher, at over 185%. Previously, ordinary Turks had used foreign deposits to keep up with rising inflation. However, as the currency stabilized, people began looking for alternative strategies to fight extreme inflation.

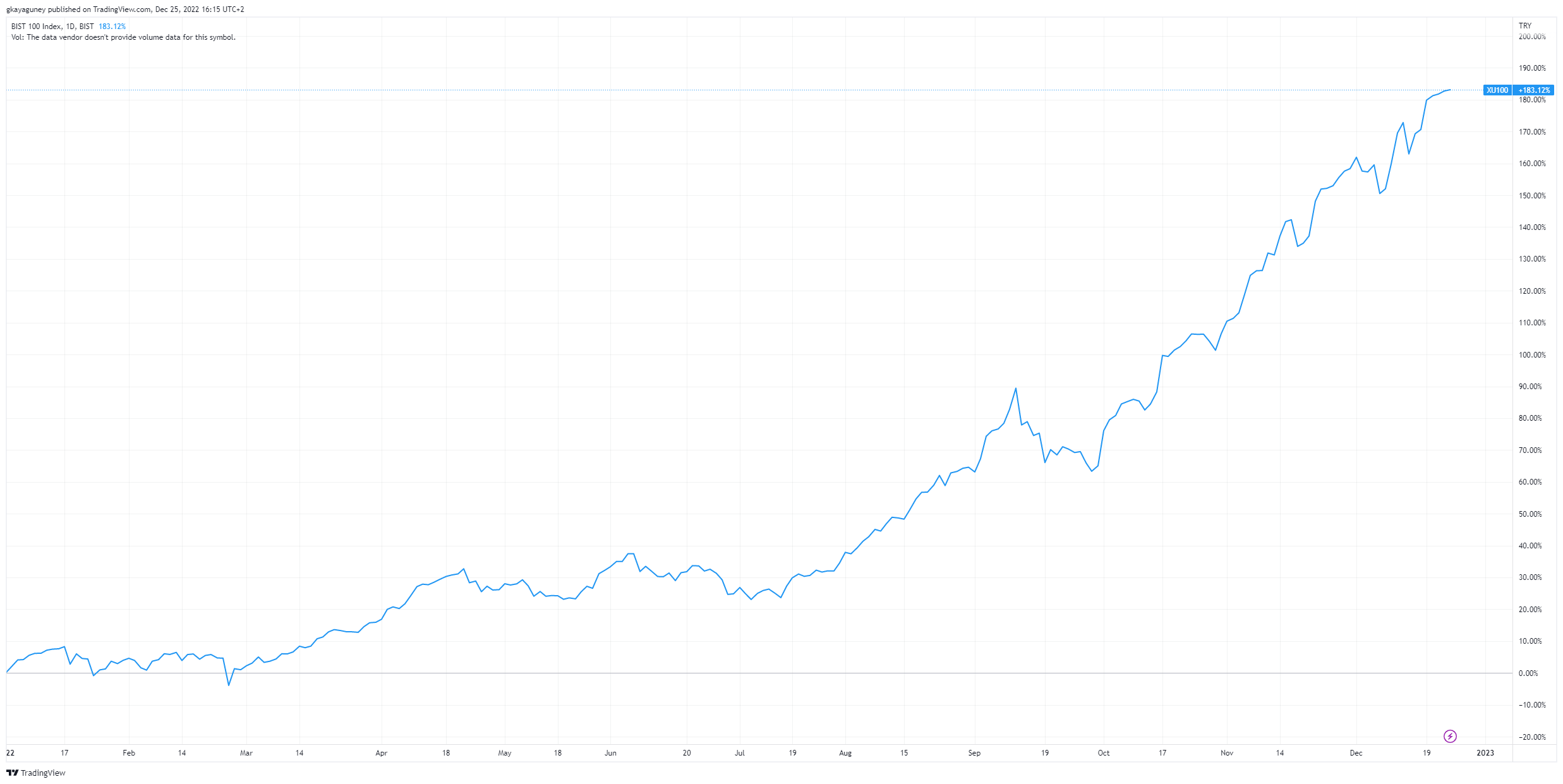

The high inflation led to record-breaking revenues and profits for companies, and the Turkish stock market (BIST) soared as soon as financial results were announced. The middle class, seeking alternatives to holding foreign deposits with minimal interest, rushed into the stock market. In 2022, more than 1.2 million people who had never invested in the stock market joined. It is an increase of over 50% in the number of individual investors, which now stands at 3.6 million. As a result of this demand, the BIST 100 index, which includes the top 100 companies listed on the Istanbul Stock Exchange, rose by over 180% in Turkish Lira and over 100% in US dollars.

{kind=link}

Source: Tradingview

It Will Work Until It Does Not

The Turkish stock market has seen a significant influx of domestic investors due to the lack of alternative investment options and cheap interest rates on the Lira. Many ordinary Turks have taken out consumer loans to leverage their positions in the stock market, and the widespread use of this tactic has led government officials to issue warnings about its risks. Additionally, the middle class has taken advantage of cash advances on their credit cards with affordable loans, further increasing their leverage. Those familiar with history can recognize the unsustainable nature of this trend, which is likely to lead to a market bubble and an inevitable crash.

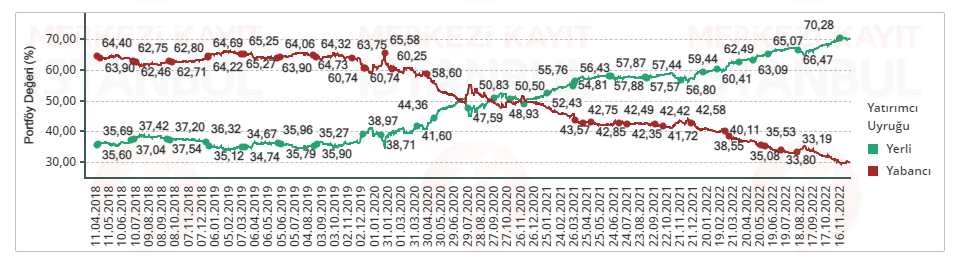

Currently, ordinary Turks make up the majority of the stock market, with foreign investment representing a decreasing portion. In the past, the foreign investment made up around 60-65% of the market, while domestic investment accounted for 40-35%. However, domestic investment now makes up over 70% of the market, and the gap continues to widen. Due to insufficient foreign investors to adjust prices and limited tools to take positions against the market, the bullish trend is likely to continue.

{kind=link}

Source: VAP

The Bull Case Argument

Recently, the minimum wage was increased for the second time this year by 55% to 8500 Lira, which is around $445. This massive increase in working-class wages will inevitably push inflation higher in early 2023, even if the Lira remains stable. As the middle class is the main driving force behind the market, people will likely reinvest their extra income into the stock market, further fueling the rally. However, this also creates a potential risk for investors as it may contribute to a market bubble.

Elections Create Uncertainty

The stock market continues to reach new highs every day, but high inflation is the word on the streets. Elections are scheduled to take place on June 2023. The impact of inflation is already being reflected in polls as Erdogan's support is at historically low levels. After twenty years in power, many believe elections will be fierce, as Erdogan will not go down without a fight. We have already seen Erdogan take anti-democratic measures to secure victory, such as sentencing the mayor of Istanbul, Imamoglu, who defeated the AKP in previous elections, to two years in prison. Although Imamoglu may not ultimately go to jail, the sentence means a political ban from elections. As the elections draw closer, many believe that Erdogan may increase his use of anti-democratic measures in an attempt to win. Elections bear a high risk that is difficult to quantify, as Erdogan is likely to do whatever it takes to emerge victorious in my opinion.

Conclusion

To conclude, Erdogan's unorthodox economic policy has successfully decreased domestic demand for FX and ultimately created a virtuous cycle for the stock market. However, the bull rally may have dire consequences for new investors as it is likely not backed by institutional investors but by inexperienced retail investor hype. While I believe the current rally is poised to continue in the short term due to increased wages, investors should be aware of the unparalleled risk posed by the upcoming elections. Additionally, inexperienced retail investors who are the backbone of the rally may flee the markets when faced with the slightest headwinds. Investors should consider these factors when making investment decisions.

For further details see:

TUR: What Awaits The Best Performing 2022 Country ETF