TKC - Turkcell Q2 Review: Exceeding Expectations On Every Front

2023-08-18 17:03:43 ET

Summary

- Turkcell's Q2 earnings showed impressive growth, outpacing inflation and industry benchmarks.

- The company's postpaid mobile business performed exceptionally well, surpassing expectations and outpacing inflation.

- Turkcell's improved balance sheet, cash flow, and FX position indicate the potential for increased shareholder returns.

I am revisiting my Q1 thesis on Turkcell Iletisim Hizmetleri A.S. ( TKC ) in light of Q2 earnings.

Looking back on my Q1 analysis, I was bullish on Turkcell with a buy recommendation. Three key factors played into my recommendation. First and foremost, Q1 earnings showed impressive growth across the business. Growth was especially strong in high-margin businesses like postpaid wireless and business services. Second, the business accelerated past the inflation rate for revenue and net income while improving its FX position. Finally, valuations were depressed relative to the industry and historical averages, and increased shareholder returns would become possible as cash flow continued to improve.

My downside concerns were around continued inflation growth that Turkcell could not outpace and a continued devaluation in the Turkish Lira.

Since publication, Turkcell is up more than 17% and has reported very favorable Q2 earnings . In addition, management raised earnings guidance for the balance of the year.

Postpaid growth, on both rate and volume, outperformed my expectations in Q2, and overall revenue outpaced inflation by nearly double while the EBITDA margin improved. The balance sheet and cash flow position improved, and while the Lira continues to devalue, Turkcell actually improved its FX position. Lastly, valuation multiples continue to be depressed despite the recent run-up in stock price.

With Turkcell meeting or exceeding every point in my Q1 thesis, I continue to believe there is an upside to the stock, even at a higher price, and maintain my buy rating.

Turkcell Continues Outpacing Inflation And Industry

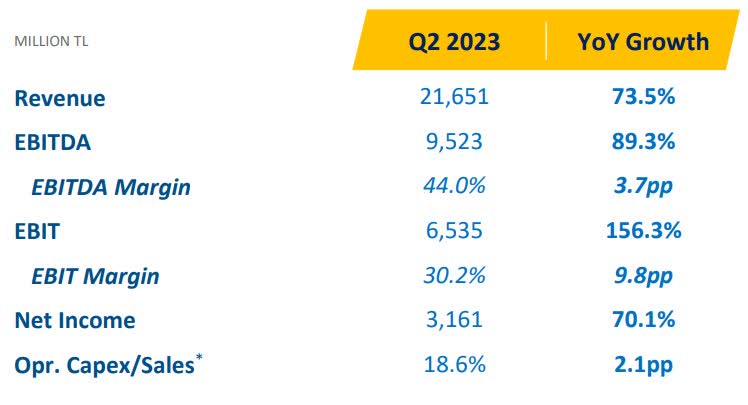

The average inflation rate in Turkey for Q2 2023 was right around 40%. Compare that with the impressive revenue growth, EBITDA growth, Net Income growth, and margin improvement Turkcell delivered.

{kind=link}

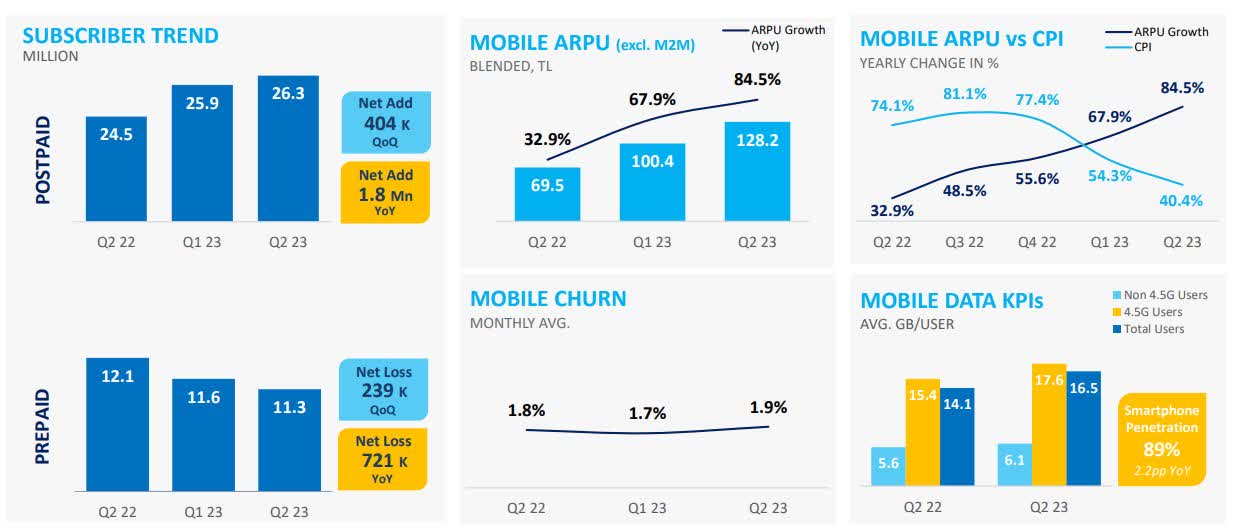

Not only was the P&L strong, but the underlying metrics in its primary business, Postpaid mobile, were strong across the board. Mobile ARPU especially began outpacing inflation in Q1 2023, but surged ahead in Q2 2023. From the earnings call , management believes that additional pricing action is possible through the balance of the year, and was a factor in the revised earnings guidance.

{kind=link}

Turkcell also performed better than its primary competitors, Vodafone and Turk Telecom. Vodafone's Turkey business delivered 384,000 net adds versus Turkcell's 404,000. They were also 10ppt behind on ARPU growth. Turk Telecom went backward by 9,000 mobile subscribers and could not keep up with inflation.

Turkcell also drives growth in its high-margin businesses, as detailed in the earnings deck . Postpaid mobile is almost double inflation, residential fiber is up 48.6%, digital services are up over 80%, and tech fin is up 85-95% across the business. While still a smaller part of the portfolio, I am excited to see the growth in higher-margin products and services while also managing to grow ARPU within each category.

Increased Shareholder Returns Are In Sight

Turkcell has had an erratic dividend history as it struggled with inflation and economic impacts. Historically, the dividend was more frequent and more substantial. With improvements in FX, cash flow, and balance sheet, I see the potential for a return to historical levels of investment.

{kind=link}

Despite the devaluation in the Turkish Lira, Turkcell improved its FX position and put it in the green for the first time in several quarters. They continue to maintain an aggressive hedging strategy, primarily with proxy hedges. This aggressive and so far successful FX management is a strong signal to me that currency risk is manageable.

Q2 2023 FX Position (TKC Investor Relations)

Improved cash flow has also started to shore up the balance sheet.

Q2 2023 Balance Sheet (TKC Investor Relations)

Cash on hand and cash flow now rival years when the dividend payout was 2 to 3x what it is today, with the operation generating more cash and investments absorbing less cash. I believe as the balance sheet continues to improve, shareholder returns will increase by more than has been priced in.

Multiple Signals For Undervaluation

Valuation multiples continue to be depressed nearly across the board. Earnings and profitability metrics are especially compelling, earning A ratings across the board. Normalizing P/E GAAP ((TTM)) to the industry would peg TKC at $12/share.

TKC Valuation Multiples (Seeking Alpha)

The quant rating is equally bullish. While it shows a Hold at the moment, favorable marks across valuation, growth, profitability, and momentum are weighed down by revisions that don't seem to have considered the revised earnings guidance.

{kind=link}

Sell-side ratings present a strong buy recommendation with a $5.00 price target.

While historical stock price is not always a perfect indicator, let's look at how Turkcell performed when the dividend yield peaked. When Turkcell paid a $0.20 dividend in 2H 2019 , the share price ran, on average, in the high $5s.

Even at the low end, $5.75 / share represents over 20% upside to the share price, in addition to what I believe will be a higher dividend yield.

Downside Risk

While Turkcell demonstrates promising dynamics, investing in it is not without risk. One of the most pressing concerns is the ongoing devaluation of the Turkish Lira . Turkcell has large debt obligations denominated in US currency due in FY25 ($950 million) and FY27 ($888 million). While they continue focusing on and improving FX exposure with a derivative portfolio, currency risk remains.

Another key risk is the potential loss of momentum. Turkcell's impressive performance has been driven by robust postpaid growth. However, sustaining this level of growth over the longer term can be challenging. Like any company, Turkcell is susceptible to market fluctuations and changes in consumer behavior. A slowdown in the Turkish telecommunications industry or evolving consumer preferences could lead to losing momentum.

Verdict

Turkcell's impressive second-quarter earnings report outpaced the industry. Management hasn't hesitated, raising earnings guidance for the rest of the year.

It's not just the numbers; it's about where the growth comes from. Turkcell has seen significant growth in its postpaid base, outperforming expectations in both rate and volume. Also, the company has shown a remarkable ability to outpace inflation, with its revenue almost double the inflation rate.

But that's not all. Turkcell's balance sheet and cash flow positions have markedly improved, translating to the potential for increased shareholder returns. Even with the continued devaluation of the Turkish Lira, Turkcell has improved its foreign exchange position.

One may wonder if the recent stock price surge signals overheating. However, valuation multiples remain depressed despite the stock's recent run-up, which I feel indicates that this stock still has room to grow.

While there's some risk tied to the volatile Turkish Lira and a potential loss of momentum, the overall picture for Turkcell is overwhelmingly positive. Given the compelling evidence, I continue to believe Turkcell is a buy.

For further details see:

Turkcell Q2 Review: Exceeding Expectations On Every Front