TKC - Turkcell: Successfully Navigating Inflation

2023-05-10 13:21:15 ET

Summary

- Turkcell Iletisim Hizmetleri A.S. is a wireless communications provider from Turkey that has been impacted by runaway inflation and a weakening Turkish Lira.

- Despite inflation, Turkcell has continued to grow and outpace the competition, with revenue beating earnings estimates and outpacing inflation in Q1 2023.

- I rate this stock a buy as I believe the market has overreacted to inflation news, and the upside potential outweighs the risks of ongoing inflation.

Turkcell Iletisim Hizmetleri A.S. ( TKC ), a wireless communications provider from Turkey, has been impacted by runaway inflation and a weakening Turkish Lira. Despite this, the company has continued to grow and outpace the competition, beating earnings expectations for Q1 2023. Turkcell has also successfully navigated the impacts of inflation on its business, and the financials accelerated out of 2022 and into 2023. On the pricing side, I see depressed valuation multiples and healthy cash flow to pay a dividend.

While there is a long way to go, I am cautiously optimistic that Turkcell's management will continue to effectively offset inflation. I rate this stock a buy as I believe that the market has overreacted to inflation news, and the upside potential outweighs the risks of ongoing inflation

Q1 Earnings Beat Expectations With Strong Growth

Turkcell Iletisim Hizmetleri A.S. ("Turkcell") is a leading provider of wireless communication services in Turkey, covering 99% of the country. They also have a presence in broadband and coverage in Ukraine, Belarus, Northern Cyprus, and the Netherlands.

Since Covid and the war in Ukraine, Turkey has been experiencing runaway inflation peaking at 86% in 2022. From reading article after article, I feel the inflation situation in Turkey has caused many investors to immediately discount Turkish stocks. I agree that there is a need to be cautious, especially when evaluating revenue and expense growth. However, with inflation starting to moderate ( ranging from 51-58% in Q1 and down to 44% in April ), we need to look closer at the fundamentals and how Turkcell is setting up for the future.

First and most importantly, with revenue of $885 million, Turkcell beat consensus revenue estimates for Q1 2023 by $33 million. In addition, Turkcell is pacing well ahead of 2023 earnings guidance . Q1 revenue was up 61.5% versus the guidance's 55-57% revenue growth.

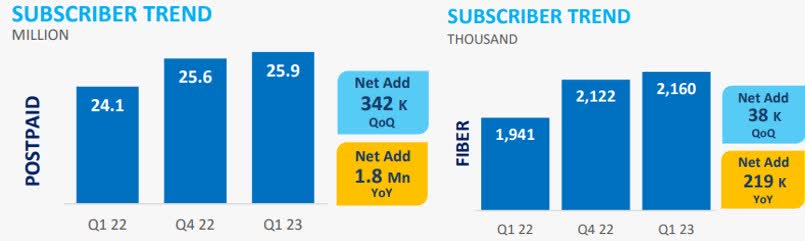

Turning to the growth drivers, in the Q1 2023 Earnings Presentation, Turkcell showed impressive growth in postpaid and fiber subscribers, the highest-margin products.

Turkcell Postpaid and Fiber Subscribers (turkcell.com.tr Investor Relations)

{kind=link}

Looking at newer businesses, Digital Business Solutions and Paycell (TechFin) outpaced inflation, growing 104% and 79%, respectively.

New business growth Q1 2023 (turkcell.com.tr Investor Relations)

{kind=link}

And what I believe to be the most important point, Turkcell significantly outpaced Vodafone's Turkey business in both Mobile Net Adds and revenue growth. To me, this demonstrates strong fundamentals and a strategy that is resonating with consumers.

Financials Accelerating As Inflation Is Addressed

In a high inflation environment, I am focused on two things: is revenue tracking with inflation, and is revenue growth outpacing expense growth?

Based on Q1 2023 results , revenue grew at 61.5% in Q1 versus 2022 from both business growth and multiple rounds of pricing hikes, outpacing average inflation for the quarter of 55%. Turkcell saw success outpacing inflation across every business (remember that Turkcell International, which grew at 31%, does not operate in Turkey and experienced lower inflation). The aggressive price hikes from 2022 have caught up to inflation and are driving momentum into 2023.

Continuing to review the Q1 2023 results , EBITDA for the full year grew 57.1%, 4.4 ppt behind revenue growth. So for the quarter, revenue growth could not keep up with expense growth driven by inflation. However, digging in further to expense growth, employee expenses drove the EBITDA miss as annual raises went into effect. The remaining operating expenses actually improved from a margin perspective.

Looking back to Q4 2022, EBITDA grew at 58.4%, outpacing revenue growth by 1.0ppt. Last year, Turkcell improved its ability to combat inflation throughout the year and set up momentum going into 2023. We see this momentum continuing in non-labor expenses. With that in mind, I believe the Q1 impact was a one-time blip that the business can grow past.

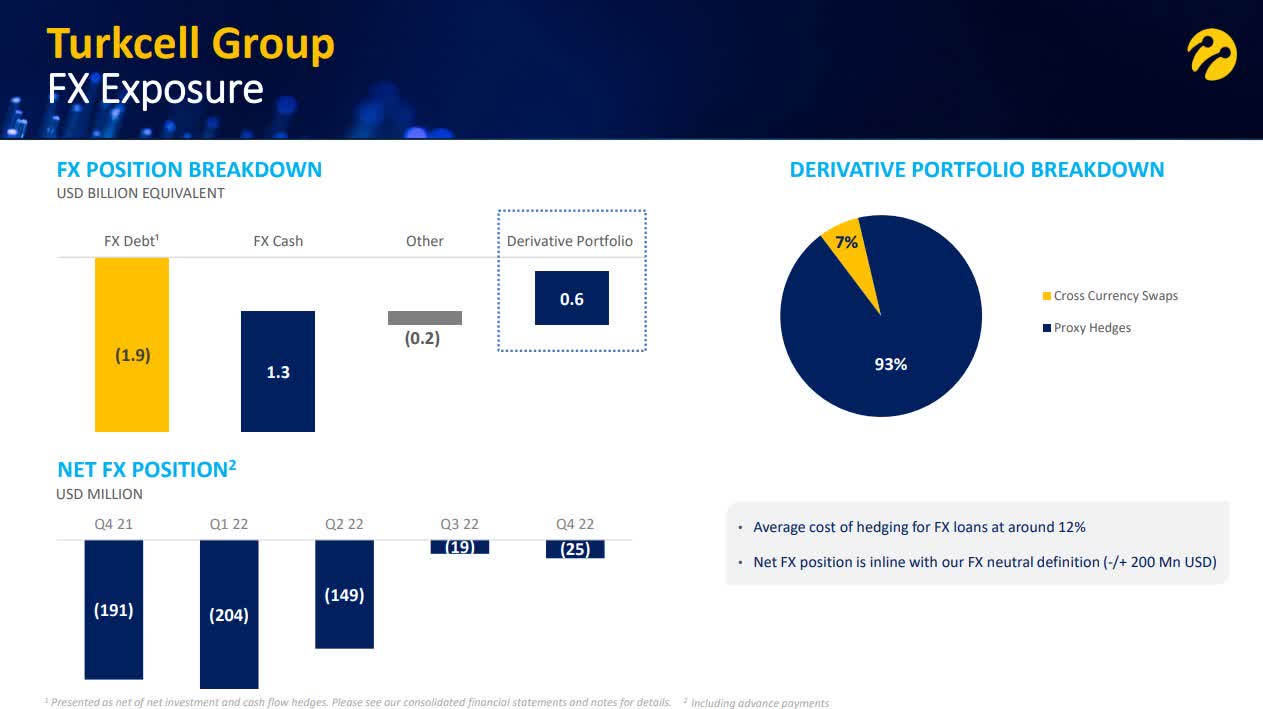

Another major impact of inflation has been the devaluation of the Turkish Lira , down to 19 Lira / Dollar as of March 2023. For Turkcell, this impacts their ability to repay debt as well as their ability to purchase capital equipment.

Looking at the April Investor Presentation , Turkcell started 2022 with a significant Fx exposure, $204 million USD, but ended the year at $25 million through cash flow hedges. They currently hold $1.9 billion of debt but have $1.3 billion of foreign currency and $0.6 billion of derivates.

Turkcell FX Position (turkcell.com.tr Investor Relations)

{kind=link}

Again, management is taking the necessary actions to protect the business from inflation and grow despite it.

Upside For Stock Price

Following Q1 2023 earnings, I believe that the stock price has bottomed out as valuation multiples are depressed relative to both competitors and the historical average. In addition, the dividend has been reduced as the company stabilizes cash, but as inflation moderates, Turkcell has the cash flow to easily return more cash to shareholders.

Non-GAAP PE is down an eye-raising 74% to competitors and 47% to the historical 5-year average. EV/Sales is down 37% to competitors and 24% to the historical average. EV/EBITDA is also down 67% to competitors and 24% to the historical average.

Turkcell's business is strong and growing based on the Q1 2023 results we reviewed above. Furthermore, their growth is accelerating, and it is accelerating into high-margin businesses like fiber and post-paid wireless. New businesses are even seeing success and outpacing inflation. In my opinion, this doesn't look like a business where ratios should be depressed. This looks like an overreaction to inflation.

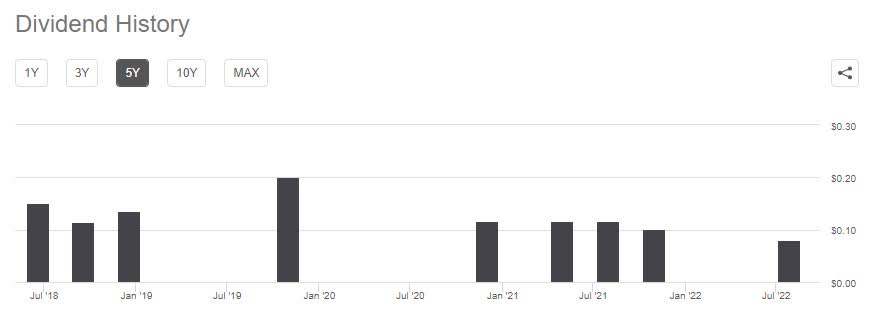

On the dividend side, Turkcell has had an erratic history with its dividend as it managed capital investment and the impacts of inflation.

Turkcell Dividend History (Seeking Alpha - TKC)

{kind=link}

That said, the business is generating almost $1 billion in cash flow after capex, only paying out $67 million in dividends across 2022. The cash balance in 2022 grew $391 million to $1.6 billion even after restructuring debt and accounting for inflation. Moving into 2023, the cash balance increased in Lira (slightly decreasing in USD) as the company grew. Today, Turkcell has plenty of headroom to maintain the dividend. As the Turkish economy stabilizes, Turkcell is well-positioned to increase dividends and return more to shareholders.

Downside Potential

The biggest risk to Turkcell is that inflation doesn't moderate. Over time, I believe Turkcell's ability to raise prices would erode as their customers tire of frequent price hikes. This would pressure their topline growth, margins, and cash flow.

In addition, the Turkish Lira could continue to weaken even as inflation moderates. The currency risk could be significant during an extended downturn if the hedging portfolio is not timed correctly with debt maturity.

Either of these risks would put pressure on both margin and cash flow, risking the dividend yield. As we move through 2023, I will keep an extremely close eye on how revenue and expense perform versus inflation. I will also be watching the company's FX position closely.

Verdict

The company is doing what it can to protect itself from inflation and drive growth. However, the risks remain, and investors should diligently monitor these potential threats. As long as Turkcell continues to execute its strategies and manage risk effectively, it could continue to be a solid investment for those seeking exposure to Turkey's market. I am cautiously optimistic as the business beat earnings in Q1 2023, outpaced earnings guidance, and continues to generate substantial (and hedged) cash flow. I rate this stock a buy, as the growth trajectory and upside potential outweigh the risks of ongoing inflation.

For further details see:

Turkcell: Successfully Navigating Inflation