TKC - Turkcell: The Stock Is A Buy

Summary

- Turkcell reported strong 3Q 2022 financial results and I expect its 4Q 2022 results to be strong too.

- The company’s liquidity and leverage ratios indicate its healthy conditions to handle potential risks in the future.

- Despite the negative effect of continuing inflationary pressures and recent earthquakes that can disrupt demand for tourism, Turkcell’s subscriber base continues to increase.

- The stock is a buy.

Inflationary pressures on Turkcell’s ( TKC ) operational expenses and capital expenditures are still continuing. Also, the recent earthquakes can disrupt tourism and hurt Turkcell’s revenues from selling its services to tourists. However, these negative effects should only limit Turkcell’s net income growth. I expect Turkcell stock’s 4Q 2022 financial results to be as strong as in 3Q 2022. Also, I expect the company to continue reporting strong financial results and huge profits in 2023. TKC’s liquidity ratios and leverage ratios improved in the first nine months of 2022 and I expect them to improve in 2023. The stock is a buy.

Quarterly results

In its 3Q 2022 financial results, TKC reported revenue of TRY14.7 billion, compared with 3Q 2021 revenue of TRY9.4 billion, up 56.7% YoY, driven by strong ARPU performance, an increased subscriber base of Turkcell Turkey, and the contribution of international operations. In the first nine months of 2022, the Turkcell Turkey subscriber base increased by 2.2 million. The company’s EBITDA increased by 48.7% YoY to 6.0 billion. Its EBITDA margin decreased by 2.2 bps and to 40.9%. Turkcell’s net income increased from TRY1.4 billion in 3Q 2021 to TRY2.4 billion in 3Q 2022, up 67.6% YoY. For the first nine months of 2022, Turkcell reported net income of TRY5.1 billion, compared with TRY3.6 billion in the first nine months of 2021.

In its 3Q 2022 financial results, Turkcell upgraded its previous guidance for 2022. The company expected its full-year 2022 revenue to be 47%-48% higher than in 2021 (compared with 40% which was previously announced). Also, Turkcell expected its full-year EBITDA to be TRY21 billion, compared with TRY20 billion which was previously estimated. Overall, Turkcell reported strong results in the third quarter of 2022.

“In this period consumer spending strengthened, demand accelerated, and recovery of the market increased. Additionally, rising mobility in the summer period, the tourism sector, which even exceeded its pre-pandemic level, and the back-to-school period accelerated our operations. In addition to an expanding subscriber base, consistent price increases and upsell efforts, we achieved an accelerated quarterly performance with the contribution of digital business services, techfin, and our international operations,” the CEO commented.

The market outlook

Turkcell has a market share of more than 40% in the Turkish mobile network industry, and is the largest operator in Turkey. Also, the company’s fiber broadband customer base is increasing which is expected to bring more revenue to the company. In 2Q 2022 and 3Q 2022, tourism played an important role in increasing Turkcell’s subscriber base. “Rising mobility in the summer period, the tourism sector, which even exceeded its pre-pandemic level, and the back-to-school period accelerated our operations,” the CEO commented. It is worth noting that the recent earthquakes can disrupt Turkey’s tourism increasing demand for a few months, and lower the pace of Turkcell’s subscriber base growth.

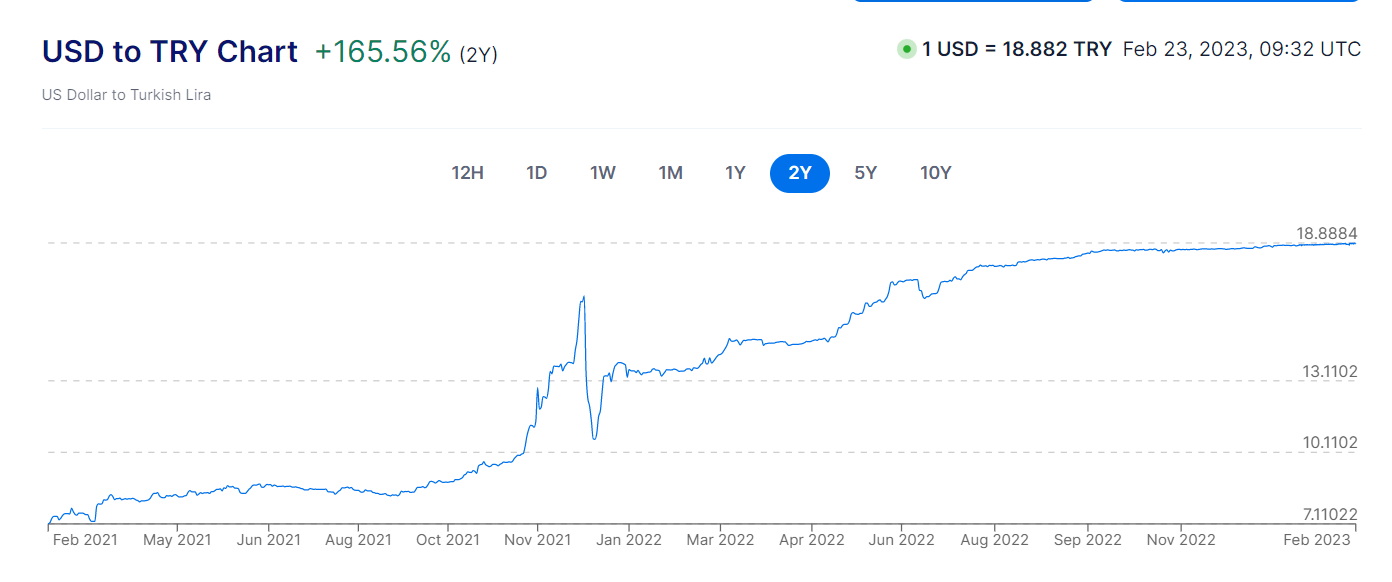

One of the challenges that Turkcell has been facing in 2022 is the inflationary pressures that caused its operating expenses and capital expenditures to grow faster than its revenues, making its EBITDA margin impaired. Inflationary pressures decreased in the past few months, however. According to Figure 1 , the Lira has depreciated significantly against USD in the first nine months of 2022. However, in the past few months, the Lira has been relatively stable and depreciated against the USD slightly.

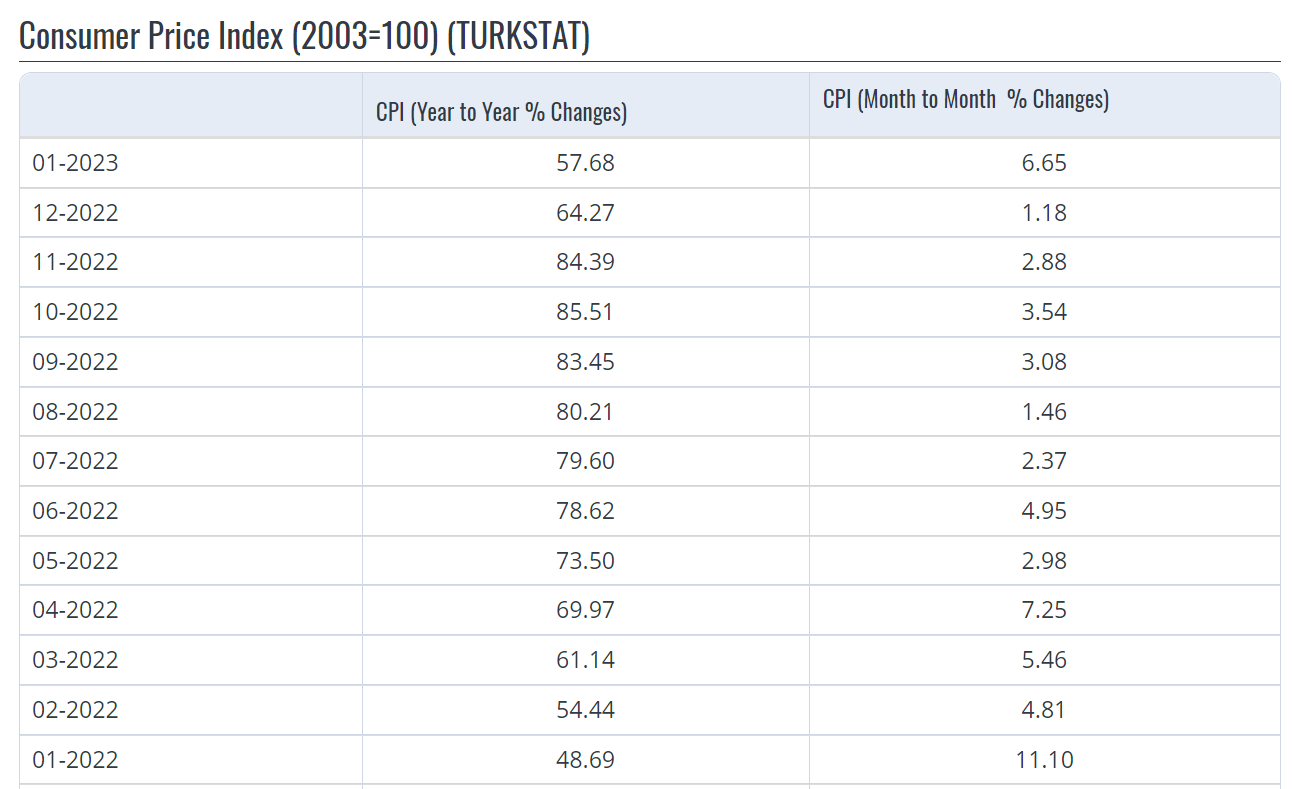

Figure 2 shows the inflation rates in Turkey in the past 13 months. We can see that from January 2022 to November 2022, the annual inflation rate in Turkey was increasing. However, in December 2022 and January 2023, as a result of lower energy prices, the annual inflation rate decreased. However, it is not safe to ignore the fact that money supply in Turkey increased considerably in January 2023 and with the country’s current monetary policy, and the cost of recovery from the recent earthquake, the country’s inflation rates probably cannot drop to low rates anytime soon.

Although, the inflation rate in 2023 is expected to be lower than in 2022. According to the median forecast of 13 economists, Turkey's inflation is expected to fall to 42.5% in 2023. Continuing inflationary pressures in Turkey may continue hurting the company’s EBITDA margin. This a risk that should be considered in your investment decision.

Figure 1 – USD to TRY chart

{kind=link}

Figure 2 – Inflation rates in Turkey

{kind=link}

Performance outlook

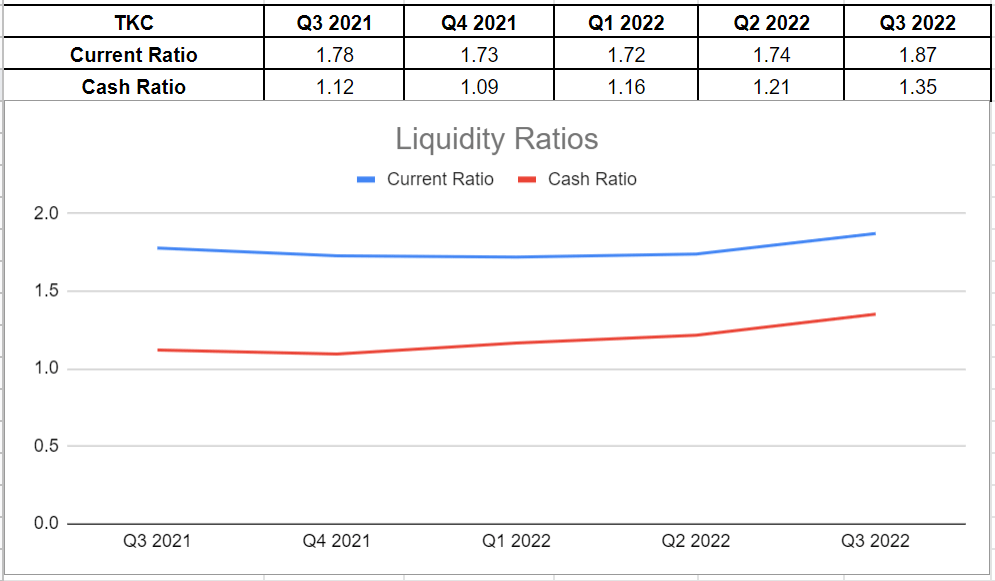

Turkcell has had solid revenue and income conditions. So, it is not unexpected to see their effects on the company’s liquidity condition. Liquidity ratios are indicating a good picture of the company’s capability to keep its balance between the ability to safely cover its obligations and manage proper capital allocations. In this regard, I investigated TKC’s liquidity structure across the board, looking at cash and current ratios.

As the liquidity ratios have assets on top and liabilities on the bottom, it is paramount to consider whether their amounts are above 1.0 to analyze if the company is able to face its obligations. According to Figure 3, it is observable that TKC showed an encouraging increase in its cash and current ratios, which indicates that the company should be able to easily face its liquidity problems. Turkcell’s current ratio has been on an increasing path during 2022 and finally increased by 7% and sat at 1.87 in 3Q 2022 versus its level of 1.74 in 2Q 2022. Also, the current level is 5% higher year over year compared with 1.78 at the same time in 2021.

Similarly, the company’s cash ratio, which is a stricter and more conservative measure, improved slightly and sat at 1.35 in 3Q 2022. Also, the cash ratio is 20% higher year over year versus its level of 1.12 in 3Q 2021. Thus, it is observable that a large amount of the company’s liabilities can be paid off directly by its cash and cash equivalents. As a result, the liquidity condition of Turkcell Company improved during recent years and depicts an encouraging picture of the upcoming 2023 conditions.

Figure 3 - TCK’s liquidity ratios

{kind=link}

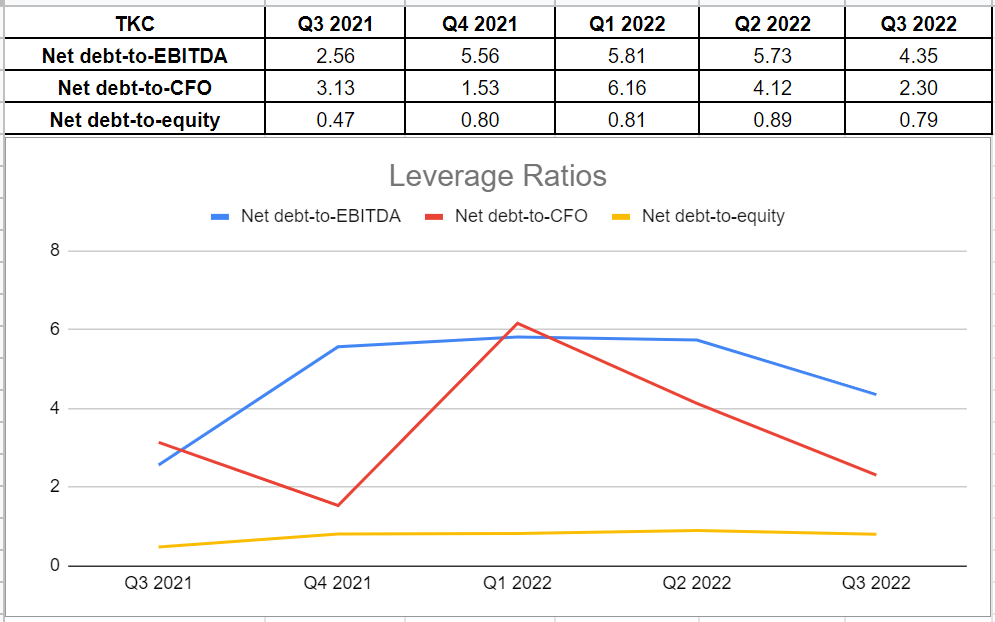

Furthermore, I analyzed how TKC’s assets and business operations are financed by investigating its leverage ratios. As Figure 4 indicates, all mentioned ratios had lower levels compared with their prior quarters. Turkcell’s net debt level decreased by about 16% from $1276 million in 2Q 2022 to $1095 million in 3Q 2022. Also, its EBITDA level, which works as a good proxy for the cash generation capacity of the company improved by 11% in the third quarter of 2022. Thus, a combination of a decline in net debt and an increase in EBITDA led to a 24% decline in net debt-to-EBITDA of 4.35 in the third quarter of 2022.

Notwithstanding a decline in the ratio, its level is still far higher year over year compared with 2.56 in 3Q 2021. On the other hand, TKC’s net debt-to-operating cash flow dropped by 44% in 3Q 2022, while it was 4.12 in its previous quarter. This ratio dropped deeply year-over-year compared with its level of 3.13 in 3Q 2021. Ultimately, the debt-to-equity ratio or risk ratio indicates how the company’s capital structure is tilted, whether toward debt or equity financing.

TKC’s risk ratio was 0.79 in 3Q 2022, meaning it was 11% lower than its level of 0.89 in 2Q 2022. It is worth mentioning that albeit the ratio declined in 2022, its total equity level was on a decreasing path as well. In other words, the company’s total equity declined by 44% to $1380.3 million in 3Q 2022 compared with the same time in 2021. When all was said and done, Turkcell’s leverage condition depicts its healthy position and capability to face upcoming risks in the future in my view.

Figure 4 - TKC’s leverage ratios

{kind=link}

Summary

Turkcell’s cash and current ratios increased by 11% and 7% in 3Q 2022, respectively. A better net debt condition aligned with higher operating cash flow caused its net debt-to-CFO to drop by 44% in 3Q 2022. I expect the company’s 4Q 2022 and 1Q 2023 financial results will be strong and its subscriber base will continue expanding. The stock is a buy.

For further details see:

Turkcell: The Stock Is A Buy