TPC - Tutor Perini Corporation: Strong Backlog Growth Reveals Sticky Demand (Rating Upgrade)

2023-10-24 14:49:49 ET

Summary

- Tutor Perini Corporation has seen a decrease in share price but strong Q2 earnings with a backlog of orders growing by 27% YoY.

- TPC operates in the construction and engineering sector, with a focus on infrastructure projects and strong connections with the government.

- Rising material costs and supply chain disruptions pose risks to TPC's profitability and project execution.

Investment Rundown

Since my last article on Tutor Perini Corporation (TPC) back in July the share price has decreased by a bit but has left me quite willing to upgrade my rating to a buy rather than a hold. The company provided strong numbers in the last quarter where the backlog of orders grew by as much as 27% YoY to $10.9 billion. Seeing as TPC had annual revenues of $3.7 billion in 2022 that is roughly another 3 years of revenues at least, a strong foundation to be on in my opinion.

TPC is involved in construction and with higher interest rates the cost of funding new projects and buildings has increased as capital becomes more expensive to get a hold of. This is likely going to be a short-term headwind for TPC but not something that is enough to dismiss the long-term outlook of the business. Investors are still getting a good deal here and with the company having been profitable in previous years it's an appealing risk/reward trade you are getting right now. In 2021 the net margins were just shy of 2% and should TPC return there I can see there is an 8x earnings multiple applicable, which leaves a price target of $14.4, a significant upside from the current price levels TPC trades at right now.

Company Segments

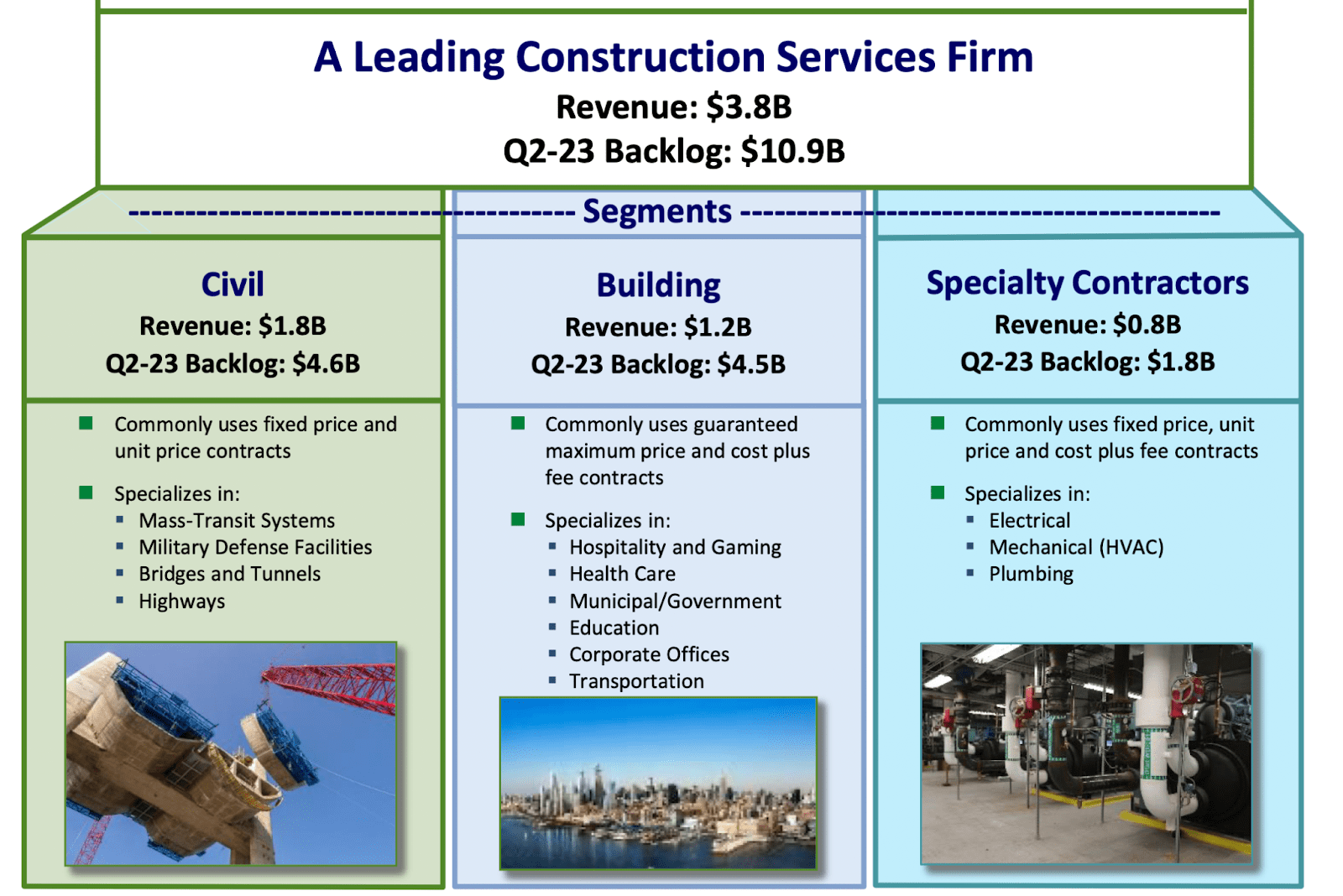

TPC is a construction company within the United States, undertaking diverse projects across the nation. Over the years, the company has cultivated its standing through a comprehensive range of services. Notable among these offerings are diversified general contracting and adept construction management.

To optimize its operational efficiency, TPC has strategically organized itself into three distinct segments: Civil, Building, and Specialty Contractors. The Civil segment is chiefly engaged in public works construction and holds the responsibility for the replacement and reconstruction of existing infrastructure and buildings. This multipronged approach empowers TPC to effectively address various construction needs, allowing for adaptability and a comprehensive service portfolio.

{kind=link}

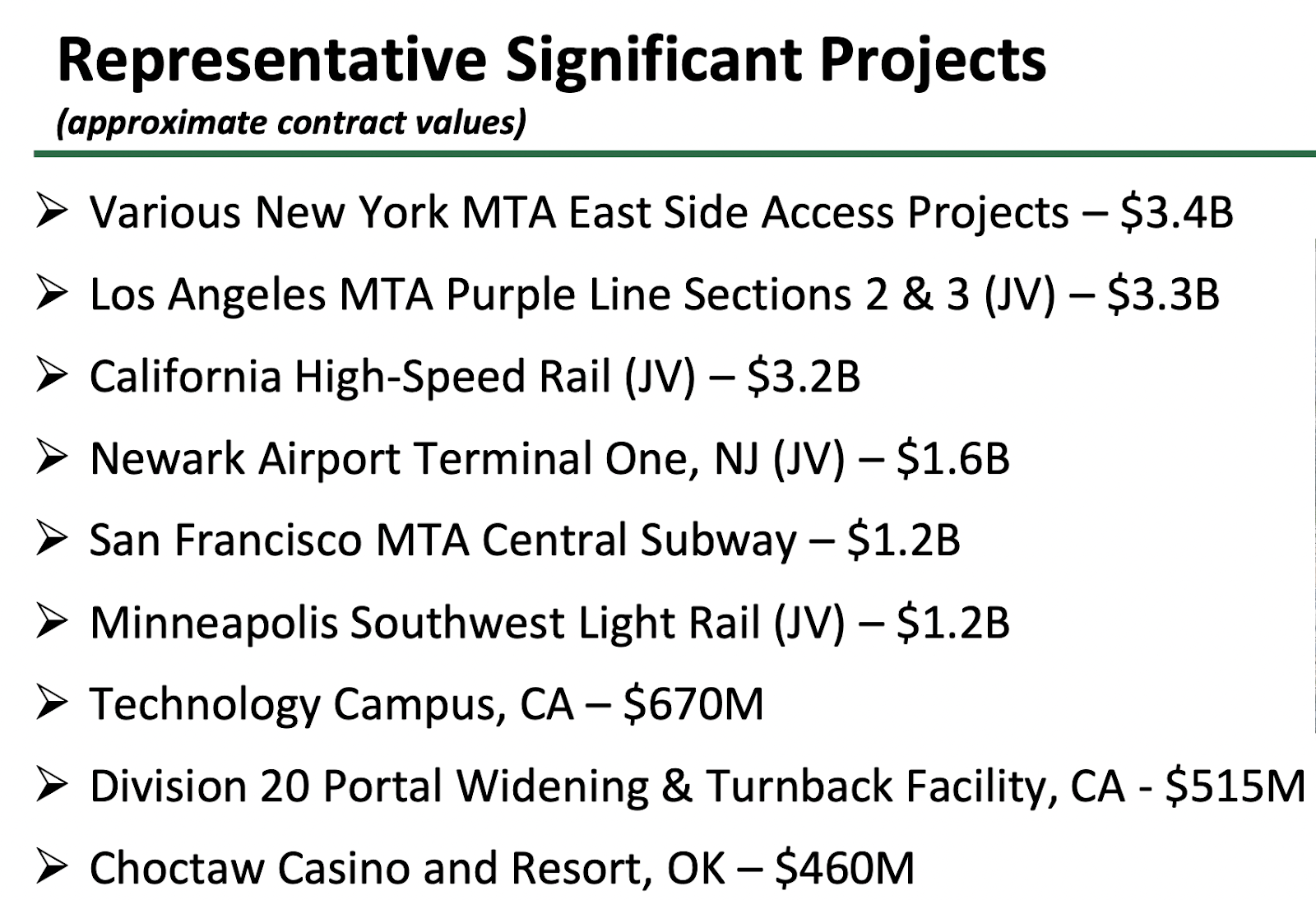

One of the key factors contributing to the company's prominent standing is its impressive track record of successfully executing large-scale projects, which has been a key reason for TPC being able to grow backlogs and be awarded new projects consistently. These endeavors have played a pivotal role in elevating the company to its current prominent position. Notable among these achievements is the Los Angeles MTA Purple Line Sectors 2 & 3 , a substantial project valued at $3.3 billion, showcasing the company's capacity to handle complex and high-value projects.

{kind=link}

Additionally, TPC's second segment specializes in delivering a diverse array of services tailored to meet the unique requirements of specialized building projects and markets. This specialized approach underscores the company's versatility and its ability to cater to a broad spectrum of construction needs, further solidifying its status as a well-rounded and highly capable construction entity.

Markets They Are In

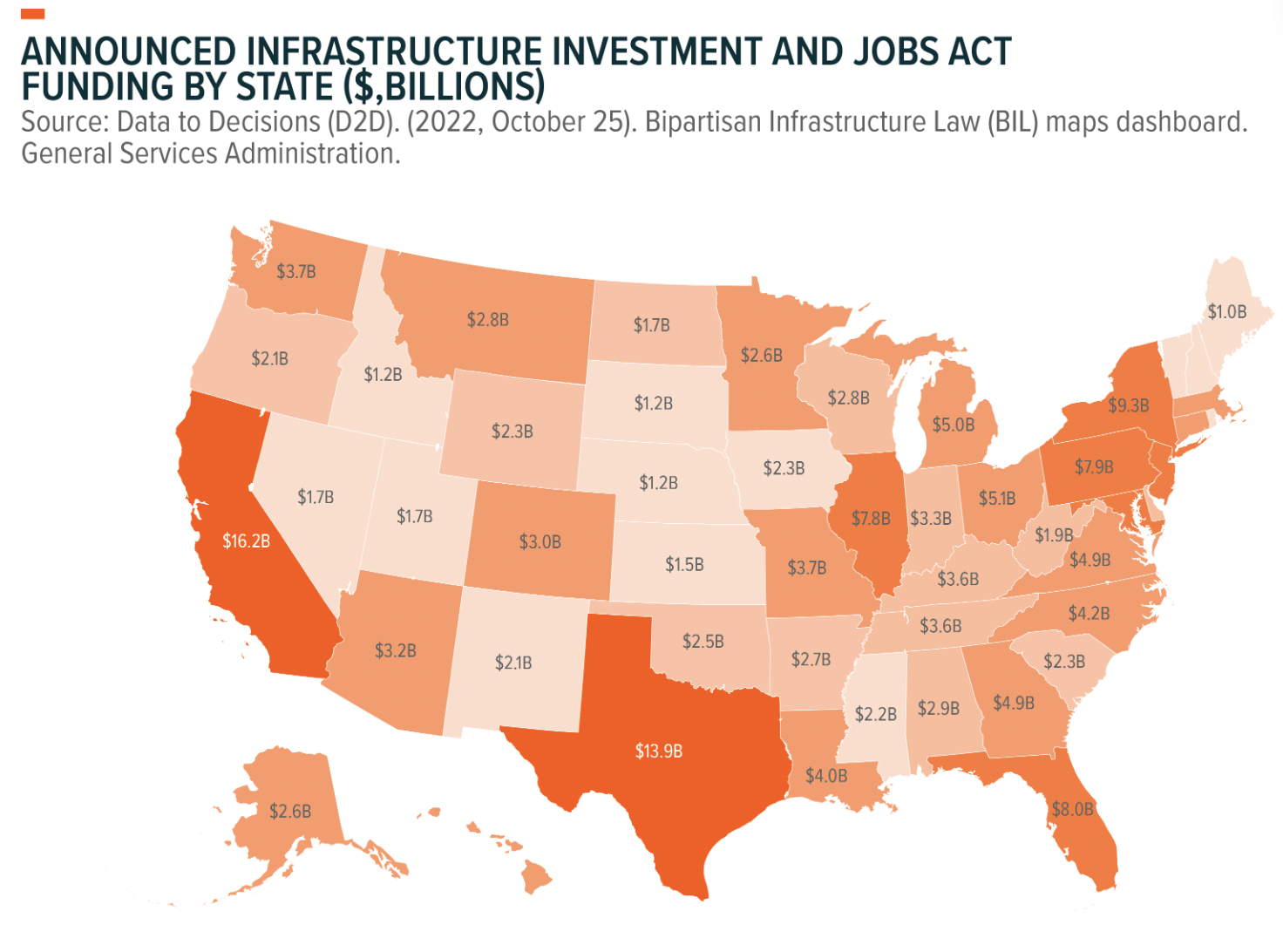

TPC operates within the construction and engineering sector, catering to a diverse clientele. Leveraging their robust market position, they are well-positioned to reap the rewards of substantial investments in infrastructure. TPC prides itself on being the go-to choice when it comes to such endeavors. Their strong connections with the government further enhance their ability to secure long-term contracts, providing a steady stream of reliable revenue.

{kind=link}

This synergy between TPC and government entities not only underscores their dependability but also serves as a testament to their ability to play a pivotal role in crucial infrastructure projects. This strategic advantage has the potential to contribute significantly to the company's sustained growth and financial stability.

Earnings Highlights

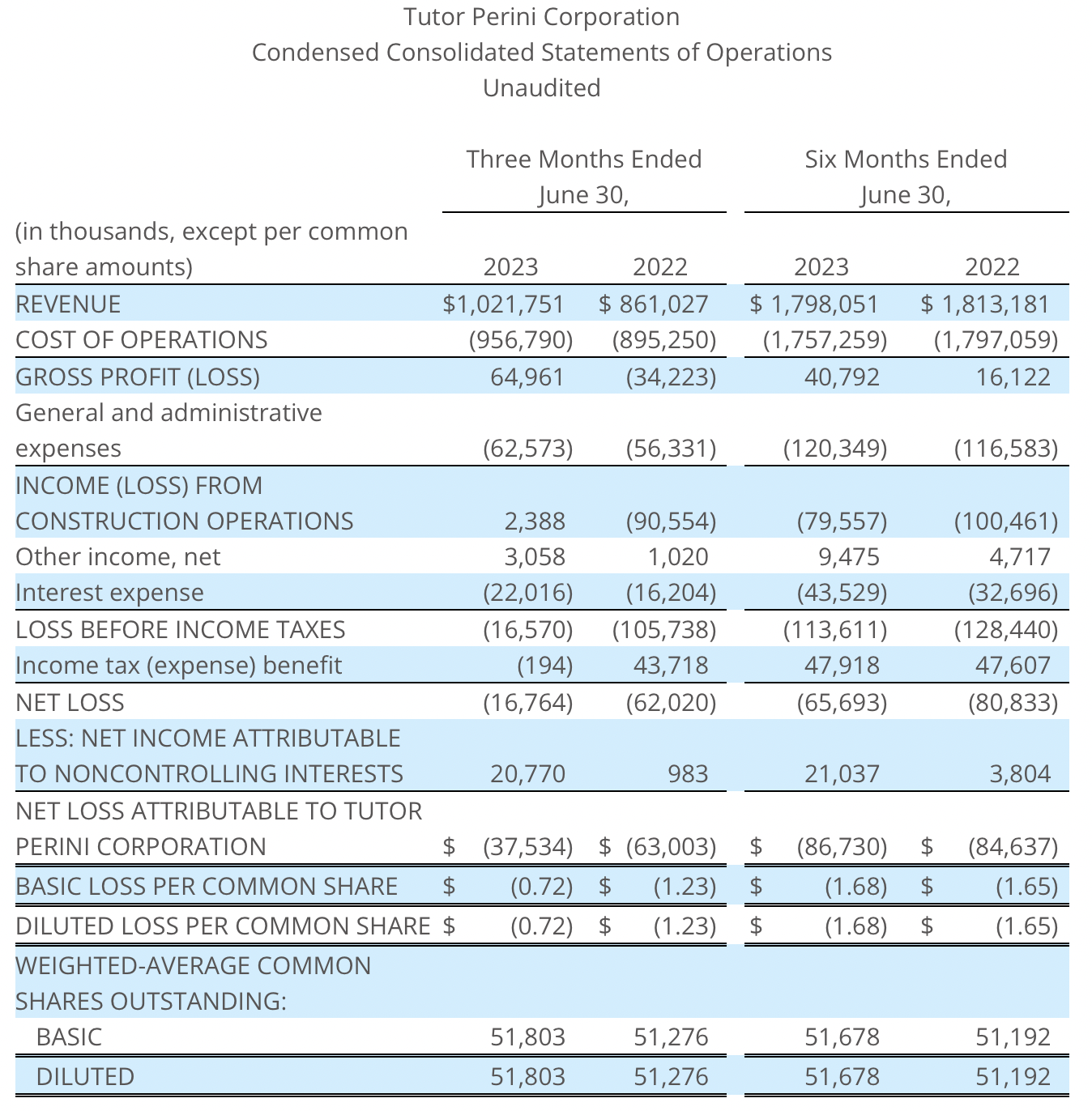

Recapping the last earnings report which was on August 3 by the company there were some very positive moves in my opinion, like the revenues growing by 19% YoY to over $1 billion, setting TPC up very well to achieve annual revenues of $4 billion, something they haven't done since 2021. Furthermore, the backlogs for the company improved very well too, reaching over $10.9 billion now, a 27% YoY growth.

The primary reason for the increase in backlogs was the positive growth in the building segment and this is praying TPC is still in high demand even as interest rates are rising and capital becomes more expensive to access. I have a lot of faith that TPC will see its top line grow strongly over the next decade as a lot of things are pointing toward there being a heavy infrastructure upgrade and investment needs in the US right now and going forward.

{kind=link}

Going into the next quarterly report on November 3rd I will be looking for continued backlog growth and double-digit YoY growth at least and perhaps even on a QoQ basis even as well. It seems like we are reaching a sort of ceiling right now for the interest rates in the US and I do think this will mean companies are more willing to start new construction projects which of course will be a tailwind for TPC. The management of the company is anticipating strong backlog growth over the next 12 - 18 months as large projects in the pipelines are presenting strong growth opportunities. Given the track record and history of projects that TPC has taken on already, I see them as a strong contender to take on a lot of this. Furthermore, operating cash flows are to set record highs at over $207 million. Should there be a large beat on that front I can see TPC being awarded a higher FCF multiple, closer to 8, which highlights the solid upside potential here as it has a TTM p/fcf of just 3.4 right now.

Furthermore, on the margin side, I will be looking for solid improvements to the bottom line in the coming report, as that will be crucial in order for TPC to maintain a sound financial position. Lacking profitability could force them to tap into cash reserves in the short term and that also limits expansion and investments in the short term, possibly resulting in a lower share price. Maintaining positive cash flows is also a key point to watch, and one where I think TPC can provide impressive results.

Risks

An escalating concern within the construction sector, particularly in recent years, revolves around the surging costs of materials. The industry has witnessed pronounced inflation in construction materials, spanning from essential resources like lumber and steel to foundational elements like concrete and copper. These mounting material expenses have the potential to exert substantial pressure on project budgets, possibly resulting in cost overruns and influencing the overall profitability of construction ventures.

White House

Furthermore, the predicament is compounded by supply chain disruptions and shortages, which can exacerbate the situation. These challenges introduce uncertainty into project timelines, leading to delays that not only hinder progress but also pose financial setbacks, amplifying the industry's concerns related to cost management and project execution.

Final Words

Construction companies have not gotten the attention they deserve I think. The share price for TPC has been in a steady decline the last couple of months and is lower than when I last wrote an article on them. Since then though we have gotten the Q2 earnings report which shows strong backlog growth and is something that is expected to continue for the last 4 - 6 quarters at least. Should TPC achieve net margins similar to that of 2021 then there is an immense upside potential here in the medium term as I set my price target at $14 - 15 with a net margin of 1.9%. I had a hold for TPC last time but I am more bullish now and will be issuing an upgrade to a buy. I think the market is too pessimistic with the sector and this has created the low valuation the company trades at and the appealing investment case that is.

For further details see:

Tutor Perini Corporation: Strong Backlog Growth Reveals Sticky Demand (Rating Upgrade)