TPC - Tutor Perini: Easy Money Has Already Been Made

2023-10-20 18:22:12 ET

Summary

- Shares of Tutor Perini Corporation have rallied close to 40% in the past six months after hitting a bottom in April.

- The company's sales and backlog growth do not guarantee significant earnings growth, with the fiscal 2023 EPS estimate having fallen significantly over the past six months.

- TPC's balance sheet trends, including falling shareholder equity and rising shares outstanding, adversely affect its valuation.

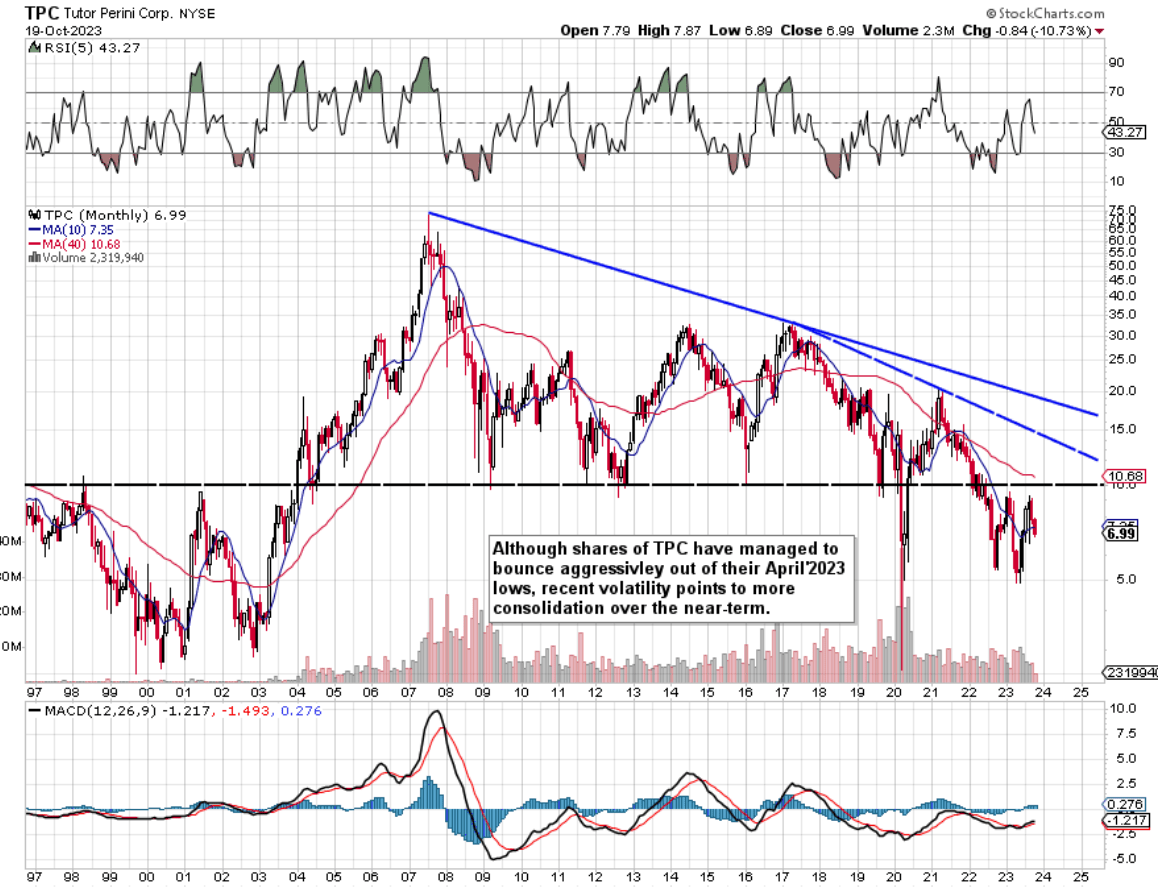

We wrote about Tutor Perini Corporation ( TPC ) back in April 2023 of this year when we were sizing up when shares of the engineering & construction company could finally rally. We gave the stock a 'Hold' rating at the time of writing due to having no clear buying signal on the technical chart. In fact, given that shares of TPC were trading at roughly $5 a share at the time, we didn't discount the fact that shares (due to their bearish trend and testing of underside support) could indeed have traded lower (back down to the stock's 2000 or 2002 lows). This though did not take place as support actually held firm as we see on TPC's long-term chart below.

Suffice it to say, once we got the bottom we were looking for, shares rallied hard and have now tacked on close to 40% which is an excellent return over the past six months all things remaining equal. Fundamentally, one could see where investors were coming from considering TPC's oversold valuation at the time. We state this because the reported net loss number of -$4.09 per share in fiscal 2022 was predominantly down to settlements, charges, and multiple judgments which all adversely affected TPC's income statement meaningfully. The performance of the Civil segment (which is where the lion's share of TPC's potential lies) also underperformed significantly in fiscal 2022 and did not give a true reflection of TPC's fundamental strength in this area.

However, when we revert to the long-term technical chart, we see that the stock's August highs ($9.30) of this year failed to take out the stock's 2023' February highs of approximately $9.55 a share. This leads us to believe (given TPC's long-term bearish trends lending itself to significant overhead resistance) that shares will trade in a range for the foreseeable future (between $5 & $9). Therefore, we are going to remain with a 'Hold' rating in TPC for reasons which we discuss below.

{kind=link}

Backlog & Sales Growth Do Not Tell The Whole Story

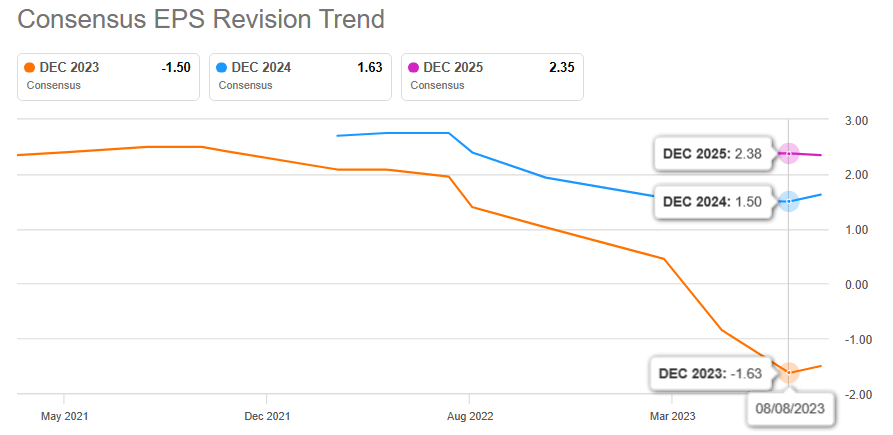

Although management believes that the company's top-line trend will keep improving (post the almost 20% increase in TPC's most recent second quarter), growth in both the company's sales & backlog does not guarantee that significant margin & earnings growth will follow suit. We acknowledge that the present bottom-line estimates for fiscal 2023 & fiscal 2024 ($1.63 & $2.35 per share) demonstrate strong year-over-year growth, but there is no guarantee that this trend will indeed continue. In fact, (given that we always look more closely at how near-term projections get impacted), observe below how the fiscal 2023 EPS estimate has literally fallen off a cliff over the past six months. Therefore, can we say with certainty that this pattern (where litigation woes have remained at the forefront) will not repeat going forward even in a rising sales environment? Time will tell.

{kind=link}

Suffice it to say, it is all about sustained bottom-line growth on Wall Street which is why cash-collection initiatives remain crucial going forward. The reason is that interest expense ($22 million in Q2 ) continues to rise on the income statement which means the company needs to collect as much of its receivables as possible in order to position itself for a refinancing of its debt next year.

Therefore, with debt ($905 million at the end of Q2) continuing to overpower projected operating profit by some distance, the real question here is how much is management willing to give up in order to bring cash back into the company. Therefore, one has to take that $3+ billion receivables number with a pinch of salt in that most likely multiple low-ball offers from debtors will be accepted by Tutor Perini to make its balance sheet as attractive as possible to creditors next year for refinancing.

Balance Sheet Trends Adversely Affect The Valuation

Given the expected consolidation in the share price in upcoming weeks as well as the lack of paying dividends, investors need to look at the financials (and specifically the balance sheet ) to ensure the company is on a path to getting much stronger. However, shareholder equity ($1.367 billion) continues to fall sequentially every quarter and the number of shares outstanding (52 million approx.) continues to rise. These are not shareholder-friendly trends and especially so when one understands that $3+ billion of receivables help to make up that positive book-value number on the balance sheet.

Suffice it to say, that TPC's ultra-low stated forward-book multiple of 0.25 is not an accurate picture of how cheap the company's assets are at this point in time in our view. Remember, the company remains unprofitable where the lion's share of present cash-flow generation has not been directed to capex spending but rather debt reduction.

Conclusion

Therefore, to sum up, given the growth of TPC's backlog with particular strength in its civil segment, we believe shares will remain above their April lows printed earlier this year. However, given the weakness of the balance sheet, ongoing litigation woes, and significant overhead technical resistance, we do not believe the company has sufficient fundamental strength to outperform over the next 12 months for example. TPC remains a 'Hold'. We look forward to continued coverage.

For further details see:

Tutor Perini: Easy Money Has Already Been Made