GFF - Tweaking Its Strategy Will Keep Griffon Corporation On The Hunt

2023-12-11 17:55:55 ET

Summary

- Griffon Corporation faces short-term headwinds due to economic uncertainty, low industrial growth, and low consumer demand.

- The company is implementing a global sourcing strategy to counter challenges and strengthen its competitive positioning.

- GFF expects to gain market share in the residential and commercial markets in 2024, but the stock appears relatively overvalued.

GFF Will Emerge Through The Obstacles

I have covered Griffon Corporation ( GFF ) in the past, and you can read the latest article here . Griffon's outlook has diverged between the short- and medium-term horizons. In the short term, I see headwinds in economic uncertainty, low industrial growth, and low consumer demand. The company adopted a global sourcing strategy to counter the challenges while strengthening its competitive positioning with customers and distributors. However, the strategy will incur additional costs in the coming quarter. It invests in productivity improvement, including expanding its door manufacturing capacity.

So, GFF expects to gain market share in the residential and commercial markets in 2024. The company's cash flows improved impressively in 2023. Despite high leverage (debt-to-equity), the company has returned substantially to its shareholders through buybacks. The stock appears relatively overvalued. So, investors should continue to "hold" the stock.

Strategy Fine-tuning

Recently, GFF expanded its global sourcing strategy in the Consumer and Professional Products segment. In many operations, consumer demand fell, and customer inventory levels increased. It plans to utilize an asset-light structure in response to the challenging market conditions.

So, its US operations with a more flexible and cost-effective global sourcing model can lower its costs and improve margin. It continues to leverage its brands while strengthening its competitive positioning with customers and distributors.

{kind=link}

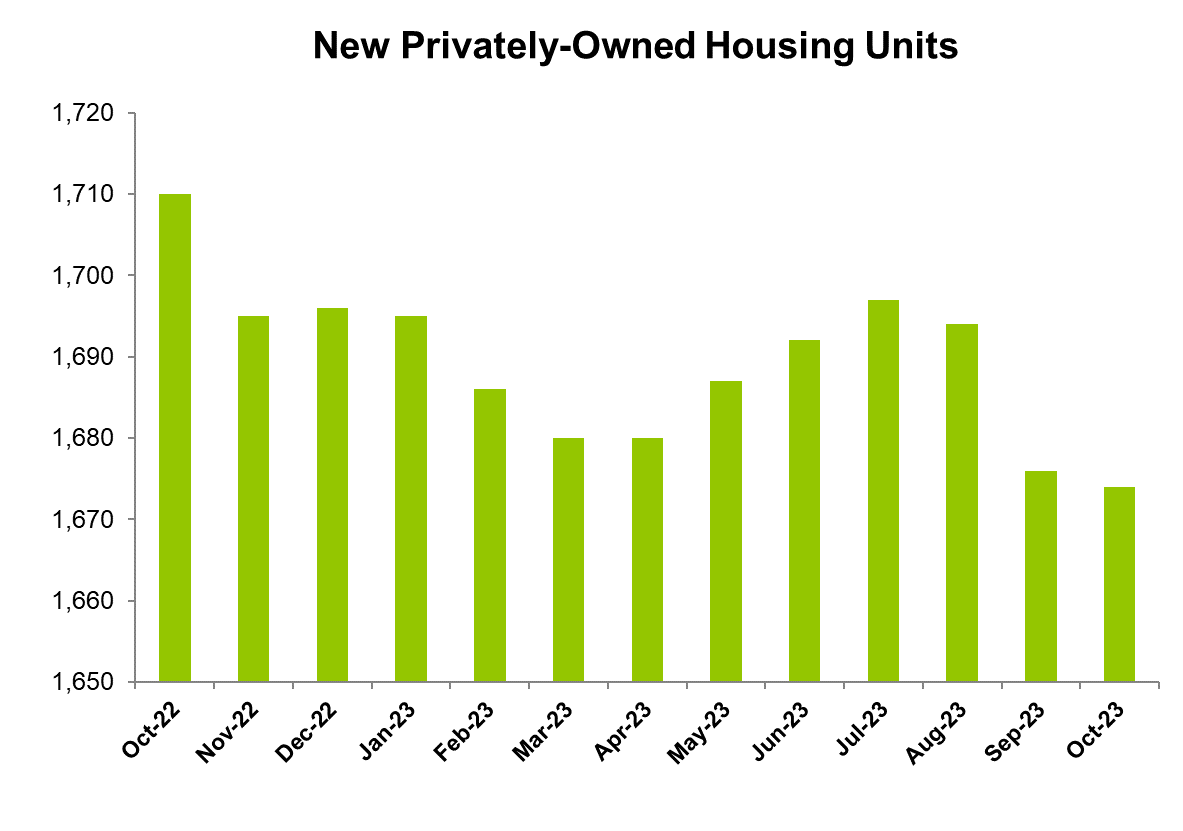

In the Home and Building Products segment, residential volume continues to face challenges but saw signs of improvement. The backlog level normalized. The new privately owned housing units in the US have remained steady. Year-to-date until October 2023, it fell by 1%. Its pricing stabilized while the sales mix across all products and channels improved. It will continue to invest in productivity and innovation.

Recently, it has invested in expanding Clopay's sectional door manufacturing capacity in Ohio. For the premium products, it invests in adding advanced manufacturing equipment facilities. It disclosed plans to close four manufacturing and four wood mills earlier. The entire restructuring project is to be completed by the end of 2024.

Market Trends

{kind=link}

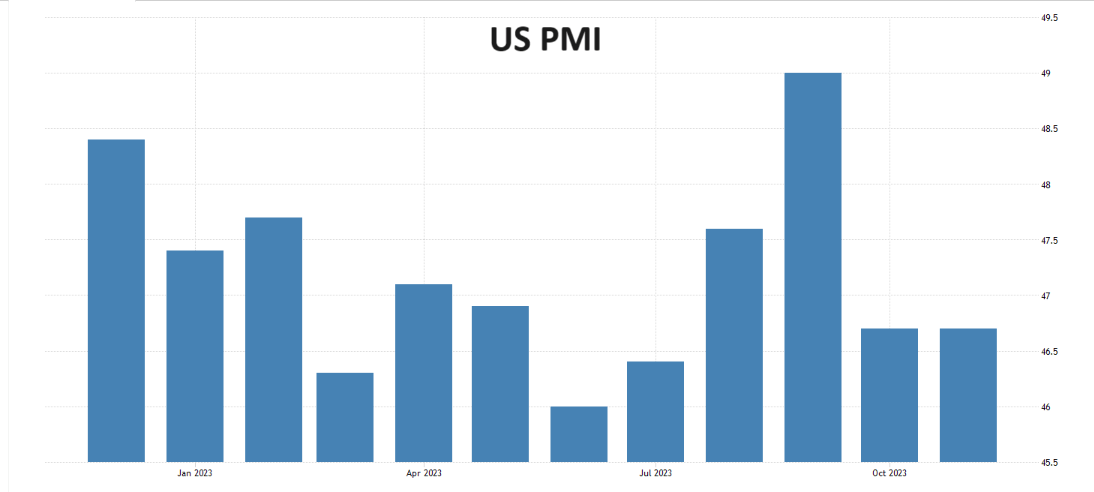

The US unemployment rate of 3.9% was one of the highest in October in the past several years. This was a sharp reversal from the multi-year low rate at the middle of the year. Month-over-month, the ISM Manufacturing PMI remained at 46.7 in November. Order softness in the manufacturing sector continued during the month. So, the PMI's remaining below 50 and a relatively high unemployment rate point to uncertainty in the economic and industrial environment.

FY2024 Guidance

{kind=link}

Based on the global sourcing strategy in 2023 and the continued challenges in the CPP segment, the company's management expects its FY2024 revenue to decrease by 3% to $2.6 billion. It also expects an adjusted EBITDA of $525 million in FY2024, or 6% lower than FY2023. Also, in 2024, it can incur additional expenses related to the AMES (a leading brand in the CPP segment) global sourcing expansion and strategic review retention.

In the Home and Building Products (or HBP) segment, GFF expects revenues to decrease by 3%-5% due to still-elevated residential door backlog volume and seasonality. In 1H 2024, demand typically falls as normal seasonal demand patterns return. In the second half of the year, demand typically rises. However, partially offsetting the headwinds will be the company's market share gains in the residential and commercial markets. The company expects the EBITDA margin for 2024 in this segment to exceed 30%, which means it will remain stable compared to Q4 2023.

In the Consumer and Professional Products (or CPP) segment, the company's revenues can decrease by 3%-5% year-over-year in FY2024. As in the other segment, 1H 2024 is expected to underperform compared to the second half due to seasonality and customer destocking. During 2H, I expect the inventory levels to return to normal. The segment EBITDA margin, however, can improve modestly as the AMES US operations transition to an asset-light operating model.

Segment Performance And Drivers

{kind=link}

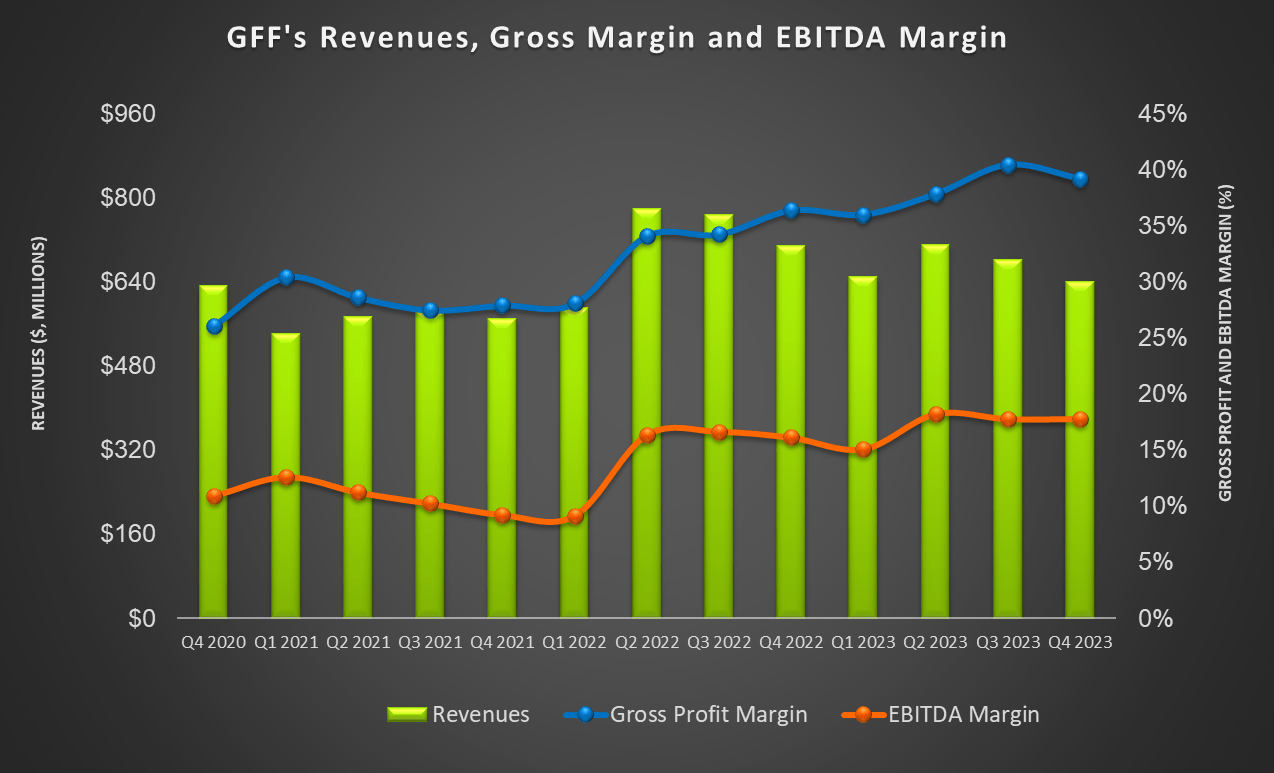

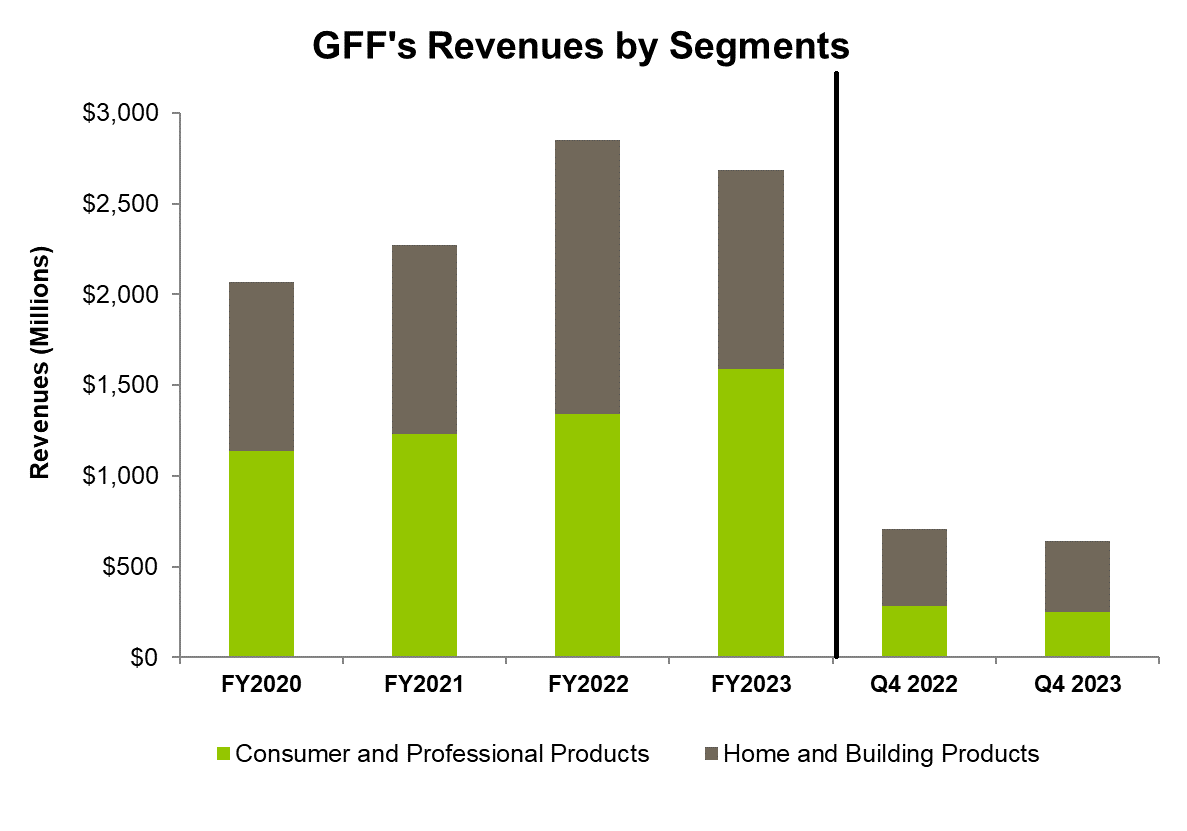

From Q4 2022 to Q4 2023, GFF's CPP segment revenues decreased by 13% because volumes were reduced in all channels and geographies. Higher customer inventory, more competition in the market, and lower demand led to the topline drop. Despite volume dropping, the segment adjusted EBITDA more than doubled due to lower material costs.

The company's HBP segment saw year-over-year revenues decrease by 7% in Q4 2023. The adjusted EBITDA margin in this segment contracted by 60 basis points. Increased labor, marketing, and advertising costs adversely affected the margin growth during the quarter.

Cash Flows And Shareholders' Returns

In FY2023, GFF's cash flow from operations (or CFO) increased remarkably compared to a year ago. Although revenues declined over the past year, improving working capital led to an improvement in CFO. Free cash flow (or FCF) (excluding acquisition) increased by ~20x in the past year. In FY2024, the company expects capex to be $70 million, which would be used for upgrading the Clopay sectional door manufacturing facility.

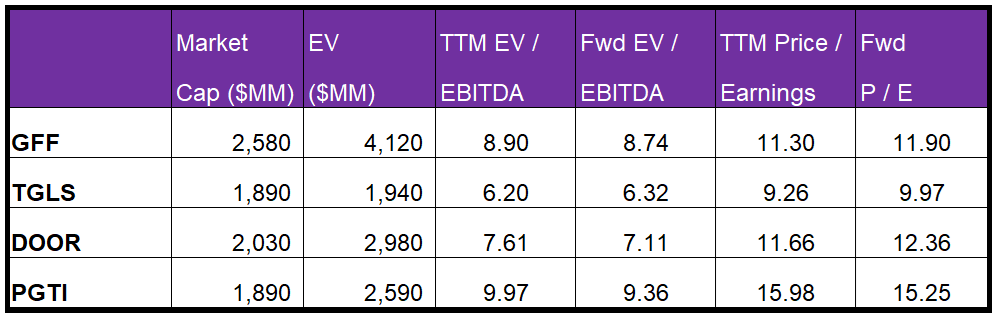

The company's debt-to-equity ratio (4.7x) is much higher than that of its competitors (TGLS, DOOR, and PGTI). It also has $539 million in liquidity as of September 30. In FY2023, it returned $285 million through dividend payments and share repurchases. In November, it increased its share repurchase program by $200 million to $262 million. Since April, it has repurchased 9.2% of its outstanding shares at an average price of $37.15 per share, significantly lower than its current share price ($49.36).

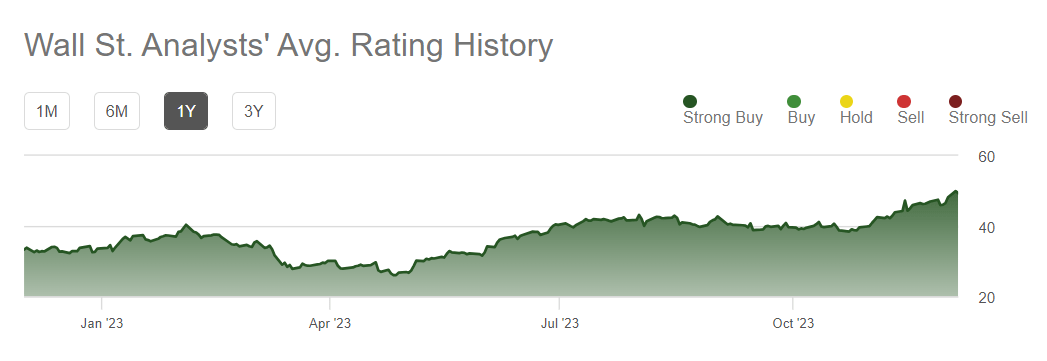

Analyst Rating

{kind=link}

According to Seeking Alpha , six sell-side analysts rated GFF a "buy" in the past 90 days (including "Strong Buy"), while none rated it a "hold" or "sell." The consensus target price is $67, suggesting a 36% upside at the current price.

Relative Valuation

Author Created and Seeking Alpha

{kind=link}

GFF's forward EV/EBITDA multiple versus its current EV/EBITDA is expected to contract less steeply than its peers. This typically results in a lower EV/EBITDA versus its peers' multiple because its EBITDA is expected to increase less sharply than its peers. The company's EV/EBITDA multiple (8.9x) is higher than its peers' (TGLS, DOOR, and PGTI) average (7.9x). So, the stock appears to be overvalued compared to its peers.

Given the recessionary fear in the US, I do not see the stock improving sharply in the short term. However, if it trades at the past average in the medium term, it can increase by 6% from the current level.

Why Do I Keep My Call Unchanged?

In my previous iteration, I discussed that while its sales in the repair and remodeling market improved, it faced challenges due to low demand in lawn & garden, storage, and organizational markets. Its balance sheet was also debt-ridden. I wrote:

Its current strategy involves leveraging its brands while strengthening its competitive positioning with distributors and customers. In 2022, Griffon acquired Hunter - one of its large competitors that complemented and diversified its global reach.

After Q4 2023, it emphasized the effectiveness of the global sourcing strategy, which essentially entails retaining an asset-light structure. Residential volume loss continues to pose a challenge as the economy and industrial growth decelerated. Still, it invests in advanced manufacturing equipment facilities for premium products. The balance sheet remained relatively weak. Given various opposing forces, I retain my "Hold" call on the stock.

What's The Take on GFF?

{kind=link}

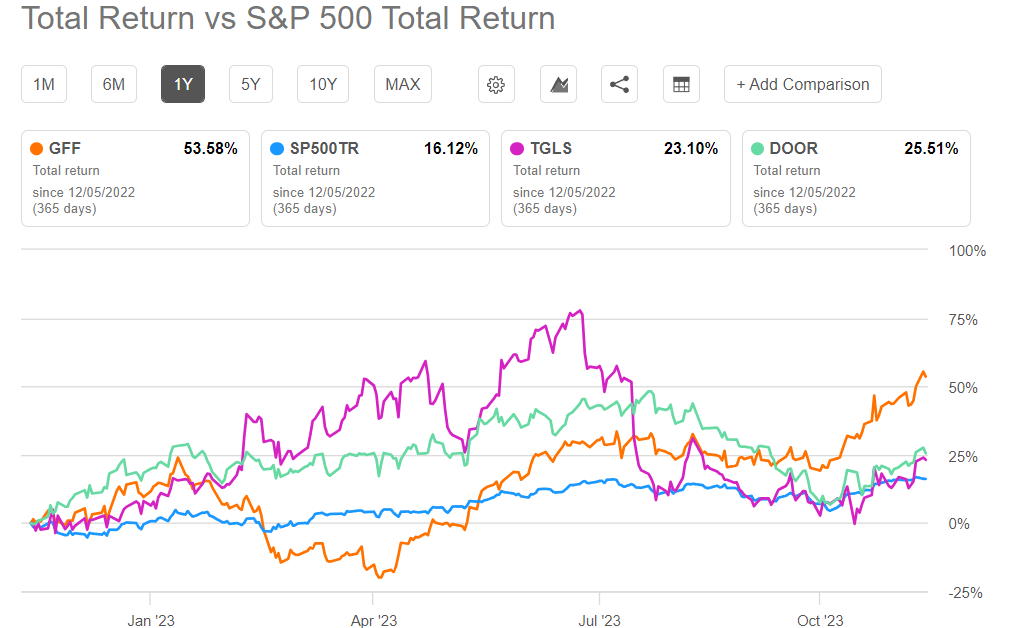

The US housing market remained stable in 2023, allowing GFF to improve its sales mix and invest in advanced manufacturing equipment facilities. Over the past few quarters, it has established a global sourcing strategy to counter the challenging market conditions in the CPP segment. With the implementation of a cost-effective policy, it has improved margin. It also appears to have gained market share in the residential and commercial markets. So, the stock outperformed the SPDR S&P 500 ETF ( SPY ) in the past year.

However, seasonal demand patterns can lower sales in the short term. The economic and industrial production indices have been below par in recent months, indicating uncertainty and volatility. Its leverage (debt-to-equity) is alarmingly high. But it has robust liquidity. Also, it increased its share repurchase program by $200 million in November. Given the stock's relative overvaluation, investors might want to "hold" the stock at this level.

For further details see:

Tweaking Its Strategy Will Keep Griffon Corporation On The Hunt