TWIN - Twin Disc: Margin Woes Continue But Growing Backlog Continues To Power Sales Forward

2023-05-26 04:13:09 ET

Summary

- Gross margin dips to 26.1% in Q3 but sales spike by 24%.

- Net income increased by 22% and operating cash flow almost surpass $7 million for the quarter.

- We expect gross margin to improve towards the 30% level over time from sustained organic and inorganic investments.

Intro

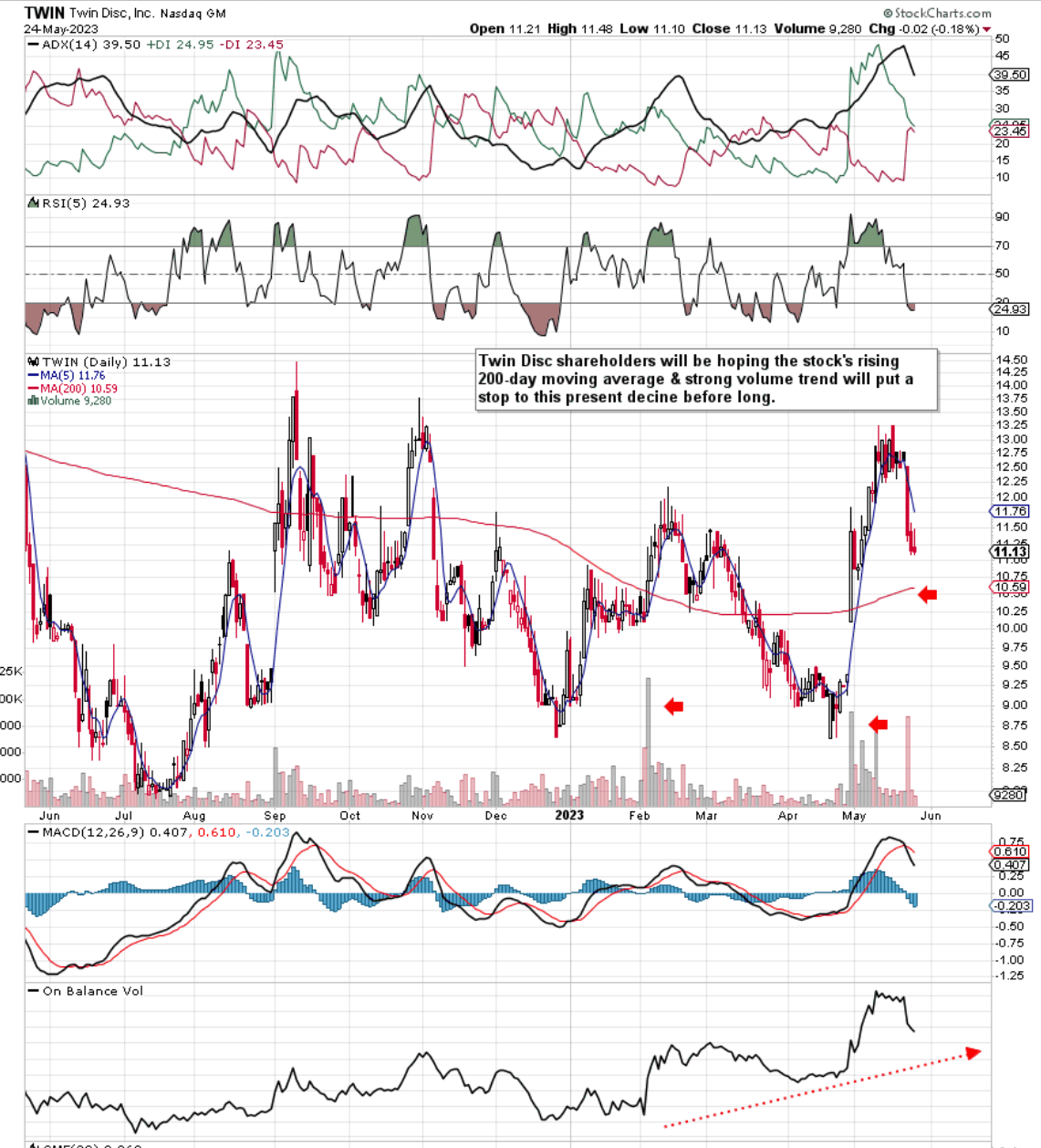

We wrote about Twin Disc , Incorporated ( TWIN ) about a month after the company's second-quarter earnings numbers (February 8th), in early March, where a pickup in demand was witnessed in the quarter. We believed momentum in the share price would continue, although we had to wait for the announcement of Twin Disc's third-quarter earnings numbers (April 28th) before shares really began to rally in earnest. As we see from TWIN stock's technical chart below, shares successfully tested support (December-2022) before gapping to the upside on those impressive Q3 numbers. Shares did top out last week (May 16th) but investors will be hoping that Twin Disc's rising 200-day moving average & bullish volume trends will be able to stop the present decline in its tracks if indeed shares continue to fall to the downside.

{kind=link}

Q3 Earnings

'Marine & Propulsion Systems' as well as 'Land-Based Transmissions' drove sales growth of 24%+ in the third quarter as demand from customers remained elevated and supply-chain headwinds eased somewhat once more. Due to continued pressure on the company's margins, favorable market conditions are vital to ensure margins do not erode over time . In fact, in Q3, we witnessed Twin Disc's gross margins drop to 26.1% from a healthier 29.8% in the same period of 12 months prior. However, the strong top-line growth rate and lower reported income tax in Q3 this year meant that net profit actually rose by roughly $500k to $2.7 million.

Obviously, this begs the question: Would earnings begin to suffer significantly if sales growth for example were to come to a grinding halt? Probably in the near term, the answer is Yes although operational efficiencies continue to improve which is enabling the company to ship more orders at a faster clip this year.

Nevertheless, if component sourcing and inflation remain significant headwinds beyond fiscal 2023 for Twin Disc, it is imperative that Twin Disc has the financial resources to be able to continue to improve its internal operations and consequently its margins. To this end, there were definitely trends in the company's most recent Q3 earnings report which make me believe that sustained investment (in a volatile environment) will be possible going forward.

Favorable Trends In the Financials

Cash flow is the lifeblood of every business (especially in volatile times) in that as long as there are sufficient sales and earnings to generate this very same cash flow, then the company in question will have the resources to keep investing in itself without turning external aid.

To this end, in Q3, Twin Disc

- Decreased its inventory position as a percentage of the company backlog (Improving working capital trend)

- Long-term debt fell to $29.3 million (a $7 million drop over the past three quarters) which means interest expense continues to improve. (Improving Leverage Trend)

- Cash balance ($14.3 million) is rising once more. (Improving Cash Trend)

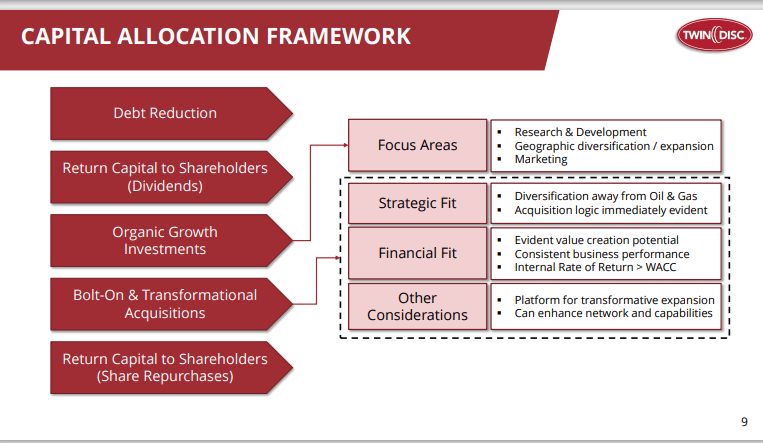

Suffice it to say, these trends led to the generation of $6.8 million of operating cash flow in Q3 which was the highest number we have seen in many quarters. With the backlog at its highest level in 5 years (Where Veth orders have remained to the fore), management believes momentum will continue in Q4 and beyond. Below, we see where management intends to invest the cash flow which is expected to come off this renewed customer demand.

Capital Allocation Objectives

{kind=link}

Now if we isolate the projected shareholder compensation initiatives (Buybacks and the introduction of a dividend fueled by free-cash-flow) out of the above scenario, it is clearly evident that Twin Disc's near-term 'spending' objectives are to continue to bring down leverage and then invest in its business both organically as well as inorganically. This means forward-looking investment dollars have already been earmarked for the following.

- 'Hybrid & Electric' initiatives to ensure Twin Disc remains at the forefront.

- Expansion of the ' Veth ' business' in particular to more jurisdictions

- Suitable acquisitions in the industrial & marine space which can add value quickly & generate strong rate of returns.

- Continue to improve operating efficiencies through the improvement of the company's legacy facilities.

Conclusion

Therefore given Twin Disc's financial trends (which have been benefitting cash-flow generation) and the company's capital allocation priorities, we believe the company will have the resources to keep on adding value even if product sourcing issues and high inflation is with us for some time to come. We still need to see a convincing 'higher-high' in the stock's financials though to designate this company a 'buy'. Let's see if the fourth quarter can live up to its billing. We look forward to continued coverage.

For further details see:

Twin Disc: Margin Woes Continue But Growing Backlog Continues To Power Sales Forward