ALPMF - Twist Bioscience: DNA Synthesis Leader Appealing 'Picks And Shovels' Play

Summary

- Twist Bioscience share price has fallen by 50% since the beginning of 2022.

- Management thinks DNA data storage could be $2 billion market for the company, aided by early mover advantage and investment in IP.

- Twist Bioscience recently raised full-year revenue guidance, which is a testament to Twist Bioscience leadership's ability to execute in a difficult market.

- Headwinds to biotech sector could lead to more customer cancellations in the near term for this business segment.

- Twist Bioscience is a Buy, appropriate only for long-term investors. Key risks include fierce competition in DNA synthesis and SynBio as well as commoditization of services offered.

Shares of synthetic DNA leader Twist Bioscience Corporation ( TWST ) have increased by nearly 300% since IPO was priced at $14 in 2018. On the other hand, valuation has been cut in half since the start of 2022.

I've run into a number of these "picks and shovels"-type ideas that generally are highly appealing to me, as they allow us to escape or at least lessen the degree of binary risk typically inherent in biotech or life science companies.

The fiscal Q3 report (period ending June 30) caught my attention here, as the company was able to top estimates and also provided guidance for full year revenues ahead of the prior outlook. Couple that with a close relationship to an emerging theme I'm a fan of (synthetic biology) and other bullish remarks from management on the recent call (antibody platform now up to 53 partners with 67 programs completed), and there's sufficient optimism here meriting a deep dive on my part.

Chart

{kind=link}

Figure 1: TWST weekly chart (Source: Finviz)

When looking at charts, clarity often comes from taking a look at distinct time frames in order to determine important technical levels and get a feel for what's going on. In the weekly chart above, it's hard to believe that shares hit a high of $200 at the peak of the bubble in biotech (likely driven in part by the link to shareholder ARK Innovation ETF (ARKK) - Cathie Wood). From there, share price bounced around in the $100 to $140 range for much of 2021 until it took the next leg lower to present levels. Presently, a bottom appears to have been established at $30 and my initial take is that long term investors looking to gain exposure would be well-served to do so here.

Overview

Founded in 2013 with headquarters in California, Twist currently sports enterprise value of ~$1.8 billion and Q2 cash position of $527M, providing them operational runway for about two years.

Management's presentation at UBS Genomics and MedTech Innovations Summit was a great help for helping me understand an industry I was quite unfamiliar with:

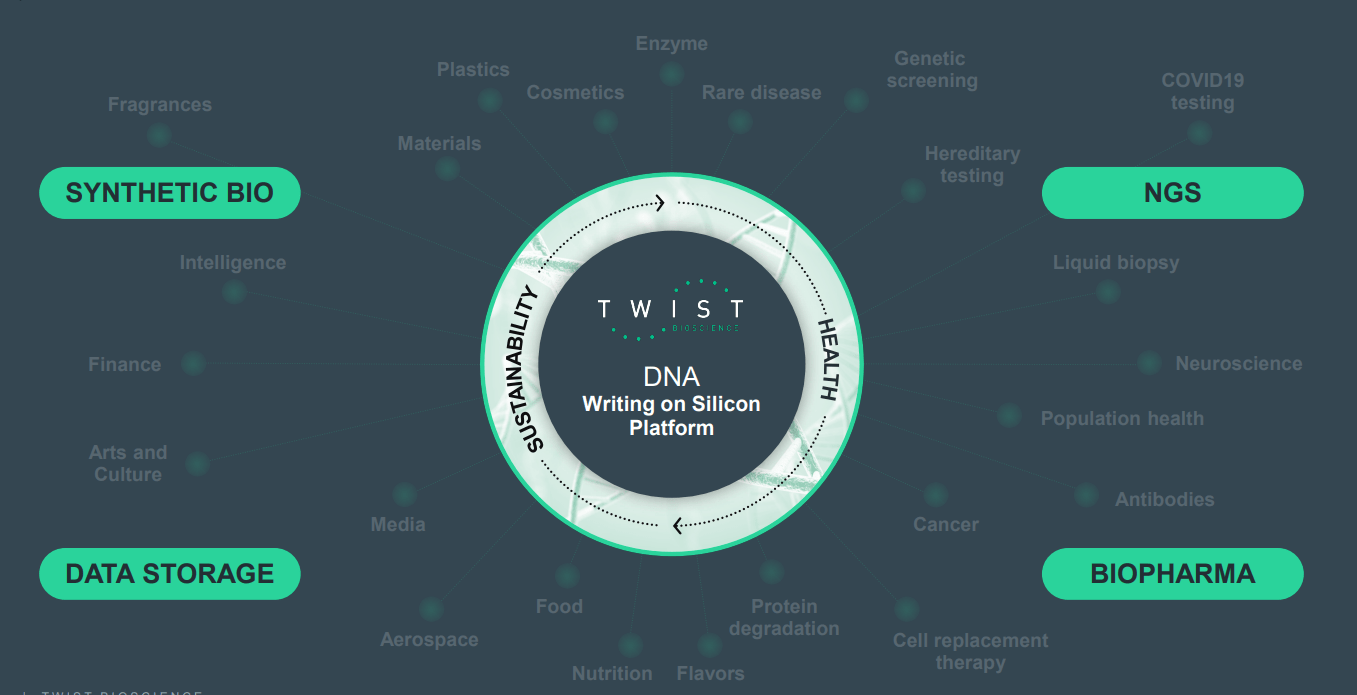

- Twist's portfolio touches on several fast-growing areas across antibody discovery, NGS (next-generation sequencing) and synthetic biology. Management reminds us that recently reported quarterly revenue came in at $56M and almost $60M of bookings/orders. NGS segment is going "extremely well" with demand coming in from liquid biopsy and clinical oncology diagnostics. Customer base is increasingly broad (working to minimize concentration risk. For this year, projected NGS business revenue is just under $100M (up from $73M last year and $44M year prior). Tailwind in NGS is due to strength of portfolio and value proposition (reduce sequencing costs for customers by roughly 50% and give faster time from sample sequencer).

{kind=link}

Figure 2: Twist is the infrastructure powering the biodiscovery ecosystem (Source: corporate presentation )

- Synthetic bio segment is also going well and seeing a pick-up in customer base. Relationship with Gingko is great and achieved remarkable scale (billions of nucleotides) over the time together. Synbio business is projected to be ~$80M this year (up from $50M last year)

- Moving on to their biopharma business (antibody discovery), they are projecting $26M of revenue this year. A few customers are canceling orders in the short term (a result of the increasingly difficult financing and market environment for the biotech sector). Management tries to portray this as glass half full (reducing costs for customers will resonate in this environment), but at least in some respects the current environment is clearly a headwind for this business segment.

{kind=link}

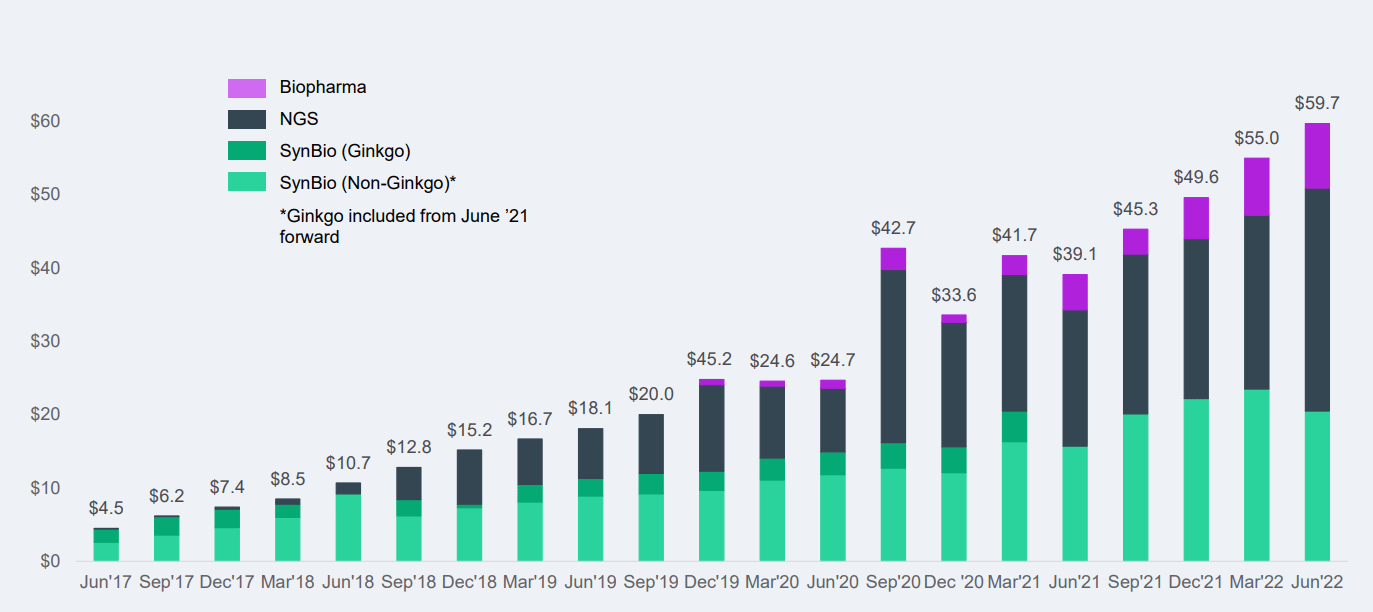

Figure 3: Revenue growth by business segment (Source: corporate presentation)

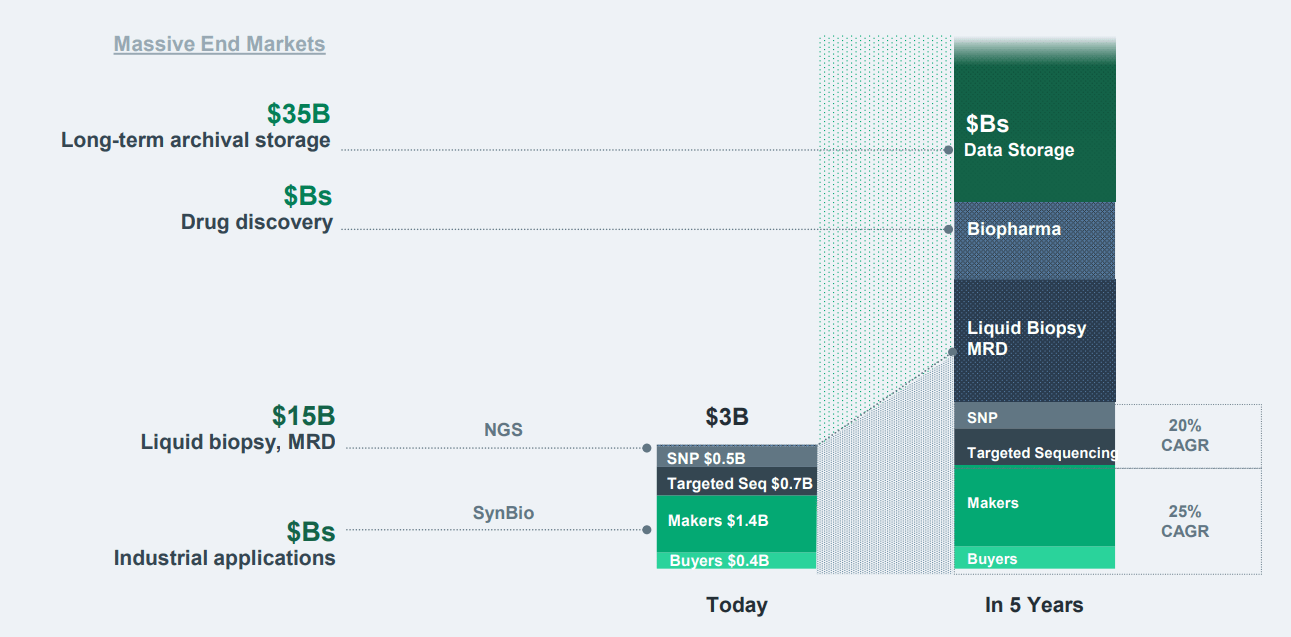

- Regarding their "factory of the future", the company is building a new 110,000 square foot facility at the site in Portland ($73M total invested of the projected $110M). It should come online shipping revenue in January of 2023. The end result is that the company will have faster turnaround time and scale the business to potentially $500M per year in the combined footprint. This will allow them in turn to go after the fast gene market (opens up the $1.4B maker's market). This gives them significant opportunity to scale the synbio business as the latest market segment is one they have not touched to date. Line of sight looks quite interesting here in next 3 to 5 years, projecting adjusted EBITDA to achieve break-even at $300M with cross-margin about 50%. This year for the core NGS & synbio business revenue is just under $180M (growing at excess of 40% per year).

{kind=link}

Figure 4: 5-year line of sight with some pretty sizeable end markets (Source: corporate presentation)

- As for opportunity in synthetic biology outside of Gingko, customer list continues to expand as Twist offers customers the ideal combination of cost savings and increased shots on goal. If you are going to design a new pathway, enzyme or therapeutic, Twist is one of several logical options and they continue to see adoption across multiple market segments. Impact of the "factory of the future" (increased turnaround time) will open up a segment of the market they don't currently have access to (also benefits some of larger pharmaceutical partners). They continue to add products to this portfolio, including from the academic setting and hope to move up the food chain in coming years.

- In the next 3 to 5 years, their synbio customers are focused on very difficult challenges to mankind today (energy dependency, food yields, novel treatments for disease) and these are all underpinned by synthetic DNA (and thus Twist's platform).

- As for NGS segment, the company recently introduced the rapid turnaround customizable panels for MRD detection in cancer screening. Management states that they are seeing significant inbound interest and will be a class-defining product (500 targets and 6 days from order at a good price point). Guidance seems to be cautious in the near term (testing, validation work to be done, etc.). Core premise is more samples will be analyzed as sequencing costs go down (volume of data goes up). Market is quite fragmented (the key caveat). In terms of revenue guidance for NGS business for the year, they are projecting $97M for the year (started year at $94M). They continue to see pick up in terms of large customer adoption and adoption in other areas (started launching synthetic controls at the beginning of the pandemic, has expanded into monkeypox and oncology controls). They are not a cheaper product but save the customer costs in sequencing (better use of "sequencing real estate"). Bottom line is that economics matter and cost of sequencing will continue to go down as number of samples goes up.

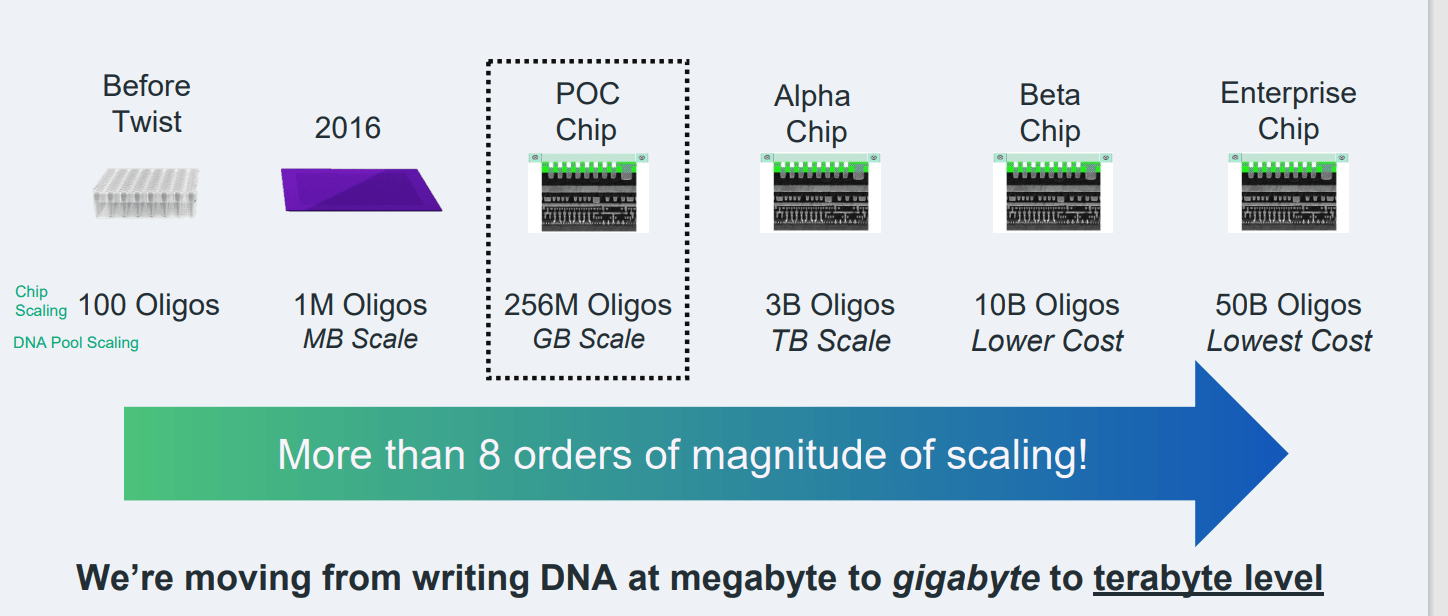

- As for data ((DNA)) storage segment, they have proof of concept $256M oligo data storage chip. Next phase is how to take it to the next level ($3B oligos in that chip). Recently, they launched a white paper highlighting opportunity in the marketplace (growing 30% to 40% per year). From technology point of view, goal is to debug the tech and continue with proof of concepts (more material updates coming in 2023). Storage market is segmented into hot (nanosecond response), warm (millisecond response) and cold (10 minutes to 48 hours). Twist is going after the cold storage (archival market). They are up against a 70-year-old technology and see a gap between demand and supply that could be a large opportunity for them in 10 years (to be fair, there will be multiple solutions and DNA will only be one of them). As for the ecosystem, DNA founding alliance started in October 2020 with Microsoft (MSFT), Western Digital (WDC), Illumina (ILMN), and Twist. That alliance is now 70. Now, they have a seat at the table in terms of defining standards and broadening out the ecosystem. IT executives are looking at DNA storage as a solution for data gap they will experience in the next 5 to 10 years. Growth of the alliance has been surprising, highlighting interest in the space including from companies like Dell (DELL) and Seagate (STX). Long term opportunity is to get into storage centers. Analyst notes that the TAM (total addressable market) for DNA storage is $35 billion. Management remarks are quite optimistic here ("no reason why this can't be a $2 billion market for Twist"). They have early mover advantage and are investing a lot into IP (think it could be a 60% gross margin business).

{kind=link}

Figure 5: Roadmap for DNA data storage (Source: corporate presentation )

- In biopharma segment, Twist Boston had 53 to 54 customers last quarter running roughly 70 projects. Customer base has quite a few high-quality clients from large pharma to well-funded smaller biotech companies. This year they are projecting $26M of revenue and this quarter is $8.5M (bookings over $8.8M). It is a tougher economic environment but quality of services, team and additional capacity position them well for growth (trend to outsource also works in Twist's favor). Majority of this is antibody discovery and management was not able to break it down by disease area. Public and private market funding for biotech has admittedly been weak, and they saw two customer cancellations last quarter (one customer had $25M quarterly losses with $150M in cash). The other company was large, had $600M but significant debt so they reevaluated based on financial situation as well. Out-licensing deal with Astellas Pharma ([[ALPMY]], [[ALPMF]]) last quarter continues to be an opportunity (15 antibodies developed) with additional such collaborations to follow. 2020 to 2021 were their 2 best years ever in terms of funding before the current slowdown. They doubled down on investment in the business at the beginning of the pandemic and believe they can continue to deliver in a tough environment (sounds like a "glass half-full" take to me).

{kind=link}

Figure 6: Pipeline of functional monoclonal antibodies (Source: corporate presentation )

- As for China opportunity, team executed well despite adverse effects from lockdowns. Relatively new sales team is starting to see traction, but again they are starting from a very small number.

Let's move on to recent news and how it's affected the story.

Select Recent Developments

On January 25th, Twist announced new collaboration with Artisan Bio to engineer next generation cell therapies. Specifically, they will discover 5 novel antibodies against undisclosed targets provided by Artisan. Twist will receive upfront technology access and project fees for each program, success-based clinical, regulatory and commercial milestones, as well as royalties on product sales.

On February 1st, the company announced collaboration with Abcam ( ABCM ) in which the latter will use a proprietary Twist VHH phage library for antibody discovery, development and commercialization for diagnostic and research applications. I've made a mental note to check out Abcam at some point in the future and add it to my article queue, as the stock is trading at lows even as its global expansion efforts continue extend the company's antibody and digital leadership.

Moving on, on March 9th Twist announced an agreement with Kriya Therapeutics around antibodies delivered using adeno-associated viral ((AAV)) gene therapy in therapeutic oncology applications.

From there, a more material development took place on April 5th with signing of a new agreement with partner Gingko Bioworks to expand the depth and breadth of the collaboration between two of the leading organizations in the synthetic biology ecosystem. The four-year agreement includes an increased commitment by Ginkgo to purchase products from Twist, with the option to access significantly more synthesis capacity to meet Ginkgo’s anticipated growth. Such a large DNA supply agreement has the scale to impact multiple industries and it's clear that much of Twist's future rests on the shoulders of its key partner in the synthetic bio space.

On April 7th, Twist signed an agreement with cell therapy company MediSix Therapeutics to discover novel antibodies against five undisclosed targets. Deal terms seem typical, characterized by upfront payment and eligibility to receive milestone payments plus royalties on net sales (focused on downstream economics).

Another big-name deal took place on May 9th, as Twist announced research collaboration and exclusive option license agreement with Astellas Pharma. The goal here is to jointly conduct research activities to identify and optimize proprietary Twist antagonist antibodies, targeting an undisclosed checkpoint inhibitor pathway in the tumor microenvironment ((TME)), as potential therapeutic development candidates. Astellas will have the exclusive option to license any development candidates generated as part of the collaboration, while Twist receives typical mix of upfront payment, milestones and royalties.

Skipping forward to August 2nd, Twist shared a new white paper from Furthur Market Research highlighting the increasing need for new enterprise storage technologies that can be deployed more cost effectively at massive scale with minimal power consumption (DNA data storage fits this definition). Demand growth rates exceeding 25% annually would exceed available supply of enterprise-grade media, necessitating novel options to be introduced and adopted. Two scenarios posed are 35% annual growth rate pointing to 7.9 million petabytes zone of potential insufficiency during 2030, while projected 45% annual growth rate would make that number exceed 25 million petabytes (triple). Twist CEO stated that DNA storage offers the unique combination of ultra-high-density, reasonable cost, and sustainability to address the $7B or more of unmet storage demand projected in coming years.

Also on August 2nd, Twist announced that partner Biotia received expanded Emergency Use Authorization ((EUA)) from the FDA for its SARS-CoV-2 Next-Generation Sequencing ((NGS)) Assay for the qualitative detection, identification and differentiation of SARS-CoV-2 lineages and identification of specific genomic mutations. The Assay was developed in 2020 and has the ability to analyze the entire RNA viral sequence, and to determine the presence or absence of the virus. CEO notes that they continue to "believe this assay will be critical to monitor the sequence evolution of SARS-CoV-2" as the disease transitions to being endemic.

Other Information

For the second quarter of 2022 (fiscal third quarter), the company reported cash and equivalents of $527M as compared to net loss of $60M (up 50%). SG&A rose significantly to nearly $54M, while research & development expenses nearly doubled to ~$37M. I estimate that the company has about 2 years of cash on hand, so I would expect another secondary offering by 1H 2023.

Revenues rose from $35M to $56M, while cost of revenues rose to $31M. Total orders rose from $39M to nearly $60M.

For full year 2022, management has increased revenue guidance to $203M. SynBio revenue (including Gingko) is expected to be $80M (up from $71M - $73M). NGS revenue is estimated to be $97M (up from $94M -$96M). Biopharma revenue is expected to come in at the low end of expectations ($26M). Meanwhile, gross margin is expected to be 40%.

As for prior offerings, $250M secondary in February was closed at price point of $55/share (representing nearly 40% upside from current levels).

As for competition, one could argue it is getting even more heated and DNA synthesis becoming more and more of a commodity. Some companies they are competing with in core SynBio space include peers that are far better capitalized with resources necessary to "out-muscle" smaller players (think GenScript, DNA Script, GENEWIZ, Integrated DNA Technologies which is owned by Danaher (DHR), GeneArt which is owned by Thermo Fisher Scientific (TMO), Sigma-Aldrich Corporation which is owned by Charles River Laboratories (CRL), Promega Corporation, OriGene Technologies and others. In NGS, they are competing with Thermo Fisher Scientific, Illumina (the giant that comes to my mind instantly), Agilent (A), and Roche NimbleGen, to name a few.

As for institutional investors of note , ARK Investment Management continues to own an 11.14% stake in the company (not much of a green flag these days given Cathie Wood's dismal performance and constant cycle of expressing confidence in key holdings followed by selling them out at lows when they disappoint). Generalist investor BlackRock owns an 8.7% stake.

As for insiders, founder William Banyai owns over 250,000 shares. Steady stream of insider sales over the past couple years is potentially a negative indicator (I would like to see more conviction from management as well as more skin in the game).

As for relevant leadership experience, Chief Commercial Officer Patrick Finn served prior as VP Sales and Marketing for Enzymatics (acquired by Qiagen).

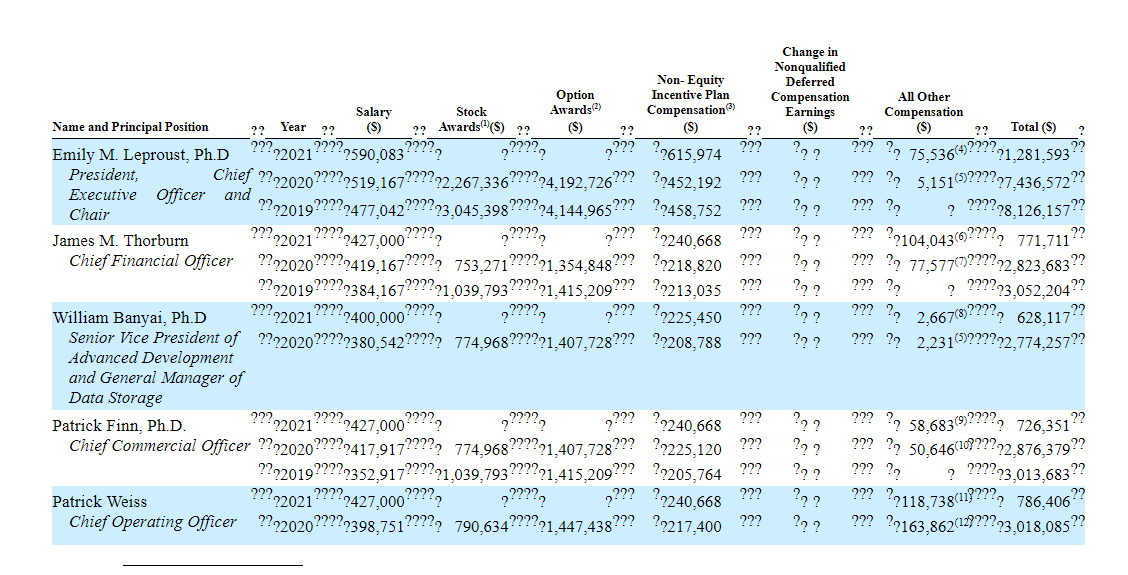

Moving on to executive compensation, cash portion of salaries appears in the expected range ($350k to $600k). Likewise, I don't see stock and options awards as being excessive.

{kind=link}

Figure 7: Executive compensation table (Source: proxy filing )

The important thing is to avoid companies where the management team is clearly in it for self-enrichment instead of creating value for shareholders, and looking at compensation is one of several indicators in that regard.

Final Thoughts

To conclude, I do appreciate how this management team is consistently executing in a difficult environment, particularly with core business segments of SynBio and NGS. Increasing full year revenue guidance was a bullish signal and again per commentary on the prior call there is a clear path forward in coming years to break-even EBITDA for certain segments and improving margins. Conversely, inflationary pressures are a cause for concern as is the commoditization of certain areas like DNA synthesis (to my eyes at least).

As seen with my recent article on partner Gingko Bioworks ( DNA ), I have a hard time with companies where aggressive assumptions are made regarding total addressable market in 5 or 10 years timeframes, as well as business models relying on downstream economics while realizing very little of the deal value upfront. Speaking of Gingko, the collaboration could be a double-edged sword in that the close integration of the two companies' efforts provides a nice tailwind in SynBio but also poses concentration risk for Twist should anything go awry.

For readers who are interested in the story and have done their due diligence, TWST is a Buy at current levels and especially on subsequent dips. However, I caution that it's only appropriate for patient investors with long term time frame.

From a Core Biotech perspective (emphasis on next 3 to 5 years), much like with Gingko Bioworks I confess my lack of familiarity with this space and am not as comfortable with relying on a business model where there's not much visibility in terms of downstream economics and when they will be realized.

Risks include additional dilution by the first half of 2023, further slowdown in the biopharma services segment of the portfolio and potential inability to hit recently raised revenue forecast (unlikely as management has been quite consistent in their execution). Fierce competition in several areas in which they operate is my chief concern, including SynBio and DNA storage. Increased commoditization of said field could result in lower margins and decreased longer term upside potential.

Author's Note: I greatly appreciate you taking the time to read my work and hope you found it useful. Look forward to your thoughts in the Comments section below.

For further details see:

Twist Bioscience: DNA Synthesis Leader Appealing 'Picks And Shovels' Play