AQN - Two 13% Yields To Buy In April

2023-04-05 07:35:00 ET

Summary

- I love a good contrarian investment, where I buy against market sentiment.

- You can unlock massive yields, but first, you must evaluate the fundamentals to ensure they are sound.

- Retirement requires cash to pay your bills; get it from your investments.

Co-produced with Treading Softly.

Have you ever bet on the underdog?

People seem to love a good underdog story, coming from a disadvantaged place and succeeding despite all odds. Betting on the underdog can be extremely profitable when everyone else is betting against them.

Other people love a "sure thing." They don't like taking risks or betting against the norm, and I get that. However, in order to be a truly skilled income investor, you need to get some contrarian thought flowing through your blood. The most popular dividend stocks have yields that are in the low single digits. To get a reasonable income, you would need to invest millions.

The market often moves like a herd, chasing the next "cool" thing while selling off what is misunderstood and unpopular. Those income stocks cast off to the side trade at lower prices and earn buyers a higher yield.

This is where we can lock in massive income from just a little capital invested. It does require a level head, a strong understanding of what you're doing, and a willingness to take on the risk of knowing your underdog may still lose in the final round. But when getting compensated with yields in the mid-teens, there is bound to be some risk-taking accepted.

Today, we're going to look at two misunderstood underdogs who are primed to provide good income with strong potential to shine in the future.

Let's dive in.

Pick #1: AQNU - Yield 13%

When it comes to poorly timed acquisitions, the Algonquin Power & Utilities Corp. ( AQN ) acquisition of Kentucky Power has to take the cake for unfortunate timing.

AQN has a long history of growing rapidly through buying other utilities and bolting them onto their current portfolio of holdings – especially when it comes to regulated utilities. They've been a master at doing so efficiently and effectively over the years, with most of their earnings growth coming from acquisitions.

Then AQN decided to take on an ambitious purchase of Kentucky Power from American Electric Company ( AEP ). This acquisition led to conflict with regulators that delayed the closing, and to make things worse, interest rates started skyrocketing. This planned $2.6 billion acquisition started to become a massive burden on AQN's balance sheet as the costs associated with it rapidly rose alongside interest rates.

The longer the market had to digest this planned purchase, the more investors soured on the deal. To make matters worse, credit rating agencies started to sour on AQN's credit rating – which would only compound the cost of getting financing for future activities.

What did AQN's management do? They gave up their long track record of dividend growth and cut their dividend. This reduced how much cash they were sending out the doors each quarter to allow them to do more with less financing. Second, they reduced their capital spending plans. The two steps they undertook are prudent choices but make the growth story of AQN appear to be in the past.

AQN reduced its planned capital spending in 2023 to $3.6 billion. This may still sound large, but the Kentucky Power deal is $2.6 billion, leaving only $1 billion for them to spend on other organic growth – this means we should expect very little if any earnings growth from AQN in 2023 aside from the KY power purchase. Also, AQN is focused on completing $1 billion in "capital recycling" - aka asset sales. AQN has long been known for building renewable assets and selling off part of its ownership of them to outsiders and unlocking that capital.

Part of these asset sales may come from Atlantica Sustainable Infrastructure plc ( AY ), which is completing a "strategic review." AQN owns approximately 42% of AY shares, and if AY does go private or get taken over, AQN would receive a large payout. AY's market cap is $3.14 billion, meaning AQN has over $1.3 billion in value at the current trading price in AY.

So, while AQN's quarterly earnings were sound, fully covered their (new) current dividend, and more than effectively serviced their debt, the KY power purchase remains the overhanging cloud on AQN's share price.

Thankfully, we got a small update on this attempted purchase at Q4 earnings. Previously AQN and AEP submitted their plans to FERC - the Federal regulator that must approve the purchase and who previously rejected the transaction from being completed – with the hopes of approval before the closing date of April 26th. This approval needs to come quickly for the purchase to be completed, otherwise AQN can walk away from the deal or force further concessions from AEP.

This deal was originally announced in 2021 when rates were at historic lows and AQN has been attempting to complete it. However, various hurdles from AEP and regulators have delayed it.

If AQN completes the purchase, we expect it will take time to absorb the acquisition and see positive results in cash-flow. We are expecting with the already intense negativity towards the deal in Kentucky that FERC will reject the purchase again, leaving AQN a chance to cancel the purchase in full. The market might hold a grudge about the dividend cut, but AQN would be able to more quickly resume dividend raises and focus on growth plans that are more appropriate in a higher rate environment.

AQN did receive some good news in recent months, due to their dividend cut and reduced capital spending plans, their credit rating was upgraded back to a stable outlook from a negative outlook. Maintaining a BBB rating is crucial, as it can greatly impact the cost of future borrowing. For a utility company, credit ratings can make the difference on whether they can afford to expand at all. The dividend cut was painful for common shareholders, but at least it achieved the goal of protecting the credit rating and keeping prospects for future growth alive.

We see Algonquin Power & Utilities Corp. Equity Units Due 06/15/2024 ( AQNU ) as a positive risk-reward investment offering high income now while there is a massive question about AQN's future potential. If the KY power deal falls through, we expect AQN's share price to appreciate as investors are not keen on its completion. If it is completed, AQN's ability to pay AQNU holders is not in question however AQN's dividend growth will be stalled. By 2024, when the units convert, AQN would be starting to see the cash flow benefits.

We see both outcomes providing a lift for the common share price eventually. AQNU are convertible units that pay a fixed dividend up front, and in June 2024, are converted into common equity. For the common share price, 15 months is a very long time and provides an opportunity for all the concerns about the KY acquisition to be answered definitively one way or the other. AQNU pays a hefty 13% yield while we wait.

Pick #2: NLY - Yield 13.8%

Annaly Capital Management, Inc. ( NLY ) recently announced the dividend cut that management telegraphed at Q4 earnings – and the price went up. The macro events are overshadowing the dividend. NLY sold off along with everything else that touches the financial world when Silicon Valley Bank failed. Investors saw a bank failure, and panic sold everything "financial."

Some were claiming that SVB's failure was a "Lehman moment," and a few are still saying that it will be. If it is, that is great news for NLY investors. Let's take a look at what happened to NLY from September 1st, 2008 (two weeks before Lehman filed bankruptcy) through the end of 2009:

NLY's price went up, its dividend went up, and the rest of the market went down – it was fantastic for NLY. Though it is interesting to note that as strong as NLY's 2009 was, the initial reaction to the Lehman collapse was a selloff. NLY sold off along with everything else. It wasn't until a couple of months later that NLY started heading upward and outperformed the market.

NLY is one of the best companies to own if you believe that there will be a financial crisis. This might seem odd since NLY is part of the financial world, but the reason is the assets that NLY holds.

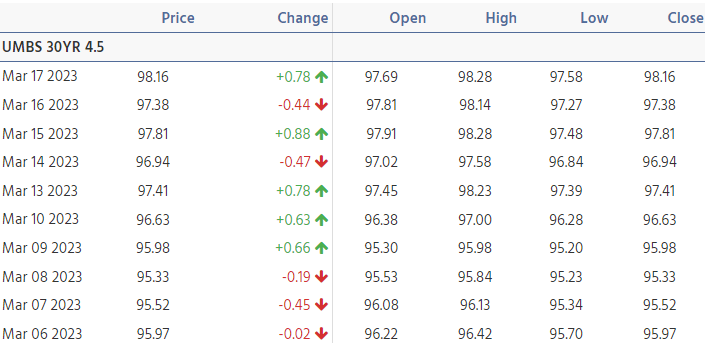

NLY owns agency MBS – an asset class that is considered to have no credit risk because if a borrower defaults, the "agency" (Fannie Mae or Freddie Mac) buys the mortgage back at $100 par value. Here is a look at the 4.5% Coupon MBS prices: Source .

{kind=link}

Note that they started rallying significantly on March 9th as the news of bank failures was just starting. They rallied from $95.33 to $98.16 the following week, a 2.9% increase.

2.9% might not sound like a lot until you consider that NLY owns over $70 billion in agency MBS. Now 2.9% of $70 billion is a lot.

On the other hand, MBS prices are still down a lot. A year ago, these 4.5% coupon MBS were trading at around $104 and bottomed in October 2022 at around $92. So, a recovery in MBS prices has started, but they still have a way to go.

We can't know for certain if this recovery will continue. The Fed is going to be very important. Will these events cause the Fed to be more cautious about hiking interest rates?

The market certainly thinks so and is pricing in an 89.3% probability that the Fed will be cutting interest rates by the end of the year. Source .

{kind=link}

This is a radical shift from just a few weeks back, when the market was projecting a 0% probability that the target rate would be below 450 bps. This shift has been caused by inflation not being as high as many feared and the cracks showing up in the financial system.

We don't know if this newfound dovishness will persist. What we do know is that if the banking system is going to melt down and a financial crisis starts, NLY is a stock we want to be holding.

If the system doesn't melt down, and interest rates stabilize in the 5%'s before trending back down more calmly, NLY is still a very attractive investment that will provide a hefty income while we wait for the interest rate cycle to turn.

Conclusion

With AQNU and NLY, we can collect strong income now as we watch future events unfold and impact their trading value. Take 13% yields now and enjoy the income they provide over the long haul.

With any income portfolio, investors should be careful not to place any bet on just a few select names – don't bet the farm on ten picks alone! We recommend holding over 40 unique investments. Furthermore, we suggest having at least 40% of your portfolio invested in fixed income to provide a stable foundation for your recurring income stream and to reduce volatility – so when your underdogs move rapidly, your portfolio isn't shaken or stirred.

I want a retirement where I have plenty of income to pay my bills and enjoy my hobbies. I also want to have excess income that I can invest in underdogs I see at amazing yields with a clear path to strong total returns over an expected period of time. Looking ahead, AQNU and NLY can provide you with that.

If you like dividend stocks, check out our other previously provided public articles, or check out our 'Model Portfolio,' which has an average yield of over 9%.

In the end, I want you to have an abundant and enjoyable retirement that is supported by outstanding levels of dividend income. That is what our Income Method can accomplish for you, and that's the beauty of income investing.

For further details see:

Two 13% Yields To Buy In April