TWO - Two Harbors: A Mortgage REIT Recovery Play With A 13% Yield

2024-01-07 02:53:15 ET

Summary

- Two Harbors stock is a potentially attractive investment opportunity in the mortgage REIT sector.

- The Federal Reserve's decision to lower the federal fund rate in FY 2024 could benefit mortgage REITs by reducing interest expenses and reducing pressure on MBS values.

- As a result, Two Harbors may see improved portfolio performance and return to book value growth.

- Shares are trading at a 12% discount to book value and are cheaper than those of Annaly and AGNC.

In the last two months I bought into a number of mortgage REITs, including Annaly ( NLY ) and AGNC ( AGNC ) because the fundamentals in the sector are at the brink of improving. The Federal Reserve announced in December 2023 that it would seek to lower the federal fund rate this year which strongly suggests that the mortgage REIT sector is facing relief in terms of interest expenses. As a result, I believe the mortgage REIT sector in general has attractive revaluation potential and could return to a period of book value and earnings growth. Another mortgage REIT that I added last week was Two Harbors Investment ( TWO ) which cut its dividend twice last year, but which could now start to benefit from easing pressure on its MBS portfolio!

Previous rating

I worked on Two Harbors in 2021 and since owned a small position in the mortgage REIT. Since 2021 a lot has happened, however, chiefly because the Fed's raising interest rates aggressively during the 2022-2023 period hurt mortgage REITs' book values and dividend prospects. Since my last coverage, Two Harbors has lost more than 50% in value. With the Federal Reserve now being at the brink of changing its tightening policy, I believe Two Harbors, and mortgage REITs with mortgage-backed securities in their portfolios, could generate better returns for shareholders this year.

Two Harbors: agency and MSR investments

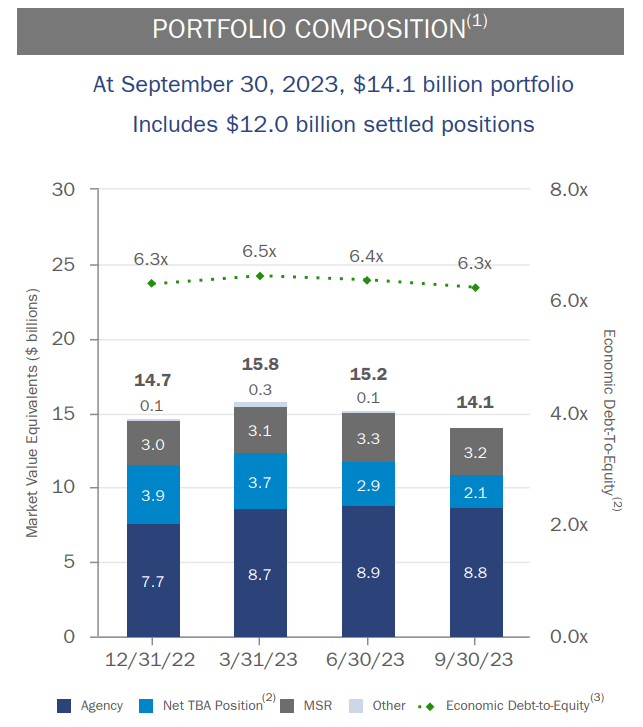

Two Harbors is a mortgage REIT with significant investments in residential mortgage-backed securities. Mortgage-backed securities, of which Two Harbors owned $8.8B worth of in September, are rate-sensitive assets and, like other fixed income assets, decline in value when interest rates rise. Now that the Federal Reserve has pretty much decided that its period of monetary tightening is ending in 2024, I expect mortgage REITs with mortgage-backed securities as their core investments to see improving fundamentals this year.

The reason for this is two-fold: 1) Mortgage REITs are leveraged, meaning they rely on a lot of debt to earn income. With financing costs set to decline in 2024, Two Harbors could see a positive catalyst for core earnings growth as soon as the Federal Reserve lowers its federal fund rate, 2) The relationship between interest rates and MBS values is inverse, meaning falling interest rates should be expected to result in a broad increase in the value of MBS portfolios, potentially resulting in a catalyst for book value growth as well.

{kind=link}

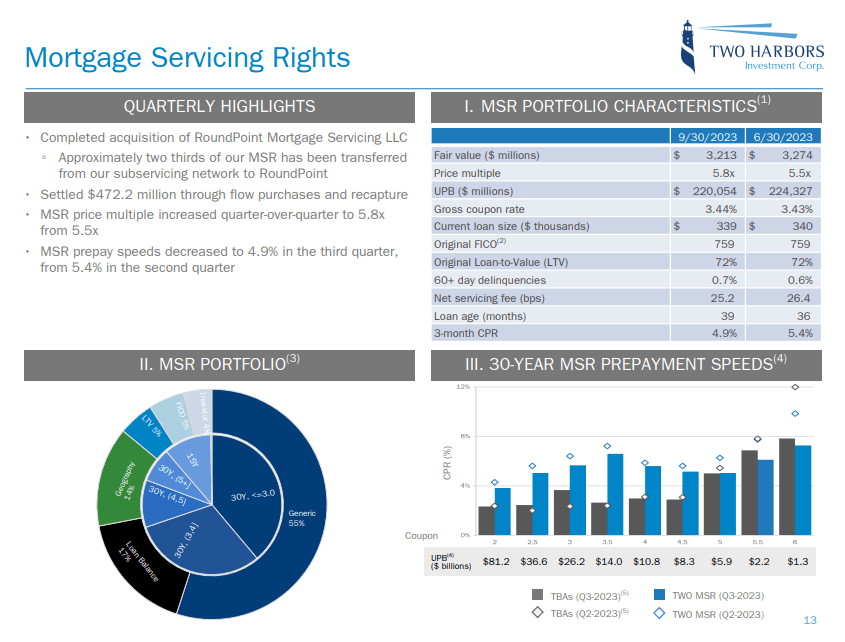

Besides $8.8B in MBS investments, Two Harbors owned a large block of mortgage servicing rights which provide the mortgage REIT with a hedge, so to speak, against rising interest rates. Higher interest rates cause the value of mortgage servicing rights to increase as the fee stream associated with such rights becomes more valuable in a rising-rate world. At the end of the third-quarter, Two Harbors owned $3.2B worth of mortgage servicing rights (fair value), representing an unpaid principal balance of $220B. The REIT’s primary investments are mortgage-backed securities, however.

{kind=link}

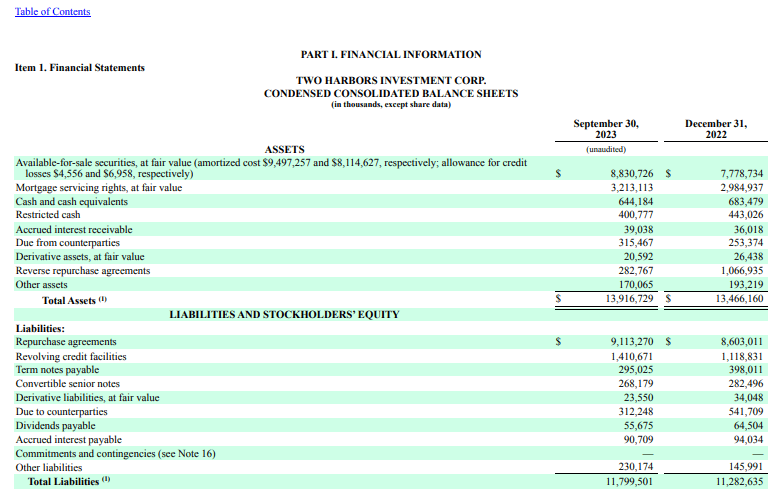

Consequently, the balance sheet chiefly consists of residential mortgage-backed securities and mortgage servicing rights and their corresponding repurchase and financing agreements. Two Harbors had $9.1B in repurchase agreements on its balance sheet as of Q3'23 as well as $1.4B in revolving credit facilities. A decline in interest rates would most likely benefit Two Harbors' net interest expense line positively. The REIT's leverage ratio was 6.3X at the end of Q3'23 compared to 6.4X in Q2'23.

{kind=link}

Earnings available for distribution

The more expensive debt becomes, the weaker the earnings prospects are for mortgage REITs. Two Harbors suffered from rising interest expenses in a rising-rate world in FY 2023 and in the third-quarter the mortgage REIT reported negative net interest expenses of almost $50M. A decline in interest expenses is therefore the fastest way for Two Harbors to achieve an improving earnings trajectory in FY 2024.

In the last year, the REIT has seen a material increase in its net interest expenses which outstripped the growth rate in its interest income by a wide margin (108% interest expense growth vs. 31% growth in interest income). With interest expenses rising much faster than interest income, the REIT also suffered a major contraction in its earnings available for distribution ((EAD))... which declined by a massive 84% year over year. The consolidation of its EAD has been the main reason behind Two Harbors cutting its dividend twice since FY 2022. A normalization of the interest expense picture, which has gotten much worse in the last year, could help Two Harbors restore its EAD and result in a safer dividend for investors.

The Federal Reserve has made clear that investors and mortgage REITs can expect lower interest expenses this year which in turn could boost Two Harbors' earnings potential and reduce the risk of additional dividend cuts.

| () |

| Q3'22 |

| Q4'22 |

| Q1'23 |

| Q2'23 |

| Q3'23 |

| Y/Y Growth |

| Interest Income |

| $94.4 |

| $99.3 |

| $116.6 |

| $117.8 |

| $123.6 |

| 30.9% |

| Interest Expenses |

| $83.4 |

| $115.6 |

| $142.5 |

| $159.6 |

| $173.1 |

| 107.6% |

| Net Interest Expenses |

| $11.0 |

| -$16.3 |

| -$25.9 |

| -$41.8 |

| -$49.5 |

| - |

| Earnings Available For Distribution |

| $68.9 |

| $34.6 |

| $20.6 |

| $8.4 |

| $11.3 |

| -83.6% |

(Source: Author)

Two Harbors is trading below book value

Mortgage REITs have started to trade at larger discounts to their respective book values in the last several quarters as the potential for book value declines in a high-rate world dampened prospects for growth. Dividend cuts have also hurt investor confidence and Two Harbors is not without fault here: the mortgage REIT lowered its dividend twice since FY 2022, by a total amount of 34%.

Besides pressure on its costs, Two Harbors has suffered a decline in its book value, as most mortgage REITs have. Two Harbors saw three straight quarters of book value declines in FY 2023 and suffered a total decline of 13% to $15.36 per-share.

Two Harbors

Currently, shares of Two Harbors are valued at 0.88X book value which compares favorably to the price-to-book ratios for Annaly and AGNC, both of which are now trading at premiums to book value... after a strong recovery push in November and December. Investors may still underestimate the potential for a recovery in the MBS market which is likely the reason why shares of TWO are still selling for a discount to book value.

In a low-rate world, I estimate that Two Harbors could revalue to book value and possibly even trade at a small premium to book value as its EAD situation improves and dividend risks subside. Assuming that book value can be reached ($15.36), shares of Two Harbors have 13% revaluation potential.

Risks with Two Harbors

Should the federal fund rate stay higher for longer than expected then investors may find that it will also take longer for the investment thesis as presented here to gain traction, but even in this case I would rate Two Harbors as a buy due to the discount to book value that is currently available. Dividend investors, however, must be aware that Two Harbors has lowered its dividend twice since FY 2022 which attests to the risk of investing in mortgage REITs more generally. Mortgage REITs are subject to intense earnings volatility, which is chiefly related to interest rate and MBS spread volatility. Therefore, I would recommend to very much limit any kind of high-yield, high-risk mortgage REIT investment to a very small percentage of investment assets.

Final thoughts

I believe Two Harbors could potentially be an attractive investment for investors in a low-rate world as the mortgage REIT’s MBS-focused investment portfolio is set to experience less book value pressure going forward. With interest expenses also set to see some relief in FY 2024, I believe Two Harbors could return to a period of earnings growth and a more stable dividend. Since Two Harbors’ shares are selling for a 12% discount to book value, I believe the risk profile is attractive enough to warrant a speculative buy position for income!

For further details see:

Two Harbors: A Mortgage REIT Recovery Play With A 13% Yield