TWO - Two Harbors: The Book Value Is Still The Issue

Summary

- External economic factors are making Two Harbors Investment Corp.’s position quite challenging in 2023, and the book value per share is likely to decline further.

- Futures markets initially predicted that the U.S. Federal Reserve would cut interest rates twice before the end of 2023, but there might be no rate cuts at all in 2023.

- The company reported surprisingly good Q4 earnings, but the reverse stock split and declining book value trend suggest caution for investors.

Investment thesis

Two Harbors Investment Corp. (TWO) reported positive fourth-quarter results compared to their not-very-great third-quarter figures. Despite this positive news, the book value per share has been declining for years, and their portfolio is under pressure due to external market forces such as the RMBS market issuances and still-rising interest rates. In addition, the latest inflation report suggests that the Fed might not cut interest rates at the end of 2023 but rather keep them at elevated levels, which will prolong the difficulties TWO is facing. The stock is fairly valued, but if the book value keeps dropping, the current price could easily become overvalued within a year.

RMBS market for 2023

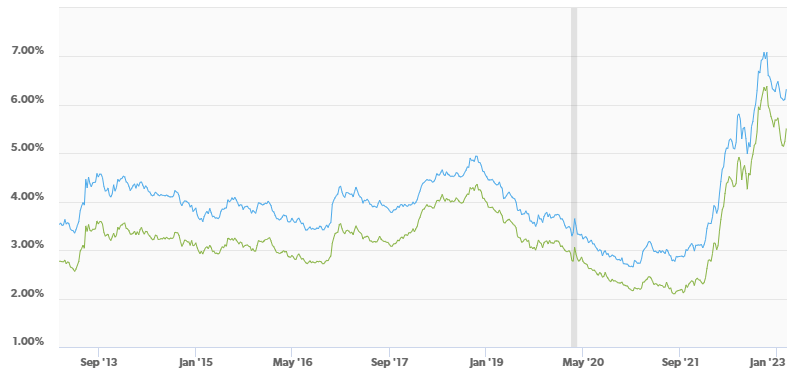

The last quarter of 2022 and the beginning of 2023 were quite turbulent in the mortgage markets. Last October, mortgage rates reached a more than 10-year high of 7% due to the Federal Reserve making rapid rate increases in 2022. The housing sector was hit the hardest by this, with mortgage rates almost double what they were a year prior. Since the peak mortgage rates have slightly declined. Mortgage rates have been slowly but steadily decreasing since last November (but we have seen a small uptick in February) and enjoying a bit of a positive impact on the housing market. The average rate for a fixed-rate mortgage increased in February following the 10-year Treasury, which rose from 3.39% at the beginning of the month to 3.86% this week. Freddie Mac reported that the 30-year fixed-rate mortgage increased to an average of 6.32% yesterday, compared to 6.09% from the beginning of February.

{kind=link}

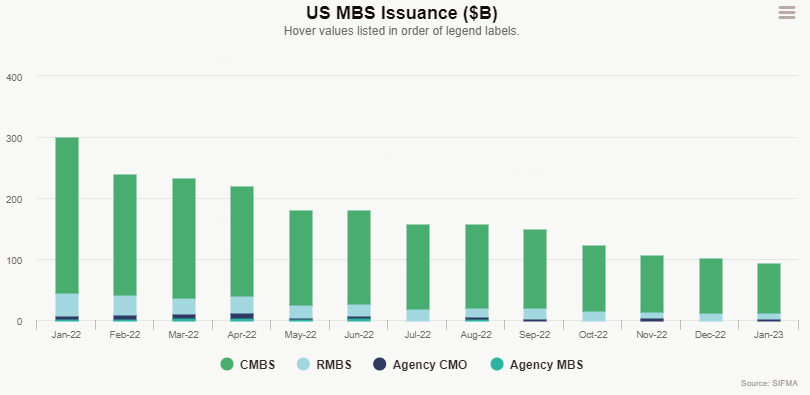

In the fourth quarter of 2022, an average of $13.3 billion RMBS per month was issued in the U.S. I assume the first quarter of 2023 will be similar, we already see January's figure of the issuance of $11.9 billion RMBS. However, these issuances are down by 60-65% Y-o-Y. Both CMBS and RMBS issues are down by significant numbers, and the vast majority of TWO's portfolio consists of residential mortgage-backed securities.

{kind=link}

Home prices have grown by approximately 20% since the start of the pandemic, and despite recessionary fears, prices have not dropped significantly (yet). So, it remains difficult for many potential buyers to purchase a home. This is further complicated by current owners who are reluctant to sell due to the ultra-low mortgage rates they got in recent years. I expect this trend to continue in the upcoming months, possibly until late 2023. The number of completed transactions of single-family homes, townhomes, condominiums, and co-ops fell by 38% by the end of 2022 compared to the beginning of 2022, and the current figure is approximately 25% lower than that pre-pandemic average home sales number.

In addition, in the past few months, investors had been expecting the Federal Reserve to reduce interest rates at the end of 2023. However, recent higher-than-expected U.S. inflation rate figures have caused analysts and investors to rethink their earlier predictions. Futures markets initially predicted that the U.S. Federal Reserve would cut interest rates twice before the end of 2023, but since the January inflation report came this week, futures markets suggest there might not be any rate cuts at all at the Fed's later-year meetings in 2023. This will prolong the pressure on TWO's portfolio for this year.

Q4 results

Two Harbors Investment Corp. reported fair fourth-quarter earnings after the Q3 disaster. The book value at the end of Q3 was $16.42 per share, representing a -16.2% total economic quarterly return. In Q4 the economic return was +11.6%. The portfolio performance reflected one of the most challenging market environments in decades in the third quarter, and the fourth quarter positivity is rather just a temporary good performance. While the interest income has seen a surge of 5.2% compared to Q3 due to the rise of cash rates, the decrease in RMBS portfolio size has somewhat leveled it out. MSR borrowing expenses rose significantly (by 38%) due to higher financing rates and larger average balances, while RMBS expenses dropped because of a lesser average balance. The book value has been declining steadily for years, in the last quarter of 2020 the book value per share was $30.52 (adjusted for the reverse stock split) and by the end of 2022, this figure was down to $17.72, even with a 7.9% increase compared to Q3 2022.

Fourth Quarter Presentation 2022

In the third quarter, the company sold RMBS and used some of the proceeds to repurchase 2.9 million preferred shares. This has continued in the fourth quarter, with another 2.9 million preferred stocks repurchased in the open market. This signaled to me that the company has faith in the value of these shares. It's clear to me that TWO's management sees their preferred stocks as a good investment. I cannot say the same about its common stock. Moreover, the company made a one-for-four reverse stock split in November 2022, which could also be a red flag for investors.

Valuation

In my opinion, TWO is trading at a fair price at the moment, but as the book value declines this price might seem overvalued in a year. It is trading at 1.04x its book value, which is in the upper part of the last 12 months, the average would be approximately 0.92-0.94x. There were times when TWO was trading at 0.8x its book value just a couple of months ago due to its share price decline in September and October, so the current price and book value seems fair. However, if the book value per share continues to decline in line with the current trend (which is approximately 16-20% per year), by the end of 2023 the book value could be around $14 per share. In that case, the current $17 stock price could seem overvalued. That is why I am neutral on TWO.

Final thoughts

Two Harbors Investment Corp. has been struggling to maintain its book value per share for years, and due to the challenging economic circumstances, this is likely to continue in 2023 as well. The longer-than-expected elevated interest rate environment will also have a negative impact on its portfolio, and I am not sure in the long term they can generate substantial shareholder value. Two Harbors Investment Corp. stock is fairly valued, but if the book value per share continues to decline the current price is rather overvalued. The reverse stock split is also a warning sign for me, so that is why I rate TWO as a Hold.

For further details see:

Two Harbors: The Book Value Is Still The Issue