TWO - Two Harbors: Two Yields

Summary

- Two Harbors recently cut its quarterly cash dividend payout by 12% with its yield now at 14.2%.

- A further near-term cut to the payouts is likely with the mREIT's earnings and book value to face headwinds this year.

- The preferreds come with a 9.2% yield on cost and a 52% yield to call.

Two Harbors ( TWO ) faces a sustained erosion of its book value and a quarterly dividend payout now under siege from rising Fed funds rates. The mortgage REIT last declared a quarterly dividend payout of $0.60 per share, a 12% decline from its prior payout, for a 14.2% yield.

The St Louis Park, Minnesota-based externally managed mREIT has had a tough few years with the direction of total returns first reflecting the pandemic and only partially recovering to then run into headwinds from the current rising Fed funds rate environment. Critically, it's the book value that matters and this last came in at $17.72 per share during the company's recently reported earnings for its fiscal 2022 fourth quarter. Whilst the commons trading at a 4.7% discount to book value might imply a certain margin of safety, this has been falling for a while now.

The First Yield

The mREIT had to engineer a 1 for 4 reverse stock split in November last year to hedge the prospect of delisting against a stock price approaching the NYSE minimum listing requirement. Book value per share of $5.87 in the year-ago quarter can be adjusted up to $23.48 to place the most recent figure at a 24.5% decline from its year-ago figure. The mREIT invests in agency residential mortgage-backed securities and mortgage servicing rights. This helped Two Harbors build a portfolio that was fully valued at $14.7 billion as at the end of its fourth quarter.

Earnings available for distribution was $22.2 million, or $0.26 per share, down materially from EAD of $73.3 million in the year-ago quarter. This was driven by an average portfolio yield of 4.92%, up from 4.61% in the prior third quarter. However, the mREIT's average cost of financing was 3.95%, up sequentially by 111 basis points from 2.84% in the prior third quarter. This meant a net spread of 0.97%, down from 1.77%.

The stabilization of the mREIT's book value forms the most near-term need for the bulls. On a quarter-on-quarter basis book value per share grew by 11.6% from $16.42 to reflect what was the mortgage spread tightening as well as the mREIT's purchase of 2.9 million shares of preferred stock. An action that contributed $0.26 to the book value during the quarter. The current rising rate environment is fundamentally an antithesis of the mREIT model which highly depends on leverage to drive returns. The current year poses uncertainty with inflation still elevated and the Fed signaling they are willing to go further than initial market expectations for only three 25 basis point hikes. Hence, we will likely see more volatility with book value this year even as the quarter-on-quarter results were positive and with the mREIT recently issuing 10 million new shares as a form of less expensive financing to expand its RMBS and MSR portfolio. Coverage of the dividends is currently impaired from an EAD perspective but the company fully covered it with a new metric introduced called income, excluding market-driven value changes. This was $0.73 per share during the fourth quarter.

The Second Yield

Two Harbors' 8.125% Series A Fixed-to-Floating Rate Cumulative Preferred Stock ( TWO.PA ) pays out a $2.03 coupon for a 9.2% yield on cost. Whilst this is around 500 basis points lower than the commons, it comes with close to zero risk of income deterioration. They're essentially a form of fixed income wrapped within an equity-like security with no voting rights but with a higher rank than the commons on the capital structure. This means they have a greater claim to earnings.

{kind=link}

To be clear here, any disruption to the mREIT's earnings has and will continue to be shouldered by the common shareholders with the preferreds trading with a cumulative clause. This means any unpaid distributions accrue as liabilities on the Two Harbors' balance sheet. With the Series A currently trading at $22.10, an 11.6% discount to their par value, their yield to call stands at 52% with total income payments of around $8.6275 until 2027 and a $2.9 uplift from a return to par.

The Series A will also move to a floating rate equal to three-month LIBOR plus a spread of 5.660% per annum. It's hard to forecast what interest rates will be at this date with both inflation and deflation being predicted by a range of economists for the next few years. LIBOR is also set to change to SOFR on June 30, 2023.

{kind=link}

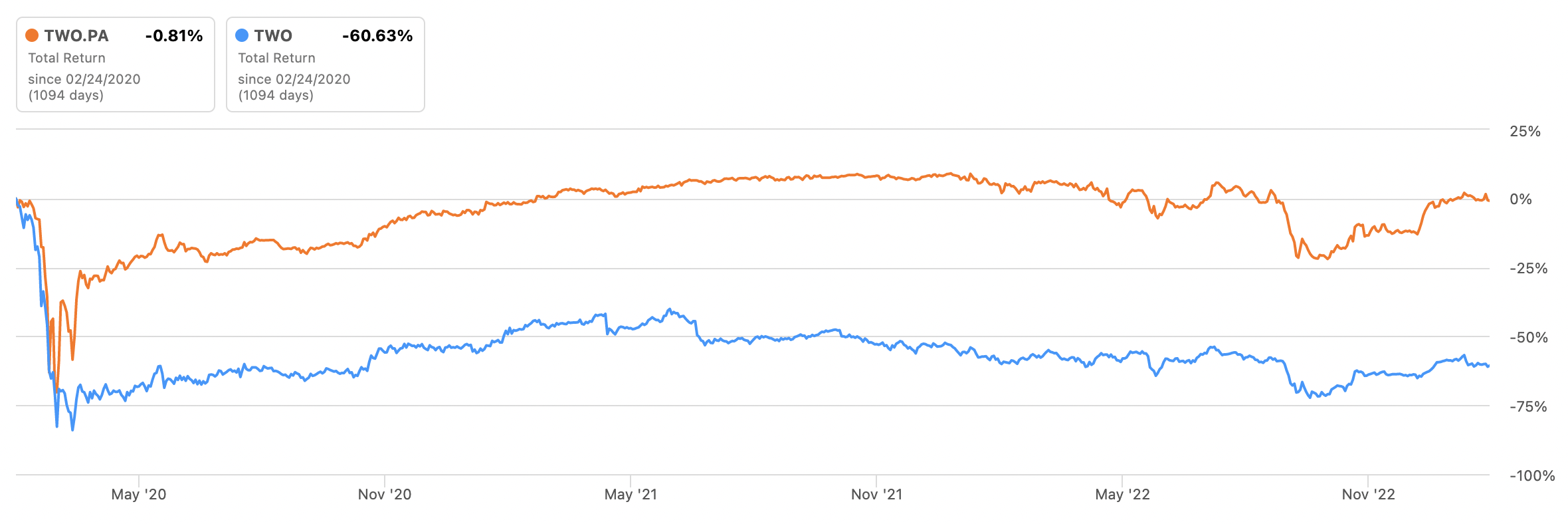

Over the last 12 months, on a total return basis, the preferreds are down by 5.05% versus 2.66% for the commons. Performance divergence over the last three years is stark with the preferreds down 0.81% versus a loss of 60.63% for the commons. Performance over the next year will likely see the preferreds outperform the commons with continued macroeconomic uncertainty and still rising Fed funds rate posing headwinds to the full stabilization of book value and earnings. Against this, the preferreds look like the better option for prospective investors.

For further details see:

Two Harbors: Two Yields