CWEN - TYG: Shares Underperforming Portfolio Could Present An Opportunity

2023-12-28 09:28:20 ET

Summary

- Tortoise Energy Infrastructure Corporation is a closed-end fund that provides access to a diversified portfolio of pipeline operators and renewable energy producers.

- The TYG closed-end fund offers a higher yield of 9.92% compared to other energy infrastructure funds.

- The fund's performance has been mediocre, but its leverage has decreased, and its net asset value has increased, making it potentially undervalued.

- The assets held by the fund should enjoy relatively stable cash flows over time, but the fund's share price will exhibit a high degree of correlation with energy prices.

- The fund's distribution is fully covered, and it is trading at an enormous discount on net asset value.

Tortoise Energy Infrastructure Corporation (TYG) is a closed-end fund aka CEF that provides an easy way for investors to gain access to a diversified portfolio of liquids and gas pipeline operators along with similar companies. The fund is structured as a corporation, which allows it to be easily included in a retirement account or similar tax-advantaged structure. This could be a very nice thing for retirees or future retirees because master limited partnerships, or MLPs, have a number of characteristics that make them very good investment vehicles for those individuals who need income to finance their expenses without going to work every day, but tax laws make it very difficult to include these companies in a traditional retirement account. This fund provides a solution to that problem as well as providing shareholders with a very attractive 9.92% yield. This is a higher yield than most other energy infrastructure funds possess:

| Fund |

| Current Distribution Yield |

| Tortoise Energy Infrastructure |

| 9.92% |

| First Trust Energy Income and Growth Fund (FEN) |

| 8.30% |

| Neuberger Berman Energy Infrastructure and Income Fund (NML) |

| 10.32% |

| ClearBridge MLP and Midstream Fund (CEM) |

| 8.20% |

| First Trust MLP and Energy Income Fund (FEI) |

| 6.94% |

| Tortoise Midstream Energy Fund (NTG) |

| 8.95% |

The fact that this fund has a higher yield than many of its peers could appeal to those investors who are seeking to earn a very high level of income from the assets in their portfolios. However, if the comments on some of my previous articles are any indication, Tortoise is not exactly a well-liked fund manager among some investors due to losses suffered by one of their funds back in 2020 when the entire traditional energy sector collapsed following the imposition of the COVID-19 lockdowns. Those comments were generally directed at the Tortoise Midstream Energy Fund though, not at Tortoise Energy Infrastructure Corp. As I have pointed out in the past though, anyone purchasing a fund today will not be affected by events that occurred in the past because they are purchasing the fund as it is today.

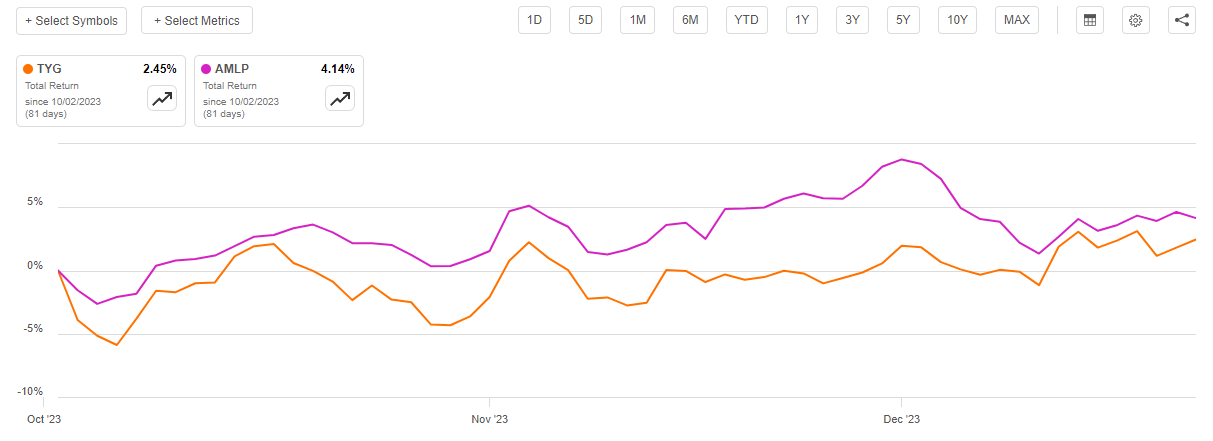

As regular readers can likely remember, we last discussed Tortoise Energy Infrastructure in early October 2023. The market has strengthened considerably since that time, although energy prices have generally not delivered the same price appreciation that we have seen in other market sectors. As such, we do not see the same recent strength from this fund as we have seen in some of the other funds that we have discussed over the past few weeks. Shares of Tortoise Energy Infrastructure are down 0.10% since the date that my previous article was published, which is a worse performance than the 1.97% gain of the Alerian MLP Index (AMLP):

{kind=link}

This is something that will likely disappoint potential investors, especially those who remember my previous article. After all, in the previous article, I did show that this fund has historically underperformed many of its peers.

However, Tortoise Energy Infrastructure has a higher yield than the Alerian MLP Index. The index yields 8.30% at the current price. As such, we can expect that the fund's comparative performance will look better when we include the distribution in the performance chart. When we do this, we see that investors in this fund actually received a 2.45% gain from the date that my previous article was published. However, this is still not as good as the total return that the Alerian MLP Index delivered over the same period:

{kind=link}

This is quite discouraging, especially because the Tortoise fund is using leverage so it should be able to handily outperform the unleveraged index fund. As is the case with most energy infrastructure closed-end funds though, it fails to accomplish this task. There could be other reasons to consider this fund as opposed to the index though, which we will discuss over the remainder of this article.

About The Fund

According to the fund's website , Tortoise Energy Infrastructure has the primary objective of providing its investors with a very high level of total return. The fund explicitly states that it expects that the securities that are held in its portfolio will deliver the bulk of their total returns in the form of distributions, dividends, and other direct payments. This makes sense when we consider that this fund primarily invests in equity securities. According to CEF Connect, 98.69% of the fund's assets are invested in common equity securities alongside a small allocation to preferred equity securities:

CEF Connect

Common equity is by its very nature a total return investment vehicle. After all, investors purchase common equity securities because they want to earn a certain amount of income via the distributions and dividends that these securities pay out to their owners. In addition, investors are frequently seeking the capital appreciation that typically accompanies the growth and prosperity of the issuing company. The proportion of the total return that will be delivered in the form of capital appreciation as opposed to dividends depends on the individual company and the sector that the company is in. For example, the information technology sector tends to be far stingier about paying out dividends than utilities. In the case of energy infrastructure companies, or indeed any infrastructure company, growth rates tend to be fairly low and dividend yields are comparatively high. As such, we can see why this fund would expect that received dividends and distributions will account for a greater proportion of its total returns than capital gains will.

The website specifically describes the companies that this fund invests in:

Positioned to benefit from growing energy demand and accelerated efforts to reduce global CO2 emissions in energy production, TYG invests in energy infrastructure companies that generate, transport and distribute electricity, as well as process, store, distribute and market natural gas, natural gas liquids, refined products and crude oil.

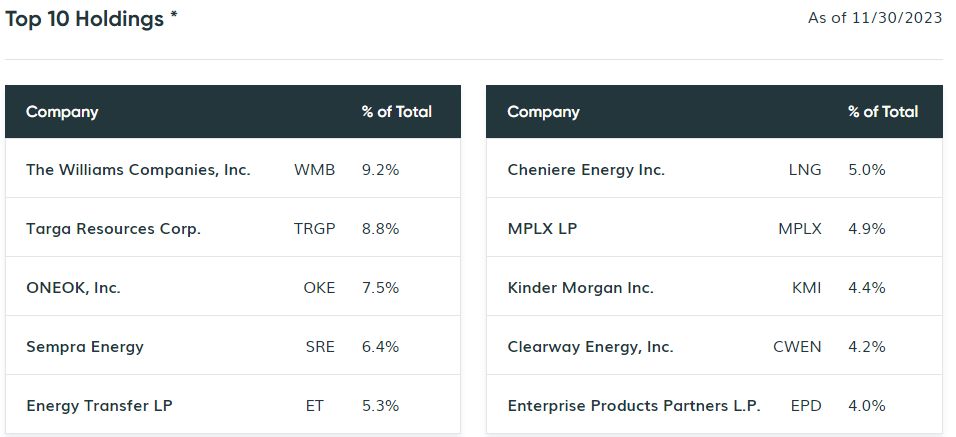

In other words, the fund will invest in primarily midstream companies and utilities. This is similar to many of the other energy infrastructure funds that we regularly discuss here at Energy Profits in Dividends. As regular readers are no doubt well aware, I have devoted a considerable amount of time and effort to discussing both midstream companies and utilities here and on the Seeking Alpha main site. As such, the largest holdings in this fund will likely be quite familiar to most regular readers. Here they are:

{kind=link}

I have discussed all of these companies numerous times over the years, with the notable exception of Clearway Energy (CWEN). Clearway Energy is a renewable energy producer that focuses on selling the electricity produced by its utility-grade power plants to its customers under long-term power purchase agreements. The company's website describes its operations:

Clearway Energy, Inc. is one of the largest renewable energy owners in the US with over 5,500 net megawatts of installed wind and solar generation projects. The company's over 8,000 net megawatts of assets also include approximately 2,500 net megawatts of environmentally-sound, highly efficient natural gas generation facilities. Through this environmentally-sound diversified and primarily contracted portfolio, Clearway Energy endeavors to provide its investors with stable and growing dividend income.

This description makes the company sound much like a yieldco like NextEra Energy Partners (NEP). Clearway Energy's 5.79% yield reinforces this conclusion as this is a much higher yield than most utilities offer, although it is not nearly as high as some of the best pipeline companies offer. This is still far different than many other renewable companies though, as its long-term contracts provide a relatively stable source of income and cash flow despite the unreliable nature of renewable energy generation.

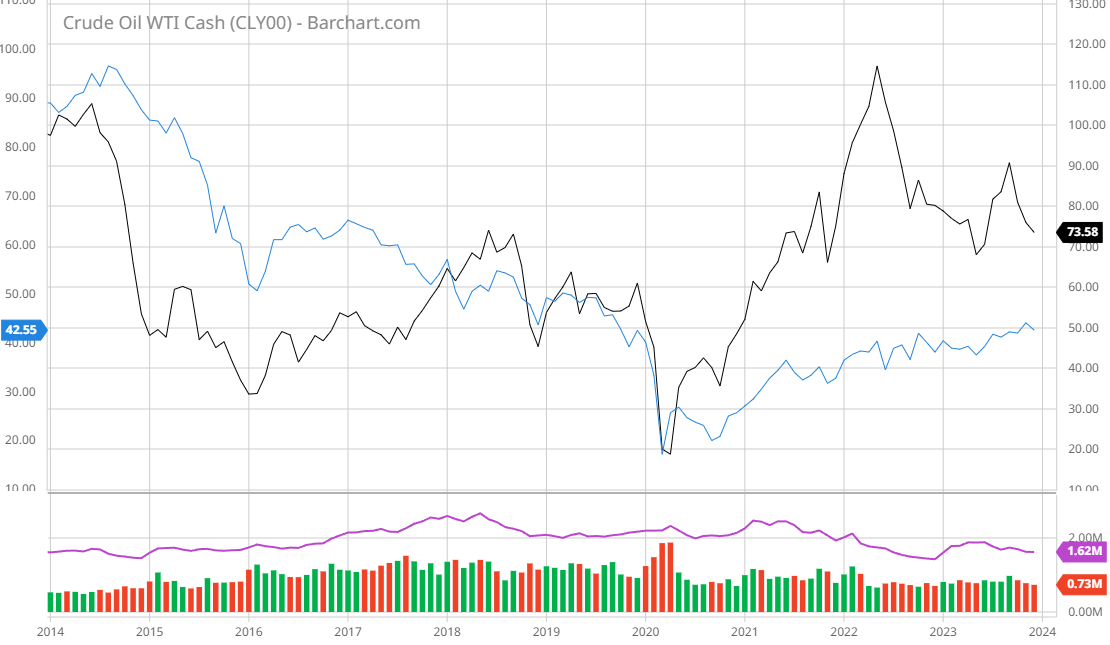

As we have discussed in numerous previous articles, midstream companies also tend to have very stable cash flows over time due to the long-term contractual nature of their business. The cash flows of these companies tend to not be affected much by macroeconomic events or changes in energy prices. However, midstream companies do experience some share and unit price correlations to crude oil prices. For example, this chart shows the spot price of West Texas Intermediate crude oil against the Alerian MLP Index over the past ten years:

{kind=link}

As we can clearly see, when the price of crude oil declines, midstream master limited partnerships typically see their unit prices decline. The reverse is also true, as rising crude oil prices correlate with rising prices of these companies. It is not a perfect correlation, but we can still see that energy prices will have a significant impact on the market performance of these companies.

There are seven companies on the fund's top ten holdings list that are midstream firms. An eighth company, Cheniere Energy (LNG), is not strictly speaking a midstream company but it can also be expected to exhibit a certain amount of correlation to energy prices. As such, we can expect that energy prices will have a significant impact on the performance of this fund.

We can see that this is even more true when we look at the entire portfolio instead of just the ten largest positions. As we can see here, 56% of the fund's assets are invested in natural gas-focused midstream companies and another 7% of its assets are invested in liquids-focused midstream companies:

{kind=link}

That means that fully 63% of the company's assets are invested in companies with some connection to the traditional oil and gas space. As such, we can expect that the fund's share price and overall portfolio performance will at least somewhat correlate with energy prices. This is something that could be important next year, as it is uncertain where energy prices will go.

For the most part, if the economy manages to avoid a recession, energy prices should go up in 2024. This is the so-called "soft landing" scenario. This is because the balance between supply and demand of crude oil is currently very tight and if the global economy remains strong then there is no reason to expect that the consumption of crude oil will decline. In a recession, energy consumption typically declines so this should alleviate some of the supply tightness and push prices down.

Another factor to consider is that a reduction in interest rates could have the effect of pulling the U.S. dollar down. That will apply upward pressure on crude oil prices, along with just about every other real asset.

It is therefore uncertain which direction energy prices will go next year. The companies in the fund should not see their cash flows affected either way, but the market price of their securities will certainly be affected either positively or negatively. That could still have an impact on your decision regarding an investment in this fund.

Leverage

As is the case with most closed-end funds, Tortoise Energy Infrastructure employs leverage as a method of boosting its effective yield and total returns. I explained how this works in my previous article on this fund:

In short, the fund is borrowing money and using that borrowed money to purchase common equities of midstream and renewable companies. As long as the purchased assets deliver a higher total return than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case. However, it is important to note that this strategy is not as effective today with interest rates at 6% as it was two years ago when rates were at 0%.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. Thus, we want to ensure that the fund is not using too much leverage since that would expose us to too much risk. I generally do not like to see a fund's leverage exceed a third as a percentage of assets for that reason.

As of the time of writing, Tortoise Energy Infrastructure has leveraged assets comprising 22.38% of its portfolio. This is quite a bit better than the 23.11% of assets that the fund had the last time that we discussed it. This is caused by the fact that the fund's net asset value has increased by a whopping 10.32% since the last time that we discussed it:

{kind=link}

This is very surprising considering the fund's mediocre share price performance over the same time period, and it could suggest that the fund has become substantially undervalued over the past few months. We will discuss this later in this article.

For right now, the important thing is that this increase in the fund's net asset value has decreased its overall leverage. That makes a great deal of sense, as the portfolio is now larger than it was back in early October. If the fund's outstanding leverage remained the same, then it would represent a smaller percentage of the portfolio today.

The current leverage is lower than the leverage of many other closed-end funds. It should represent a fairly reasonable balance between the risk and reward. As such, we should not need to worry too much about the fund's leverage right now.

Distribution Analysis

As mentioned earlier in this article, the primary objective of Tortoise Energy Infrastructure is to provide its investors with a very high level of total return. In pursuance of this objective, the fund invests in a combination of midstream companies and renewable energy firms. Midstream companies deliver the majority of their total returns in the form of direct payments to the shareholders, and many of them have very high yields right now. Renewable companies may or may not boast high yields, although some yieldcos certainly do. The fund collects all of the payments that it receives from the assets in its portfolio. It combines this money with any capital gains that it manages to realize through the sale of appreciated common equities. The fund then pays out all of this money to the shareholders, net of its own expenses.

This business model has resulted in the shares of this fund having a very high yield. Tortoise Energy Infrastructure pays a quarterly distribution of $0.71 per share ($2.84 per share annually), which gives the fund a 9.92% yield at the current price. As mentioned in the introduction, this is higher than the yield currently possessed by many other energy infrastructure funds. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years. As we can see here, the fund managed to do reasonably well until the COVID-19 lockdowns, but then it had to slash its distribution and it remains much lower than it had prior to the pandemic:

{kind=link}

This poor performance history will almost certainly prove to be a turn-off for any investor who is seeking to earn a safe and consistent income from the assets in their portfolios. The distribution does appear to have stabilized somewhat though, and the fund did increase it rapidly following the cuts. The fund's distribution history is still much worse than that of funds such as the Neuberger Berman Energy Infrastructure and Income Fund, though. Thus, nobody could be blamed for being concerned about the safety of the distribution.

As I have pointed out numerous times in past articles though, the fund's distribution history is not necessarily the most important thing for anyone who is considering purchasing the shares today. This is because today's buyer will receive the current distribution at the current yield and will not be affected by the actions that the fund had to take in the past. The most important thing for today's investors is how well it can sustain the current distribution. Let us investigate this.

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on May 31, 2023. As such, this report will provide no insight into the fund's performance over the past seven months. This is disappointing because we have no information about how the fund handled the volatility that existed during the intervening period. After all, we saw both a bear market run over the summer and a bull market that started in the middle of October. These could both have presented opportunities and challenges for the fund, and we have no insight into how well it handled either situation. It will probably be another month or so until the fund releases its annual report, so unfortunately, we have to go with the information that we have available to us for the time being.

During the six-month period, Tortoise Energy Infrastructure received $13,235,185 in dividends and distributions along with $261,997 in interest from the assets in its portfolio. However, some of this money came from master limited partnerships and so is not considered to be investment income for tax or accounting purposes. As such, the fund only reported a total investment income of $8,511,566 during the period. The fund paid its expenses out of this amount, which left it with $2,275,338 available for shareholders. That was, unfortunately, nowhere near enough to cover the distributions that the fund paid out over the period. The fund's distributions during the period totaled $16,090,742, which was obviously substantially more than the net investment income. At first glance, this might be concerning as the fund clearly did not have sufficient investment income after expenses to afford the payout that it made.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distribution. For example, it might have been able to realize some capital gains by selling securities when the market goes up. It also received some money from master limited partnerships that is not considered to be investment income for tax or accounting purposes, but obviously represents money coming into the fund that can be distributed to the shareholders. The fund had mixed results in this area during the period. It reported net realized gains of $22,361,867 but this was offset by $74,841,900 net unrealized losses during the period. Overall, the fund's net assets declined by $66,295,437 after accounting for all inflows and outflows during the period.

Generally speaking, if the fund had sufficient net realized gains and net investment income to cover the distribution then we do not have to worry. As we can see, that was the case with this fund during the most recent reporting period for which we have current results. While the fund's net assets did decline once we consider its unrealized losses, unrealized losses can easily be erased when the market turns so these are not necessarily a big deal.

Of course, the most recent report was for a time period that ended seven months ago, and a lot of things have happened since that time. Fortunately, it does not appear that the fund has been having problems carrying its distribution. As we can see here, its net asset value per share is up 4.72% since June 1, 2023:

{kind=link}

This strongly suggests that the fund has managed to fully cover all of the distributions that it has paid out since the ending date of the most recent financial report. As such, we should not need to worry about a distribution cut right now. The fund's distribution appears to be sustainable right now.

Valuation

As of December 22, 2023 (the most recent date for which data is available as of the time of writing), Tortoise Energy Infrastructure has a net asset value of $35.49 per share but the shares only trade for $29.00 each. This gives the fund's shares a whopping 18.29% discount on net asset value at the current price. This is admittedly not as good as the 20.44% discount that the shares have had on average over the past month, but realistically a double-digit discount is almost always representative of a good entry price for a fund. As such, the current price appears to be quite reasonable if you wish to add this fund to your portfolio today.

Conclusion

In conclusion, Tortoise Energy Infrastructure provides a way for investors to add a diversified portfolio of pipeline operators and renewable energy producers to their portfolios. The fund's shares have substantially underperformed the actual portfolio in the market recently and this has provided investors with a very good entry point. Tortoise Energy Infrastructure Corporation is admittedly not the most popular name among investors due to the poor performance of some of its funds around the time of the pandemic, but this fund does look okay right now. The incredibly large discount might be enough to prompt some investors to give it a chance.

For further details see:

TYG: Shares Underperforming Portfolio Could Present An Opportunity