TYL - Tyler Technologies: Earnings Beat Supported By Strong Demand

2023-08-02 16:06:58 ET

Summary

- Tyler Technologies reported strong Q2 earnings, beating revenue and EPS expectations.

- The company's 2030 vision is off to a great start.

- Guidance for 2023 was slightly adjusted, with a decrease in revenue projection but an improvement in EPS guidance.

Introduction

Last Month I initiated my coverage of Tyler Technologies ( TYL ). The company reported second quarter earnings last week. In this Analysis, I will take a deep dive into the recent earnings and explain my thesis in small detail.

Reaffirming The Investment Thesis

TYL is a market leader , delivering mission critical software to the public sector. The firm announced its 2030 vision back in June 2023, which includes increasing recurring revenue to 90% by migrating customers to its SaaS model. The other part of the plan is to enhance margins (30%+ operating margins and 20% FCF margin) by completing the shift towards the Cloud-First.

As I said in my last analysis I think the firm's plan is achievable because TYL's customers seem to love the new SaaS model (subscriptions revenue has increased from $220.5 million in 2018 to $1.0 billion in 2022). An increase in recurring revenue will make TYL's business more stable.

As for margin enhancement, The company plans on doing that by moving to the cloud. I believe that a shift to the cloud will improve the firm's margins because it limits IT expenditures. It eliminates the need to invest in hardware and software. Instead, they can just use a third party to host their cloud such as AWS.

TYL's market is growing and its customers (local governments) have difficulties attracting and retaining staff to support their IT functions. So, they establish long-term relationships with reliable providers that can offer them those services, such as Tyler. TYL's market is very fragmented and the firm has done a good job at capturing as many sectors as it can.

Q2 Earnings

{kind=link}

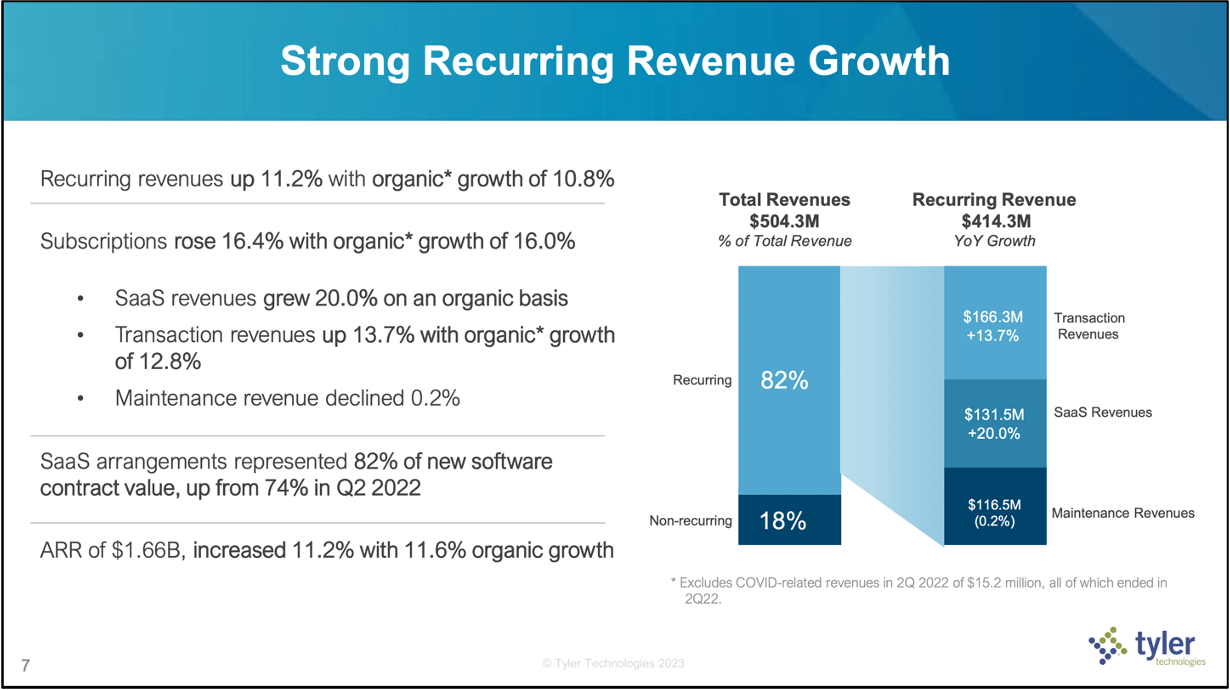

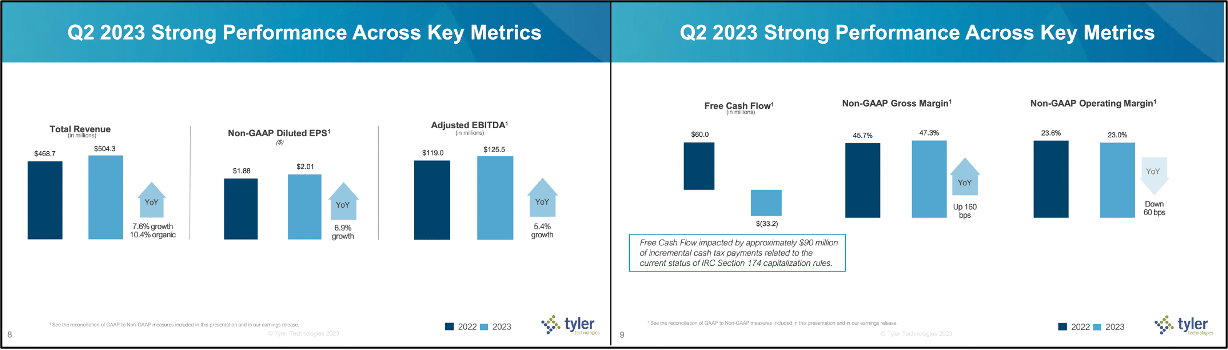

TYL had a good second quarter beating on both revenue and EPS. The company reported revenue of $504.3 million beating Factset's estimate by 3%, and an EPS of $2.01 beating the expectation of $1.89. The firm surpassed $500 million in total quarter revenue for the first time. Recurring revenue was up by 20% year over year. TYL also pointed out that they are still the #1 market leader.

{kind=link}

Operating margins saw a decline of 60 bps YoY and ADJ EBITDA of 50 bps. These margin compressions were expected as more customers transition to SaaS, which will have a negative impact on margins in the short term. As for the cloud first transition, the company said it is executing strongly against its strategy.

In the Q2-23 earnings call, Management stated that demand is stable and is at or above pre-COVID highs. As long as demand stays high or stable, revenue is set to increase. This is what was said by the CFO in the call:

Yes, the demand environment, as we said in the prepared remarks, is stable or growing generally at or above kind of our pre-COVID highs. So a very robust demand environment coming out of Investor Day and really very similar to what we’ve seen throughout this year and don’t see signs of that changing right now. So stable at a high level.

All in all, I believe TYL had a good quarter, beating heavily on EPS despite the accelerated shift towards the SaaS model. Considering the robust and growing demand, I don't think the firm will have much of a problem in the third quarter.

Guidance

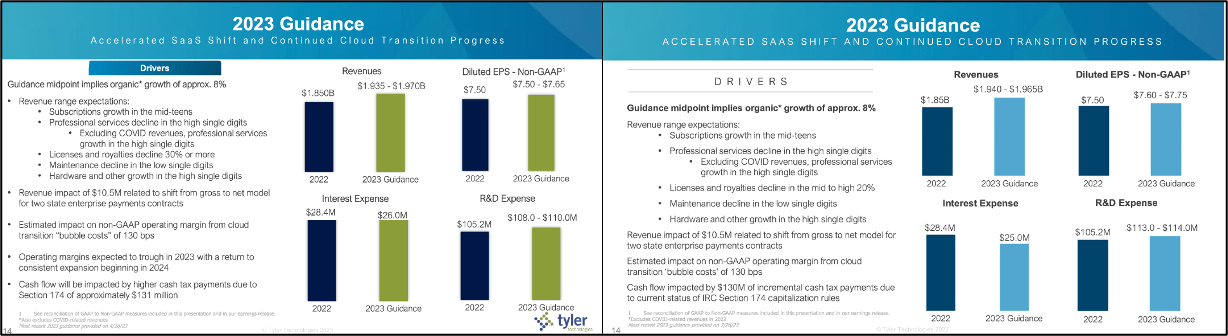

{kind=link}

TYL has altered its 2023 guidance a little bit. The slide on the left is from Q1 23 , and the one on the right is from Q2 23. The company cut its revenue projection for 2023 from $1.935–1.970 billion to $1.90–1.965 billion. Not a very big change in my opinion. TYL did improve its EPS guidance from $7.50–$7.65 to $7.60–$7.75, With interest expense decreasing by $1 million from Q1-23 to Q2-23. TYL's is expecting to spend $113–$114 million on R&D in 2023.

Overall, the changes made by the firm to its 2023 outlook aren't that major in my opinion because the only negative thing about them is the revenue revision. Aside from that, the bump in EPS is mainly attributed to the drop in interest expense. This guidance might be revised again down the line.

Valuation

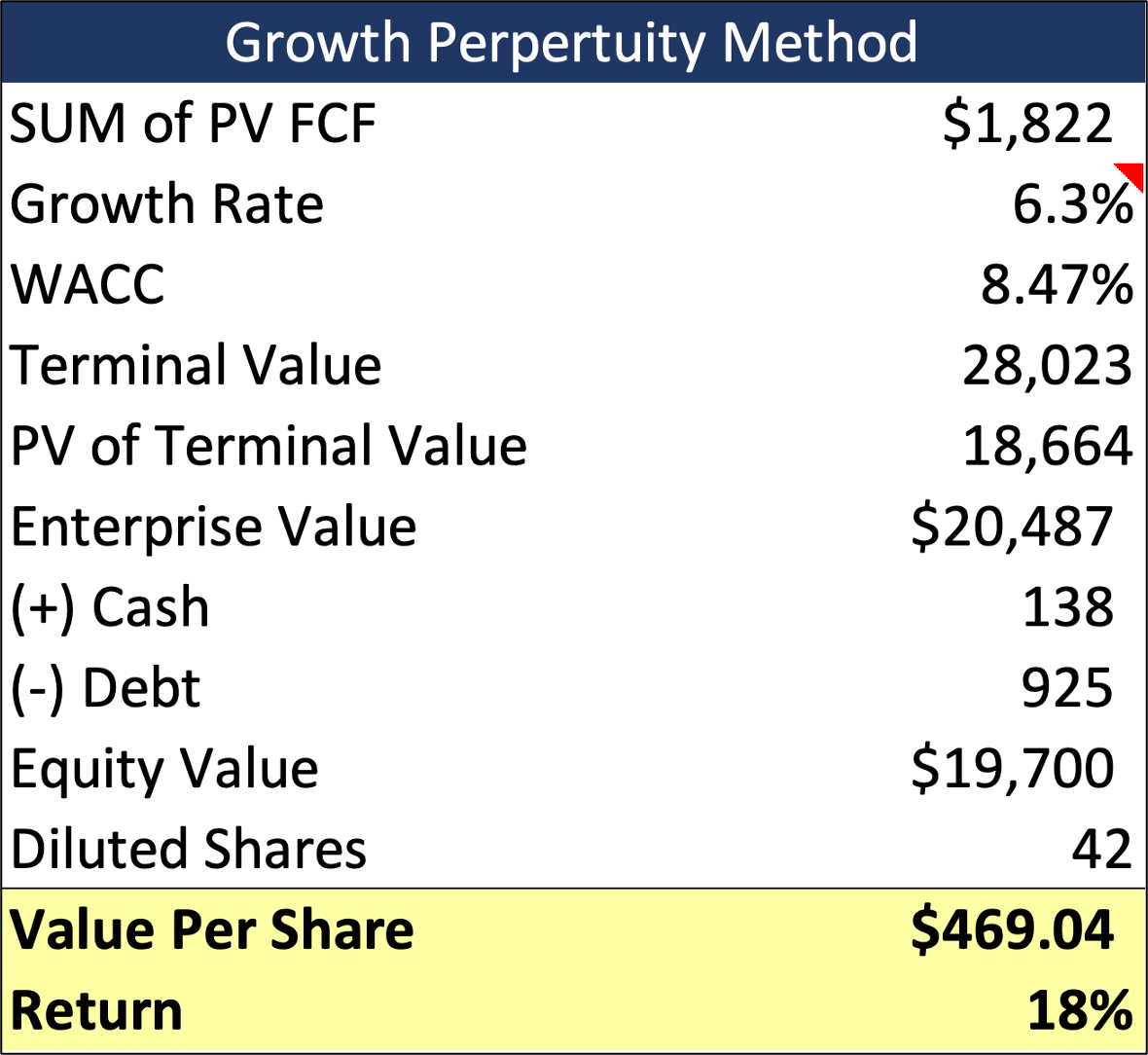

My valuation of TYL remains unchanged. My fair value is $469 which equates to an 18% upside from the current price. As I expected the company migrated more customers to subscriptions and added new ones. My revenue assumption is still the same I expect revenue to compound at an annual growth rate of 8.09% from 2023 to 2027, with both license and maintenance revenue experiencing declines every year as the shift towards SaaS continues.

The main revenue drivers in my model remain unchanged: market growth and increased customer spending. The firm can also leverage its large customer base (TYL has 13,000 client locations and 40,000 client installations) to attract new ones. On average, every customer uses at least three TYL products.

The consensus for Q3 23 revenue is $496.77 million, and EPS is $1.99. My revenue estimate is $497 million, with an EBITDA of $117 million.

{kind=link}

I will stand by my HOLD rating, not because there is something wrong with the business but because an 18% upside doesn't seem that attractive to me. TYL has 42 million shares outstanding, cash of $137.9 million, debt of $924.9 million, a share price of $398, and an enterprise value of $17.5 billion.

Conclusion

The bottom line is that TYL had a good quarter in my opinion, beating expectations. What really impressed me was that the company beat EPS by $0.12 despite the accelerating shift towards SaaS. Historically, As companies shift toward the SaaS model their profitability takes a hit until they build scale. Customers seem to love the SaaS business model, and the demand environment seems stable, which is good for the company's revenue. TYL made some tweaks to its 2023 guidance but nothing major. I assign a hold because my valuation indicates an 18% upside which isn't very attractive to me, but that might change if the price drops and nothing bad happens to the business.

For further details see:

Tyler Technologies: Earnings Beat Supported By Strong Demand