TYL - Tyler Technologies: High-Quality Business But Massively Overvalued

2023-11-14 22:51:31 ET

Summary

- Tyler Technologies is a high-quality business, which I see from the pace of revenue growth and wide profitability metrics.

- I like the management's prudent capital allocation and commitment to innovation.

- My valuation analysis suggests that massive optimism is already priced in, as TYL stock is about 40% overvalued.

Investment thesis

Tyler Technologies ( TYL ) is a superstar in the domain of professional services to the public sector. The company's revenue compounded at a staggering 18% CAGR over the last decade, but profitability stagnated. To address this issue, the management started conducting a big strategic shift towards a SaaS model and cloud-based solutions, which aligns with the evolving technological landscape. The fact that recurring revenue already represents more than 83% of the company's total revenue is a solid bullish sign, meaning that the management's execution of the transition is going well. I also like the firm commitment to innovation and financial position improvement, but my valuation analysis suggests that the vast optimism is already priced in. According to my calculations, the stock is about 40% overvalued, and I do not recommend paying such a massive premium even despite the company's stellar performance. All in all, I assign TYL a "Hold" rating.

Company information

Tyler Technologies is a leading provider of integrated information management solutions to the public sector, offering software applications based on software-as-a-service [SaaS] and on-premise options.

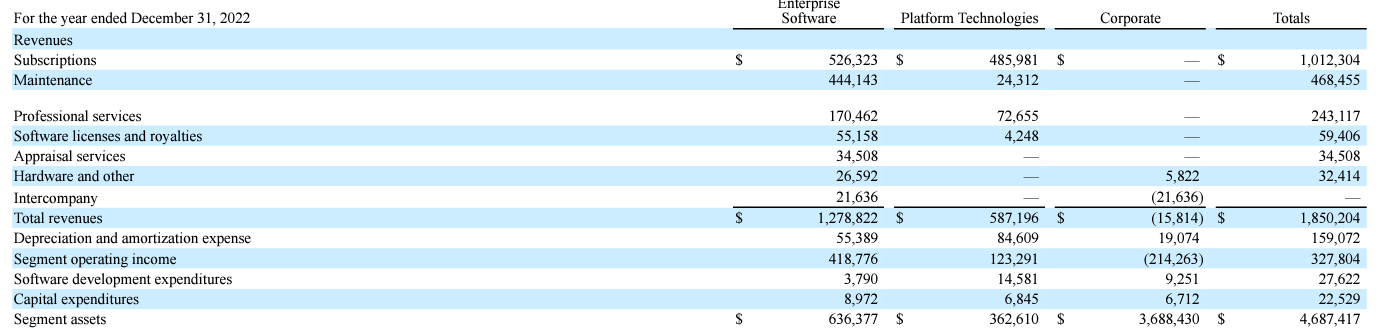

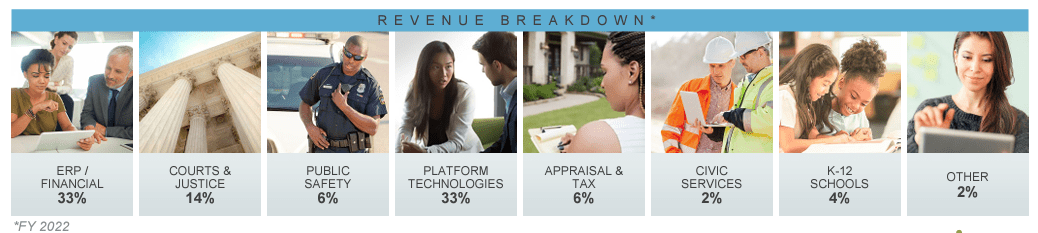

The company's fiscal year ends on December 31. The business is operated via two segments: Enterprise Software [ES] and Platform Technologies [PT]. According to the latest 10-K report , the ES segment represented 69% of the total revenue in FY 2022.

{kind=link}

Financials

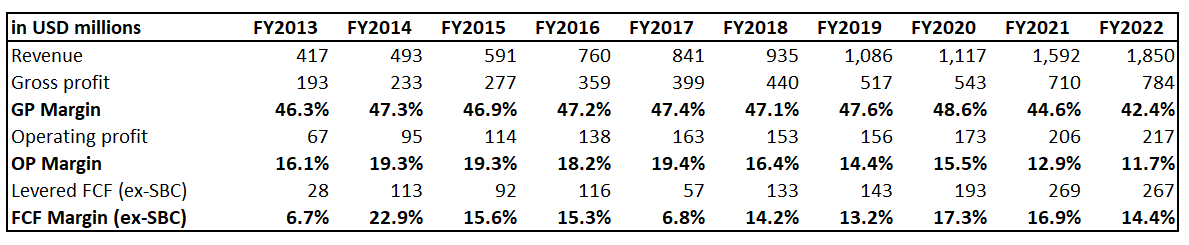

I have mixed feelings about the company's financial performance over the past decade. On the one hand, revenue compounded by an impressive 18% annually. On the other hand, the gross and operating margins declined despite stellar revenue growth. The inability to expand profitability metrics is a warning sign to me since it might suggest a lack of pricing power or cost management issues, which are both red flags for investors.

{kind=link}

Despite profitability decline, TYL's free cash flow [FCF] margin ex-stock-based compensation [ex-SBC] is still stellar. It enables the company to maintain a strong financial position with low leverage and healthy short-term liquidity metrics. Despite a solid FCF margin, the company does not pay dividends to shareholders, and stock buybacks cannot be called substantial.

Seeking Alpha

The latest quarterly earnings were released on November 1, when the company slightly missed revenue consensus estimates but outnumbered the bottom-line expectations. Revenue grew by 4.5% YoY, and the adjusted EPS also slightly expanded from $2.06 to $2.14.

Seeking Alpha

The gross margin expanded YoY by more than two percentage points, but this effect was almost fully offset by the increased SG&A expenses. As a result, the operating margin remained almost flat YoY with a slight five basis points expansion. From the latest earnings release, I see several bullish signs. For example, the revenue mix improved, and recurring revenue now represents more than 83% of the total sales, which improves earnings stability and predictability. SaaS revenue grew by more than 20% for the eleventh straight quarter, which indicates a massive demand for the company's subscription offerings.

TYL's latest earnings presentation

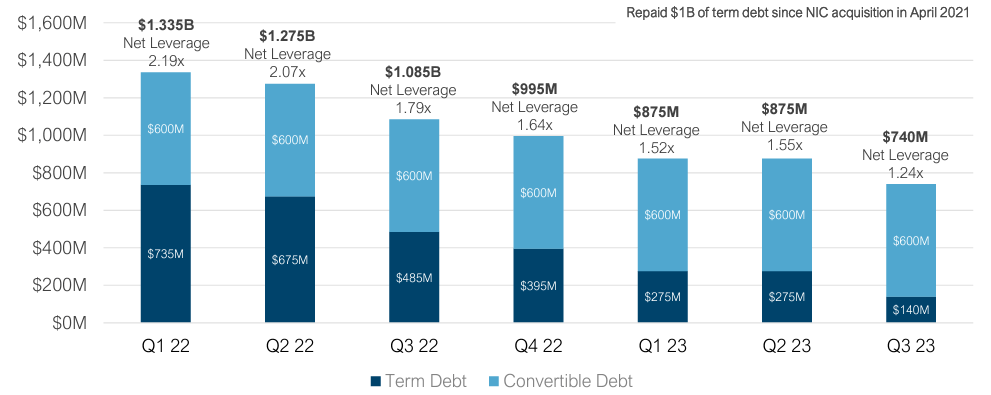

Another solid bullish sign is the pace of the balance sheet improvement. The management targets aggressive leverage decrease as the net leverage ratio has almost halved over less than two years. Such a rapid, substantial improvement of the financial position indicates effective financial management and contributes to the overall company's resilience and capacity to finance future strategic initiatives. Prioritizing the improvement of the financial position also highlights the management's financially disciplined approach, increasing the chances that the company can sustain its growth profile and stellar profitability .

{kind=link}

The earnings release for the upcoming quarter is scheduled for February 7. Consensus estimates expect revenue at $485 million, which means an 8% YoY growth. The adjusted EPS is expected to follow the top line and expand from $1.66 to $1.86.

Seeking Alpha

TYL operates in a highly competitive environment, marked by many players varying in size and scope. The competition extends to consulting firms, publicly held companies, and privately held smaller entities. While I have underlined the declining profitability at the beginning of my analysis, I like the management's vision to shift the mix more to the SaaS model as it provides greater predictability of future cash flows. The company's transition to the cloud is a sound decision that aligns with the evolving technological landscape. While any strategic transition is risky, I believe that shifts related to innovations are inevitable if companies want to stay in business for longer. As the company's SaaS revenue streams have grown to double digits for eleven straight quarters, it strongly indicates that the transition execution is being executed well.

The company's stellar revenue growth suggests that the company focuses on customer satisfaction and building long-lasting relationships with clients. The company's large scale and long history of success means the company is able to leverage deep expertise across different domains in government operations. The ability to cover various clients' needs provides TYL with better cross-selling opportunities and gives it a reputation as a solid "one-stop shop," which always helps build stronger bonds with clients.

{kind=link}

I like the management's ability to recognize changing trends and flexibility, which allows us to innovate. The company regularly upgrades core software applications, introduces new features, and expands its set of offerings both through internal development and with the help of strategic acquisitions. A firm commitment to innovation enhances the market appeal of the company's products, which means that a strong revenue growth profile will likely be sustained for longer.

Valuation

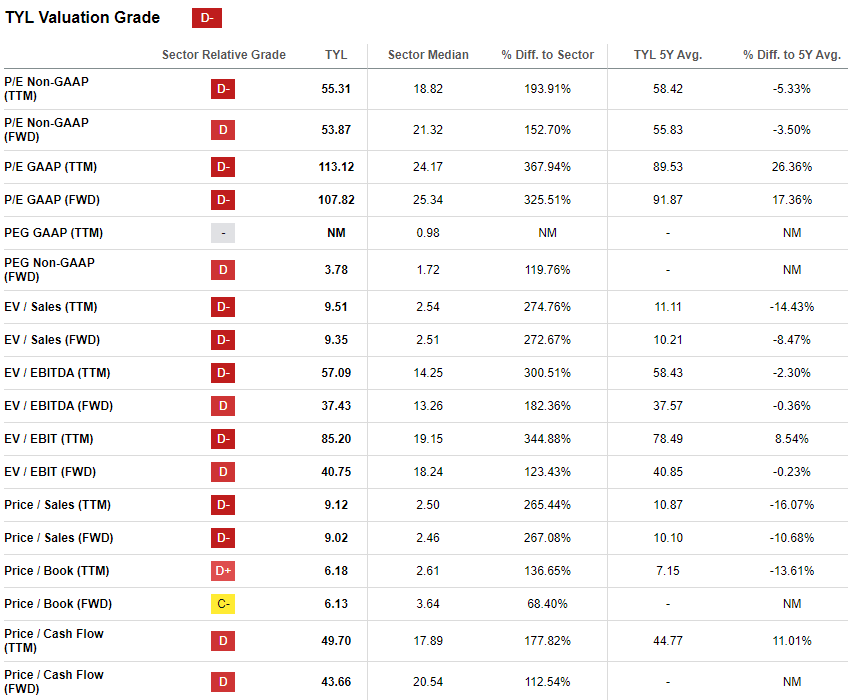

The stock rallied by 31% year-to-date, substantially outperforming the broader U.S. market. Seeking Alpha Quant assigns the stock with a low "D-" valuation grade because valuation ratios are multiple times higher than the sector median across the board. However, given the company's dominating position in its niche, I would prefer to look at the comparison to historical averages better. Current multiples are in line with the last five years' averages, which indicates fair valuation.

{kind=link}

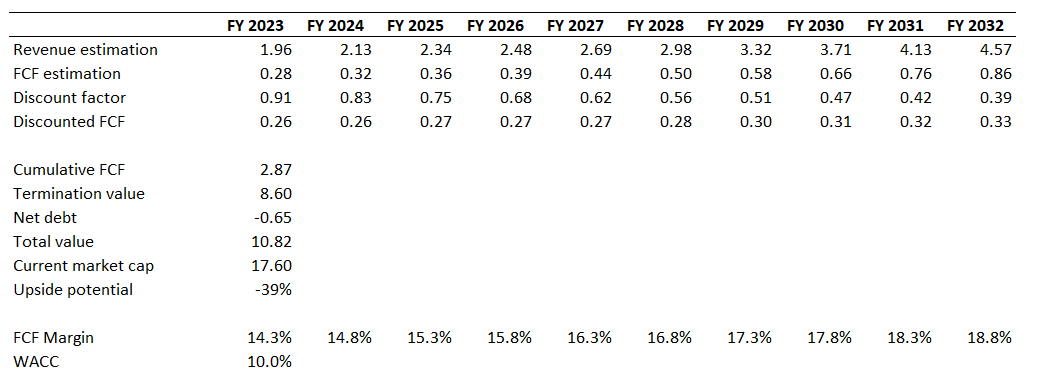

I want to proceed with my valuation analysis with the discounted cash flow [DCF] simulation. I use a 10% WACC for discounting. Revenue consensus estimates project a 10% CAGR for the next decade, which I consider fair enough to incorporate into my fair value calculations. I use a 14.3% TTM FCF ex-SBC margin for my base year and expect a 50 basis points yearly expansion.

{kind=link}

According to my DCF simulation, the business's fair value is below $11 billion. That signals almost a 40% downside potential for the stock. I recognize TYL's unique positioning and strong business presence in the public sector, but I still do not see reasons for investors to pay such a massive premium for the stock. That said, my fair price for TYL is about $250.

Risks to my cautious thesis

Many of TYL's potential clients purchase products and services through an open bidding process. That said, the pipeline of new projects might be relatively unpredictable. While this is a risk for business, it can only play as a positive catalyst for the stock price in case the company unexpectedly wins a big contract. Such success is likely to enhance investor confidence in Tyler's ability to secure lucrative contracts, leading to a favorable revision of earnings estimates.

Another risk to consider for my cautious thesis is the current strong momentum for TYL. Positive market sentiment and investor enthusiasm could continue driving the share price growth. Strong momentum can persist until a significant event, such as an earnings miss or negative hot headlines, emerges, which will highly likely disrupt the momentum. That said, there is a substantial level of uncertainty regarding how long the bull run can last.

Bottom line

To conclude, TYL is a "Hold". Multiple bullish signs indicate that Tyler Technologies is a high-quality, well-executed business. However, the stock is substantially overvalued, and I do not recommend buying the stock with a massive premium that is higher than its fair value.

For further details see:

Tyler Technologies: High-Quality Business But Massively Overvalued