TYL - Tyler Technologies: High-Quality IT Service Provider For Public Sector

2024-01-10 11:23:42 ET

Summary

- Tyler Technologies has strong organic growth and a niche business in providing IT services to the U.S. public sector.

- The company's subscription and maintenance segments contribute to recurring revenue and higher valuation.

- The relatively recent acquisition of NIC expands Tyler's offerings in the government sector, but increased debt leverage is a concern.

Tyler Technologies ( TYL ) is a niche IT service provider for the U.S. public sector, and its revenue has been growing at a high-single-digit organically with comprehensive product solutions. The NIC acquisition is complementary to their existing business. However, the stock price is extremely overvalued, and I am initiating a 'Sell' recommendation with a fair value of $250 per share.

Strong Organic Growth and Niche Business

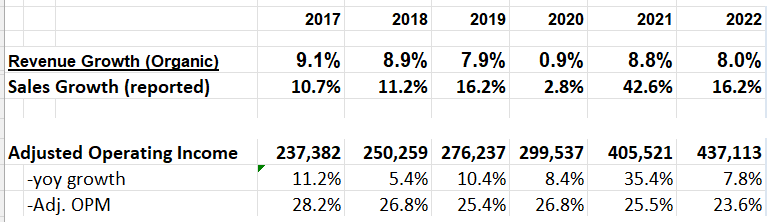

Tyler has delivered solid organic revenue growth in the past few years, boasting a high-single-digit growth rate. Their adjusted operating margin has consistently remained above 23%. Notably, the company has substantially increased its subscription and maintenance business in recent years, with the revenue percentage rising from 63% in FY17 to 80% in FY22.

{kind=link}

The growth of the subscription and maintenance segments is crucial for Tyler's business for several reasons. Firstly, these businesses exhibit a recurring nature, enhancing overall business visibility. The more recurring their revenue, the higher valuation the market tends to assign to the stock, in my view. This factor contributes to the premium stock price they have attained.

Secondly, Tyler's strategic shift from traditional software arrangements to the SaaS model is pivotal for margin expansion and organic growth. Unlike the traditional approach where the sales force might need to encourage customers to upgrade on-premise platforms for new revenue, the SaaS model allows customers to pay on a monthly or annual basis, with automatic inclusion of all upgrades in the offering.

Lastly, these subscription services align with customers' cloud transition strategies. If Tyler's platform fails to support cloud infrastructure, there is a risk of gradually losing these customers over time. This underscores the importance of staying aligned with evolving industry trends and customer preferences.

Healthy Public Sector Market

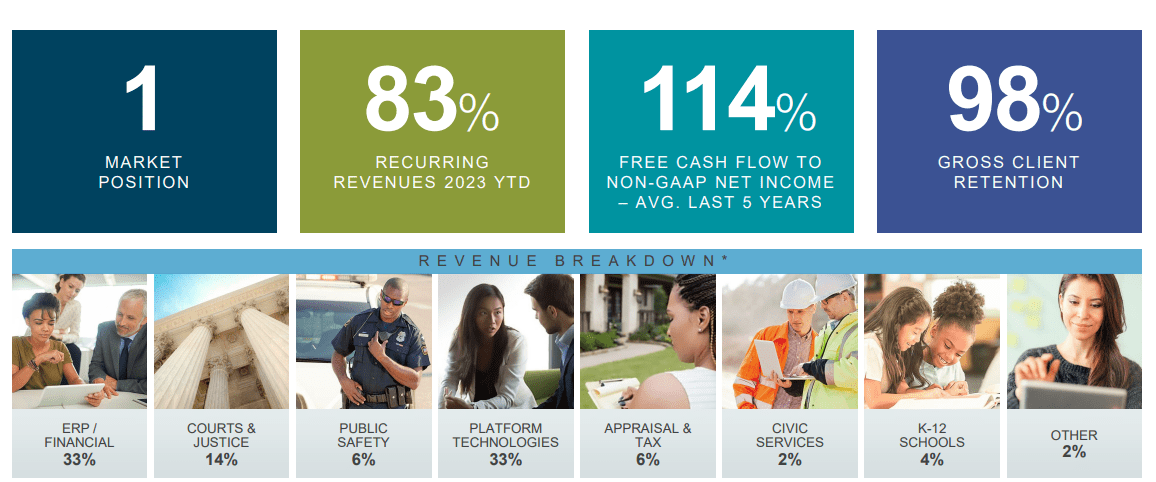

Compared to the private sector, the public sector market is generally more stable, with the main variable being the tax revenue collected by the government. Tyler stands out as a clear leader in providing software solutions to the public sector. Their comprehensive range of solutions spans ERP, courts and justice, public safety, appraisals, civic services, and more. This diversification within the public sector positions Tyler as a key player across various government functions, contributing to the stability of its market presence.

{kind=link}

These niche markets shield the company from intense competition for several reasons. The total addressable market is relatively small, with Tyler's total revenue being less than $2 billion despite its leadership position. The limited market size reduces interest from larger tech companies. Furthermore, commercializing IT solutions designed for local governments into the private sector is nearly impossible due to the highly customized and dedicated nature of most IT systems for local governments. This customization presents a significant challenge for other software companies looking to extend their solutions from the private to the public sector.

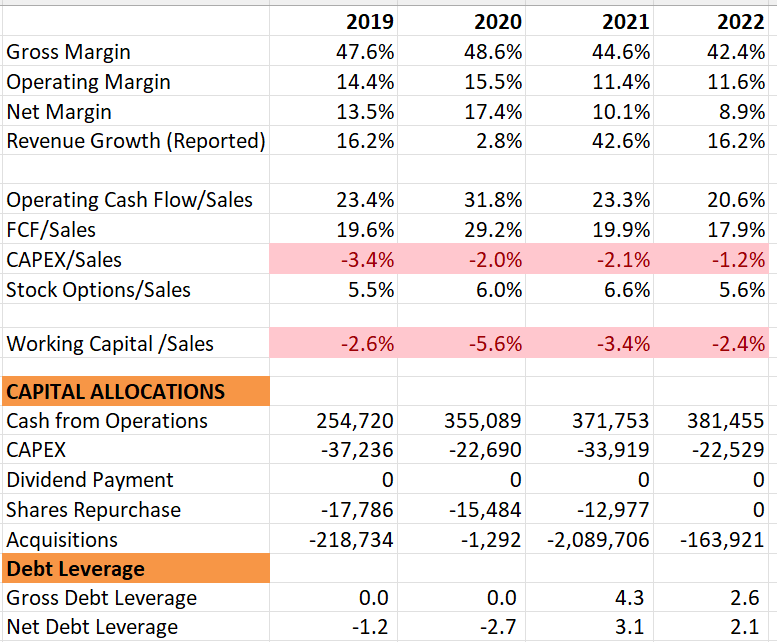

Due to the limited competition, Tyler enjoys healthy margin and free cash flow profiles. Historically, their free cash flow conversion has been close to 20%, and they operate on an asset-light business model, with a capex ratio of less than 2%. The majority of cash generated from operations is typically allocated to share repurchases and acquisitions, which is a common practice for software companies.

{kind=link}

Acquisition of NIC

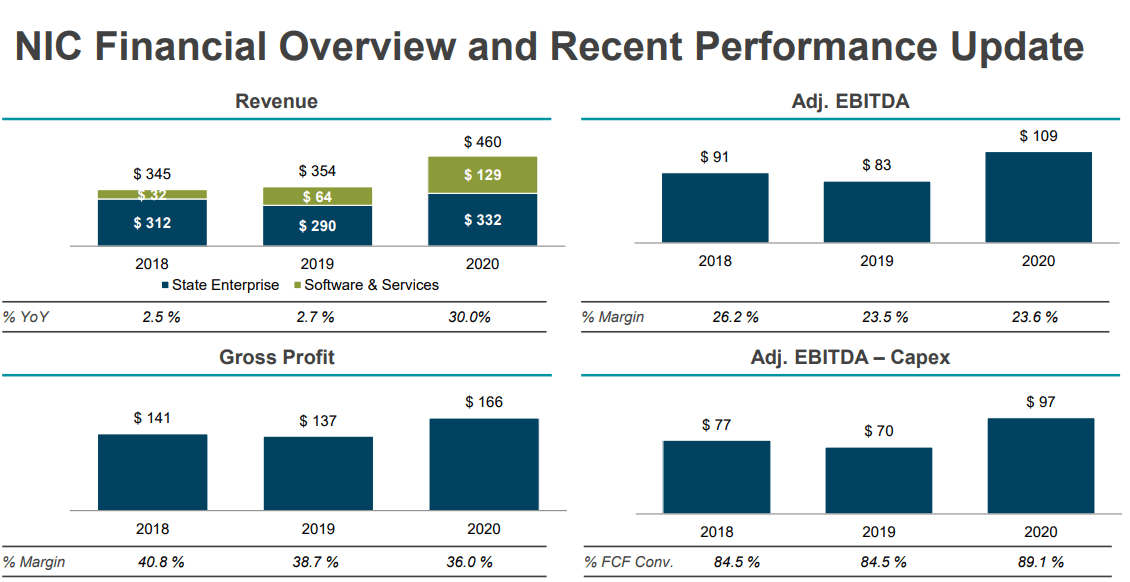

Tyler Technologies acquired NIC for $2.3 billion in 2021. NIC specializes in providing payments technology and online portals to government agencies and municipalities, catering to over 7,100 federal, state, and local government entities in the U.S.

This acquisition marks the largest in Tyler's history, and it's worth noting that the deal price was substantial, representing a 19x EV/EBITDA multiple. Despite the elevated cost, the acquisition strategically expands Tyler's offerings in the government sector.

However, it's essential to acknowledge that the deal increased Tyler's debt leverage on their balance sheet. The gross debt leverage rose to 2.6x in FY22, reflecting the financial impact of this significant acquisition.

{kind=link}

On the positive side, NIC is highly complementary to Tyler's existing products and solutions, with both companies servicing the public sector. The combination of Tyler and NIC can connect public communities within a seamless infrastructure. Their solutions are achieving great synergies across business solutions, taxes, court/police, and public health care sectors.

Recent Results and FY24 Preview

During Q3 FY23 , they experienced a 6% organic growth in revenue, and the adjusted operating profit increased by 4% year over year. More significantly, recurring revenues from maintenance and subscriptions showed an 11% year-over-year improvement, and the annualized recurring revenue increased by 11% year over year. Free cash flow amounted to $162.7 million, marking a notable 40.7% year-over-year increase.

{kind=link}

For the FY23 guidance, they anticipate 7.5% organic revenue growth at the mid-point, with reported diluted EPS expected to range between $3.82 and $3.96. The cash flow forecast for the full year falls within the range of $220 million to $240 million. Anticipating no surprises in their Q4 FY23 results, given their consistent solid growth in the past three quarters and the high ratio of recurring revenue providing good visibility for the near term.

Looking ahead to FY24, I expect another year of high-single-digit revenue growth and notable margin expansion. Firstly, significant license deals that slipped into 2024, as mentioned in the earnings call, are expected to contribute additional growth for FY24.

Secondly, Tyler is poised to further benefit from the acquisition of NIC as they integrate digital payment solutions into their existing software platforms. This consolidation is anticipated to generate substantial revenue synergies.

Lastly, the ongoing transition from license sales to cloud subscriptions prompts the closure of data centers, one in FY24 and another in FY25. This move is expected to reduce operating expenses and maintenance capex spending, positively impacting margin and free cash flow generation.

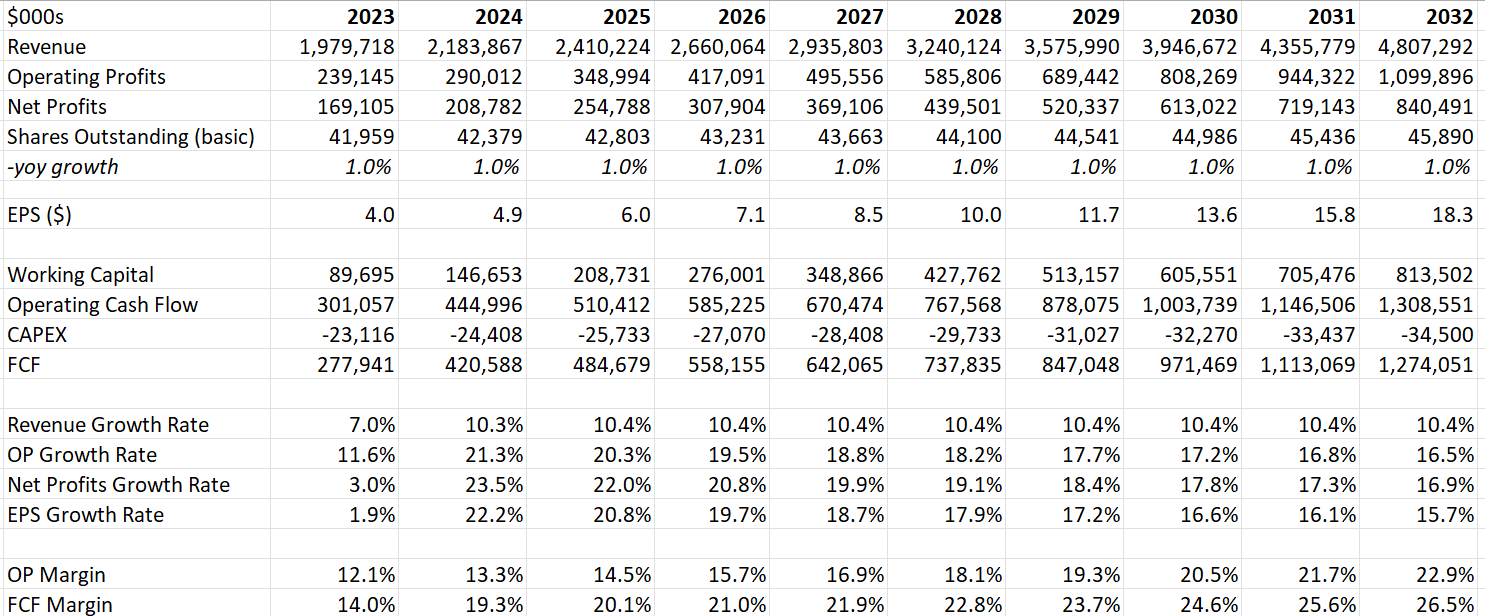

Valuation

The assumptions for FY23 align with their formal guidance. For normalized growth, I assume 8.6% of organic revenue growth and 1.7% of acquisition growth. These assumptions are consistent with their historical averages. I believe their unique value proposition and leadership position in the public sector will contribute to maintaining outstanding growth in the near future. On the margin side, I anticipate a meaningful expansion over time, driven by the closure of their own data centers and the full integration of NIC's business unit.

{kind=link}

The model utilizes a 10% discount rate, 5% terminal growth rate, and a 22% tax rate. According to these parameters, the fair value is estimated to be $250 per share in my model.

Key Risks

Stock Options Diluting Their Shares Outstanding : Their diluted shares outstanding increased by 3.5% in FY20, 1.7% in FY21, and 0.4% in FY22, indicating that their share repurchases couldn't fully offset the impact of stock options issuance. Due to their most recent acquisition, they suspended their share repurchase program in FY22. It's not anticipated that there will be any shares repurchased until they deleverage their debts.

Hardware Business : They are selling hardware products to the public sector as part of the IT integration. This hardware segment represented 1.8% of the total revenue in FY22, and the hardware business is known for being a low-margin venture. Given the relatively small contribution to the overall revenue, I don't have significant concerns about this aspect.

Conclusion

Although Tyler is recognized as a high-quality and niche growth stock in the U.S. market, the stock price is deemed to be extremely overvalued. Consequently, I am initiating coverage with a 'Sell' recommendation and a fair value estimate of $250 per share.

For further details see:

Tyler Technologies: High-Quality IT Service Provider For Public Sector