TYL - Tyler Technologies: Solid 2030 Vision But Still Outside Buy Zone

2023-07-11 17:05:17 ET

Summary

- Tyler Technologies is a market leader in providing digital solutions software to the public sector, with a focus on shifting towards a SaaS business model for stable, recurring revenue.

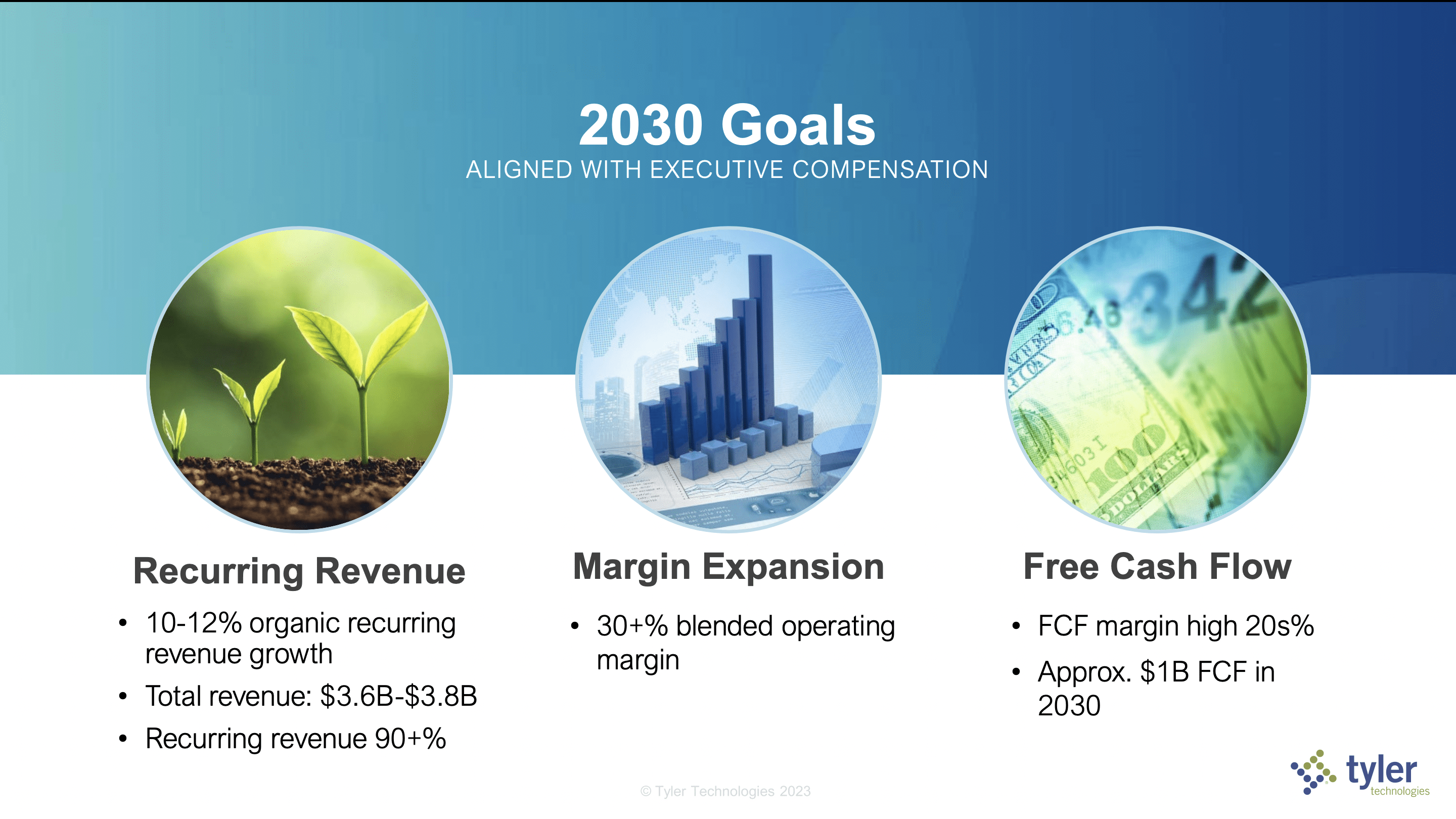

- The company's 2030 Vision includes a 10-12% recurring revenue growth, making 90% of revenue recurring, and enhancing margins.

- Tyler's market is substantial and growing. I assign a hold because of the current valuation.

Thesis

Tyler Technologies ( TYL ) is a market leader, delivering mission-critical digital solutions and software to the public sector. The firm's continued shift towards a SaaS business model has provided them with a stable and high retention rate. TYL announced an impressive 2030 vision, and if they deliver on their promises, I think shareholders can really benefit. TYL's market is substantial and growing. The market is also very fragmented, with no company having the same scale as TYL. I assign a hold rating because of the current valuation, and I will explain each of my thesis's key parts in the following sections.

Company Overview

Tyler Technologies provides a broad line of software solutions and services to address the IT needs of cities, counties, schools, and other government entities. Its products and services are used in Financial management, education, courts, tax billing, Human Resources, public safety, and more. TYL has 13,000 client locations and 40,000 client installations. The firm allocated 77% of FCF in the past five years towards 17 acquisitions. 75% of The company's revenue is derived from the U.S., 10.2% from the U.K., 6.7% from Canada, and 5.3% from Australia. The firm has three core products, Munis (ERP system), Odyssey (court management system), and payments. The company makes revenue from five primary sources: Subscription-based services, Maintenance, Professional Services, Software licenses and royalties, and Appraisal services.

Outlook

Company's 23 Investor Day Presentation

{kind=link}

On June 15th, 2023, TYL had its investor day for the first time in more than four years. The firm introduced its 2030 Vision. The company is projecting 10-12% recurring revenue growth and expanding operating and FCF margins. I believe these expectations/goals are achievable and will explain why.

Let's start with the recurring revenue growth. Is it possible for the company's recurring revenue to grow at an annual rate of 10-12%? I believe it is because demand for SaaS is increasing, and TYL customers seem to love this business model. In fact, TYL's subscription revenue has been booming over the past five years, increasing from $220.5 million in 2018 to $1.0 billion in 2022. The company had this to say in its annual report.

have seen a steady increase in the percentage of new software clients choosing our cloud model in recent years... with an increasing preference to provide our solutions in the cloud. We are making significant investments in optimizing our products to be deployed efficiently in the public cloud and over a multi-year period are transitioning from hosting clients in Tyler's proprietary data centers to utilizing Amazon Web Services ("AWS") for cloud hosting.

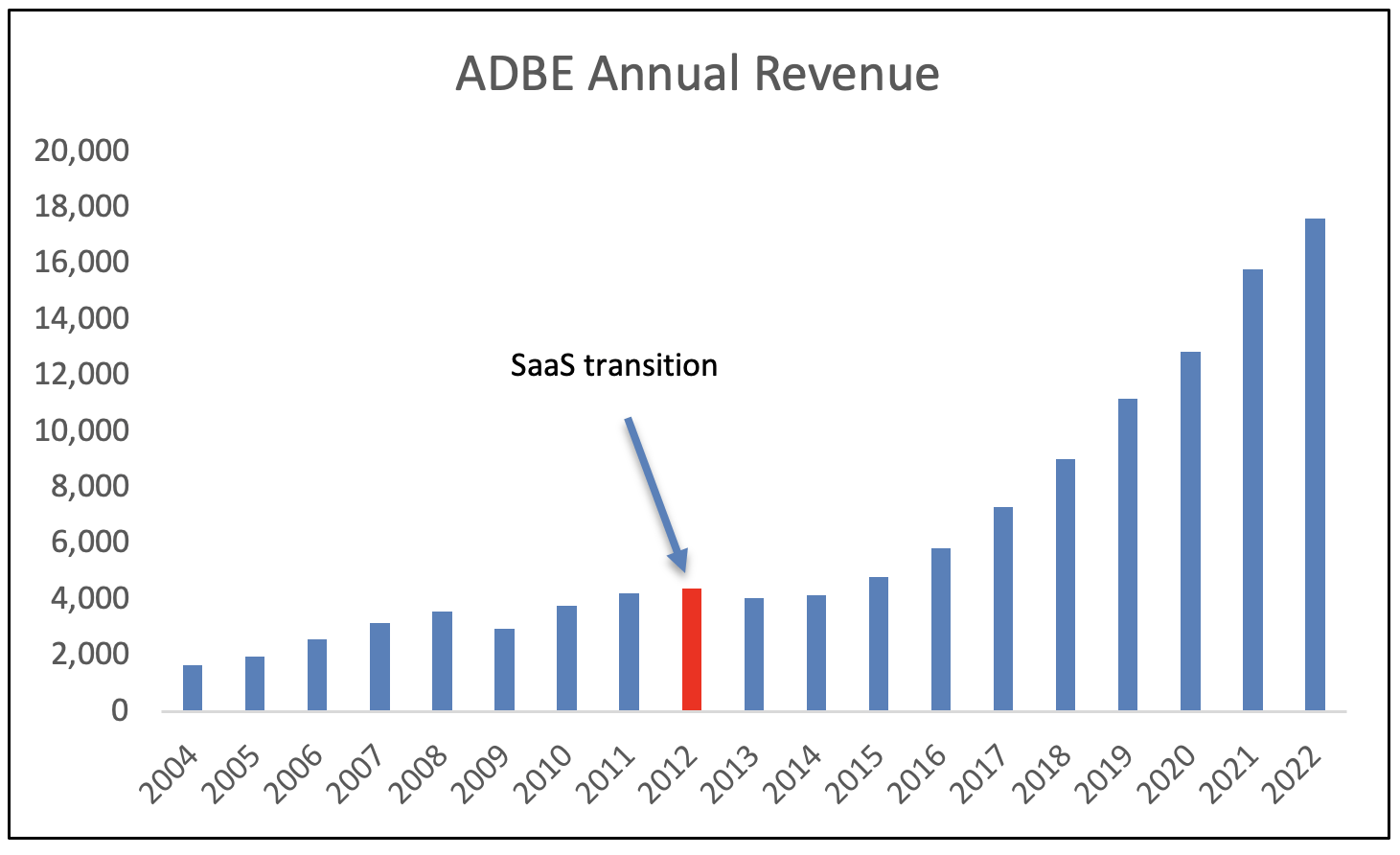

Given the fact that TYL already has 13,000 client locations, The firm has established a strong reputation and can easily leverage the existing client base as an asset to get new clients. TYL can also add more services to its subscription so that it's more attractive to clients who are a little hesitant about switching. I think it is worth mentioning that maintenance revenue will decline as licensed clients migrate to SaaS, but the firm believes that the tailwind from SaaS Growth will exceed the headwind from Declining License Fees. Historically, SaaS transitions have proven to increase customer retention and the company's revenue over time. We saw that happen with Adobe ( ADBE ) after the company transitioned into the SaaS business back in 2012 and experienced exponential revenue growth.

{kind=link}

As for the 400-500 bps (4-5%) margin expansion by 2030, TYL hopes to do that by completing the shift towards Cloud-first. I believe enhancing margins through a shift toward the cloud is possible. How, you might ask? Well, the cloud is cost-effective, and It helps companies minimize IT expenditures because it eliminates the need to invest in hardware and software. Instead, they can just use a third party (like AWS) to host their cloud. As costs decrease, margins increase. As margins increase, the company finds itself with extra cash. It can spend that cash on acquisitions and investments, return it to shareholders in the form of buybacks, or increase the dividend yield.

Market Overview

The state and local government market is one of the largest and most decentralized IT markets in the country, consisting of all 50 states, approximately 3,000 counties, 36,000 cities and towns, and 12,900 school districts. The firm has capitalized on the fragmented market by capturing every section of the public sector it can. Additionally, Many local governments have difficulties attracting and retaining staff to support their IT functions. As a result, they establish long-term relationships with reliable providers that can offer them those services, such as Tyler. TYL's market is expected to keep growing. The firm had this to say about market growth in its 2022 annual report.

Gartner, Inc., a leading information technology research and advisory company, estimates that state and local government application and vertical-specific software spending will grow from $27.8 billion in 2023 to $40.0 billion in 2026. The professional services and support segments of the market are expected to expand from $33.5 billion in 2023 to $41.9 billion in 2026. Application and vertical-specific software sales in the primary and secondary education segments of the market are expected to expand from $5.4 billion in 2023 to $6.6 billion in 2026 while professional services and support are expected to grow from $5.1 billion in 2023 to $6.1 billion in 2026. For the national and international government markets, application and vertical-specific software sales are expected to expand from $42.2 billion in 2023 to $61.5 billion in 2026 while professional services and support are expected to grow from $65.6 billion in 2023 to $82.1 billion in 2026.

I calculated the annual growth of all the sectors mentioned by management above, and they averaged a 7% annual growth rate from 2023 to 2026. I have checked for competitors in the industry, but I couldn't find one that has the same scale as TYL.

Valuation

I expect TYL's customers to continue shifting towards subscriptions. I estimate that total revenue will grow at a compounded annual growth rate of 8.09% from 2023 to 2027. The main revenue drivers in my model are market growth and increased customer spending. The company can use its current customer base to upsell products. It can also use it as leverage to add new customers. On average, every customer uses at least three TYL products.

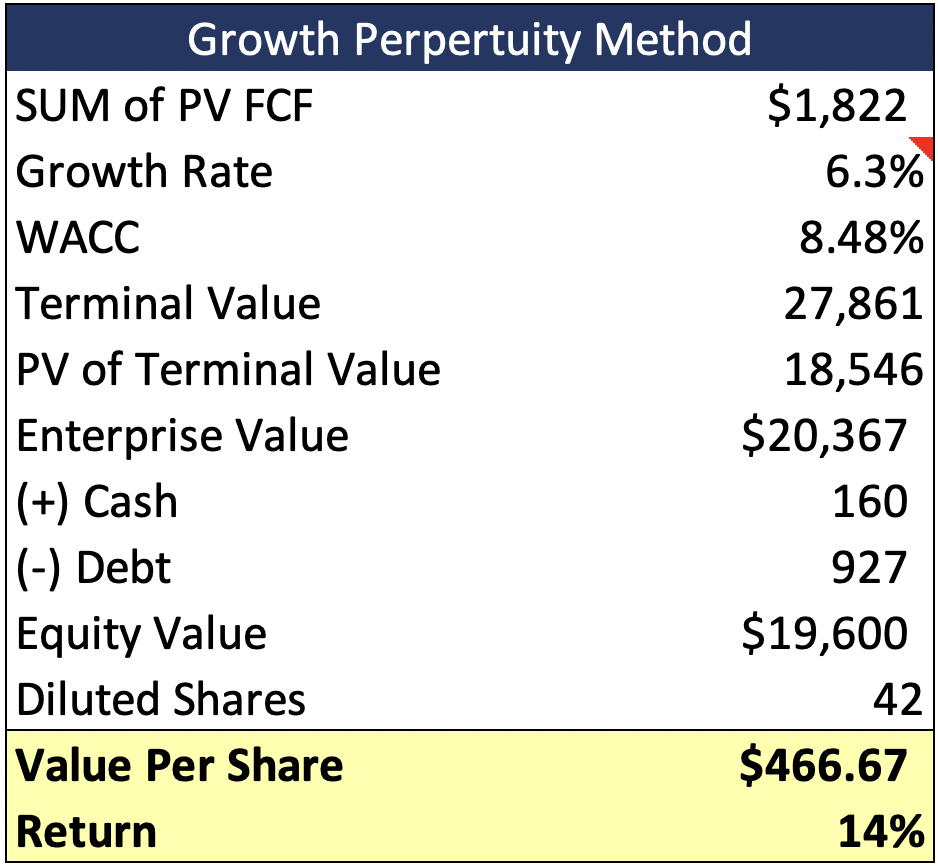

My fair value of TYL is $468, which represents a 14% increase from the current price. This implies an EV/EBITDA ratio of 43.16x for 2023. The company has also stepped up its R&D spending (almost $300 million) in the last three years. I believe this was part of the cloud investment in order for the company to deploy its products efficiently.

I assign a hold because, according to my valuation, the company seems fairly valued at $411. Plus, a 14% return isn't that attractive to me. TYL has 41.9 million shares outstanding, cash of $159.7 million, debt of $926.5 million, a share price of $411, and an enterprise value of $18 billion.

{kind=link}

Risks

1) TYL historically has been trading at a very high multiple compared to the competitors I listed above. Although TYL operates in a market where there is no competitor of its scale, As TYL moves away from small-time partnerships into big contracts, it will perhaps rub shoulders with other giant software companies.

2) Given that TYL derives most of its revenue from the public sector, It is at risk of new legislation. A new law was to pass in a city that TYL operates in that prohibits local governments from contracting with third-party IT providers, a potential risk. Clients can also spend less, depending on the budget they are given.

Conclusion

The bottom line is that 80% of TYL's revenue is recurring, which provides the company with stable cash flow. A successful transition into the cloud will leave the company with more cash to reinvest or return to shareholders. I expect the company to cross-sell its huge customer base to increase revenue and customer retention. The current price is a little expensive to me; perhaps when the price comes down a little bit and nothing bad has happened to the business, then I might upgrade from hold to buy.

For further details see:

Tyler Technologies: Solid 2030 Vision But Still Outside Buy Zone