PWSC - Tyler Technologies: Well-Positioned In A Growing Market

2023-05-05 14:57:05 ET

Summary

- Tyler is a leading provider of software to local governments in a market with significant modernization potential, representing a TAM of over $12 billion.

- The company offers a comprehensive range of back-office enterprise software solutions for government operations.

- Tyler company's competitive position remains strong, and its expanding TAM and shift to SaaS should mitigate long-term revenue growth risks and improve gross margins.

- I keep a year-end price target of $464 on the stock based on a forward EV/Sales multiple of 9x and a 2024 revenue estimate of $2.13 billion.

Editor's note: Seeking Alpha is proud to welcome Next Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Thesis

Tyler Technologies, Inc. ( TYL ) holds a prominent position as a provider of crucial software to local governments, operating in a market with significant potential for modernization, resulting in a TAM of over $12 billion. The company's transition to a SaaS model will continue to support revenue growth, although it may temporarily impact margins and growth due to the slow pace of change in the public sector until FY23. I remain optimistic on Tyler's competitive position, its expanding TAM, and its transition to a SaaS model, which should reduce long-term revenue growth risks and improve gross margins. Hence, I keep a year-end price target of $464 on the stock based on a forward EV/Sales multiple of 9x and a 2024 revenue estimate of $2.13 billion.

{kind=link}

Post Q1 2023 Outlook

TYL posted a solid Q1 2023 result, with the highlights including a better-than-expected EPS, a higher mix of SaaS revenue, and an increase of 5.5% YoY in new SaaS Annual Recurring Revenue ((ARR)) bookings from new customers. The total subscription bookings also saw a 24% YoY increase, benefiting from easier comparisons with the previous year. The growth in subscription bookings was driven not only by new SaaS and conversion activity but also by cross-selling and upselling to existing customers. Looking ahead, there is a possibility that the growth in subscription bookings may moderate in the second and third quarters due to tougher comparisons. Nevertheless, this category is expected to be the fastest-growing segment of TYL's business. Looking forward, I anticipate that margins for FY24 will increase within the target range of 50-100 basis points as the company continues to operate in-house data centers until FY24, after which they will phase out, leading to a more than 100 basis points expansion in FY25.

Leading Software Provider to Local Governments

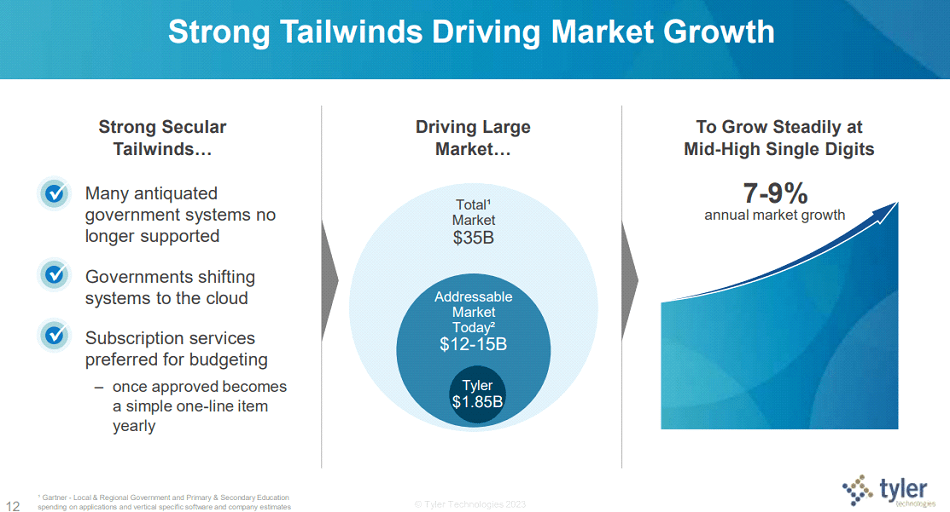

Tyler has estimated a total addressable market ((TAM)) of $12-15 billion for government and education IT spending in the United States. According to Gartner, worldwide government IT spending is projected to reach $588.9 billion in 2023, increasing by 7% from 2022. The primary drivers of this spending growth are the modernization of legacy systems and the enhancement of access to critical digital services. Tyler has focused on application and vertical-specific software spending within this market, which aligns with its product offerings more accurately.

Tyler has identified three potential growth opportunities for expanding its TAM. Firstly, the company sees potential in entering the state, federal, and international markets. While state expansion appears to be the immediate focus and is likely to have the most significant impact in the near term, the federal market and international expansion are also seen as longer-term opportunities. Although Tyler's current product offerings are more tailored to local and state governments, the federal market could be considered as a potential opportunity in the future.

Although Tyler's management has not currently planned to expand outside of the United States, international expansion could become a higher priority in the long run. It is worth noting that the company's growth potential in these markets would depend on its ability to adapt its offerings to meet the specific needs of each target market.

{kind=link}

Broad Product Portfolio

Tyler offers a comprehensive range of back-office enterprise software solutions that are crucial for government operations. Their extensive portfolio includes eight product families, such as ERP, courts and justice, public safety, platform technologies, appraisal and tax, civic services, schools, and others. This diverse range of offerings positions Tyler as a unique provider in the public sector, as few, if any, competitors can match the breadth of their solutions. This makes Tyler a convenient one-stop-shop for local governments seeking mission-critical software.

Local governments are known for being loyal customers, as evidenced by Tyler's impressive 98% client retention rate . The software provided by Tyler is not only mission-critical but also deeply ingrained in government operations. Implementing new software is considered resource-intensive in terms of time, labor, and cost, which reinforces the stickiness of Tyler's solutions.

Transition to SaaS will take some time and put pressure on margins in the near term

Tyler, like other companies in the market, is transitioning its business model from perpetual licenses and maintenance to Software as a Service (SaaS). This shift has several implications. Firstly, the move to SaaS is seen as positive because Tyler can charge approximately double for SaaS contracts compared to maintenance contracts. This is due to the additional hosting services and updates provided, which increase recurring revenue and the lifetime value of contracts, especially considering Tyler's high client retention rates.

Tyler has maintained profitability and generated consistent cash flow, and I expect this to continue despite facing some near-term margin challenges. These challenges include a shift to SaaS, resulting in a decline in higher-margin license revenues, the presence of duplicative costs for maintaining internal data centers and AWS-based cloud as SaaS clients transition, the return of travel and trade show expenses postponed during the pandemic, and rising compensation and healthcare costs. The decline in license revenues and bubble costs is expected to persist in FY23, but thereafter, cost growth is expected to stabilize, making FY23 the margin trough, in my view. Margins will continue to expand in FY24 as Tyler exits its internal data centers, eliminating duplicative bubble costs, and the shift to subscriptions offsets the decline in licenses.

Valuation

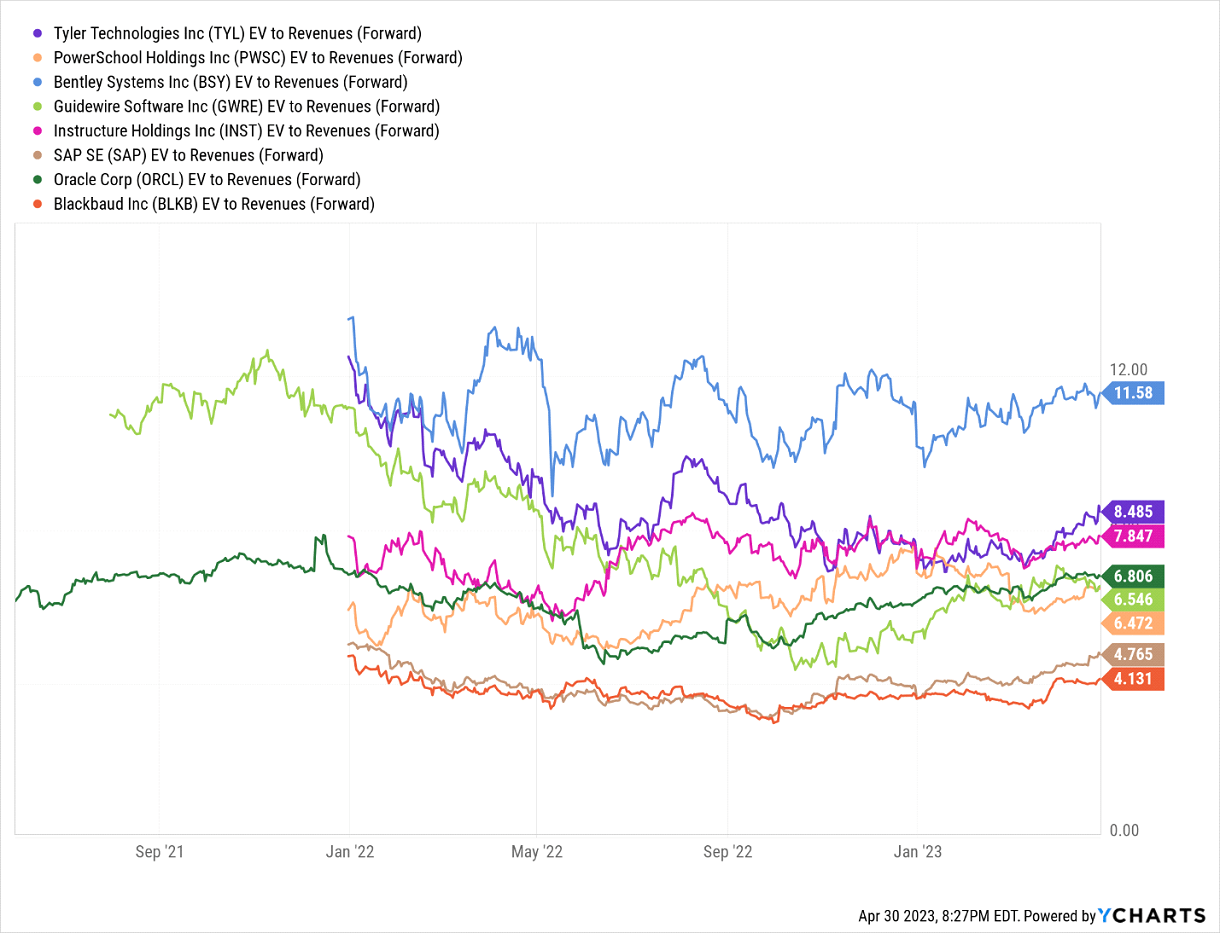

I use two comparison groups to evaluate the valuation of Tyler Technologies, Inc. The first group consists of vertical SaaS companies that are experiencing double-digit growth and have profitability. These companies have a similar financial profile and competitive backdrop as Tyler. While there are few direct competitors of Tyler at a similar scale, I look at companies focused on a single vertical with comparable financials for relative valuation. For instance, PowerSchool Holdings, Inc. ( PWSC ) and Instructure Holdings, Inc. ( INST ), which also serve public sector entities, fall into this category but trade at lower multiples due to their smaller TAM compared to Tyler.

The second group includes legacy horizontal enterprise resource planning vendors like Oracle Corporation ( ORCL ) and SAP SE ( SAP ). Although their trading levels differ significantly from Tyler, I include them in the comparison because Tyler's Munis and Incode ERP products compete with them.

Historically, Tyler has traded at an NTM EV/Sales multiple in the mid-10x range, representing a healthy premium compared to its vertical software peers. However, I remain optimistic about Tyler's competitive position, its expanding TAM, and its transition to a SaaS model, which should reduce long-term revenue growth risks and improve gross margins. Hence, I keep a year-end price target of $464 on the stock based on a forward EV/Sales multiple of 9x and a 2024 revenue estimate of $2.13 billion.

TYL's Valuation Metric vs Peers (YCharts)

{kind=link}

Risks

Like any other investment idea, my buy recommendation on TYL has some risks attached to it. The company is currently trading at a premium valuation compared to peers in the vertical SaaS market and ERP vendors, which poses a downside risk given the current market conditions. The market has not been kind to stocks with high valuations in the past one year, and there is a possibility that the multiple trends down in the medium term.

Moreover, there is potential for slower adoption of SaaS by government entities, which could result in lower growth for Tyler, which would affect the stock price. Additionally, although Tyler has benefited from the public sector's slower adoption of new technologies, if governments do not transition to SaaS as quickly as expected, Tyler may not experience the anticipated growth from recurring revenue buildup and maintenance to SaaS conversion, potentially leading to lower growth than my estimation of 8-10% annual growth.

Final Thoughts

TYL is a company that supplies essential software to local governments, and its customer base is loyal and difficult to switch. The potential market for its products and services is substantial and expanding. While Tyler's products are tailored to local and state governments, the federal market and international expansion remain longer-term opportunities, contingent on adapting offerings to meet specific market needs. The company is transitioning to a SaaS model, which will continue to support revenue growth. I keep a buy rating on the stock with an end-of-year price target of $464.

For further details see:

Tyler Technologies: Well-Positioned In A Growing Market