TSN - Tyson Foods: Deep Drop After Earnings Presents Opportunity

2023-05-18 02:44:26 ET

Summary

- Tyson Foods fell hard after their earnings, but things have been stabilizing a bit since.

- I believe that shares were cheap previously, and despite a loss, the shares still look cheap.

- TSN is a more cyclical company, despite being a consumer staples stock.

- Buying when things are dire can often lead to being rewarded long term.

Tyson Foods ( TSN ) was hit when they announced their latest earnings last week. Since announcing these results, the shares have come back from the lows but are still off meaningfully from where they were prior. The quarter was a shock as the company announced a loss for the quarter.

TSN Q2 Earnings News Post (Seeking Alpha)

This was most definitely a shock as it missed analysts' expectations for a $0.80 profit for the quarter. That compares with the $2.29 they had earned in the year prior. They also missed revenue estimates, but it was up a touch year-over-year. They also took their fiscal 2023 sales expectation down to $53 to $54 billion. That was down from the $55 to $57 billion expected in the previous quarter .

What's The Problem With Tyson?

TSN has been on my watchlist for a while, and in a previous article posted last December, I felt that shares were "getting cheap."

TSN Performance Since Prior Update (Seeking Alpha)

I also had an update in earlier 2023 in January , where I outlined some puts I had sold expiring worthless. (In hindsight, I certainly dodged a bullet there!)

I certainly wasn't expecting a loss for the quarter, but I do feel that TSN still represents a fairly interesting name to consider. In the previous update on TSN, I also noted that they are a more cyclical food company. They aren't as steady in terms of Conagra ( CAG ), Kellogg ( K ) or General Mills ( GIS ). We highlighted this previously when looking at how volatile their earnings had been historical. This latest quarter certainly reflected that. That being said, this is also their first loss since going back to the great financial crisis.

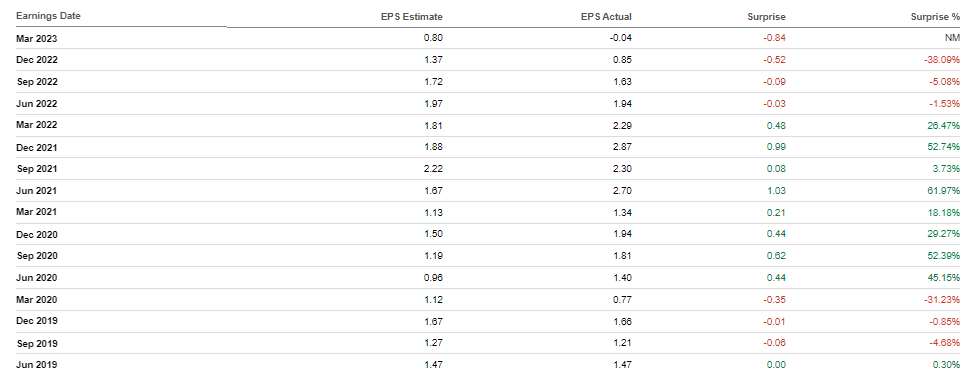

TSN has also been on a pretty poor run of continually missing analysts' expectations over the last year. To be fair, though, this was also after many quarters of putting up numbers that were also well ahead of analysts' expectations.

TSN Earnings Misses/Surprises (Seeking Alpha)

{kind=link}

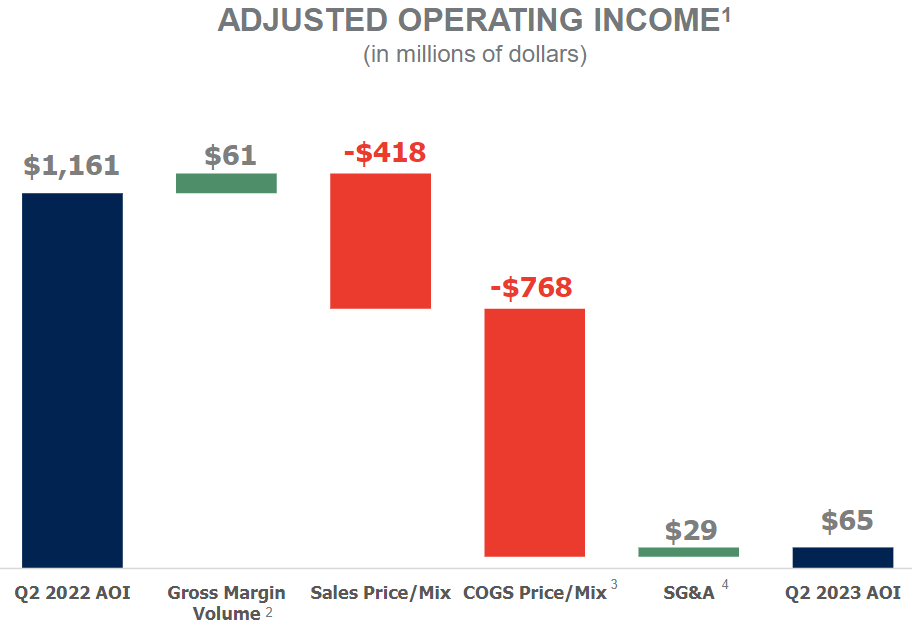

Besides the weaker sales than expected, there are other headwinds going on with TSN. Volumes were up, with chicken being the primary driver. Beef volume was lower due to "softer export markets." The average sales price was down overall, with beef and pork pricing weaker. The cost of goods was a big factor in hitting their income for the quarter.

TSN Adjusted Operating Income YoY (Tyson Foods)

{kind=link}

The driver of this was in beef and chicken, that they specifically noted on their call .

More than 90% of the decline in adjusted operating income was driven by lower earnings in Beef and Chicken. Higher input costs per pound in all segments except Pork increased our cost of goods sold. The majority was driven by inflationary impacts on raw material and labor costs. The remainder of the increase was due to a few things: inventory value adjustments, unfavorable derivative impacts and a shift producing more value-added mix and this was partially offset by savings from our productivity program, reduced outside meat purchases in Chicken and decreased supply chain costs.

Beef is the largest segment for them in terms of sales, followed by chicken. It is then retail brands, and pork is their smallest segment. Retail brands/prepared foods saw operating margins tick a bit lower, but it certainly wasn't negative like we saw in the chicken and pork categories. They essentially finished flat with adjusted operating margins of 0.2% for beef in the quarter.

With no operating margins or negative operating margins in their largest category, it doesn't matter how much they have in sales; it won't be a pretty outcome.

TSN Segment Margins (Tyson Foods)

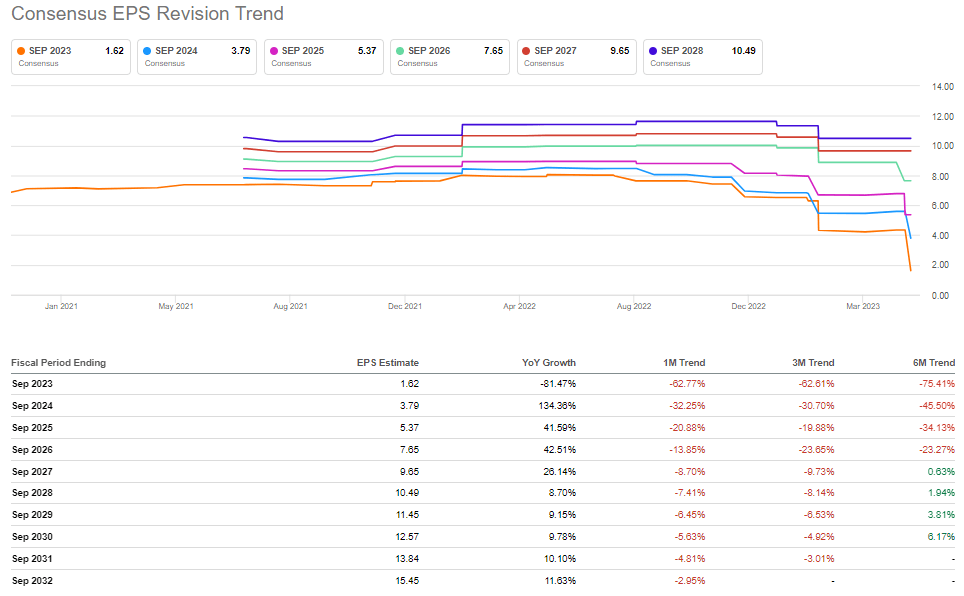

Of course, after such a quarter like that, analysts raced to revise the outlook lower.

TSN Earnings Revisions (Seeking Alpha)

{kind=link}

Despite this rush to reduce their outlook, analysts are still expecting a profitable year through fiscal 2023. As this was TSN's second-quarter earnings, we have the second half to go. In the first quarter, they announced $0.85 in adjusted earnings. That leaves us at $0.81 for the first half of the year. In total, analysts expect EPS to come in at $1.62. That leaves just another $0.81 in adjusted EPS in the next two quarters. It certainly isn't a high bar at this point.

TSN Earnings Estimates (Seeking Alpha)

{kind=link}

However, with a weaker economy expected towards the end of the year, that could be another potential headwind. As they are a meat protein company, consumers tend to be more price sensitive. That's how we end up with more cyclical earnings in the first place for TSN. They are more dependent on a healthier economy, making it a cyclical food name.

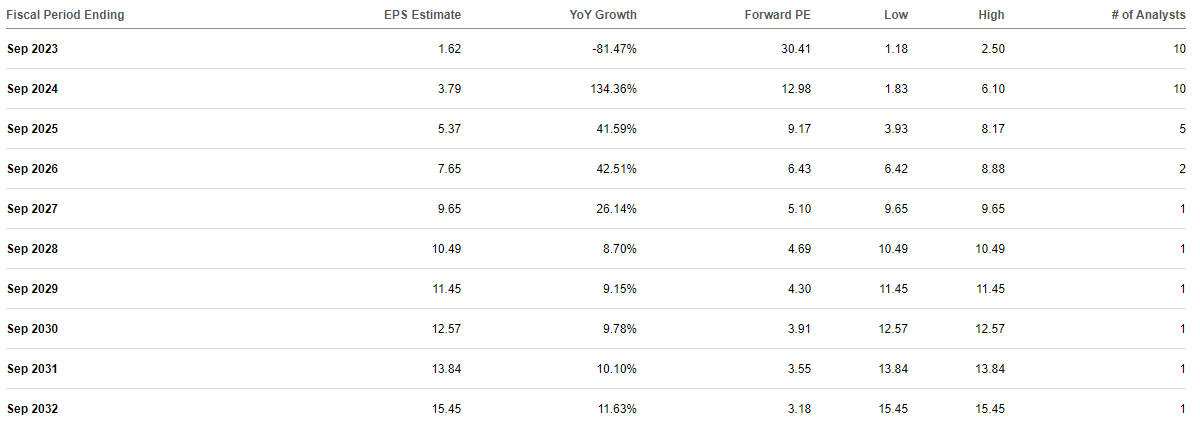

Still, despite that, analysts are expecting earnings to recover meaningfully in the next fiscal year. Then the company's earnings are expected to thrive for several more years after that.

Where Is Fair Value For Tyson?

Being that this is a more cyclical name, it's often the best time to pick up shares when things look the most dire. With an earnings loss, things certainly seem ominous at this point. It's usually when no one wants to buy shares.

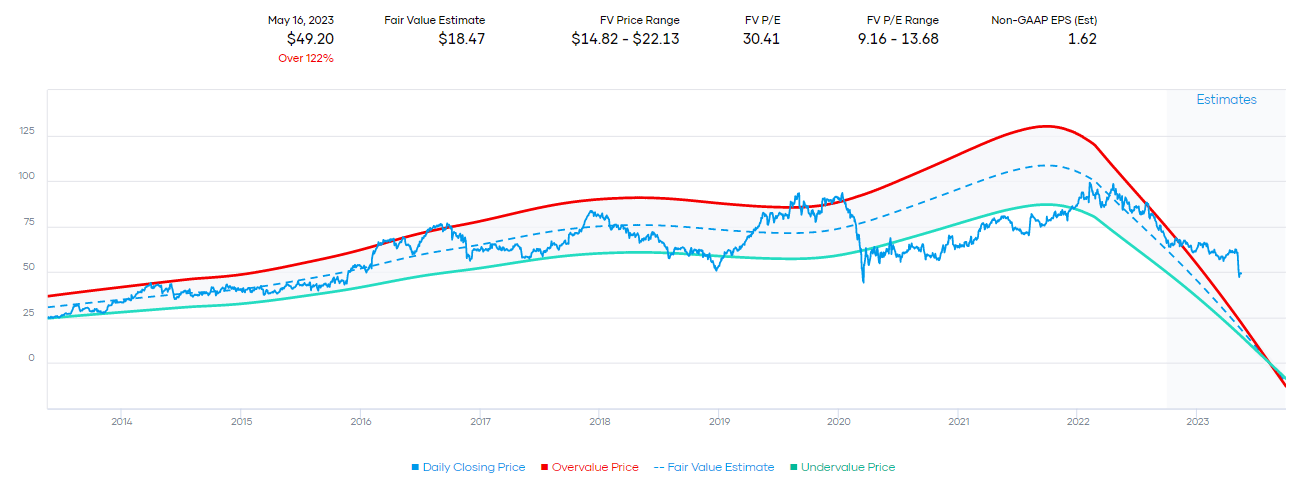

And that said, one of my favorite ways to find a fair value for a company is based on its historical trading range based on its P/E in the case of this company. With negative earnings, that doesn't give us too much to go off of with the chart I usually use.

TSN Fair Value Estimate Range (Portfolio Visualizer)

{kind=link}

This is because it doesn't estimate out beyond the next year. Therefore, it just illustrates a drop in the next year and would assign an incredibly low fair value. However, if we look back at the earnings expectations for the coming years, we can see a forward P/E of around 13x kick in next year when earnings are expected to push higher to $3.79.

Given that information, and if they are able to achieve that, it would put them right in their longer-term range. That could indicate that if an investor has a year or more to invest, TSN could be considered fairly reasonably valued at this time.

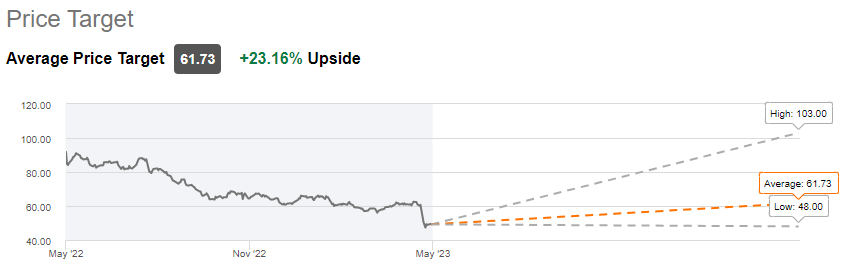

We can also take a look at the price target of Wall St. analysts. In this case, they assign an average price target of $61.73.

TSN Price Target (Seeking Alpha)

{kind=link}

That could also indicate that now is a fairly strong time to consider picking up shares at this level. Interestingly, Morningstar also still assigns the shares a price target of $103 despite that latest quarter. That seemingly is the outlier in the chart above.

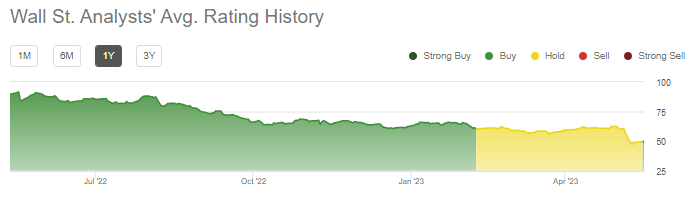

Wall Street analysts actually had rated it a "Hold" prior to these earnings. Yes, they were also bullish throughout most of the prior year as shares sank lower. However, they only more recently averaged back to a "Buy" rating. The breakdown is 4 analysts rating the stock a strong buy, 6 holds and 2 sell ratings.

TSN Wall St. Analyst Rating History (Seeking Alpha)

{kind=link}

Still, like buying any investment, it's impossible to know exactly where the low is, and things can always go lower. With the expectation for a recession, things could remain challenging for TSN over the next several quarters. Analysts seem to anticipate that 2023 overall will be a tough year, but they are much more optimistic for 2024.

Is Tyson's Dividend Safe?

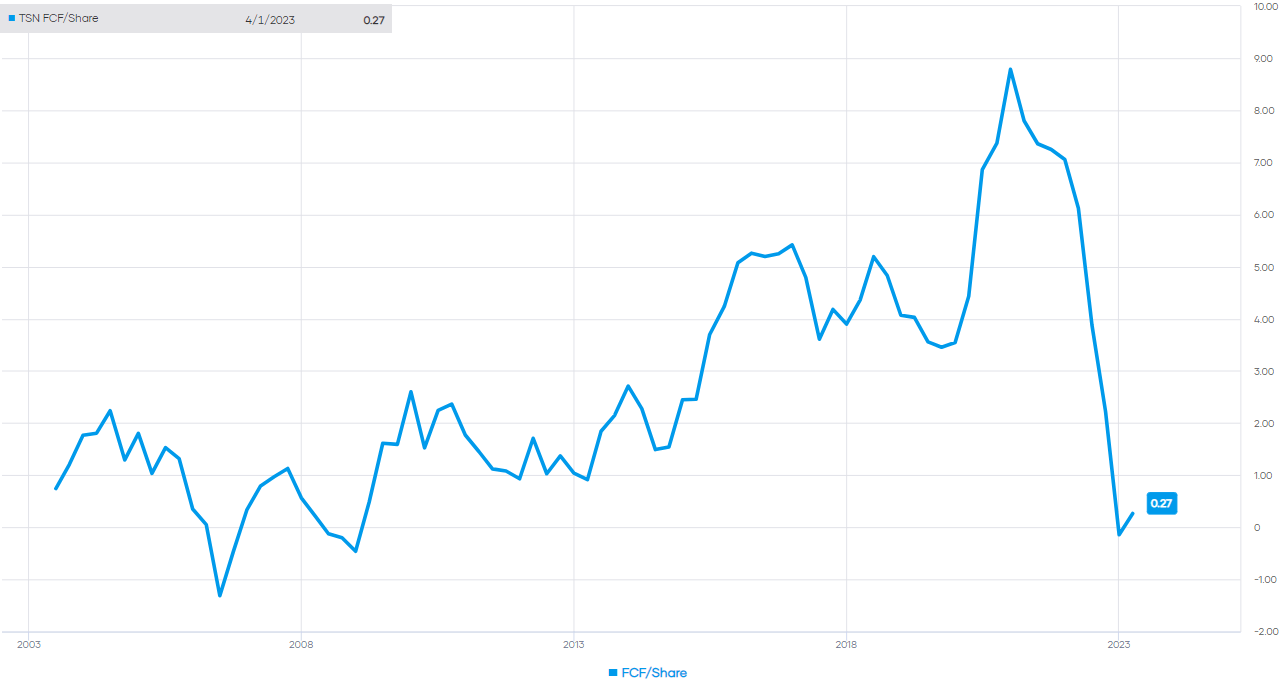

After their earnings, they announced their next quarter's dividend in line with the previous. At $1.92, that's above the consensus estimate for EPS through this year. Along with their EPS hit, they had only shown a fraction of FCF for the quarter that would have covered the dividend as well. FCF basically fell off a cliff along with earnings.

TSN FCF/Per Share (Portfolio Visualizer)

{kind=link}

However, the company does seem to be committed to returning capital to shareholders. That's through the dividend and share repurchase.

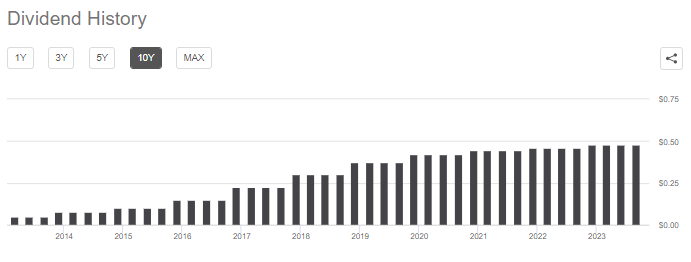

...during Q2, we returned $167 million to shareholders through dividends and $19 million in share repurchases. We have increased our dividend for 11 consecutive years and remain committed to supporting our dividend.

Dividend increases were much slower in recent years, but perhaps they knew that times were going to be tough.

TSN Dividend History (Seeking Alpha)

{kind=link}

It was since Covid that they really slowed this growth down despite what had been a low payout ratio during this time. It was generally around 20% as they benefited materially when stimulus money was being injected into the economy.

All this said, with the recent dividend announcement, it would seem that they intend to keep paying out the same amount. They may choose not to raise it later this year, though. Unless things improve materially or they have a solid outlook, that would seem pertinent.

Worth noting is that at least for the last several years, when I was following this company, they declared a dividend in line with the prior, even if it's the dividend they later intended to raise. So they announce the same dividend for calendar Q4 when they historically raise and then announce later that it will be increased. Here was how it worked last year :

Effective November 11, 2022, the Board of Directors increased the quarterly dividend previously declared on August 11, 2022 , to $0.48 per share (+4% from prior dividend) on Class A common stock and $0.432 per share on our Class B common stock.

This time it really might not be a raise, though. If the outlook turns worse, investors should also be prepared to hear about a dividend cut. They simply don't have any cushion here to really play with since they are overpaying based on the latest figures.

To sum up, they seem to be committed to the current dividend. The caveat is that with earnings and FCF coverage lacking, they could later be forced to cut without improvements. If things worsen, investors should be prepared for a decrease.

Conclusion

TSN took a beating after announcing a loss recently. However, for the more aggressive investors out there that can handle a cyclical company, this can often be the best time to consider initiating a position when things seem dire. I was bullish before, and that certainly wasn't the best timing. This may not even prove to be the low should we slip into a deep recession. For now, it would seem that most expect a recession to be more mild. Using a dollar-cost average approach could be a decent approach.

Alternatively, selling cash-secured puts can be a bit more of a conservative way to play this as well. That could allow some more downside to your strike price for further potential weakness. The premium received would also reduce the breakeven of your purchase price. If shares move higher, stay flat or even sag a bit, you simply collect the premium.

For further details see:

Tyson Foods: Deep Drop After Earnings Presents Opportunity