MORN - Tyson Foods: Getting Cheap

Summary

- TSN has been a watchlist name for quite some time.

- Shares have been coming down as expectations for earnings are heading lower.

- TSN has underperformed its sector group due to the volatility in its business.

Written by Nick Ackerman. This article was originally published to members of Cash Builder Opportunities on December 8th, 2022.

Tyson Foods ( TSN ) has been a watchlist name for quite some time. With shares coming down drastically, now is becoming a more interesting time to look at shares. My personal "buy under" target of ~$75 has been breached quite significantly as shares last closed around $61 as of writing.

Food stocks in the consumer staples sector have a tendency to draw me in. They aren't fast-growing but offer generally stable earnings and pricing power. The simple fact that people have to eat to live is what keeps the demand for food going. I'd be tempted to say utility-like qualities aren't too far off from being accurate.

TSN is a bit different in that their earnings aren't as stable. They can go from boom to bust due to trends in demand, as meats are a huge part of their business. Being on the higher end of the food category means trading down can have a more material impact. This was the specific highlight of a recent downgrade from Barclays ( BCS ) on shares of TSN (as well as Beyond Meat ( BYND )).

Due to this, TSN is underperforming the consumer staples sector quite materially. For what it's worth, it was outperforming earlier in the year before demand started to wane. Yet another sign that consumers were flush with cash but are now starting to feel the impacts of rising inflation.

YCharts

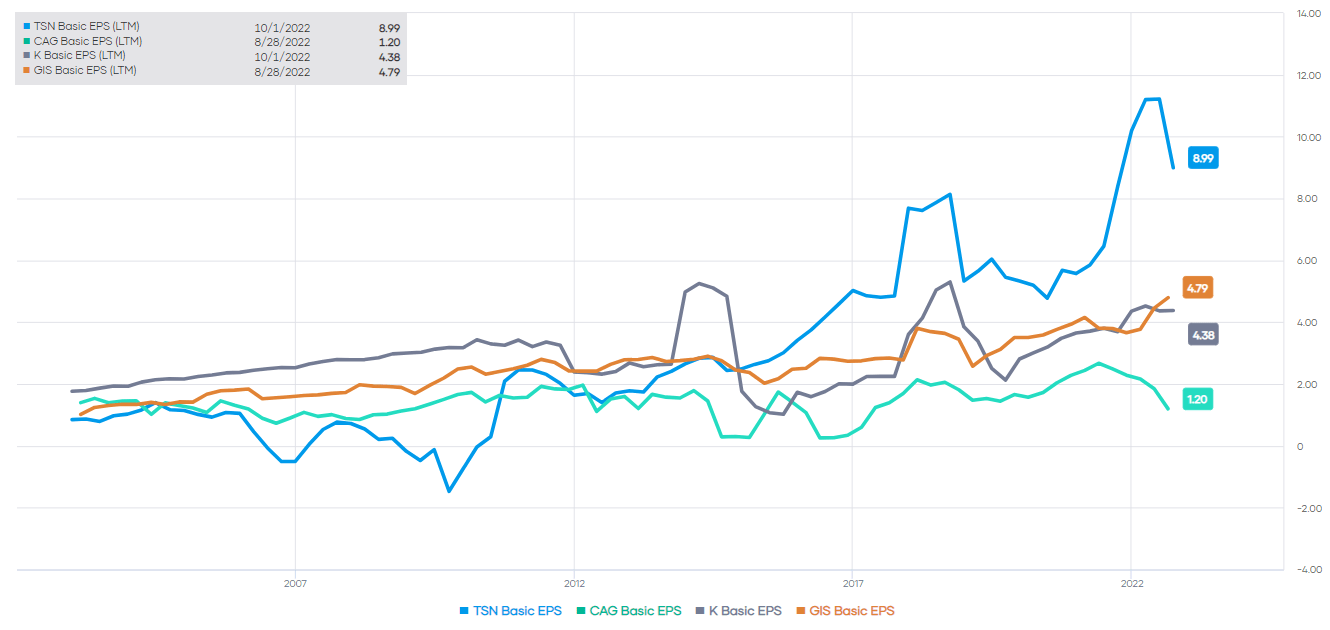

Wild Earnings

One of the benefits of being an outlier in its industry with volatile earnings is that for all the dips, there seem to be periods of faster growth too. The chart below looks at EPS over the last 20 years for several consumer staple food stocks. We are using basic GAAP EPS and no fancy non-GAAP shenanigans here to compare. Those include Conagra ( CAG ), Kellogg ( K ) and General Mills ( GIS ).

{kind=link}

The general takeaway that I see here is that there are some bumps in earnings here and there for all these companies. Though I'd argue we see more cyclicality in TSN's earnings. However, we also see that TSN has grown earnings at a faster clip. All else being equal, I would say that TSN isn't as recession-resistant as we are used to seeing in the food industry.

Some changes in earnings over time are only natural through various economic periods or restructurings of the company. That could include mergers, spin-offs and the like, as it's a relatively boring industry but goes through the same streaks of combinations and divestitures as any other industry. K is one example of this that is anticipated to split into 3 different companies.

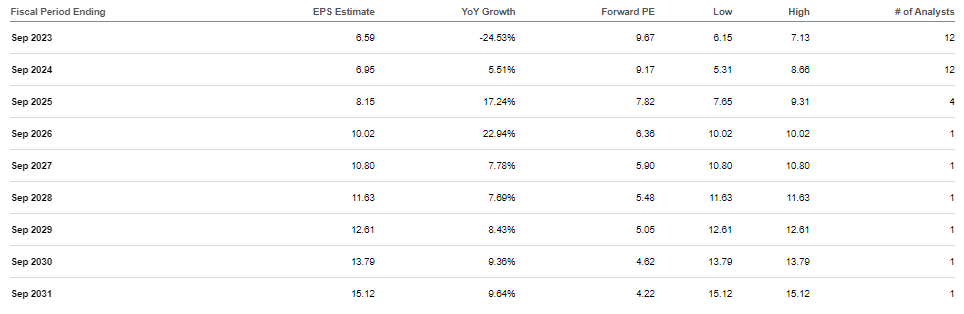

This trend of earnings for TSN doesn't seem as though it is going away either; analysts have earnings being quite volatile going forward too. Of course, this is what we would expect for TSN. However, these large increases and decreases are not usual for peers when looking at the estimates for these other companies.

{kind=link}

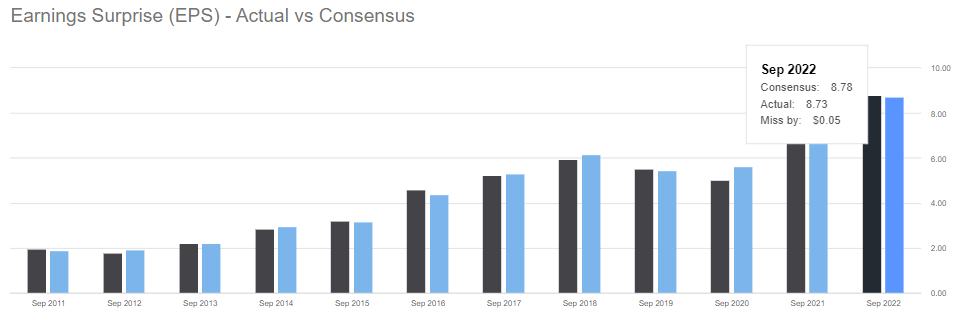

What I would note is that in 3-5 years, earnings are still expected to be higher then than they are now. They missed earnings slightly in the latest quarter, and overall for fiscal 2022, the consensus was $8.78, and they actually reported $8.73. Missing earnings aren't a habit of theirs as they've only missed 5 of the last 16 quarters.

{kind=link}

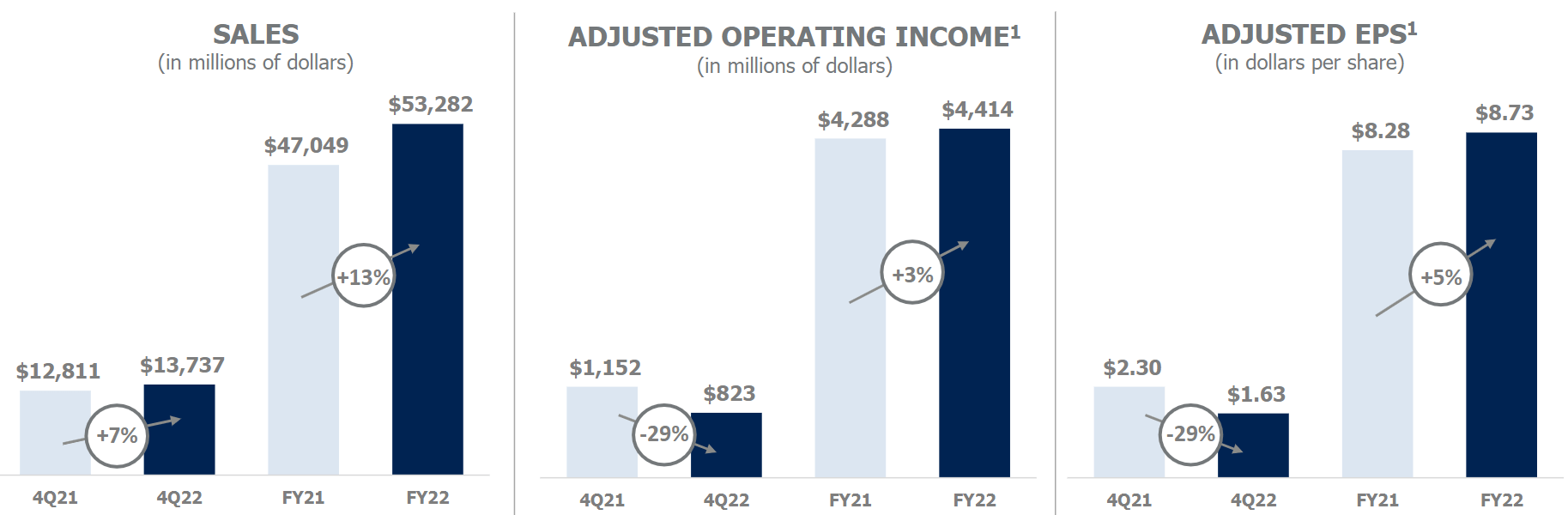

With their last earnings , they beat revenue expectations and put up revenue growth of 7.3% year-over-year. The EPS miss was by $0.09, as they reported $1.63 in non-GAAP EPS. So overall, it wasn't a terrible quarter, but it did show a year-over-year EPS drop quite significantly while sales did not.

{kind=link}

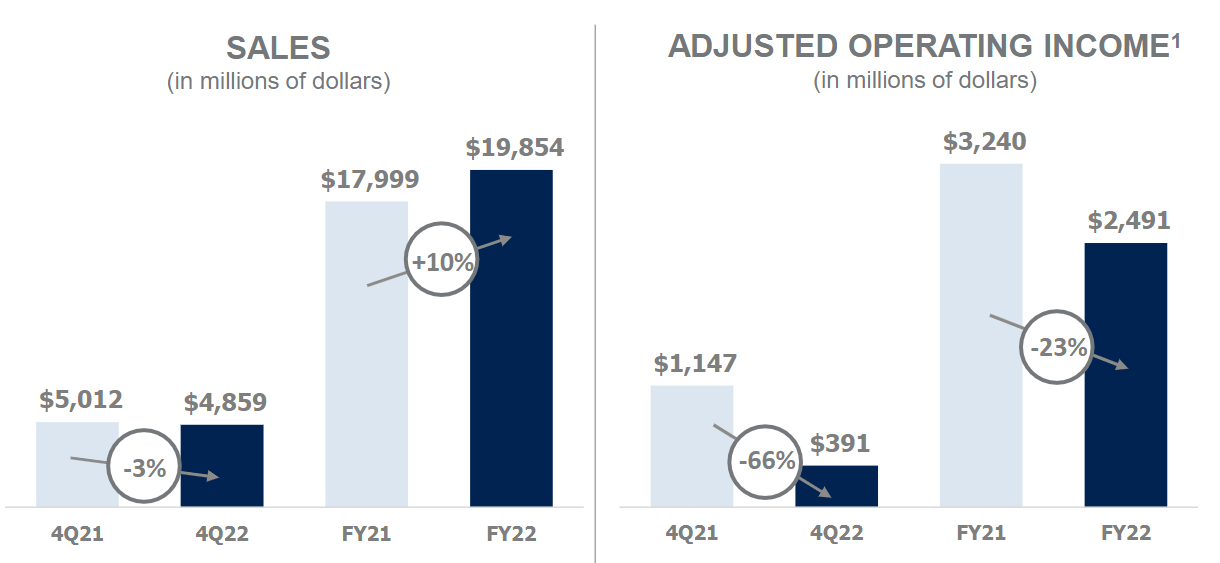

The two categories that were the underperformers were the beef and pork categories. Beef is their largest category based on total sales; this is then followed by chicken, prepared foods and then pork. Here is a look at the sales and adjusted operating income for beef:

{kind=link}

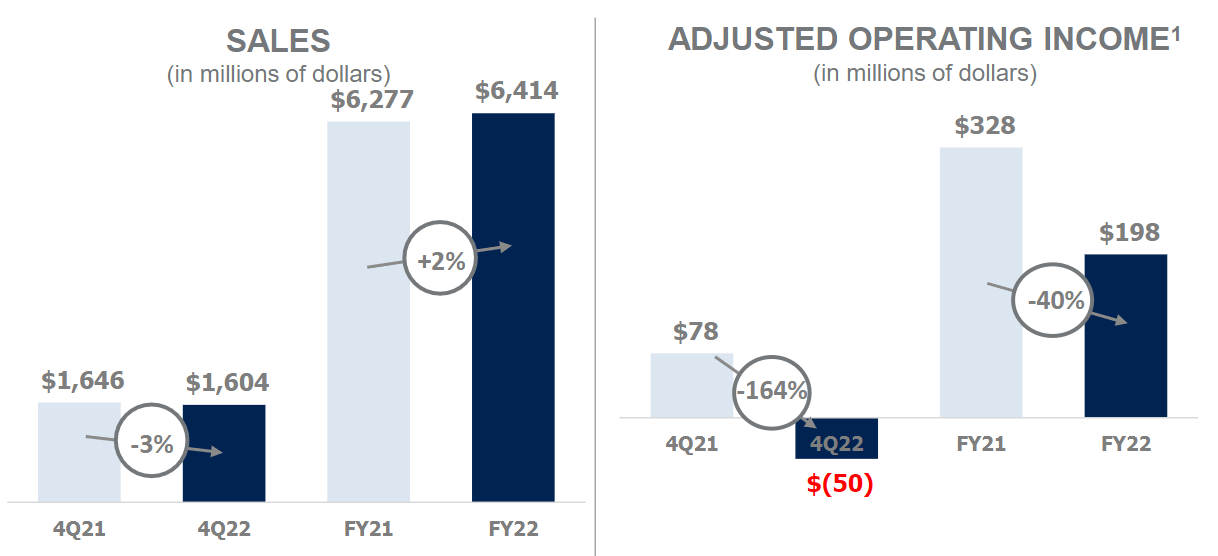

Here is a look at the pork category:

{kind=link}

Their chicken category and prepared foods were highlights of the last year, and in particular, the last quarter.

Revenue for the following year is expected to be between $55 billion and $57 billion. That's an increase from the $53.282 billion they posted this year. In the earnings call, they anticipated that chicken and prepared foods will be the leading categories to help them achieve that. In this case, not mentioning beef and chicken suggests they expect those categories to remain weak for now. Although, they noted that international as a whole should be a growth driver for them too.

We anticipate total company sales between $55 billion and $57 billion, and also expect volume growth compared to the prior fiscal year. Both total company sales and volume growth in fiscal '23 will largely be driven by our Chicken, Prepared Foods and International businesses as we work to run our plants full, optimizing our existing footprint and utilizing new capacity expansions.

For that growth, they outlined new plants coming into operation in the next year.

To grow volumes in our Chicken, Prepared Foods and International businesses, construction is in progress of six new plants, all to be in operation by the end of fiscal 2023. We're building a value-added chicken plant in Danville, Virginia, and we're growing our bacon business with a new location in Bowling Green, Kentucky. And we're also expanding our footprint and increasing volumes outside the U.S. with three plants going live in China and one in Malaysia during 2023.

These investments in the recently announced joint venture partnerships are fueling future growth, both organically and inorganically in our international business. We remain focused on growing internationally and on those fastest-growing protein consumption markets in the world.

Valuation Looking Attractive

As we all know, just because a stock is declining in price doesn't mean it is always a good value. In this case, they are running into an earnings headwind after some solid strength. That's why I believe now is a more attractive time to consider investing in TSN because it is in one of its slumps. As we saw above, earnings are still expected to rise again after 2023.

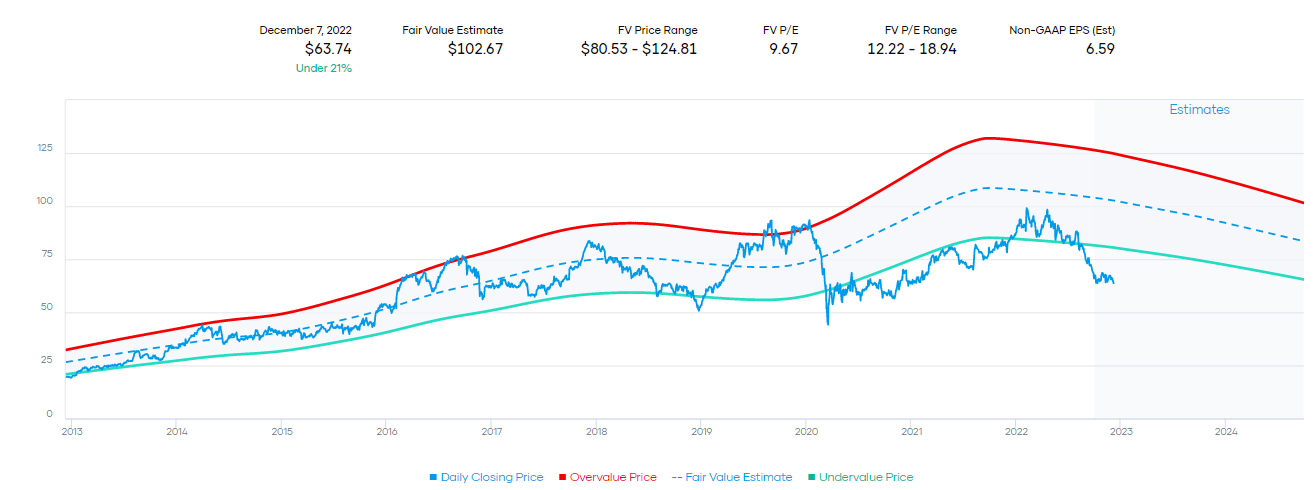

Based on the fair value estimate on a P/E basis, the stock is currently trading quite cheaply. The fair value P/E range is 12.22 to 18.94. Even in next year's slump, the forward P/E comes to 9.67. Meaning that, despite the earnings drop, the stock is still trading cheaper than its historical range by a meaningful margin.

{kind=link}

If we look at Wall Street analyst targets, they have an average price target of $78. That still suggests that there is around a 22.5% upside from here. A more aggressive price target is the fair value provided by Morningstar ( MORN ), which puts it at a hefty $102. Now that I would say it is probably a bit unrealistic. That would put it at an all-time high.

Dividend Grower

Finally, while one waits for potential upside you can be paid a healthy and growing dividend. The yield after the latest decline has now right around the 3% yield level.

{kind=link}

The dividend increases in the latest years have been a bit more tempered than previously. Still, the overall trajectory is higher dividends, which have been going on for 11 years. Additionally, with a forward payout ratio of just 30%, there is plenty of safety, in my opinion. It also leaves plenty of capacity to grow the dividend going forward for those soft earnings years.

Conclusion

TSN is a bit unusual in the consumer staples sector as it shows it can be quite cyclical in nature. However, it has proven to be a faster grower over longer periods of time. If analysts are right, assuming the continued trajectory of volatile earnings, they should be able to continue delivering faster growth going forward.

The price has slumped, and that's brought it to a better valuation, even considering the slump in earnings expected. Now would appear to be a more opportune time to consider adding TSN. On the other hand, after a stock slumps, it's generally the hardest time to find enthusiasm for shares from investors overall. This is especially true when one might need a mindset of investing for a year or two before seeing earnings growth again.

For further details see:

Tyson Foods: Getting Cheap