JBSAY - Tyson Foods: Potential Cyclical Play For Long-Term Value Investors

2023-10-11 17:42:52 ET

Summary

- Tyson's stock price has dropped by almost 50% from its highs, presenting a potential buying opportunity.

- Despite pressures from environmental activists, meat consumption in the US remains strong, benefiting Tyson's dominant market position.

- Tyson's competitors are also facing reduced profit margins, making this a common industry issue that is expected to subside in the long term.

- A margin recovery over the next few years, while the meat market cycle reverses, represents substantial upside.

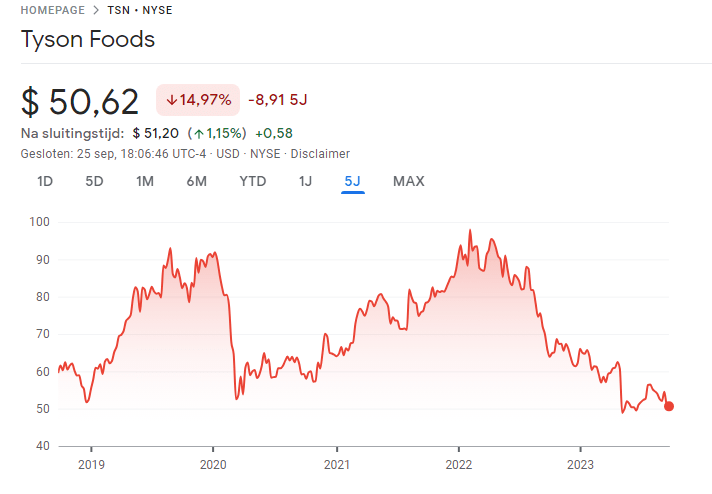

Tyson Foods ( TSN ) is the biggest protein supplier in the world by sales. The stock price dropped under 50 dollars almost 50% from its highs last year at over 90 dollars per share. The drop happened because of a cyclical downturn in the meat market that we expect to recover in the medium to long term. We therefore see this drop as a potential buying opportunity for patient value investors who are willing to play a cyclical downturn in the meat market. We rate Tyson Foods as a Buy at or below 50 USD per share.

Tyson Foods Stock Price (Google Finance, 2023)

{kind=link}

Company Overview

Tyson is a family-owned business and the biggest player in the protein business, the company has a very dominant market position as the largest supplier of protein in the US by sales. More specifically, the company achieved over 50 billion USD in sales in FY2022 and the company is in the top 10 largest consumer foods and beverages companies in the world by sales.

Tyson is primarily a US-based company; the company functions as a meat supplier to large retailers and restaurant chains, including Walmart ( WMT ), Kroger ( KR ), McDonalds ( MCD ), Wendy's, and more. International sales represent a relatively small but growing portion of revenue ( 19% at FY2022 ). As a fun sidenote: Tyson Foods also supplies meat to the US prison system.

Tyson Foods' revenue is diversified across different protein segments including beef (36% FY2022), chicken (32% FY2022), and pork (10% FY2022). If one of these segments performs poorly, the other segments can compensate for it. Moreover, Tyson Foods has its own branded prepared foods segment (18% of revenue) that enjoys much higher profit margins compared to its other segments where meats are sold as commodities with lower margins. This prepared foods segment and international sales are important focus areas for the management to spur future growth and generate higher profit margins, according to the latest earnings call.

{kind=link}

Recent and relevant developments

The big trend in food is seemingly a push towards more sustainable foods and vegetarianism. However, despite pressures from environmental activists and government over the past decade, meat consumption remains strong in the US . So meat consumption has actually increased over the past decade in the US, and people in developing economies generally start to eat more meat when they become more wealthy and prosperous over time. These environmental pressures pose a risk for Tyson Foods, but based on these findings, it seems likely that the demand for meat will remain strong in the US and even grow substantially in emerging economies in the long term.

Most importantly, the meat market is currently in a cyclical downturn since last year, due to several factors outside the control of Tyson Foods' management team. The factors include droughts, the size of cattle herds, and so on. This meat market cycle will be explained later in more detail. Importantly, however, the management went through these cycles before, and they are anticipating a recovery in the meat market. The management bought a substantial amount of stock at around 50 USD per share , which should not be followed a single indicator but is an informative and positive buy signal.

In other matters, there was a management change that was negatively received by the market. The young grandson of the family (John R. Tyson) appointed as CFO after a big scandal involving him being found drunk in someone's bed. All in all, this little incident is not as bad as some make it out to be, but this move could be seen as nepotism in the business instead of taking the best CFO available for the job. That being said, family-owned businesses do have their advantages including a more long-term perspective on the business and more stability.

Finally, Tyson seems to be planning an exit from China and Tyson has closed some inefficient chicken plants in the USA . These seem like good moves to me for reducing their exposure to China, cutting costs, and making production more efficient. However, it is not disclosed how much of their international sales came from China; they could be missing out on this large and growing market in China selling their operations there now at multi-year low prices could be a bad move.

Competitors

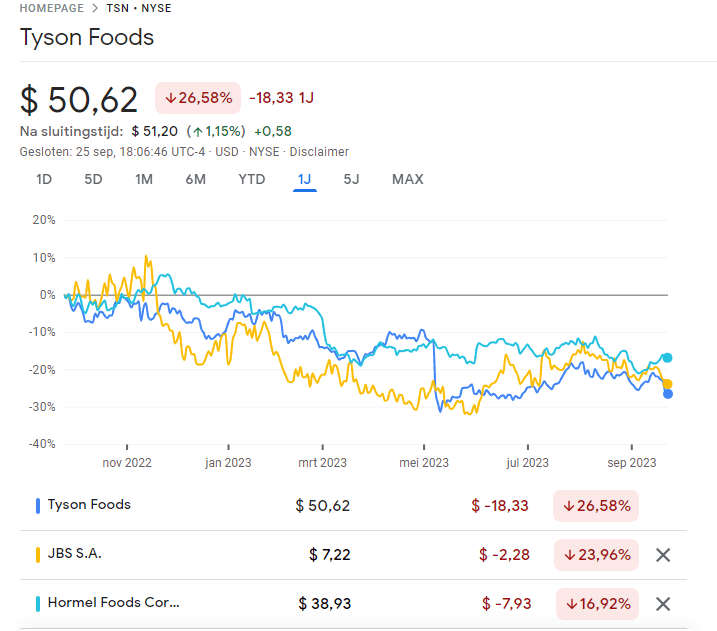

Tyson Foods Stock Price vs. Competitors (Google Finance, 2023)

{kind=link}

Tyson's main competitors: JBS, Cargill (privately owned), and Hormel are all facing the same supply chain issues and the downturn in the meat market, these businesses also suffer from reduced profit margins or are even loss-making at the moment. This data points to the fact that there is not necessarily a problem with Tyson specifically, but that the meat market as whole is in a cyclical downturn.

That being said, Hormel ( HRL ) did somewhat outperform Tyson and JBS possibly because it has a more branded portfolio of products which adds value to its products. Hormel can charge more for its branded products than generic meat products (commodities). However, Hormel's business is much smaller and achieves only a fraction (12B) of the total revenue of Tyson (50B), but Hormel surprisingly has a higher market cap at 20 billion USD versus Tyson Foods at 17 Billion USD currently. This is strange because Tyson Foods also has a prepared foods segment with similar margins that is almost the same size as Hormel in its entirety. This segment did 7.5 billion USD in revenue for the past 9 months versus 9 billion for Hormel's entire business. So, Tyson Foods' prepared foods segment alone could be worth close to the value of Hormel's entire business using the same multiples. Tyson Foods therefore plans to invest further in the prepared foods segment and this segment could become bigger than Hormel, but a lot of their meats are still sold in bulk as commodities with little to no product differentiation; with low margins but large volume.

The meat market cycle

The meat market is currently in a downturn, mostly due to lower supply of cattle that raises input costs for meat packers such as Tyson Foods and reduces their profit margins. The herds have reduced in size because of natural causes such as droughts and increased input costs for farmers such as corn prices, grain, and chicken feed. The reversal of this cycle can take a long time, some people estimate that the length of the beef cycle is 10 years. However, the length of the cycle differs between beef, chicken, and pork. Tyson Foods management can allocate resources between these segments, but all three protein segments are currently in a downturn, which is unprecedented. Some indicators point to the fact that the cycle is reversing, such as soybean and corn prices that have come down which reduces input costs for farmers.

In general, however, while timing the market is always difficult, these relatively short-term supply chain issues will most likely subside in the coming years , when herds grow back to their appropriate sizes. It takes some time to raise new animals for slaughter, but it does not take more than a year to bring a chicken from hatch to the slaughterhouse (excuse my French). Management has said in the latest earnings call that the chicken segment will be the fastest to recover because of this relatively quick production cycle, whereas beef and pork will take longer.

As often said, the best cure for high prices is high prices because farmers are more incentivized to produce and grow their herds now with higher cattle prices. In the end of this cycle, the increased supply will lower prices again. For long-term value investors with some patience and insight into these market dynamics Tyson Foods seems like a cyclical buying opportunity near the bottom of this cycle. The Q3 2023 earnings have improved sequentially from Q2 2023, which could indicate that the worst is over for Tyson Foods and they can start to recover going forward.

Additionally, during the downturn, the biggest usually get bigger while the smaller ones starve. For example, Tyson recently acquired a small sausage producer during this downturn . The management expressed confidence that Tyson will survive the downturn and emerge stronger than before, like they have done in the past through previous meat market cycles.

Financials

As a result of the downturn, profits have shrunk substantially in FY2023 and the company is currently operating around break-even, which is a big drop from FY2022 when they had net profit margins of 6%.

Financial Results (Tyson Foods, Q3 2023)

{kind=link}

Despite the recent downturn in the meat market and shrinking profit margins, Tyson still maintained its sales numbers that were about flat year-over-year. And, despite changes in profitability over the course of the cycles, Tyson has steadily grown it revenues over the past few decades as can be seen below.

The company has a strong balance sheet with low debt and a lot of tangible assets (e.g., factories, equipment etc.). The debt to equity ratio is only 50% and the company has a current ratio of 1.8. So, the company can meet its short-term debt obligations and survive a significant downturn with low profits or losses for some time if necessary, while smaller competitors may struggle.

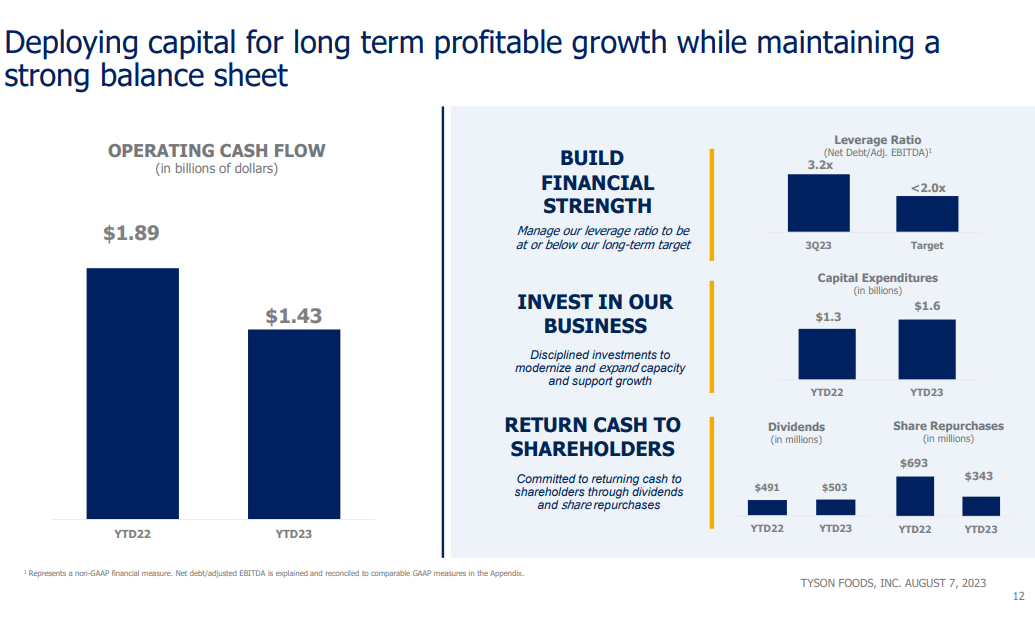

Capital allocation (Tyson Foods Q3, 2023)

{kind=link}

The company returns cash to shareholders by paying a dividend with a 4% yield currently, and they have a share buyback program to increase your stake in the business while the shares are undervalued. They maintained the dividend during the downturn, but had to borrow money to be able to pay it out which is not sustainable in the long run. However, the business expects to be profitable again in FY2024 and going forward.

Valuation

This year profit margins have severely contracted and the business operates at break-even. The business currently trades around book value (50 dollars per share), so the market is not valuing the earnings potential of this business.

We are estimating a return to historical average net profit margins of 2-5% when supply chain issues are resolved, which is a relatively conservative assumption since profit margins have been much higher than 2-5% in the past. The average between 2017 and 2022 is more like a 5-7.5% margin.

Taking care of the downside, we project net profits by estimating break-even results for FY2023 but a recovery in profit margins from 2% in 2024 to 5% in 2028 with flat sales numbers at 50 billion USD which is even below current sales. Running the numbers with flat sales and this 1% annual margin improvement, we come to a market capitalization of 27 billion in 2028 using a 10 times earnings multiple up from the 17 billion market cap from today. Discounting this future market cap five years back to today with a 10% discount rate, we come to a present value of 15.5 billion for this business compared to a current market capitalization of 17 billion, which is around fair value.

In this bearish scenario, sales are staying flat even below current levels and profit margins will not recover to what they were in the past five years. Still, this scenario does not present a large downside risk and the dividend yield at 4% will somewhat compensate a possible loss.

Projected Profits (Own Research, 2023)

{kind=link}

Taking a more bullish stance, there is substantial room for upside. Estimating margins to recover to the range of the past five years at 5-7.5% seem possible and gives a higher present value for the business. Running the same calculation going from 2% margins in 2024 to 7.5% in 2028, keeping all else equal, returns a market cap of 37.5 billion in 2028 with a 10 times P/E ratio.

Discounting this future market cap back to today at 10% returns a present value of 23.3 billion USD which represents a 35% MOS compared to the current market cap at 17 billion USD, plus a dividend yield at over 4%. Together, that is 20% dividend yield over 5 years and a 15% annual stock appreciation for the next five years. This represents a total return of over 100% in 5 years' time. This projection does not factor in any sales growth or multiple expansion beyond 10 times earnings, which is quite likely and could substantially increase the stock market performance of this business. If this margin recovery is possible over the coming years, and the company manages to increase sales like they have done in the past, then this stock could be a good buy representing enough value for a possible double in five years' time.

Finally, we estimate a more medium scenario with 5% annual sales growth and weaker margin improvement to a 5% net profit margin in 2028.

Medium Scenario Projections (Own Research, 2024)

This scenario comes to a 32 billion USD market cap in 2028 at a 10 times P/E, up substantially from 17 billion USD today. This scenario represents approximately 15% annual rate of return and a double in stock price over the next five years, plus a 4% dividend yield per year that adds up to 20% of your initial investment. The assumption of 5% annual sales growth seems reasonable because the meat market is expected to grow at over 6% annually . Moreover, a profit margin of 5% has been achieved before by Tyson Foods, margins have well above 5% even up to 7.5% over the past five years. If margins turn out to be lower, e.g., at 2-4% range, there is enough margin of safety to compensate with an estimated 15% internal rate of return.

Conclusions

The overall consumption of meat is still strong in the US and rising in emerging markets based on the actual data. Investing further in the prepared foods segment and emerging markets can improve profit margins and spur growth for Tyson Foods. There are some short-term headwinds for the company, and meat industry as whole, that I believe will subside in a couple years because these issues are mostly cyclical in nature.

The management is experienced and has been through these cycles before. Looking at the major competitors (e.g., JBS, Cargill, Pilgrim's pride) they're all suffering from the same issues with decreasing profitability as a result for FY2023. Smaller competitors or players with more debt might go out of business during the downturn but Tyson Foods will most likely emerge from the downturn stronger than before by gobbling up smaller players.

In the long term, if you don't have personal reasons for staying out of the meat business, then Tyson Foods looks like a solid cyclical play. We know that the current year will be bad, but the company will most likely survive and the stock market is too short-term oriented as always. The supply chain issues will most likely subside and the business will do fine so I believe that patience will be rewarded. We rate Tyson Foods as a buy at or below 50 USD per share.

For further details see:

Tyson Foods: Potential Cyclical Play For Long-Term Value Investors