TSN - Tyson Foods: Weak Fiscal Q4 Results Outweigh A Modest Dividend Increase

2023-11-13 12:23:06 ET

Summary

- Tyson Foods, Inc.'s stock has lost over a quarter of its value this year, and its fiscal Q4 results show weak earnings and declining revenue.

- The company's margins have been squeezed by lower chicken and pork prices and higher beef costs, leading to a significant decline in income.

- Tyson's cash flow was negative, though improving, its debt has increased, and its dividend increase may not be a prudent decision given its financial challenges.

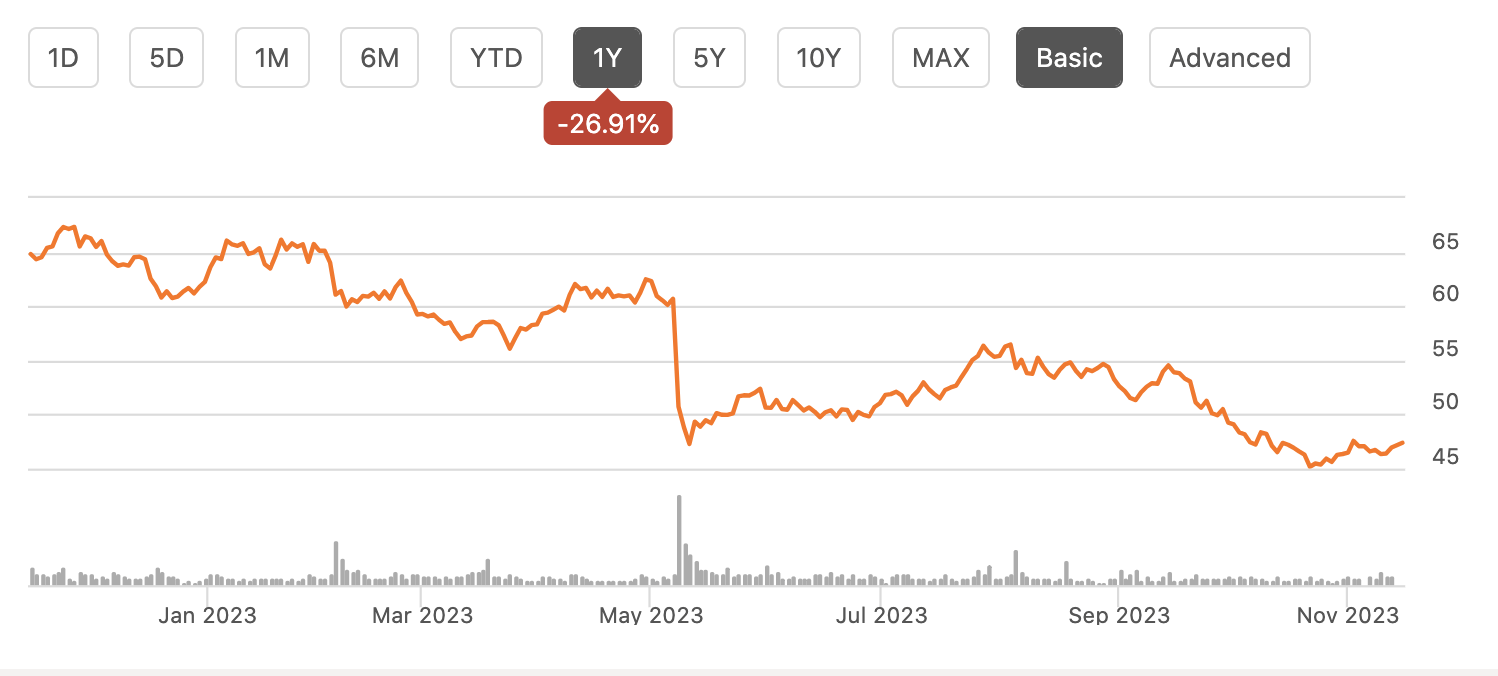

Shares of Tyson Foods, Inc. ( TSN ) have had a difficult year, losing over one quarter of their value. The stock was trading roughly unchanged on Monday, following its fiscal Q4 report . Still, results are rather weak, and given the pressures the business face, I do not see things improving for a long time. The company did raise its dividend 2% to $0.49, but given the headwinds, I am not sure this was the prudent decision. I would avoid shares.

{kind=link}

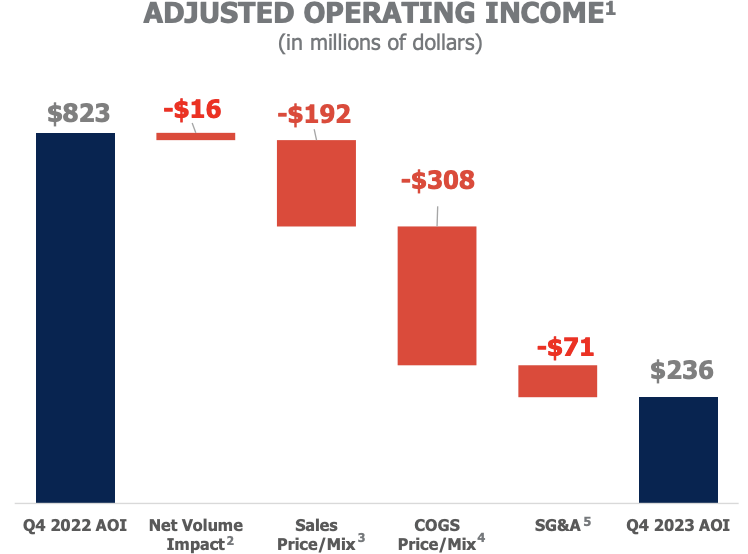

In the company’s fiscal fourth quarter , Tyson earned $0.37 in adjusted earnings, $0.12 ahead of consensus even as revenue fell by 3% to $13.4 billion. While better than estimates, earnings are still down dramatically from $1.63 last year, as the company has been hurt by lower chicken and pork prices and higher beef costs. For the full year, the company earned $1.34 from $8.73 last year. As you can see below, adjusted operating income was hit by negative variances across the board.

{kind=link}

Volumes have come down slightly as consumers are more closely monitoring their spending as inflation weighs on disposable income with meat a relatively expensive food source. Chicken prices in particular have been weak, weighing on sales prices while cattle prices have been elevated, increasing cost of goods sold. This has squeezed Tyson’s margins on both sides, resulting in the significant decline in income that we are seeing.

Drilling deeper into the results, chicken is depressed but was stronger sequentially, swinging from a $63 million loss last quarter to a $75 million profit. Volumes rose 1.7% year-over-year, but pricing was -9.2%. The unit continues to be weighed down by weak chicken commodity prices. There have been some sequential gains from operating cost improvement as TSN attempts to rationalize spending and improve efficiency given the weak pricing environment.

Beef and pork have been negatively impacted by export issues, cattle costs, and excess supply. Combined, Tyson earned just $9 million from $341 million last year on $6.5 billion in sales. That left it with just a 0.15% operating margin, functionally running at breakeven. Tyson also took a $333 million impairment on its beef segment this quarter, in recognition that these headwinds are unlikely to improve in a material way anytime soon.

For the full year, Tyson lost $77 million on chicken, made $233 million on beef, and lost $128 million on pork, making about $28 million from its commodity meat business. That is down 99% from $3.6 billion in fiscal 2022. As investors in oil & gas know, commodity businesses can be extremely cyclical with significant profitability shifts from factors largely outside of management’s direct control. That is what Tyson is experiencing now, as meat demand is relatively weak while costs remain high, reducing the spread it earns on its meat processing operations.

The one bright spot is that retail brands are performing better as Americans shift toward prepared foods (perhaps away from eating out), as they often are cheaper and of course are easier to prepare. Still, sales were down 0.6% from last year on 1% volume growth and 1.6% weaker pricing. More positively, adjusted operating income rose 3% to $151 million as margins expanded 20bp to 6%. For the full year, prepared foods earned $889 million, up nearly 14% from last year’s $782 million. Still, even here the rate of growth moderated throughout the quarter.

Because of weaker operations, Tyson burned -$187 million in free cash flow in 2023 alongside $377 million of small M&A. This free cash flow figure was also aided by $187 million of favorable working capital as inventories have come down by nearly 4%. Cap-ex spending was flat at $1.9 billion. Tyson also spent on $354 million of buybacks, which was down from $700 million last year while its dividend costs $670 million.

Because of these cash outflows, its cash on hand is $573 million from $1.03 billion a year ago. The company does have $3 billion of liquidity including its revolver. Tyson now carries $9.5 billion of debt from $8.3 billion last year

In this interest rate environment, carrying more debt is expensive. Tyson is also not doing so from an under-leveraged position. In fact, its net debt to EBITDA is at 4.1x, well above the company’s 2.0x target, due to both higher debt and cyclically depressed earnings.

Looking in isolation, this does not seem like a company that should be raising its dividend. It has burnt through cash, increased debt to twice its target, and is facing meaningful cyclical/commodity pressures that showed no sign of abating in the fourth quarter. Yes, the company has plenty of liquidity it can draw down as needed, but with rates so high, that is costly. Sometimes, I think companies can be too focused on maintaining a dividend growth “streak,” which for Tyson is 11 years . And admittedly, the $13 million increase in the dividend cost is not going to materially shift the fundamentals of its financials. Still, I do not think investors should view a dividend increase as a sign of strength.

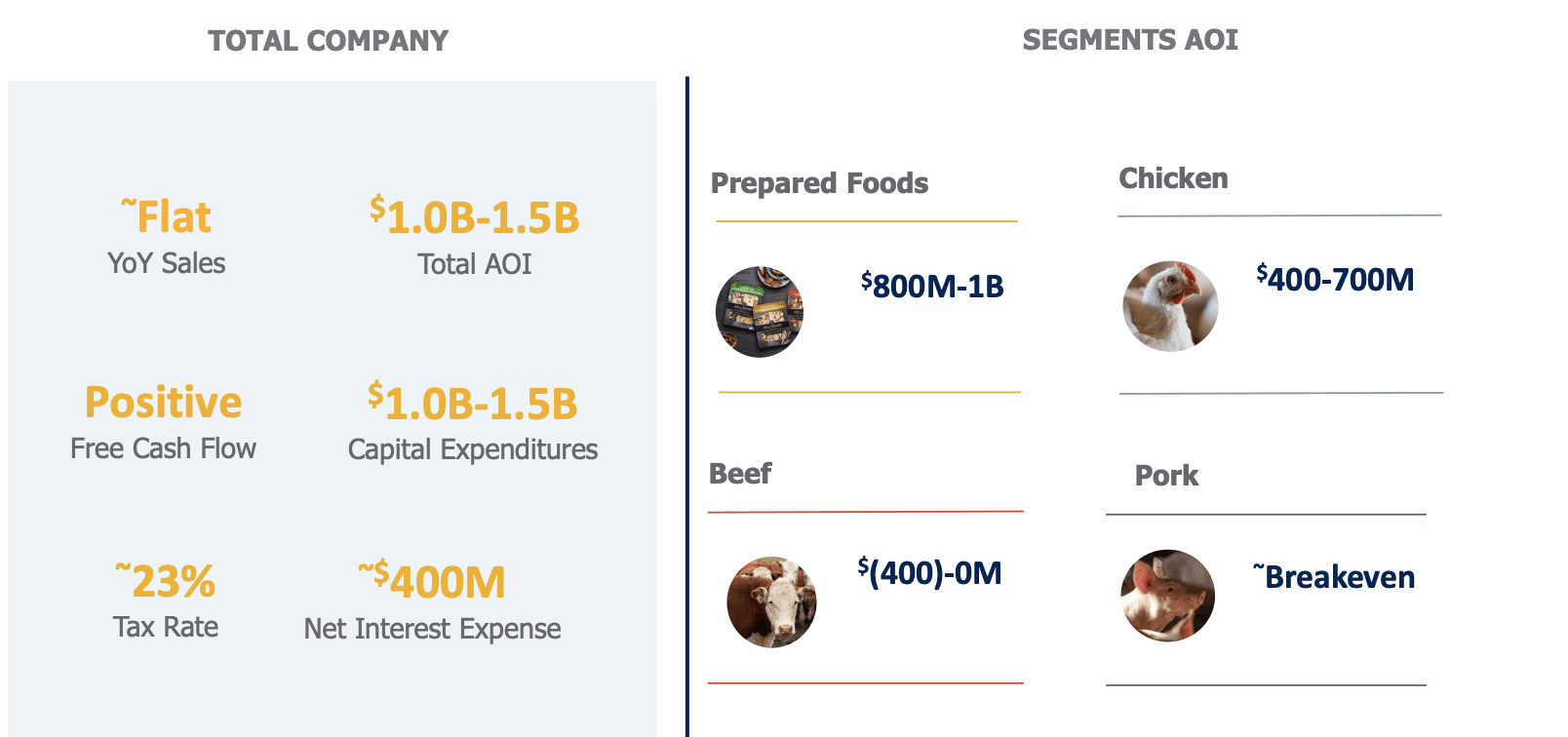

In fact, the company’s 2024 guidance is not that encouraging. It expects sales to be flat in fiscal 2024. This is based on the UDA forecast for 2024 protein production to be down with beef down 5%, pork up 2%, and chicken up slightly. Tyson sees total operating income of $1-1.5 billion. As you can see below, prepared foods will contribute similarly to this year. Chicken will continue to see sequential improvements while beef will likely deteriorate further. Management is also aggressively reducing cap-ex from the $1.9 billion spent this year.

{kind=link}

At the respective midpoints of guidance, depending on working capital, TSN should generate $500-750 million of free cash flow before dividends. That means its dividend will be just about fully covered with no remaining cash for debt reduction. That will leave leverage persistently above the company’s long-term target. Additionally, looking at macro factors, I do not see signs of significant improvement that make me believe results are on a sustained upswing or that the ~$200-400 million improvement in operating income is certain to happen.

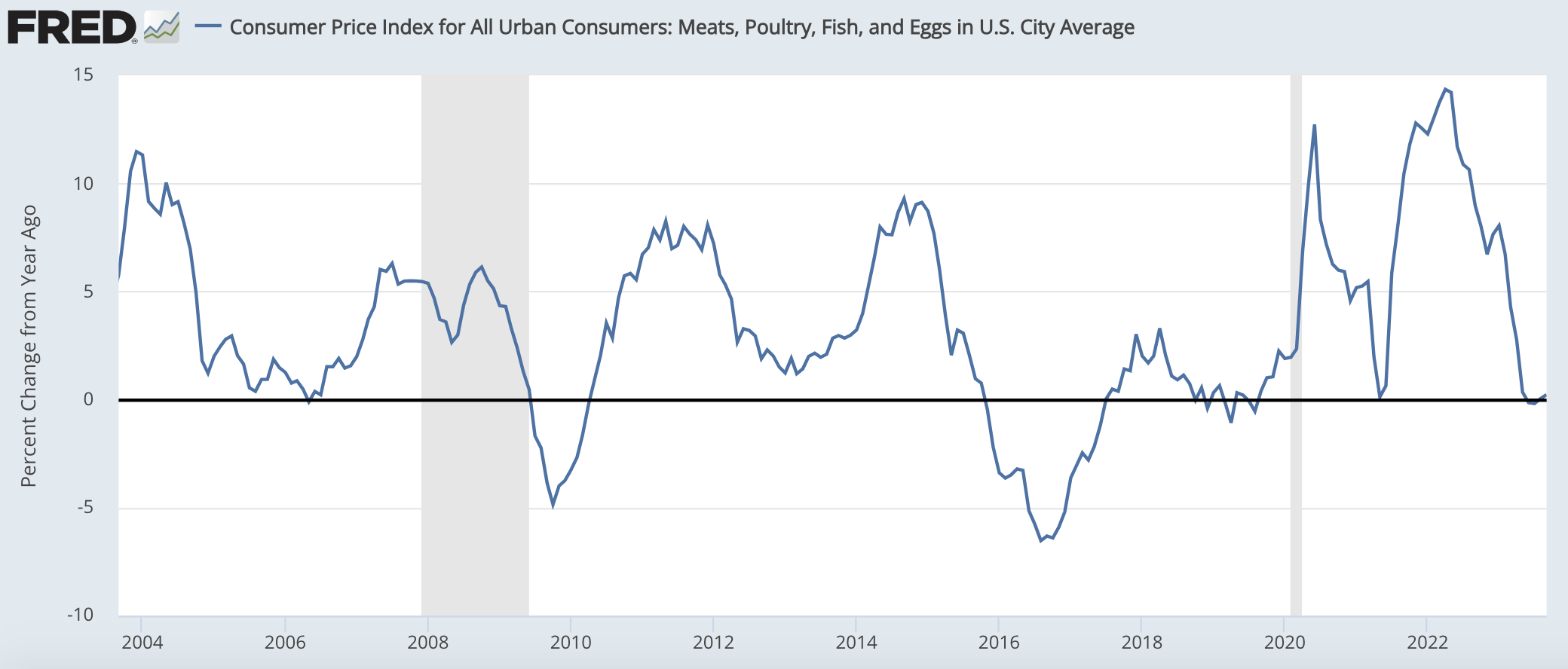

As you can see below, meat prices surged materially after COVID in two waves as supply shortages and increased at-home consumption significantly increased prices. Prices have now slowed significantly, and they are essentially unchanged with chicken being weaker than this CPI aggregation, based on Tyson’s results. This has reduced margins. Still, prices have not really retraced their COVID gains—they have just stopped rising. This creates some vulnerability should consumers face further headwinds.

{kind=link}

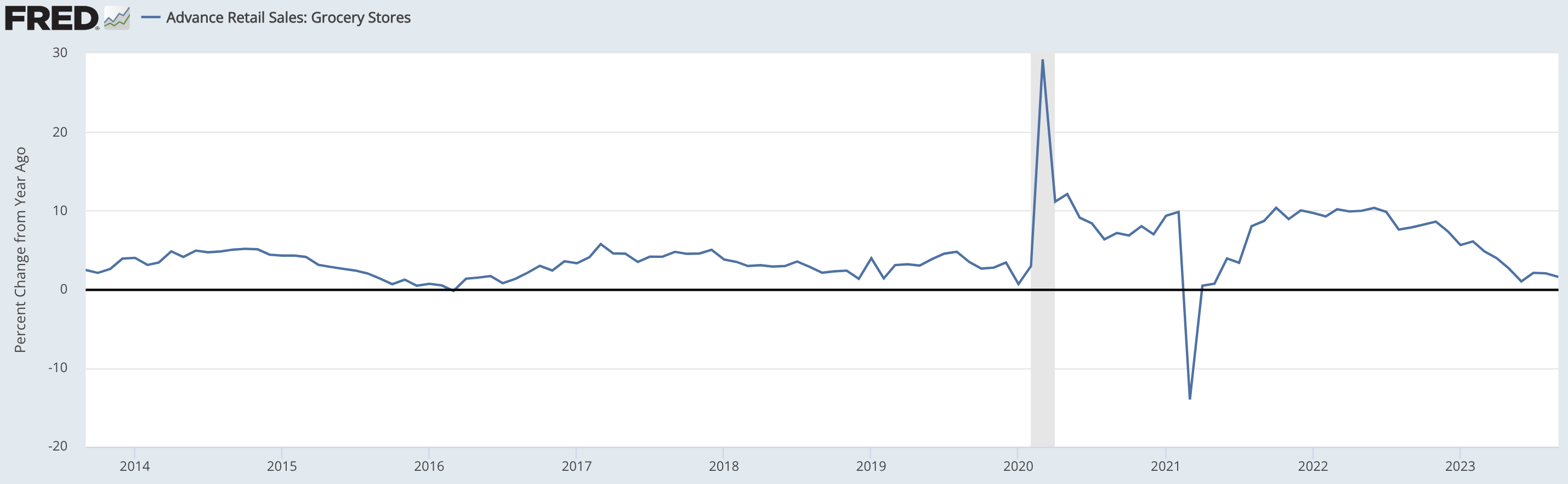

Indeed, we are seeing some signs of consumer exhaustion with spending at grocery stores steadily slowing over the past year toward the flat line. This has come as companies like McDonald’s ( MCD ) have reported solid same-store sales. Given rising food prices, some fast-food and quick-service options have become more reasonable alternatives for consumers with stretched budgets. With the Federal Reserve seeking to cool wage growth and the labor market, we should expect consumers to manage budgets tightly next year as they have this year.

{kind=link}

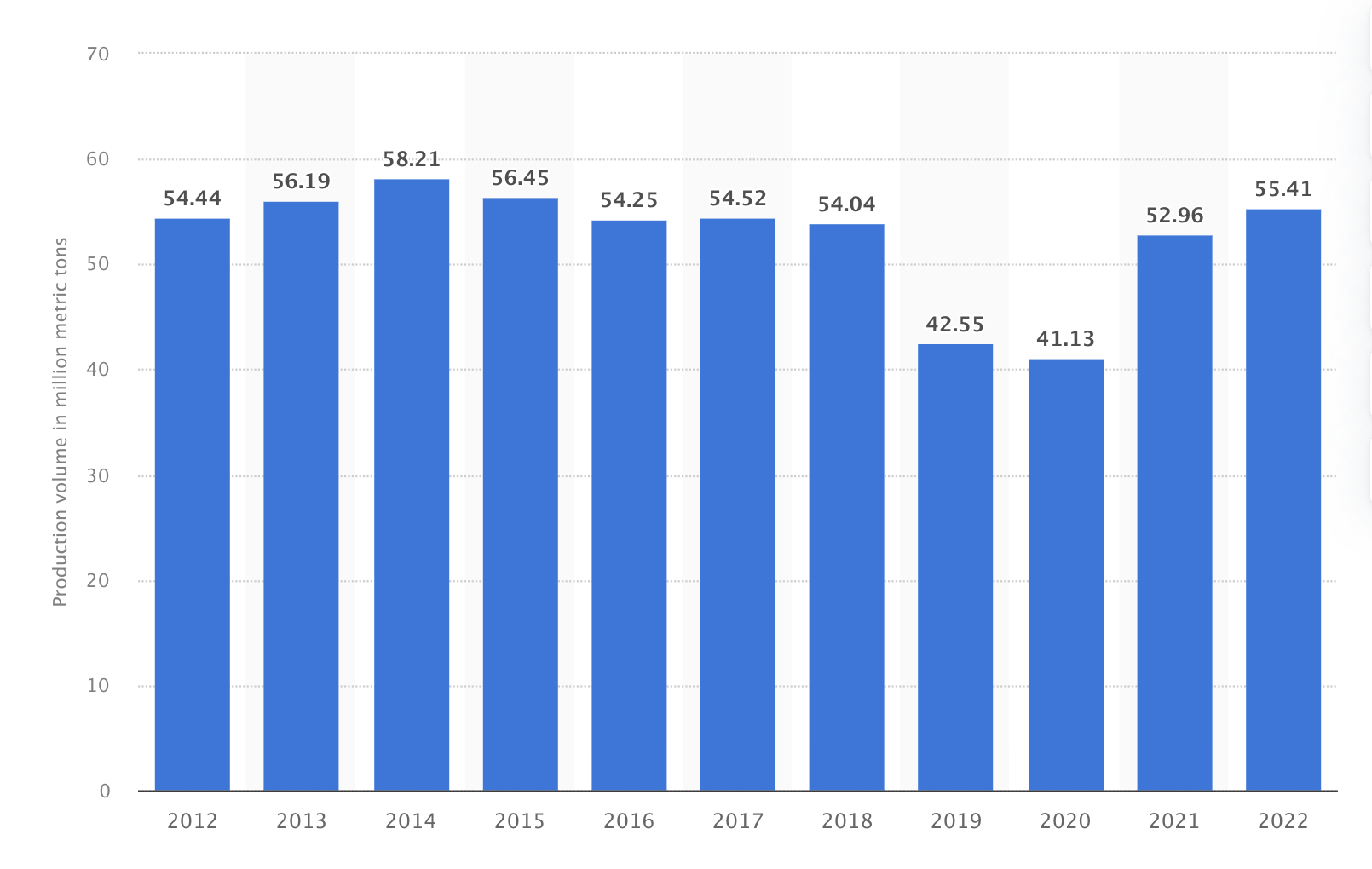

Lastly, Tyson has mentioned weakness in exports. Pork is expected to be just breakeven next year. A big reason for this is China, which consumes about 40% of all pork. When they faced the swine flu in 2029-2020, their production fell sharply, but this has sense normalized. The USDA expects Chinese pork production of about 56.5 million tons in 2023 and a 1% decline in 2024.

{kind=link}

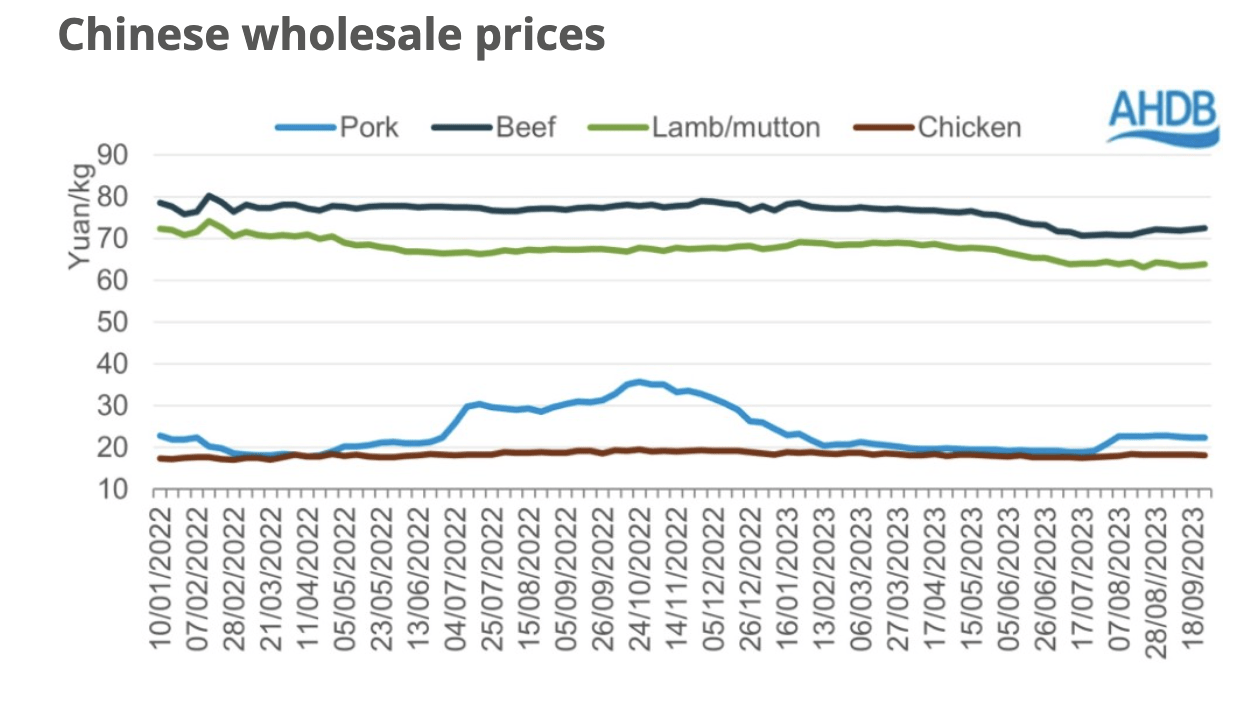

Alongside improved production, Chinese pork prices have moderated, reducing the potential spread gains by exporting to that market. With production remaining elevated relative to recent years, we should expect that trend to continue.

{kind=link}

With price-conscious consumers, relatively weak pricing, and still-elevated input costs, Tyson faces a difficult macro environment. This greatly reduced 2023 earnings power, and there is not much relief in sight in 2024. If a recession comes to pass, that will likely further reduce consumption and leave Tyson vulnerable. It is just able to cover its dividend thanks to lower capital spending, but that still leaves its balance sheet with substantial excess debt relative to target, leaving it vulnerable to higher rates.

With just a 4% free cash flow and under $2 in earnings power, shares appear expensive for a commodity company in a difficult commodity environment. I do not see upside in Tyson Foods, Inc. shares, and I believe investors should sell to rotate out of a company that is going to have headwinds for a prolonged period with a challenged balance sheet.

For further details see:

Tyson Foods: Weak Fiscal Q4 Results Outweigh A Modest Dividend Increase