VET:CC - U.S. Energy Update: A Compelling Macro Trade

Summary

- The Strategic Petroleum Reserve releases by the Biden administration are draining US inventories and artificially depressing prices.

- Domestic demand has marched steadily higher over the years.

- We could see a whiplash rebound in prices when SPR releases end in November.

The Uneconomical Seller of Oil

Last November, President Biden announced the first release of oil from the SPR (Strategic Petroleum Reserve). On the date that 50 million barrel release was announced, WTI oil was trading around $78 per barrel. As anyone who follows the oil market knows, that release was relatively ineffective.

Following the spike in oil prices post the Russian invasion of Ukraine and the subsequent political pressure of gasoline prices exceeding $5/gallon, on April 1st of this year, Biden announced a further 180 million barrel release to be conducted at a pace of 1 million barrels per day. In the context of ~100 million barrels produced worldwide every day, these 1 million barrels might not sound like a lot.

Again, for anyone who follows commodities knows, pricing is set at the margin and an extra million barrels of supply per day for that period of time can have quite a temporary impact. In this case, coupled with a recovery of production in Libya and some demand destruction in China, this release has helped lower oil prices from a peak of about $120/barrel to today's price of about $85. With the last release set to finish in late October, Biden added another 10 million barrels for November, likely just enough to cover the midterm elections (quite a coincidence!).

Judging by volumes of WTI oil futures volumes and the volume of SPR weekly releases, the US government appears to have been the main seller of oil in recent months. Keep in mind that the administ announced this release in April with a set amount over a set amount of time with no guiderails on pricing. By its very nature then, this release is uneconomical. In fact it in intended to sell oil at ever lower prices.

I have argued many times in many different places that I believe shares of oil and gas companies tend to trade on the spot price of oil. Consequently, I believe these lower WTI prices have driven down or at least capped the shares of many energy companies.

The New Supply-Demand Imbalance

Having such a large and uneconomical seller in the market has had two major impacts other than oil prices and lower share prices.

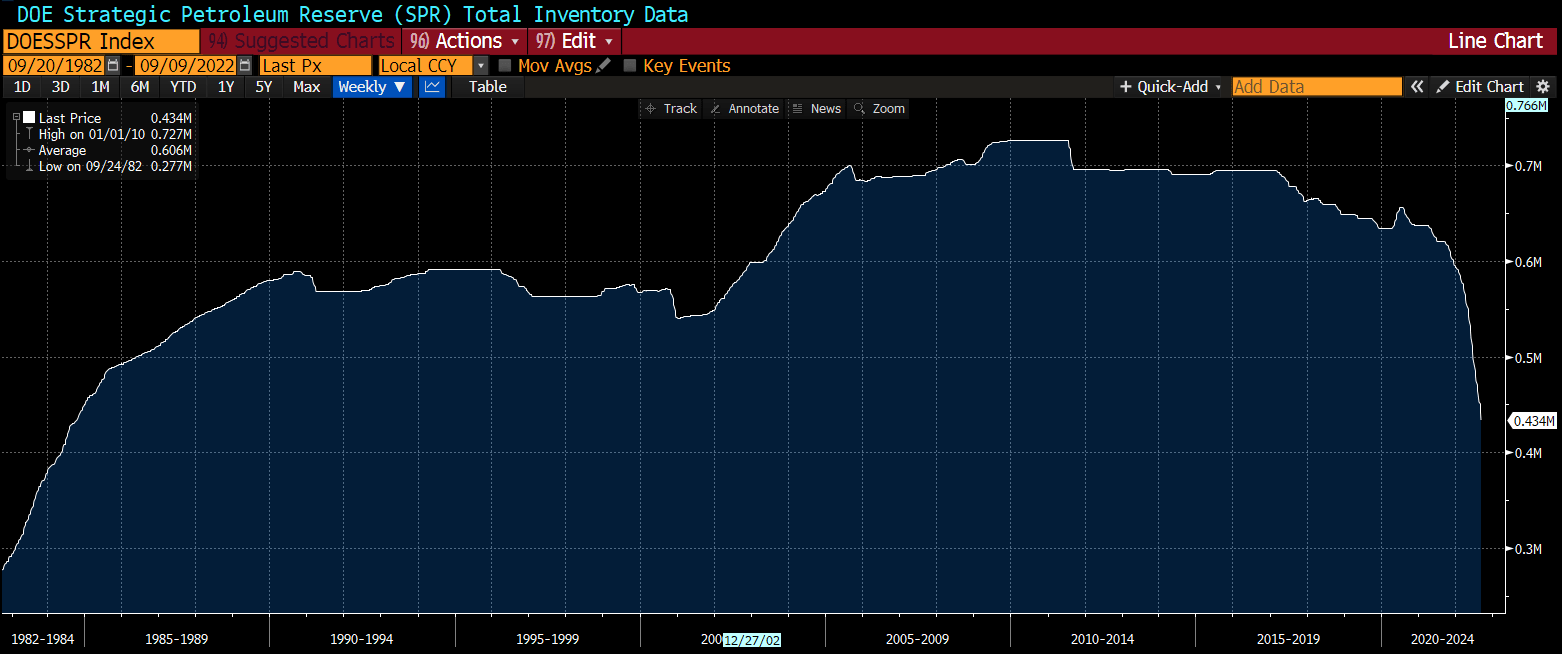

This first is it has left the SPR at its lowest level since around the time Ronald Reagan won the most lopsided reelection in history in 1984. An additional 35 million barrel release will take us even farther back in time.

In a world where energy security is economic and military security, I consider this lower reserve a pretty scary situation. The SPR was meant to supply the country with oil in case of a supply interruption, not to (in my opinion) score political points ahead of an election. The US will eventually have to refill this inventory and most likely sooner rather than later.

DOE Strategic Petroleum Reserve (in millions of barrels) (Bloomberg)

{kind=link}

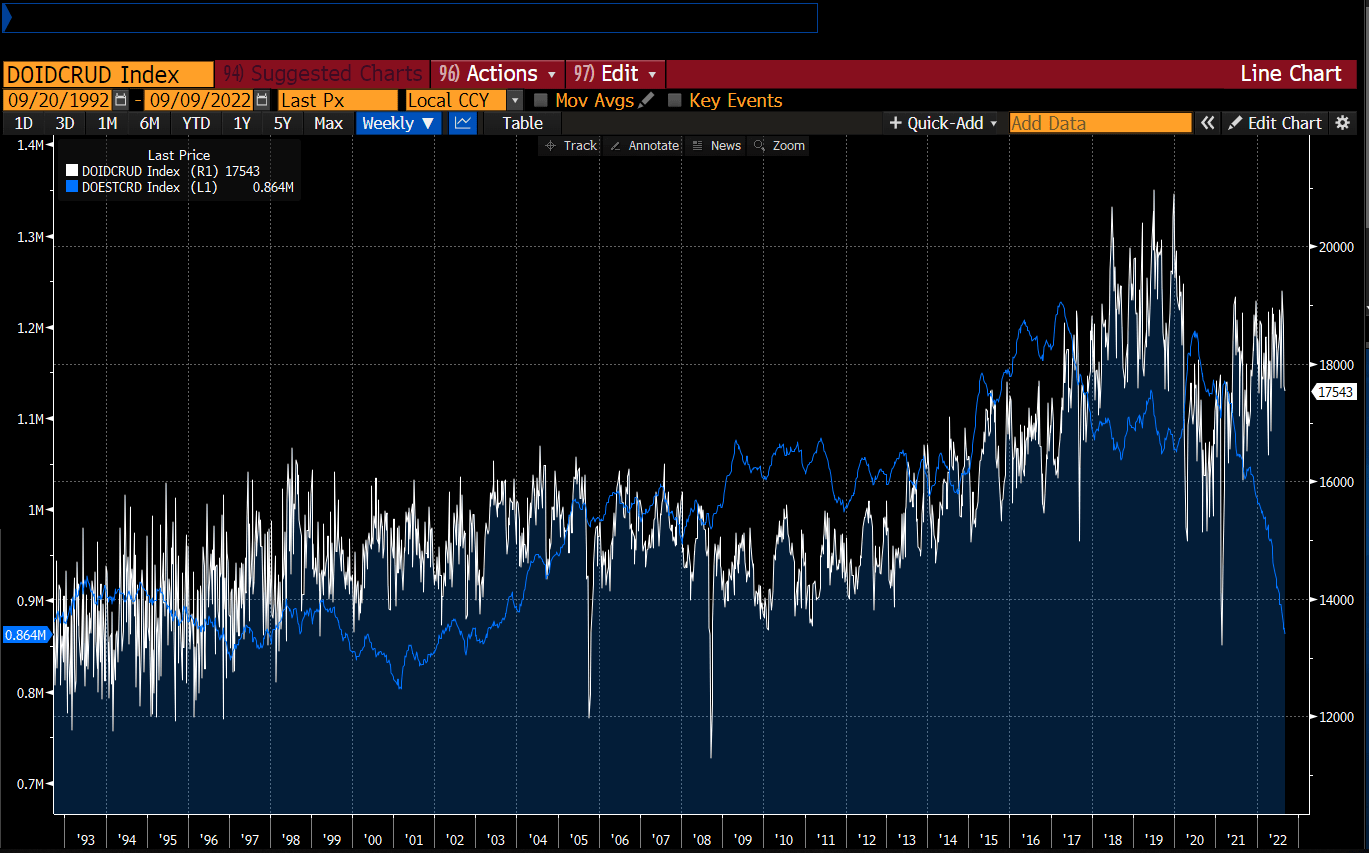

The second and perhaps more pertinent dynamic to energy investors is a massive supply/demand imbalance that is unprecedented over the past 30 years.

The graph below shows US oil demand (in white) versus total US crude oil inventories including the SPR as measured by the Department of Energy (in blue). As you can see the period when demand has exceeded inventory by large amounts has generally correlated to healthy oil prices. As you can also see, while US demand plummeted during covid and has yet to regain the pre-covid high, we have never seen such a wide gulf of demand versus inventory in the past 30 years. Unless there is a major spike in production anywhere in the world, which I don't expect based on current drilling, I don't see how such a supply demand imbalance does not lead to higher prices once the SPR releases are done.

US daily oil demand versus US total inventory including SPR (Bloomberg)

{kind=link}

How to Play It

As I have written fairly consistently over the past year and reiterated last month , the bulk of my favorite plays largely have been in the natural gas production and midstream space. They include Chesapeake ( CHK ), Crestwood ( CEQP ), Enterprise Products ( EPD ), and EQT ( EQT ). Natural gas inventories remain in a great spot so I continue to like all of those companies. I will write a follow up article more focused on natural gas.

More oily plays that I wrote up include California Resources ( CRC ), Equinor ( EQNR ), and Vermilion ( VET ). One could also add plays in small companies like SM Energy ( SM ) and larger ones like Occidental Petroleum ( OXY ) which have the optionality of potential buyouts, the former by a strategic and the latter by Berkshire Hathaway (BRK.A) ( BRK.B ) which has been steadily acquiring shares.

One could also just play the pure commodity. Given we know the SPR release will end around the midterm elections, one could structure an options trade in the oil ETF ( USO ) where you buy November calls and sell October calls. The premium outlay is less that way and you are long once the uneconomical selling from the SPR is over. One could also just buy the energy ETF ( XLE ) which is largely affected by Exxon ( XOM ) and Chevron ( CVX ) although I consider that a much more hamfisted trade.

Risks

Any time you're dealing with a commodity, particularly one as volatile and geopolitically as well as economically sensitive as oil there are many potential risks, too many to list here. I do believe, however, that current pricing is being impacted by an absolutely massive seller that is artificially depressing the current price and creating a very large supply/demand imbalance, which ultimately should mitigate any intermediate term risks. That said, a number of factors could impact price from the short to the long term.

Conclusion

Hopefully, I have laid out a reasonable rationale for my bullish call on oil. To be clear, I am not traditionally an oil or a macro trader. This situation is unique. I think it has created a dynamic that is fairly obvious and compelling. Given the timelines, one can play it in options land with defined risk and extremely compelling reward.

For further details see:

U.S. Energy Update: A Compelling Macro Trade