RYDAF - U.S. Oil And Gas Echoes Macro And Geopolitical Environment (Video)

2023-10-24 05:35:00 ET

Summary

- Geopolitical events are ramping up volatility and uncertainty in global economies.

- Energy trade relationships could be altered once again, but North America oil and gas has very good tailwinds. While other relationships appear to fray, new developments offer opportunity.

- In light of geopolitical events, consolidation and scale in the oil and gas industry, as seen in recent mega deals, are viewed positively.

- While crises continue, the U.S. energy industry offers a relatively stable investment thesis. It's not their first rodeo.

- Interest rate lag effects are still in the works.

(Note: Having recently presented work about energy and geopolitics at the University of Montana and World Affairs Council. In a related video, Editor Michael Hopkins interviews me for a download about the recent work in energy, geopolitics and recent mega deals.)

The most unfortunate threats to global economies are the volatility and instability wrought by the recent attack on Oct. 7 of Israel. We were already troubled by the Russia invasion of Ukraine. There has subsequently been a re-working of energy trade routes with both oil and natural gas. With the trouble in the Middle East, energy trade relationships could alter courses again.

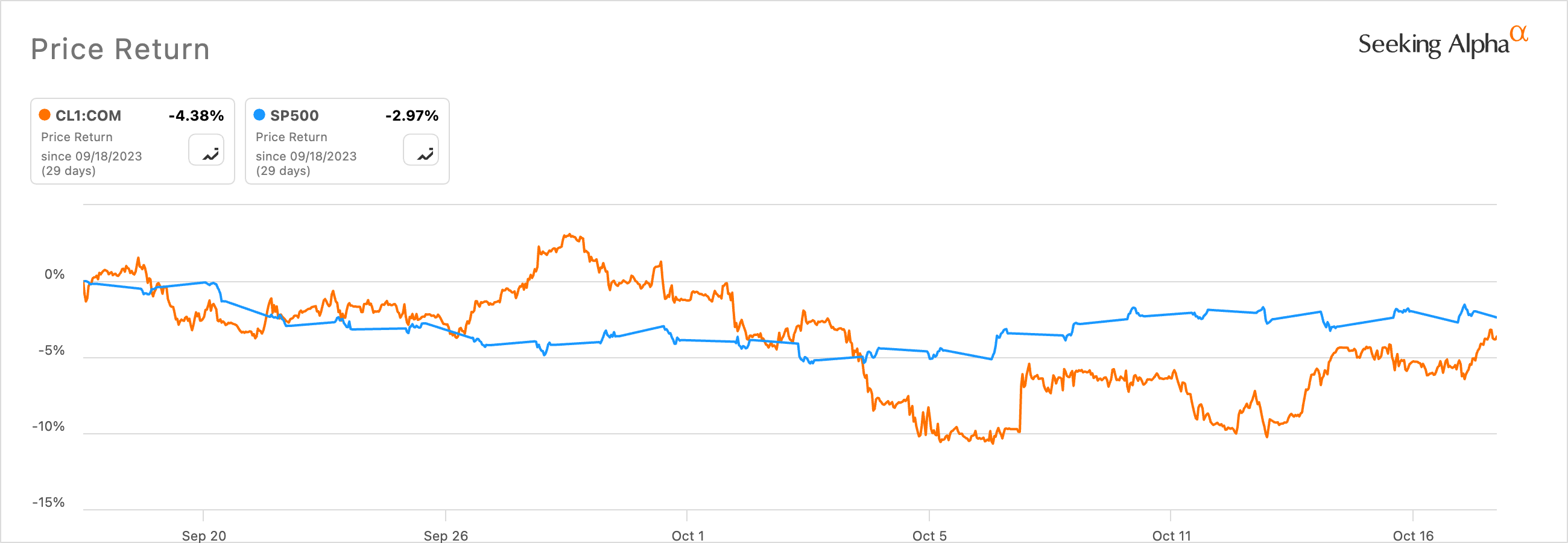

{kind=link}

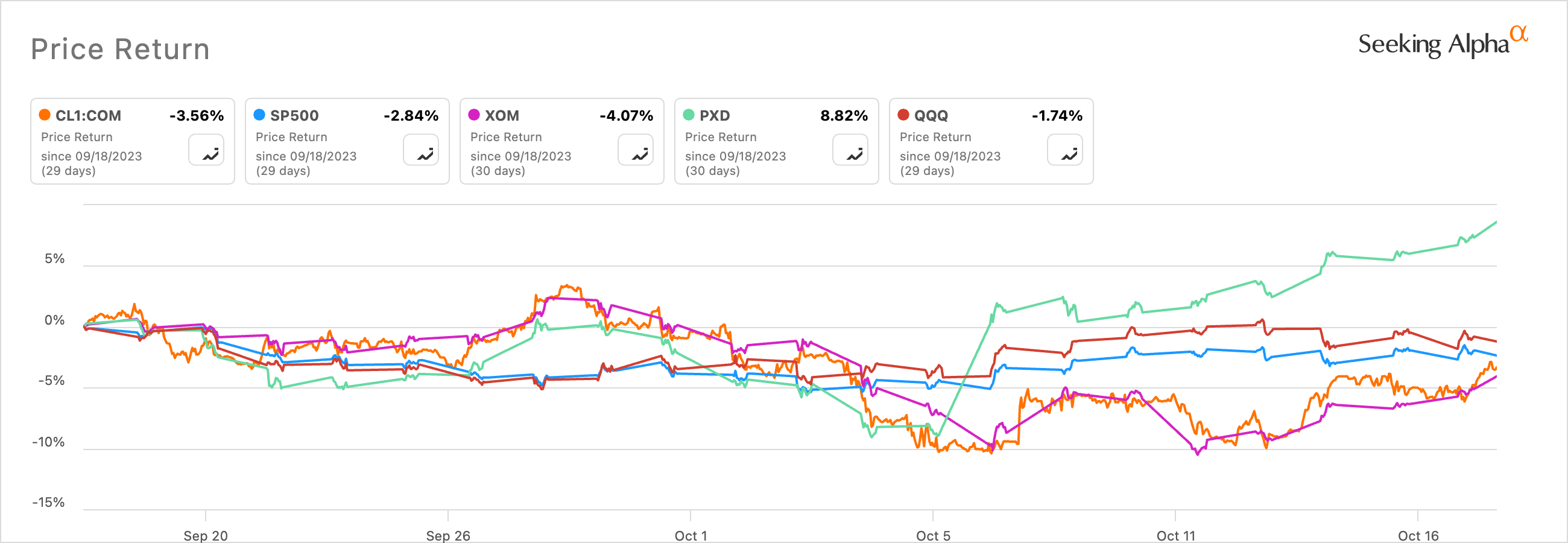

Oil and the S&P (Seeking Alpha)

Global energy

The centers of geopolitical gravity of late have been the Middle East and Russia. Notably, in a recent U.S-EU energy webinar , a NATO leader spoke of how U.S. LNG has increased 70% in Europe. Norway has stepped up and now comprises 30% of European gas, like 115 bcm. He expects energy price volatility for a decade.

With respect to the Middle East, where I have spent much of my bandwidth assessing and the majority of my time from Oct. 4 to now even — of course, oil prices have risen to reflect a risk premium. Just like what happened with Russia last year, markets start to settle once specific events and their direction are more apparent. But we have groups willing to incite scorched earth policies and events. Eventually, this will have repercussions in another form, whether it be domestic political instability or being out of favor with investors as an investment destination.

In both cases, alternative sources of gas and oil have been found by market participants. The U.S. is a significant player as a source of global oil and gas supply in Asia, and more so in Europe than previously.

Also, in Europe, from a NATO perspective, they continue with sustainable sourcing of energy such as alternative fuels, microgrids, storage — more home-grown solutions. In Montana, on a panel and conversation with a former Governor of Montana, we talked about various forms of storage and energy. Energy storage is becoming an increasingly interesting space in which new ventures and acquisitions will be happening. All of the majors such as Exxon Mobil ( XOM ) and Chevron ( CVX ) are investing to make sure they can play in emerging energy spaces of the future.

( Link to video interview about energy, macro outlook and geopolitics.)

Given the events of the day, oil and gas markets and the energy transition have changing investment implications. Interest rate increases are a driver in ways we are just starting to see, especially with renewables and EVs. Higher rates shift decision making. This idea was echoed by the CEO of AT&T, who l listened to at the economist conference I attended just before Montana. Regarding “transition” type investments, I would focus more on needs-based investments. The Inflation Reduction Act legislation is a real mixed bag on its incentives, distortions and ultimate effects, and thus capital signals.

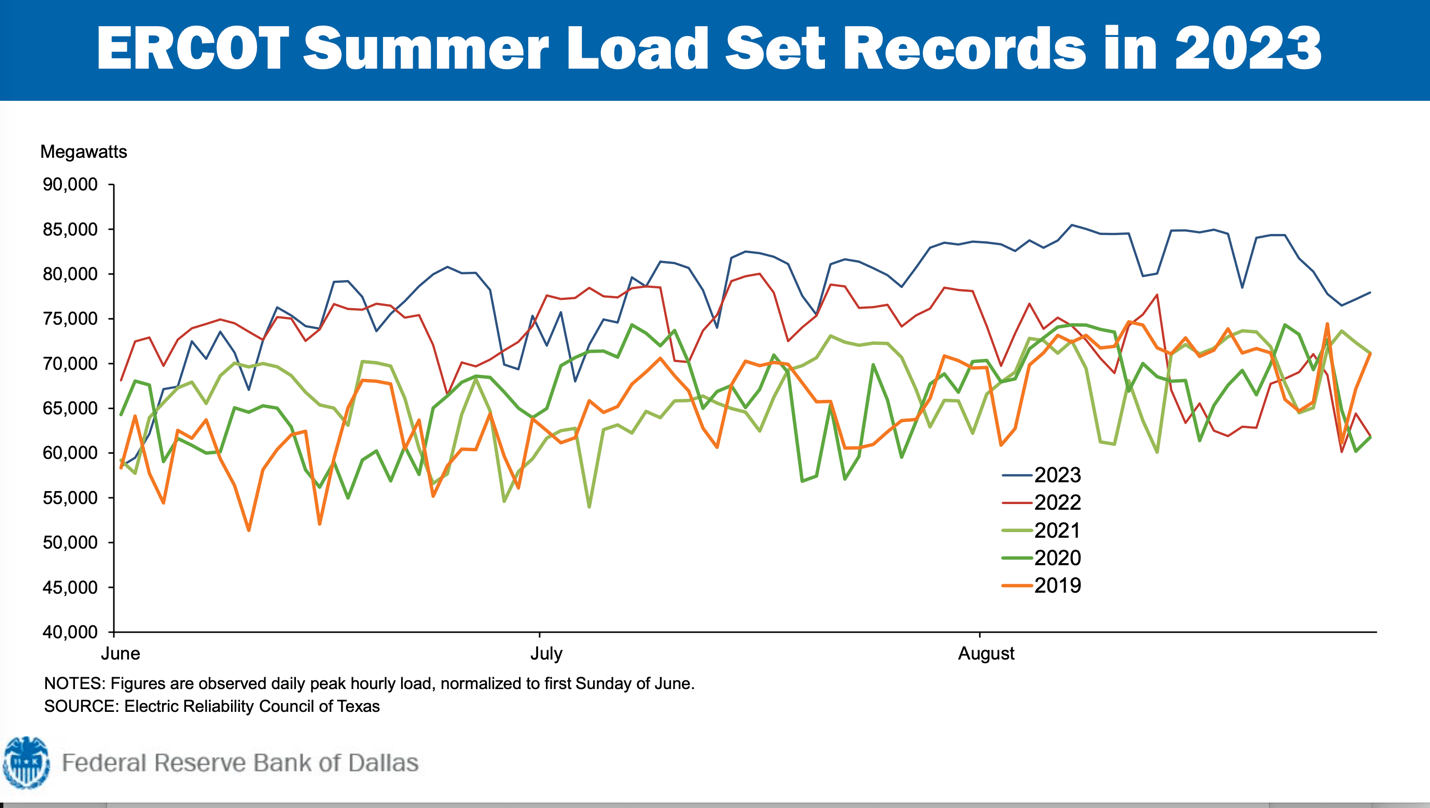

In the end, oil is fungible and a most-traded commodity. In advanced economies, electrification is becoming potentially more inflationary with all of the factors of green, as witnessed in Europe. Many countries in Europe are rolling back their initial plans to some degree, but not entirely either. Power generation grows in the rest of the world. From a recent Texas-focused energy conference at Texas Tech University on Oct. 20, unique demand centers are emerging in the tech space that can offset the supply-demand mismatches that are occurring. My 2023 theme of resource and capital efficiency is playing out in a big way in Texas, owing to its decentralized market.

{kind=link}

Texas' ERCOT Summer Load (Dallas Fed, 2023)

The natural gas trade is shifting around the globe, as alluded to in the " Solving Europe's Energy Crisis " work. The U.S. is a low-cost producer in oil and gas and a reliable partner. We're a global benchmark as I noted in the past, and in my Montana presentation (roughly half way through).

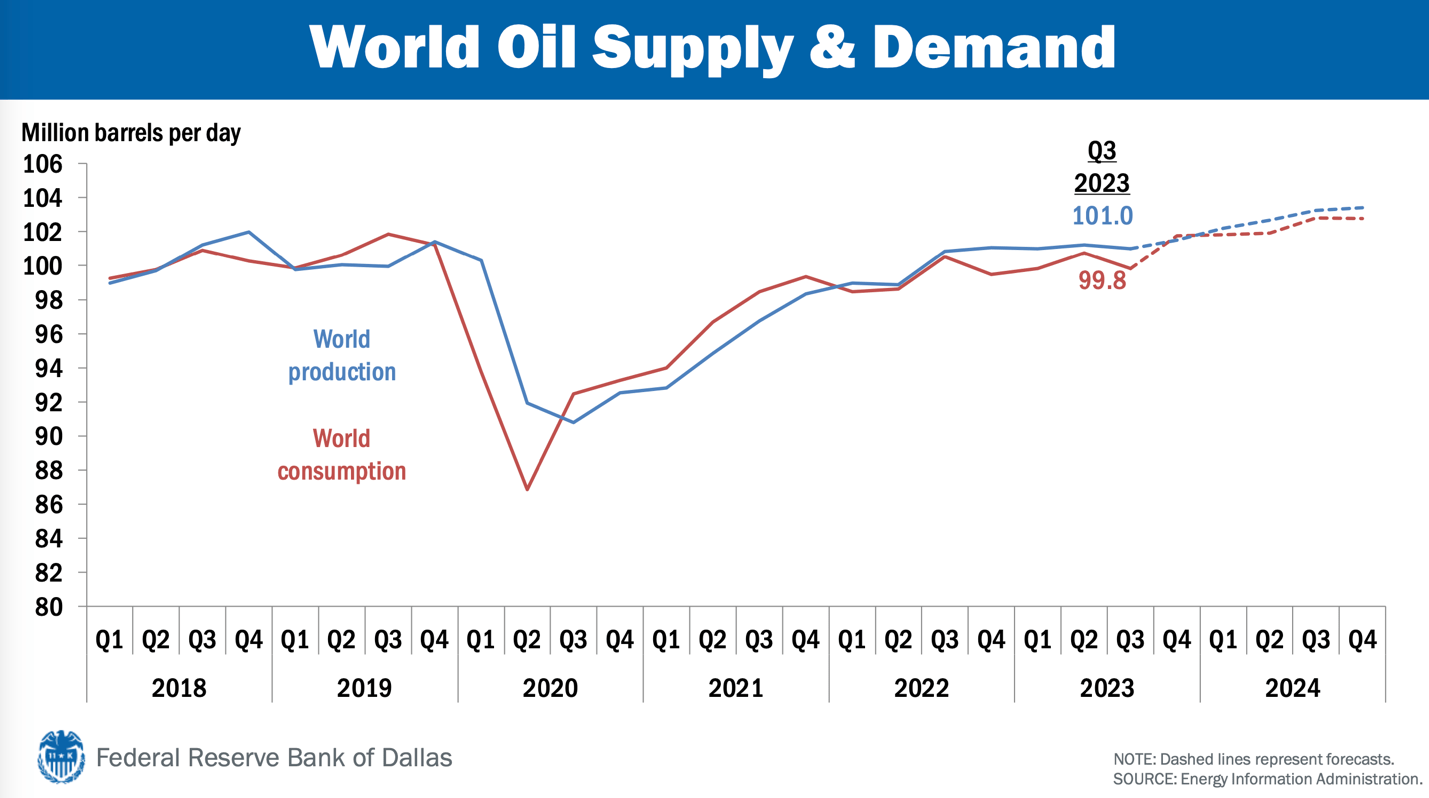

Oil prices will remain higher with tight supplies occurring to the year end. U.S. producers are expected to respond, but this is still a capital discipline regime by oil and gas firms. It seems that natural gas prices in the U.S. will stay on the lower side. Importantly, U.S. production is a player on the global stage, with new avenues emerging as geopolitics shift thinking and strategies.

{kind=link}

World Oil Supply (Dallas Fed, 2023)

(Link to page on benchmark thoughts.)

A little color follows:

In recent news , West Texas Intermediate, or WTI, a key U.S. oil price benchmark, is now to be folded into the global benchmark Brent, alongside its other constituents.

After years of wrangling, the world’s most important oil price is about to be transformed for good, allowing crude supplies from west Texas to help determine the price of millions of barrels a day of petroleum transactions.

The shift is because the existing benchmark, Dated Brent, is slowly running out of tradable oil for it to remain reliable. As such, its publisher S&P Global Commodity Insights — better known by traders as Platts — has been forced to make a dramatic overhaul.

…Dated, as it’s commonly known by oil traders, helps to set the price of about two-thirds of the world’s oil and even defines the price of some gas deals.

{kind=link}

A benchmark (Concept Elemental, Jennifer Warren)

In the past, I have written extensively about Pioneer, the Permian, and more recently about the Exxon acquisition. The market’s reception is quite significant and positively viewed. Given the events of the last couple of weeks in geopolitics, it's all the more positive that consolidation and scale occur in parts of the industry. In my article from April, where the acquisition idea was floated, much is covered. (First Pioneer-Exxon (XOM) (PXD) potential tie-up article).

With the Chevron-Hess (CVX) (HES) announcement, the continuing consolidation in the industry indicates the ideas of scale and efficiency; this was discussed and analyzed more in-depth since the first quarter of 2023. The news of Devon ( DVN ) possibly looking to acquire Marathon Oil ( MRO ) speaks to this continued theme.

{kind=link}

Energy, Tech and Mega Deals (Seeking Alpha)

{kind=link}

Exxon, Pioneer and Markets (Seeking Alpha)

Macro Points of View

At the National Association of Business Economists conference Oct. 9-10, a few takeaways stand out. One of the sessions I attended focused on the macro environment, with attention to rising long-term yields. This Wall Street Journal article speaks to the idea.

“What Wall Street thinks is going on”

Dallas Fed President Lorie Logan recently suggested that signals from term premium models made her less inclined to raise rates again this year, arguing that rising term premiums, if real, would mean that surging yields aren’t just reflecting stronger growth and a need for tighter monetary policies. — quote from WSJ

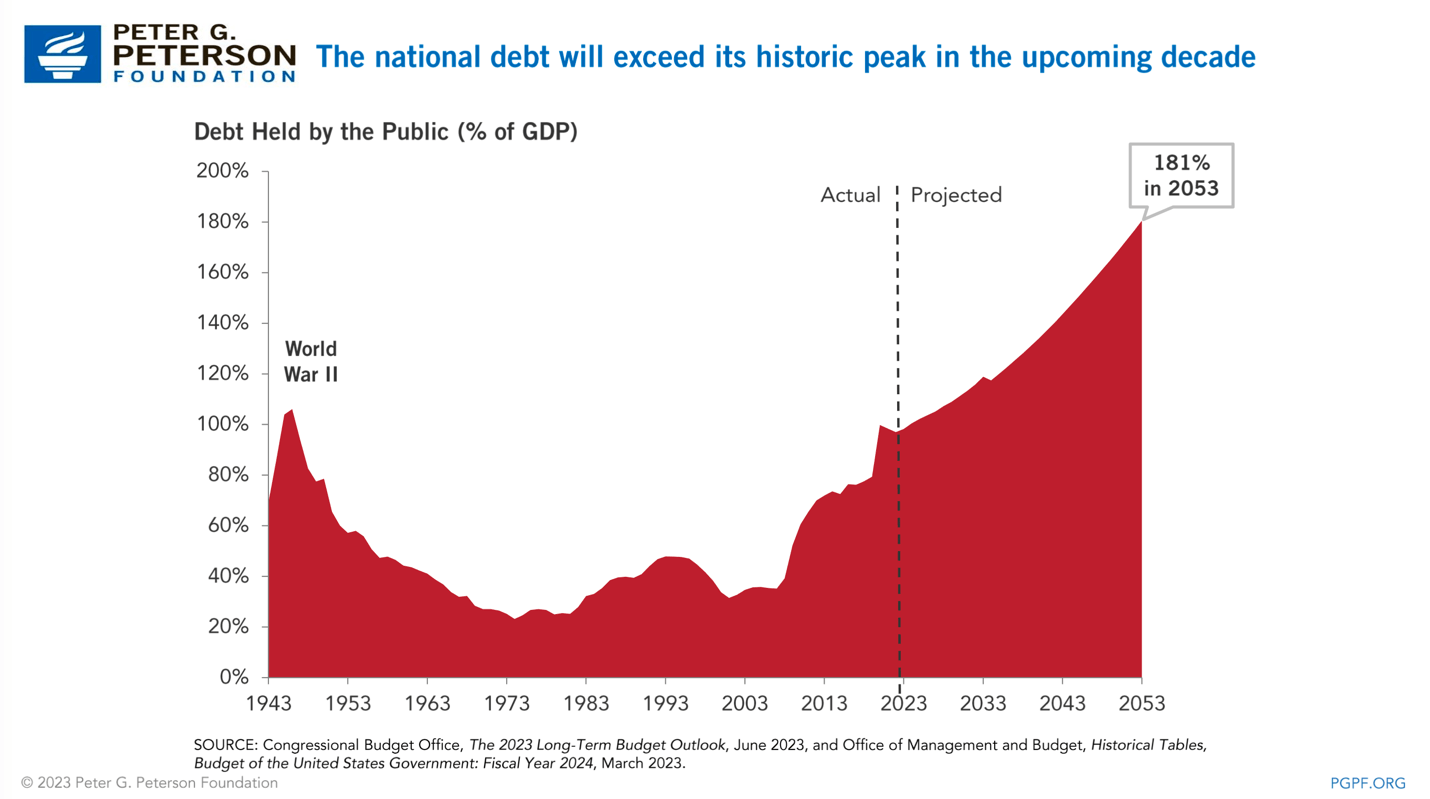

Logan didn’t delve deeply into what specifically is driving up term premiums. But on Wall Street, many have used term premium models to buttress arguments that yields have been rising largely thanks to a growing federal budget deficit.

{kind=link}

U.S. Debt (Peterson Foundation)

However, being in the room on Oct. 9, my notes say:

Economic actors are influencing the premium rather than just interest rates increases. This means the economic circumstances may do the work for the Fed and they need not raise. But overall the idea was that restrictive monetary conditions would be here for a while. And we have not seen the lag effects of policy, only the beginnings.

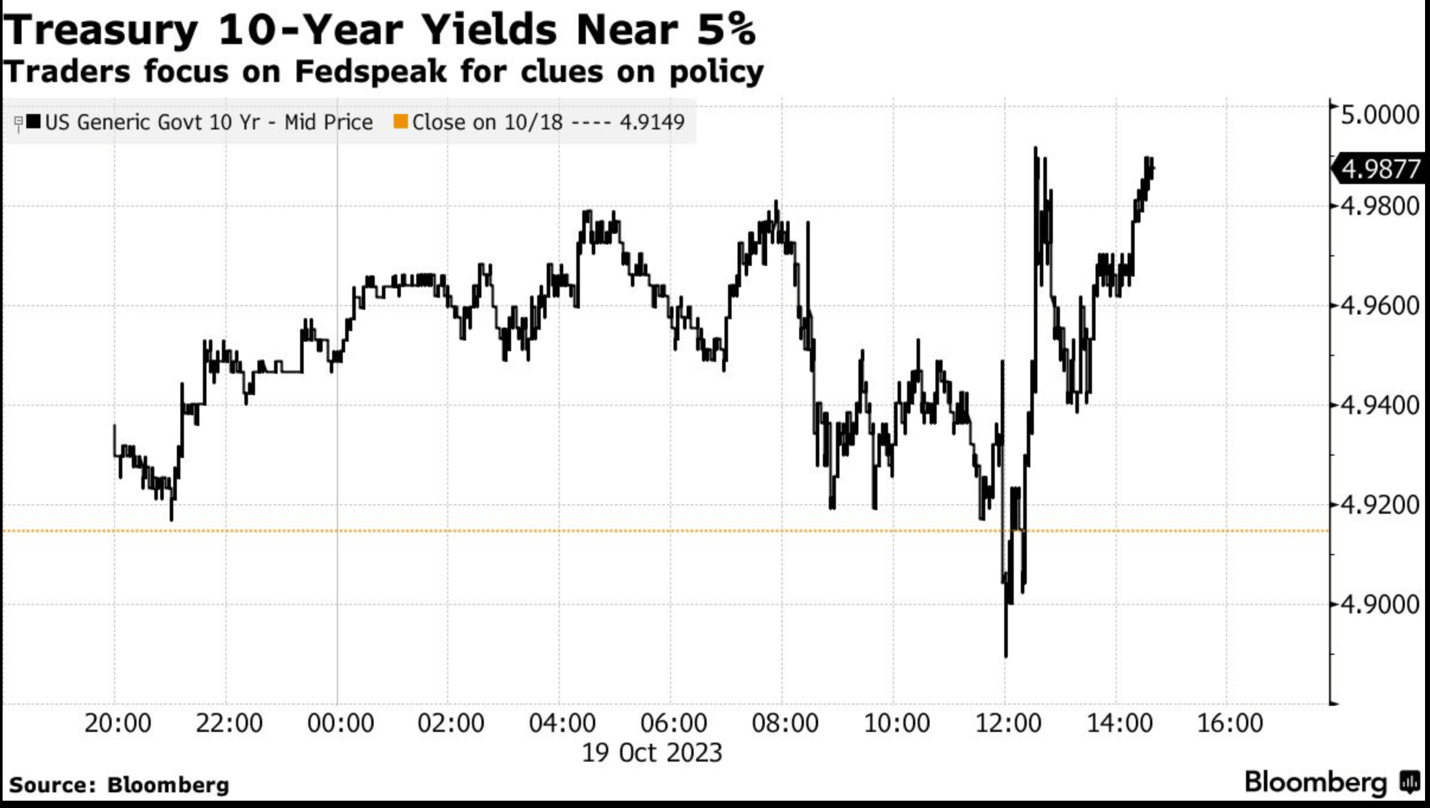

Pressure is stemming from long-term yields. Where the pressures are coming from determine the direction of interest rates changes, whether up or down. Logan mentioned that half of the long-dated yields is from the term premium.

{kind=link}

Long-term treasuries (Bloomberg, Oct 2023)

Then the 19 th , Fed Chairman Powell spoke , echoing what Logan had said:

“Powell said that, at the margin, higher long-term yields could mean less need for the Fed to hike. Yet he also said policymakers will let the rise in yields play out and watch it. He gave a number of explanations for the rise, including higher government budget deficits, which he stressed are on an “unsustainable” path…While there’s been progress, Powell said inflation is still too high and it’s too soon to be confident it’s returning to the Fed’s 2% target. The economy has surprised on the upside this year, Powell pointed out.”

On the global macro side, Logan mentioned slowing global growth in the second and third quarter. China’s structural issues influence this but also near-shoring trends are influencing global trade flows.

{kind=link}

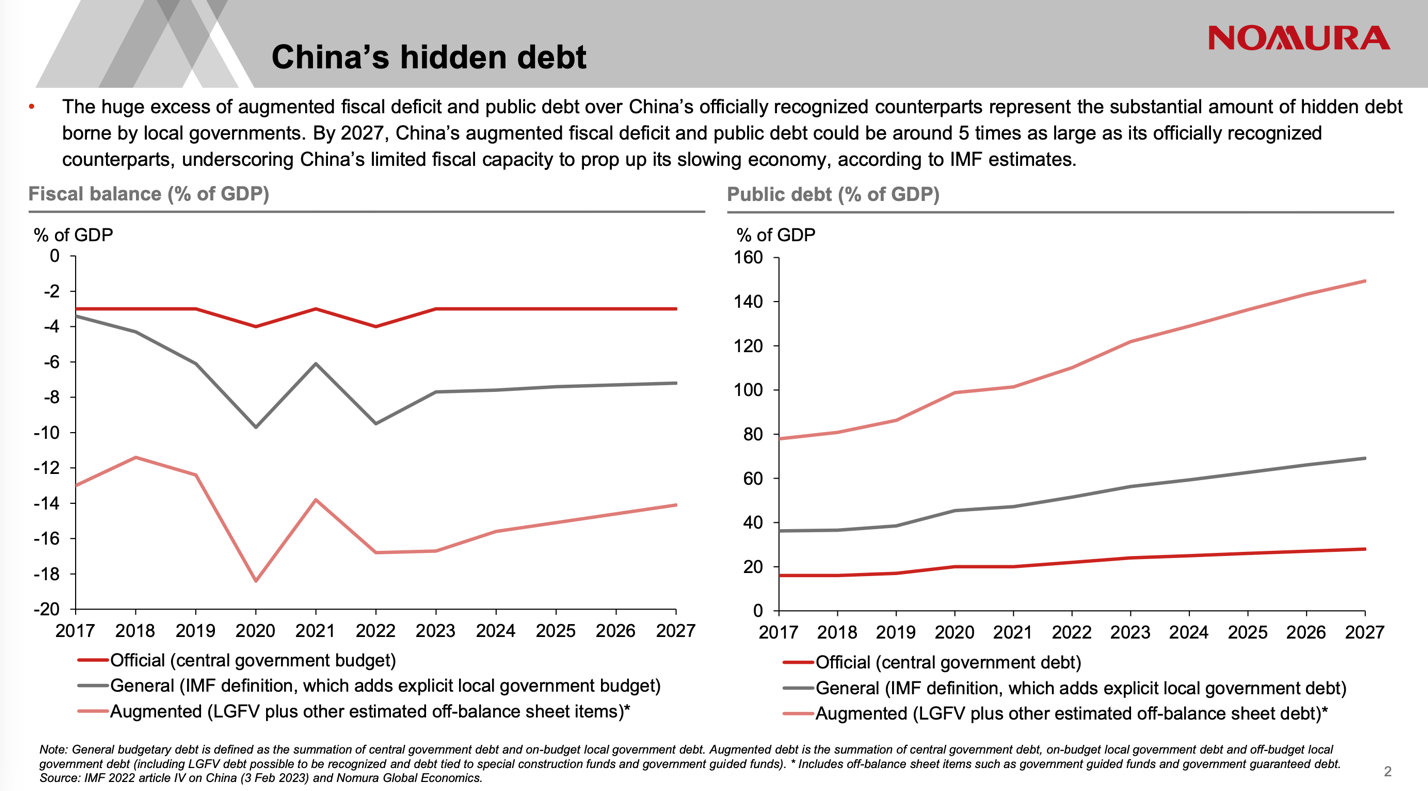

China's debt (Nomura economist)

Additionally, I was struck by a comment in the deindustrialization panel. Bottomline: Different trading relationships are happening. We're still dependent on China trade; it’s just happening differently via proxies such as Vietnam.

Also, there's the chance that trading blocs shift toward that of like-minded partners. North America looks good and offers “balance.” Other parts of the world are more difficult to project, especially now with this current crisis and its effect in the Middle East and beyond. In the longer term, the momentum of “markets” will prevail — but we are effectively disrupted.

{kind=link}

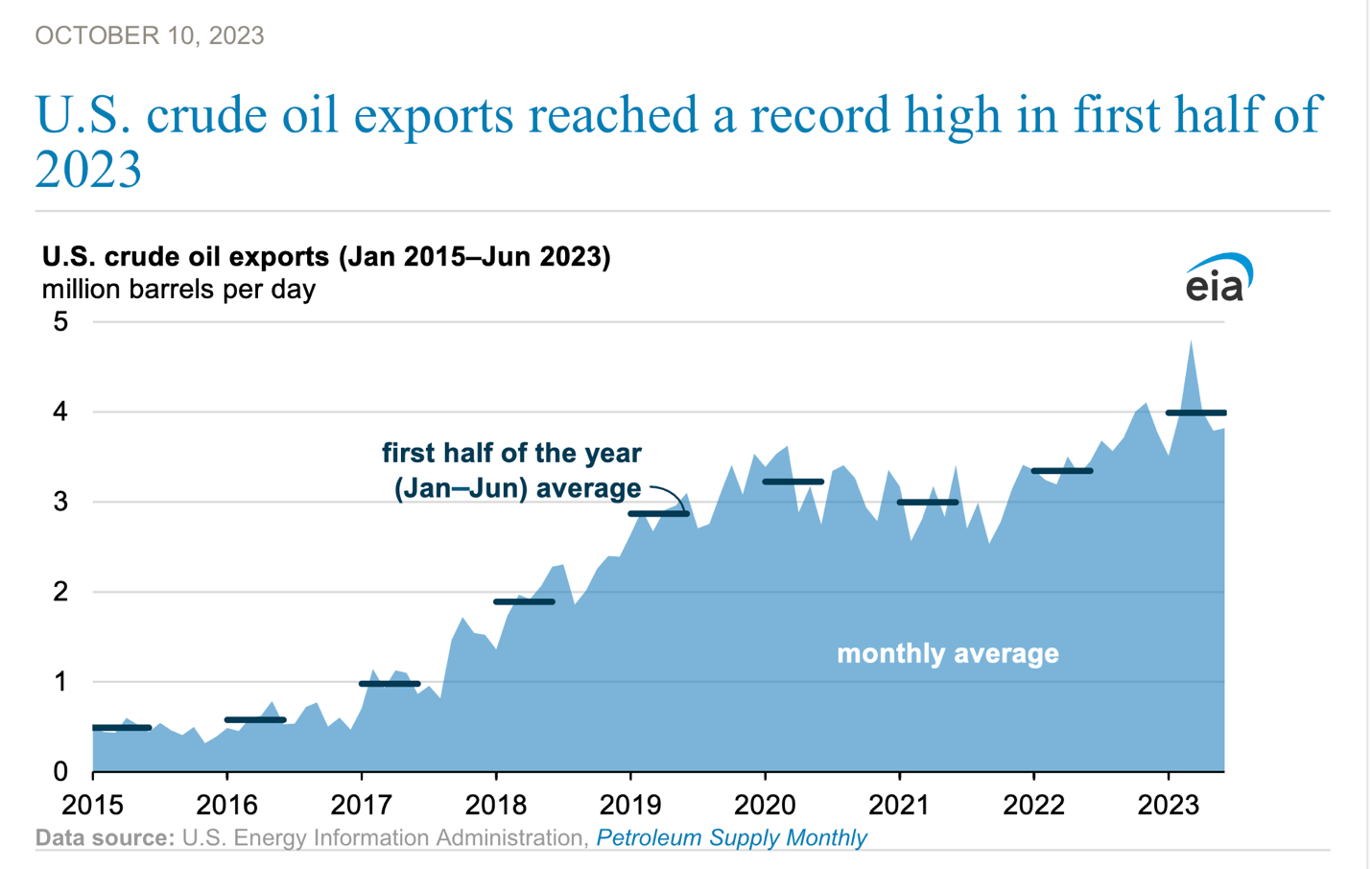

U.S. crude oil exports (EIA, 2023)

Scale, re-workings, consolidation

Our U.S. industry is global, capable and efficient. We will continue to utilize technology to produce resources more efficiently and cleanly in the future. I think with Exxon’s purchase of Pioneer, the sheer size of Exxon will allow for new advances in the Permian, and translate elsewhere. The same is true of the Chevron-Hess acquisition.

In general, my geopolitical takeaway is: Disengagement is not an option. We can engage with the rest of the world in energy and alongside our capital markets. That is a positive path forward —our technology, innovative minds and markets’ transparency.

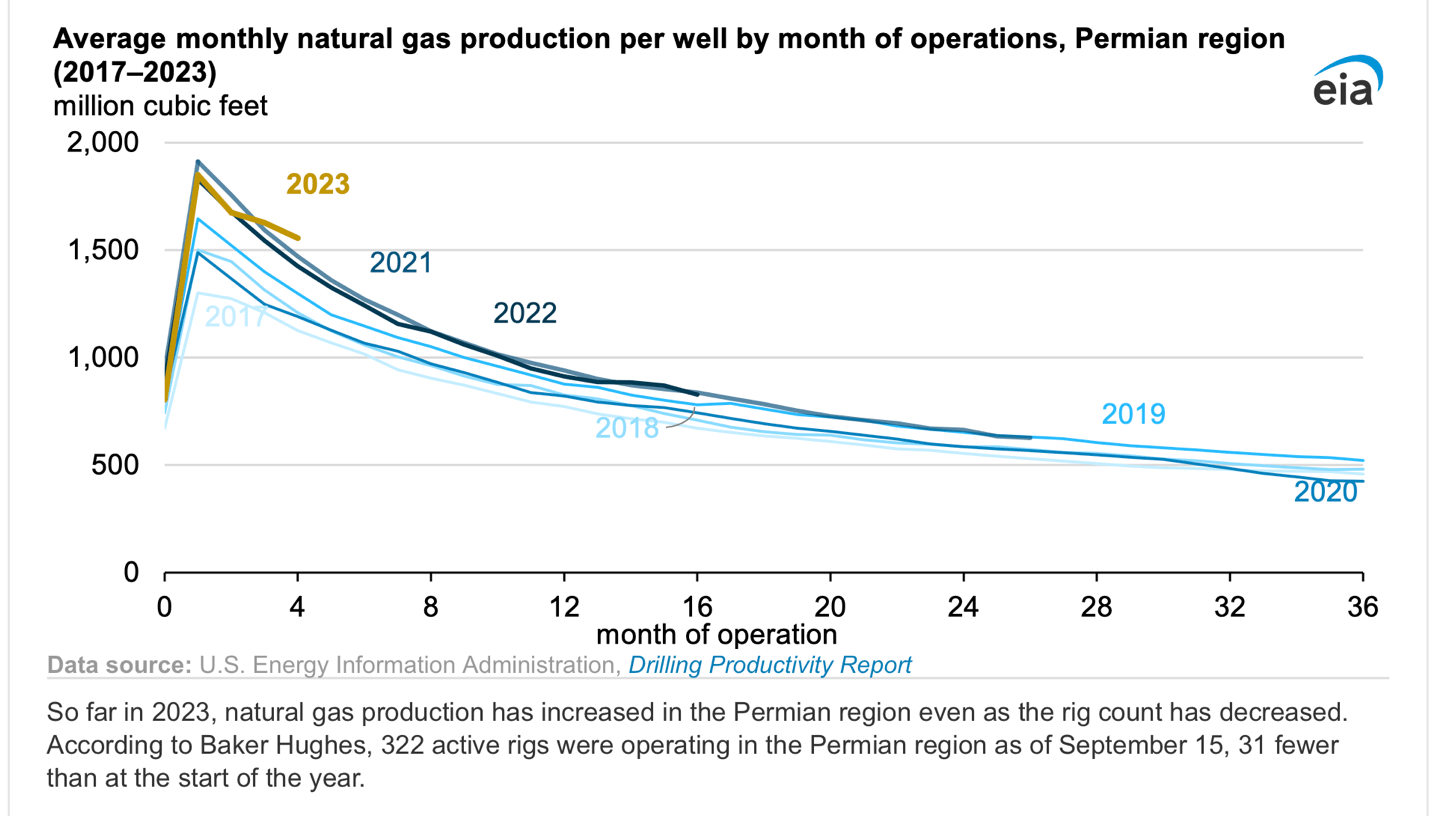

Secondly, the theme of natural gas being a “transition” fuel is still my main idea in that thought experiment. However, on a practical level, natural gas is a generally reliable and affordable source of baseload power. It has a cleaner emissions profile and more work is being done globally to cleanup methane emissions, a byproduct of its production when not addressed.

{kind=link}

natural gas efficiency (EIA, Oct. 2023)

With regards to Energy Transfer (ET) and an upcoming feature, the eventual start of their Lake Charles LNG plant is a net positive for the U.S., the industry and other countries. There has been support for their stewardship in this capacity from global players such as Shell ( SHEL ) and others. (Once the story is online, I will post a link in comments.)

In summary, U.S. oil and gas offers a bullish investment theme as noted in the video. Given geopolitics, oil market tightness and the economic outlook, the majors have picked their moment well. In the 2014 Pioneer-Permian shale story, I noted that the majors had l eft the U.S. for global fields , and now they have returned. In 2023, they have returned again in even more full force. The requisite energy infrastructure has to work, connecting supply to demand centers, as geopolitics and market conditions shift the landscape again. The midstream sector, which includes diversified players like Energy Transfer with their large global footprint, also will be part of the solution.

( Link to video interview with slides and more discussion )

For further details see:

U.S. Oil And Gas Echoes Macro And Geopolitical Environment (Video)