BKT - U.S. Real Estate Sector Report - Fall 2025

2025-10-03 09:32:00 ET

Sector conditions and outlook

{kind=link}

Current condition |

Outlook |

APARTMENT |

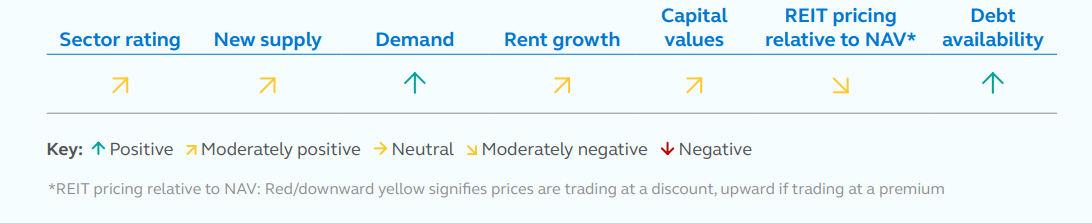

The apartment sector is experiencing a surge in demand through the halfway point of 2025. Vacancy rates have declined sharply in the past 12 months and supply pipelines are seeing significant declines in new projects. Higher interest rates, as well as material and labor costs are the primary factors. Although rental growth has remained pressured, the sector is poised to see stronger operational performance over the balance of this year. |

HOTEL |

Hotel sector performance remains nuanced, largely due to policy uncertainty and declining savings rates among middle-income households. While travel data has been supportive and occupancy levels have stayed relatively healthy, ongoing caution around the economic outlook and policy-related headwinds continue to constrain more robust sector performance. |

INDUSTRIAL |

The industrial sector is facing headwinds associated with strong new supply in select metros and tenant uncertainty surrounding the impact of tariffs, which is complicating longer-term leasing conditions. Despite these challenges and higher vacancies, the sector remains sought after by both equity investors and lenders. Sector performance will be determined by both trade flows and economic growth, which we believe will drive continued leasing for larger and more modern warehouse facilities. |

OFFICE |

Although office fundamentals show signs of stabilization, they remain weak due to a lack of hiring in traditional office-using occupations and a lack of traction in the return to the workplace. Vacancy rates remain elevated in the low-19% range as leasing activity remains soft. Liquidity within the sector has been mixed with some improvement in sales volume, but it has been limited to portfolio level activity and core assets, which are trading selectively. Leasing economics remains a challenge for owners as the pricing pendulum continues to tilt toward tenants. Limited new supply will help in the nascent recovery, but only for the most well positioned assets. |

RETAIL |

The retail sector continues to exhibit strong performance and has become more sought after by institutional investors due to outperformance in 2024. The sector’s unique position as a diversified sector continues to attract investors toward its cyclically resistant formats, which are also more defensively positioned against e-commerce penetration. Consumer resilience, however, is being tested as evidenced by a flattening of sentiment in the specter of higher inflation, which could erode discretionary spending power below all but the top income groups. |

SINGLE- FAMILY RENTAL |

The single-family rental (SFR) sector has performed well over the past 12 months but faces modest headwinds in select metros due to overdevelopment, which has tempered projected rental growth. Vacancy rates in most regions remain near equilibrium, and stable demand continues to support the sector’s income profile. |

DATA CENTERS |

Data center demand remains strong as new demand continues to outpace the pace of new supply. At present the top-10 U.S. markets have less than 10MW of power available, which equates to a vacancy rate of roughly 2%. The number of tenants in space continues to expand powered by both cloud computing and AI related companies. Hyperscalers and intermediaries are leasing power to satisfy short-term AI contracts. |

STUDENT HOUSING |

The student housing sector continues to exhibit solid fundamentals. However, it is becoming more competitive as much of the demand is now being met. Increased migration to southeastern states has generated optimism, particularly with students opting to stay closer to home. Despite these positive trends, we remain cautious about the sector due to moderating enrollment trends at four-year institutions. |

LIFE SCIENCES |

Fundamentals in the life sciences sector remain under pressure following a wave of overdevelopment and limited new space supply. Nationwide R&D lab vacancies, according to CBRE, reached 22.7% as of mid-year despite an increase in total leasing activity. However, net absorption remained negative due to lease expirations. The sector continues to face stress from persistently soft post-pandemic venture capital funding trends. |

Source: Principal Real Estate, September 2025.

Apartment

{kind=link}

Sector overview

The apartment sector is experiencing a surge in demand through the halfway point of 2025. Vacancy rates have declined sharply in the past 12 months and supply pipelines are seeing significant declines in new projects. Higher interest rates, as well as material and labor costs are the primary factors. Although rental growth has remained pressured, the sector is poised to see stronger operational performance over the balance of this year....

U.S. Real Estate Sector Report - Fall 2025