TKAYF - Uber Q3 Earnings: High Demand Drives Growth And Profitability

2023-11-07 15:40:07 ET

Summary

- A closer look at Uber Technologies, Inc.'s Q3 underlying business performance reveals a strong operational performance and significant growth across most metrics.

- Uber demonstrated impressive growth in key metrics, including gross bookings, active users, and trips.

- Looking ahead, Uber's Q4 guidance suggests a solid quarter with gross bookings on the rise. The company anticipates further revenue growth and margin improvements, reinforcing its commitment to profitability.

- Uber is facing pressure from regulators around the world with regard to gig workers.

- Based on conservative estimates, investors may look forward to close to 12% annual returns, potentially outperforming most benchmarks.

Investment thesis

I maintain my buy rating on Uber Technologies, Inc. ( UBER ) and update my revenue and EPS estimates following the company’s Q3 results.

Uber's Q3 earnings report may have slightly missed the top and bottom line consensus by a tiny margin, but a closer look at the underlying business performance reveals a strong operational performance and significant growth across most metrics. The headline revenue miss was primarily due to business model changes that impacted revenue, but not the operating income or EBITDA, meaning the company continues on its incredible growth path.

Wall Street analysts expect continued revenue growth at a mid-teens rate in the medium term, with rapidly growing EPS. Considering Uber's strong market position, brand strength, growth potential, and favorable valuation, the outlook for its shares remains positive. Based on conservative estimates, investors may look forward to close to 12% annual returns, potentially outperforming most benchmarks.

Looking past the top line numbers reveals a solid operational performance with growth across most metrics

Uber released its Q3 earnings report early this morning, and according to data from Seeking Alpha, it missed both the top and bottom line consensus by a tiny margin. However, these headline numbers are deceiving, as the underlying business performance was much stronger. Investors slowly seem to realize this, as the share price has improved from a negative couple of percentages at market open to it being up 2.5% at the time of writing.

Uber reported revenue of $9.29 billion, up 11.4% YoY and down from 14% in Q2. However, while revenue might have disappointed slightly, coming in below expectations, underlying growth was much stronger. I believe this is what investors need to focus on, as these metrics will drive long-term growth and indicate business health. Crucially, both profitability and booking growth were above expectations and guidance.

So why did revenue growth disappoint with underlying metrics remaining strong? This resulted from certain business model changes that required a reclassification of the cost of some promotions from sales and marketing expenses to contra-revenue. This impacted revenue by $521 million but did not impact either operating income or EBITDA. Excluding this impact, revenue would sit above the consensus by around $300 million.

These business model changes should continue to impact the revenue volatility in the near term, but will improve pricing flexibility and new revenue opportunities in the longer term.

Meanwhile, gross bookings growth accelerated to 20% YoY from 16% in Q2 and came in above guidance of 16% to 19% growth, resulting in gross bookings of $35.3 billion. Furthermore, excluding an underperforming freight segment, this was up 23% YoY, showing very healthy growth in demand driven by new and existing customers.

Uber Q3 Gross bookings data (Uber)

{kind=link}

MAPC’s, the number of users actively using the Uber platform for either mobility or eats, was up another 15% in Q3 to a staggering 142 million. This growth is an important indicator of demand for Uber’s services and an essential driver of both long and near-term growth. Furthermore, the number of trips was up 25% YoY, up from previous quarters, and reached 2.4 billion in Q3, or approximately 27 million trips per day on average.

{kind=link}

Overall, the Q3 results reflect a strong demand environment in which Uber continues to thrive, with most of its growth metrics remaining in the strong uptrend that started following the COVID-19 pandemic-induced lockdowns.

Many expected growth for Uber to slow down after this had recovered to pre-covid-19 levels, and while we have definitely seen a slowdown in growth over recent quarters, we can now see a stabilization in the low-20s and mid-teens in terms of growth rates, with Q3 showing accelerations across multiple metrics. Most crucially, Uber continues to expand its user base and sees activity per user increase, creating a dual motor to drive sustainable growth.

There are three important factors I want to highlight here that contribute heavily to this growth. First , Uber continues to see great benefits from its combination of eats and delivery as this allows for cross-selling opportunities and discounts as well as sharing technological insights and innovation. In other words, Uber is able to grow faster by combining both segments and attracting new customers.

The second factor contributing to Uber’s strong underlying metrics growth is the great adoption of Uber One subscriptions. Through these subscriptions, Uber increases customer loyalty and use frequency while also increasing revenue predictability and data insights for Uber. This is what Uber writes on its website :

This program extends across both Uber’s rides and delivery network and incentivizes its members to not only use rides more but also order more often.

As a result of this, Uber One members already account for 27% of gross bookings and 40% of delivery gross bookings. Meanwhile, the subscription service is still only available in 18 countries (after adding another three in Q3), leaving a long runway of growth for this service. I am expecting adoption to remain strong, which will boost growth across multiple metrics.

The final factor driving strong growth, especially in profitability, is advertising. With over 140 million users, the Uber platform, comprised of Eats and Mobility, makes an excellent advertising location.

The number of advertisers leveraging the Uber platform continued to grow strongly in Q3, with this growing another 70% YoY to 445,000, consisting of businesses of all sizes. As a result of this incredible growth in advertising, Uber is on track to exceed targets. The Uber platform is now expected to exceed $1 billion in advertising revenues by 2024. This means it has become a significant contributor to top-line growth while also meaningfully boosting profitability across the board due to the generally higher margins of this business.

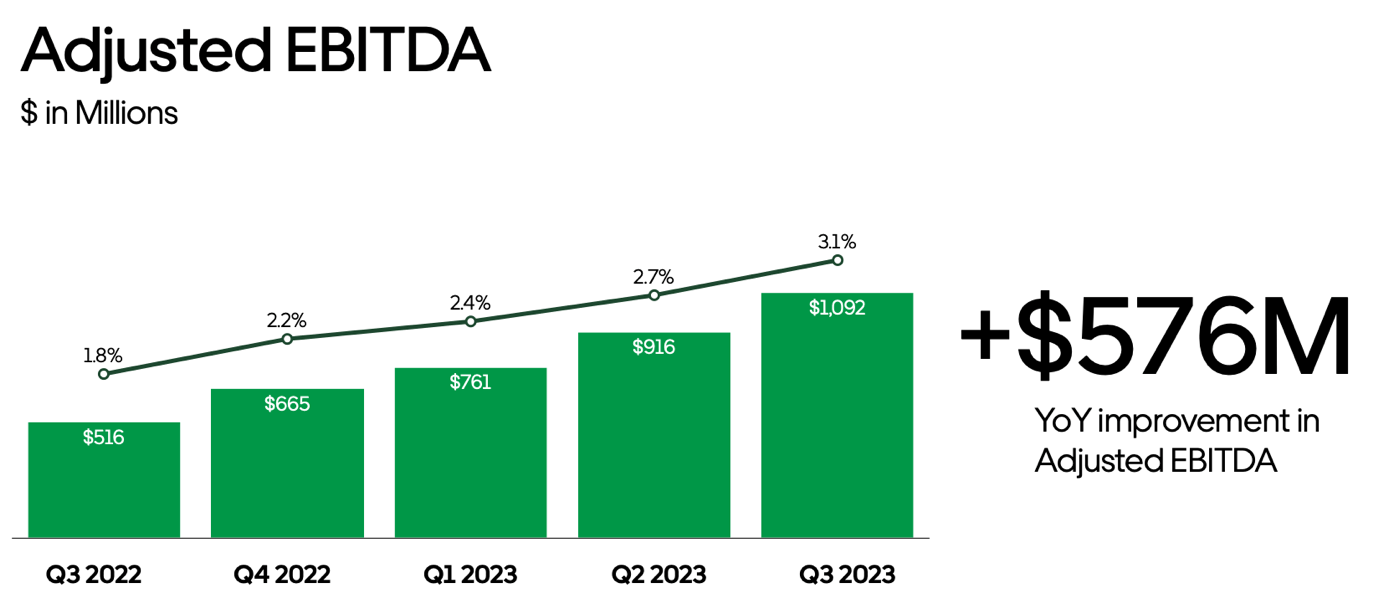

Supported by this growth in advertising revenues, Uber posted another strong bottom-line performance in Q3, with EBITDA and GAAP operating profits reaching new highs. The Adjusted EBITDA reached $1.1 billion, up 112% YoY. This result represents a record Adjusted EBITDA margin of 3.1% of Gross Bookings, up 40 basis points sequentially, and an incremental margin of 9% YoY, down from 10% in Q2.

{kind=link}

Furthermore, GAAP operating income in Q3 was $394 million, up from a negative $495 million one year ago and up from $326 million in Q2. However, Uber did not quite improve profitability as quickly as I hoped it would in Q3, with the operating margin coming in at 4.2%, sitting below my 5% estimate. Nevertheless, Uber showed that profitability is here to stay and reported a sequential improvement in the operating margin of 70 basis points, driven by an improved operating performance and lower stock-based compensation expense.

This resulted in an EPS of $0.10, carrying the impact of some unrealized losses in the company’s equity investments. Furthermore, free cash flow ("FCF") was $905 million, an increase of $547 million YoY. Still, this is down from $1.14 billion in Q2 as Q3 FCF was impacted by a $622 million cash outflow related to the payment of an UK HMRC VAT assessment. This brings the TTM FCF to $2.3 billion.

Uber ended the quarter with $5.2 billion in unrestricted cash, cash equivalents, and short-term investments, and equity stakes marked at $5.1 billion. Financially, the company is looking strong.

Overall, Uber is clearly making great steps forward in profitability, proving the critics, who believed Uber would never report a GAAP profit due to its low-margin business model, wrong. The company continues to improve its GAAP margins, and as it grows in size, I expect this improvement to accelerate YoY in the next few years.

Growth in Mobility accelerates

Mobility was once again the strongest performing segment in Q3 as gross bookings reached a new all-time high of $17.9 billion, up 31% YoY, driven by growing consumer engagement across use cases. This is highlighted by a 29% YoY increase in trips, accelerating from 26% YoY in Q2.

{kind=link}

Contributing to this is strong demand in the U.S. is a pickup in corporate travel as businesses eased travel cutbacks and announced return-to-office initiatives. Furthermore, Uber is seeing strong adoption of non-UberX products like Reserve, Uber for Business, and Shared Rides, which grew over 80% in Q3, reaching an annual bookings run rate of over $9 billion. The legacy UberX business meanwhile grew 20% YoY.

As a result of these new products and overall platform improvement initiatives, Uber management believes its category position is sitting at a multi-year high in the U.S., UK, Canada, and India as Uber continues to outgrow the competition. Meanwhile, the company also continues to expand operations in underpenetrated regions to drive additional growth.

Ultimately, this resulted in revenue of $5.1 billion, up 33% YoY. This represented a take rate of 28.3%, up 40 basis points YoY. However, this included a 90 basis point negative impact from the earlier discussed business model changes. Excluding these, the take rate was up 130 basis points, driven by an improving marketplace. This resulted in an Adjusted EBITDA of $1.3 billion, with a margin of 7.2% of Gross Bookings.

As I have explained in prior articles, the fees Uber has to pay its drivers heavily depend on the marketplace's health, including the number of drivers available on the platform and demand. Uber increases its incentives to drivers during holidays and busy seasons to create more availability, for example.

Over recent years and quarters, the marketplace has been improving in terms of health, with driver availability and overall driver numbers outgrowing demand. As a result, Uber is able to pay lower fees to drivers to satisfy platform demand, boosting its take rate. In Q3, active drivers were up 32% YoY, and driver engagement was up 5% YoY. The total number of drivers and couriers active on the platform increased to 6.5 million, up 1 million YTD.

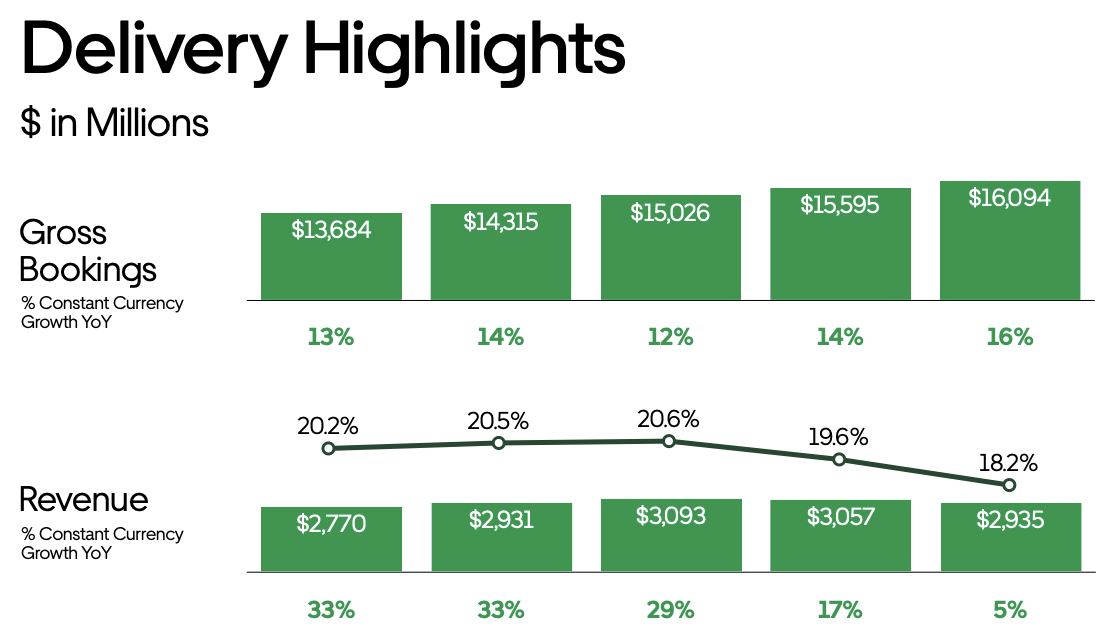

Growth in Delivery remains above expectations

The Delivery segment also delivered a very respectable Q3 result, with gross bookings growing 18% YoY, driven primarily by volume growth as basket size inflation continued to normalize. This also drove a strong performance in trips, which saw the highest growth in nearly two years as frequency reached another all-time high.

{kind=link}

Driving this growth, in part, are continued improvements in the underlying business. For example, the average U.S. delivery time in Q3 was down 3 minutes YoY. Developments like these contribute to increased retention and healthy eater growth, as highlighted by the fact that US Delivery MAPCs were at an all-time high in Q3.

Furthermore, Uber also continues to expand its delivery offering by investing in so-called “New Verticals” like grocery, convenience, and alcohol. Gross bookings for these new verticals accelerated in Q3 to 46% YoY growth, as 14% of delivery users now order new verticals.

The strong underlying operations drove revenue of $2.9 billion, up 6%. However, this included a $360 million negative impact from business model changes or 13 percentage points of growth.

This also meant that the delivery take rate was down 200 basis points, including a 220-basis point impact from the business model changes. Excluding this, the take rate was up 20 basis points, driven by demand growth and an improving marketplace.

As for profitability, Uber reported a Delivery Adjusted EBITDA of $413 million, with a margin of 2.6% of Gross Bookings. Overall, delivery continues to outperform my expectations and those of analysts as Uber continues to take market share and expand its operations and offerings.

Outlook – Is UBER stock a Buy, Sell, or Hold?

Uber continues to see demand accelerate in Q4, with trips and bookings setting new highs in October. Therefore, Uber guides for a solid fourth quarter, with gross bookings sitting between $36.5 billion and $37.5 billion, up 18% to 21%, reflecting a growth stabilization.

This growth in bookings is expected to be driven by at least 20% growth in trips as Uber continues to see strong demand. Assuming the take rate to remain similar to Q3, this would result in revenue of around $9.62 billion, up roughly 12% YoY.

This solid top line performance and further margin improvements should result in an Adjusted EBITDA of $1.18 billion to $1.24 billion, reflecting a margin of 3.3% of gross bookings, up 20 basis points sequentially.

For FY23, this should bring gross bookings to a total of over $137 billion, up 20% YoY, and an Adjusted EBITDA of roughly $4.0 billion, translating to an incremental margin of 10%.

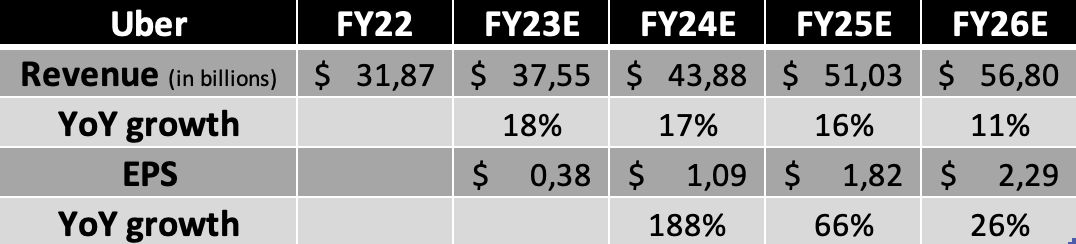

Looking forward, Wall Street analysts continue to expect Uber to keep growing revenue in the mid-teens in the medium term, which I believe is highly likely considering its growth and expansion potential. Meanwhile, EPS is expected to rapidly grow from here as the company continues to boost its margins, driven by cost efficiencies, a healthy marketplace, and size advantages.

The graph below includes the current Wall Street analyst's medium-term financial estimates.

Wall Street financial estimates (Made by author based on data collected by Seeking Alpha)

{kind=link}

This brings us to the valuation of Uber shares. Considering the company practically operates a monopoly (or duopoly), has incredible brand strength, a long runway of growth, and plenty of expansion opportunities, I believe it is safe to assume the company will grow its revenue at mid-teens to low-double digits through the end of the decade and to continue growing EPS rapidly as well.

Yet, of course, there are risks to this growth outlook. Uber is facing pressure from regulators around the world with regard to gig workers. I recently explained this in my article on Just Eat , in which I stated the following that is of importance to Uber as well:

The likes of Uber and Grubhub recently lost in an effort to block a minimum delivery pay rule in New York City, which would force companies to pay couriers an hourly rate of $17.96 or pay per delivery at about 50 cents a minute.

This is compared to a 2022 average hourly pay of around $15.84, a rate which, of course, highly fluctuates. The new rule would, therefore, increase the average hourly wage for drivers by over 13%, massively impacting either their profitability or the number of orders if these increases are pushed onto users. Of course, this also brings with it many operational problems.

Uber, DoorDash (DASH), and Grubhub are facing similar regulations in multiple regions and cities as governments are looking to create improved earnings certainty for these independent workers, creating a significant risk for these food delivery platforms.

Regulatory actions like this can massively impact Uber’s profitability and be a drag on its EPS growth, or, if Uber has to push these prices onto the consumers, on its top-line growth. Therefore, it is crucial to keep a close eye on these developments and commentary from Uber management, which responded clearly to an effort by the European Union to improve economic conditions for gig workers, forcing the likes of Uber to reclassify their couriers, giving them full working rights. This is what I wrote in my Just Eat article:

Uber executives have already released a statement against this new regulation, claiming it would force the company to shut down operations in hundreds of cities and raise prices by as much as 40% while also massively decreasing driver availability in major cities. According to Uber, it would practically destroy the operating model of delivery platforms. While I believe Uber might be overreacting here, the impact will undoubtedly be massive for Uber and Just Eat, massively eating into their profitability. Furthermore, it would complicate their operations and decrease role availability as drivers must be officially hired, not just sign up.

This, again, can have a meaningful impact on Uber’s profitability or growth in the region as it might have to shut down operations. For now, the new EU law is not close to finalization and considering the impact on the delivery industry, I have a hard time believing we will see this being finalized at all. Yet, these threats exist for Uber and do put a risk on its business model and financial expectations.

Nevertheless, I believe the positives outweigh the negatives when looking at Uber as an investment, and using the current FY26 EPS projection and a 30x P/E multiple, which I believe is more than fair considering everything pointed out above, I calculate a target price of $68.70. This means that from a current share price of around $49, investors are poised for annual returns of close to 12%, most likely outperforming most benchmarks.

As a result, I continue to view Uber shares as an attractive buying opportunity and maintain my Buy rating, as the company continues to fire on all cylinders and regulatory issues are not causing major issues today.

For further details see:

Uber Q3 Earnings: High Demand Drives Growth And Profitability