TTWO - Ubisoft: Cheap Speculation On Improving Performance

2023-04-22 00:33:58 ET

Summary

- Ubisoft Entertainment SA is a company that creates, publishes, and distributes video games for various platforms worldwide.

- Ubisoft has seen accretive growth through increased recurring revenue, while also expanding its mobile gaming footprint.

- Margins have tightened in recent years but we see a return to normal, with an EBITDA-M of c.40%.

- Ubisoft is trading at a minimal 3.8x NTM EBITDA, allowing investors to cheaply speculate on the margin expansion we expect and growth.

Investment thesis

Our current thesis is:

- Increasing recurring revenue should create greater income stability and better margins.

- Leading franchises should allow growth to grow at a similar rate to what has been achieved historically.

- Ubisoft is cheap at its current valuation, reducing risks to investors.

- The business represents a takeover target at its current price.

Company description

Ubisoft Entertainment SA ( UBSFY / UBSFF ) is a company that creates, publishes, and distributes video games for various platforms worldwide, including consoles, PCs, smartphones, and tablets.

Share price

The last decade is a story of two halves for Ubisoft. The business was gaining substantially into 2019, followed by a rapid decline to a several-year low. The business has struggled to develop despite achieving growth.

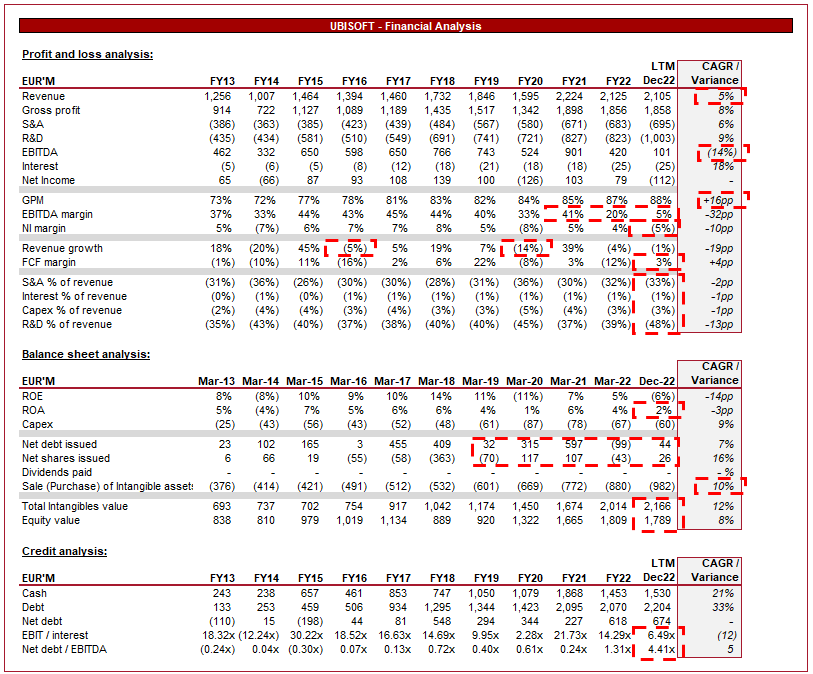

Financial analysis

Ubisoft financials (TIkr Terminal)

{kind=link}

Presented above is Ubisoft's financial performance for the last decade.

Revenue

Revenue has grown at a rate of 5%, driven by improving conditions in the gaming industry as technological development and cultural changes contribute to greater interest.

Mobile gaming has become one of the most significant trends in the video game industry in recent years, with millions of people playing games on their smartphones and tablets every day. This is an unsurprising trend in hindsight, as technological development has resulted in an impressive improvement in the quality of mobile games. Further, the majority of consumers want convenience and so the real stumbling block was the quality of games. From a financial perspective, this is a fantastic avenue for businesses as the games are highly monetizable, enticing consumers with free / cheap games. Ubisoft has looked to develop its current IP in the gaming space, launching games such as Assassin's Creed and Rainbox Six. This being said, we do feel Ubisoft has fallen behind its gaming peers in this regard. TTWO has purchased Zynga, the leading mobile game maker. Further, EA 's games are far more popular and monetizable in comparison. We have covered both these stocks here and here .

Microtransactions, including lootboxes, have become increasingly popular in the gaming industry over the past decade. Players are attracted to the possibility of receiving rare and valuable items, spending significantly more than the box price of a game over their playtime. This has been highly lucrative for gaming businesses as they historically could make one sale when the game was initially sold, losing out to the second-hand gaming market. Now, games can continually be monetized and the initial sale becomes far less important. Recurring income now represents 60% of total bookings, reflecting the importance of this way of generating income. This is positive for Ubisoft as the incremental cost of this service is minimal, so will rapidly accelerate margins, as well as revenue. This also de-risks new games released as the revenue per customer is now higher. There is some risk with this business model as businesses like Ubisoft and EA have been accused of encouraging gambling, with some calling for a ban on these transactions.

Ubisoft also has a strong pipeline of games ahead, with the following flagships due to release in the next 12-24 months: Tom Clancy's The Division Heartland, Skull & Bones, Avatar: Frontiers of Pandora, Assassin's Creed Infinity, Assassin's Creed Codename Red, Assassin's Creed VR, Beyond Good and Evil 2, Prince of Persia: The Sands of Time Remake, Tom Clancy's Splinter Cell, and Ubisoft's Star Wars. These games are market-leading titles that are the backbone of Ubisoft's brand. With so many games scheduled for release, we should see revenue remain strong as consumers flock to the titles. With games, especially AAA titles, there is always the chance they become a blockbuster hit, similar to the movie industry.

Current economic conditions are hard for discretionary industries as consumers are seeing their incomes deteriorate due to inflation in living costs. Further, interest rates are compounding the impact of this, with rates at decade-high levels. The consensus view is that every discretionary business will struggle but we have seen that gaming generally remains robust . This is due to the weight consumers place on the entertainment form, meaning they protect a certain level of expenditure. This is likely routed somewhat in the cost, as consumers may only buy a couple of games each year. This is an amount that can be saved up without too much concern. We expect revenue to remain strong, although growth will likely soften.

Margins

Ubisoft has seen its GPM trending upward in the last decade, gaining 16 ppts. This is primarily driven by greater microtransactions which come with a small marginal cost to the business.

Unfortunately for Ubisoft, this is where the good news ends. The company has seen its S&A and R&D expenses increasing at a rate greater than revenue, resulting in a dilution of margins. This is due to the most recent R&D expense, which looks to be one-off in nature, relating to in-house software-related production.

When combining these costs, alongside capex, the business looks to be spending a substantial amount of cash on operational costs (74% of revenue in FY22). We struggle to see how this can be considered a good allocation of resources given the business is not growing at a superior rate. A degree of this is Management misallocating resources in our view.

On a normalized basis, the business has been able to generate an EBITDA margin of c.40%, which it looks like it can return to. FCF has not been so clear, with the business experiencing an unusual level of volatility. We do think there is a lot to like here, but problems certainly exist.

Balance sheet

Ubisoft has an interesting capital allocation strategy. The business has been raising debt, issuing shares, and not paying dividends. So where is the cash going you ask? The company has been spending it on R&D development, consistently expending >500M a year. With EBITDA remaining depressed in the last two years, the company's leverage looks problematic. Assuming margins do return, we are not overly concerned. The reason issue is whether we have seen an efficient allocation of resources, which when you look at the net income line for the last decade, is hard to argue for.

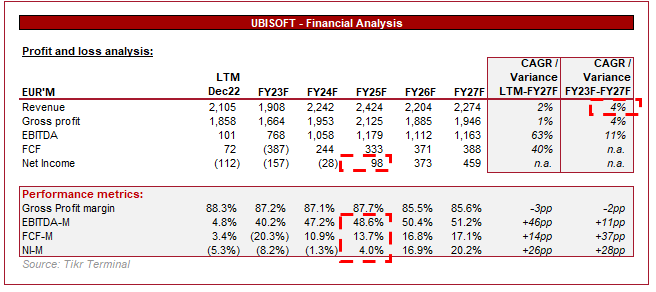

Outlook

Ubisoft outlook (Tikr Terminal)

{kind=link}

Presented above is Wall Street's consensus view on the coming 5 years.

Revenue is expected to grow at a lower level than in prior years, with the business only achieving 4%. Markets are not pricing in a spike from new game releases, believing them to be more of the same.

On a positive note, margins are expected to return to a healthy level. We concur with this view as it looked to be impacted by a one-off expense. Further, the opportunity for greater recurring revenue to be earned has the potential to push margins up. Finally, the business looks to be inefficiently run and so a better allocation of resources can easily find some gains.

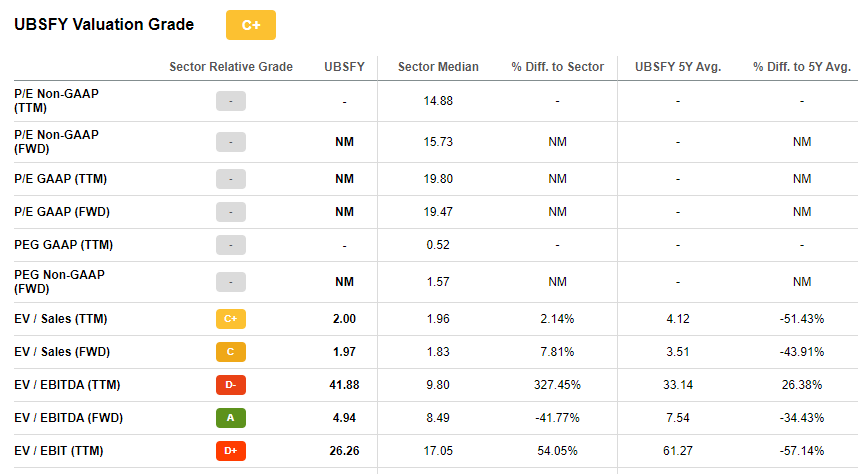

Peer comparison

Profitability (Seeking Alpha)

Presented above is a comparison of Ubisoft to a cohort of peers.

Interestingly, the company scores a C+ for profitability despite its struggles in the most recent year. Assuming EBITDA-M returns to c.40% in the next 18-24 months, the business would outperform the average by 22%. This would make the business highly attractive relative to these businesses, even with steady growth.

Valuation

{kind=link}

The key valuation metric to consider is NTM EV/EBITDA in our view. Sales will be overly harsh on the company due to its superior GPM and bottom-line profitability is less certain. Ubisoft is currently trading at a mouthwatering 3.8x, far below the sector median of 8.4x. This is a sizable which we cannot see the justification for. The business has weaknesses and we see a lot of problems, not to mention the inability to achieve consistent positive net profits. This being said, at 3.8x EBITDA, you have to ask yourself what are you buying, and the answer is a business with the capacity to generate a 40% EBITDA-M.

Takeover target

An interesting component of all of this is a potential takeover. With a lost decade of performance, during which businesses like EA and TakeTwo have gained massively, many are calling for Ubisoft to give in to a bigger player who can yield better outcomes. Industry Insider Jeff Grubb has stated that Ubisoft is seeking a 3rd party takeover currently. With a market cap of c.3BN Euros, a buyer should not be too hard to find, the problem is the lack of appetite so far.

Final thoughts

Ubisoft is operating in a fantastic industry that has grown well and has shown itself to be resilient. The problem is that Ubisoft has not fully exploited this, performing mildly at best. We do not see any glaring red flags but many issues which do not look like they are being resolved. With Ubisoft trading at 3.8x NTM EBITDA, however, the business looks like an attractive speculative play.

For further details see:

Ubisoft: Cheap Speculation On Improving Performance