UBSFF - Ubisoft: The Market Treats It Like Trash I Say 'BUY'

2023-04-04 12:30:52 ET

Summary

- I've written about Ubisoft in the past, and while my stake in the company is extremely small, I believe the last few months have seen the company become very interesting.

- Ubisoft is in no shortage of trouble, with plenty of challenges on the horizon.

- However, at nearly any sort of positive scenario, or even just managing positive earnings, the company can be said to be clearly undervalued next to peers.

Dear readers/followers,

It's time for an update on Ubisoft ( UBSFY ). This isn't an easy sort of company to invest in - it doesn't have a dividend, its returns are negative, and there are some fundamental troubles in the overall company thesis. At best, I believe it would be fair to say that Ubisoft is a "turnaround play" - though one that really has a lot to prove before we can really expect a near-term upside.

In this case, I'm going to update my thesis which at this point is over a year old.

Let's see what Ubisoft has to offer investors.

Ubisoft Entertainment - A tricky turnaround

It may be an easy belief to hold based on looking at Activision Blizzard ( ATVI ) that gaming companies are an easy way to make good money. This is not the case. There is a reason why I, as an avid gamer, have near-zero exposure to the entire industry. It's not because I don't like the products - it's because I find the product cycles as well as the business models to be oftentimes counter-intuitive to stable and recession-resistant earnings. My work on CD Projekt ( OTGLY ) is another good example that comes to mind.

Ubisoft is in no way a bad company. From a gross margin point of view, the company is among the highest in the entire industry and ranks in the 77th percentile. But that's where issues begin. Operating margins, net margins, RoE, RoA, and ROCE margins are all sub-par and below the standard 50th percentile in the industry, which for this company is interactive media - or gaming, in simple terms.

The company's interest coverage is terrible, ranking at the 14th percentile, and the company's cash, equity, and debt ratios are some of the worst I've seen in the business - and also compared to its own numbers a few years back. In short, Ubisoft has dropped, and it keeps dropping.

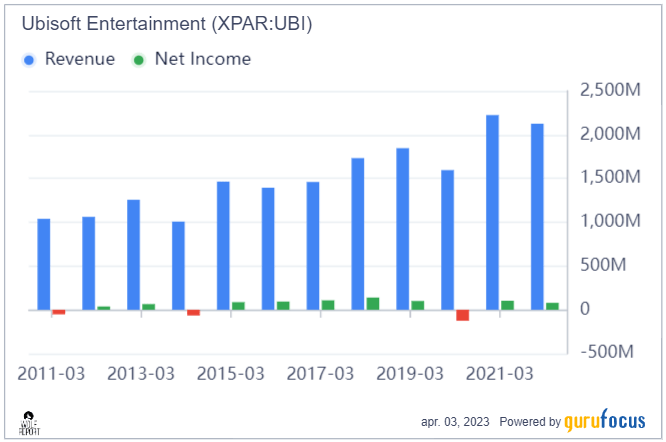

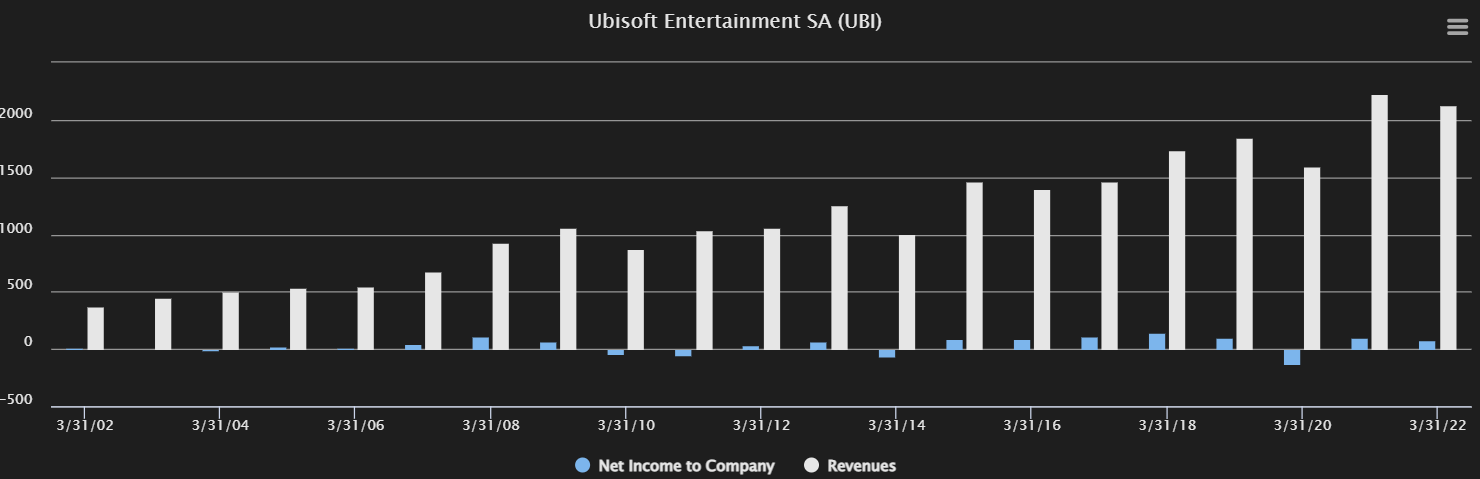

As "odd" as that may sound, it's not necessarily a problem. The way of the gaming industry is similar to movies - it goes with "blockbusters" - and Ubisoft hasn't had many of those for the past few years. Despite growing revenues, the company's net income has been stalling for some years.

{kind=link}

Cash flows, debt, dilution - none of these numbers show any sort of favorable trends. The company's revenues come primarily from the game publishing business (83%), with around 17% from the edition/production of assets. One question I get frequently about Ubisoft is how the company's gross margins can be so good, but how the company's operating margins can be so terrible. It's because most of the company's costs are not COGS, as you might see in an industrial, but Operating expenses, which in the way of accounting, are not directly associated with the production of goods. COGS is materials and transportation, OpEx is rent, utilities, office supplies, legal costs, and the like. That's why the way the company's income flows is somewhat "skewed".

As I said, Ubisoft isn't a bad business. it's actually one of the oldest companies still on the market in this segment, with founding in 1986 and being a multi-platform publisher. Ubisoft has taken an overall similar path to attempted growth as other publishers have. They've tried increasing their mobile sales due to the significant margins and the scalability of these products.

However, Ubisoft by and large, despite a well-filled library of games including the series of Assassins Creed, Far Cry, and Tom Clancy titles, have largely failed to generate significant returns here. By having "failed", I am referring to the following trends.

{kind=link}

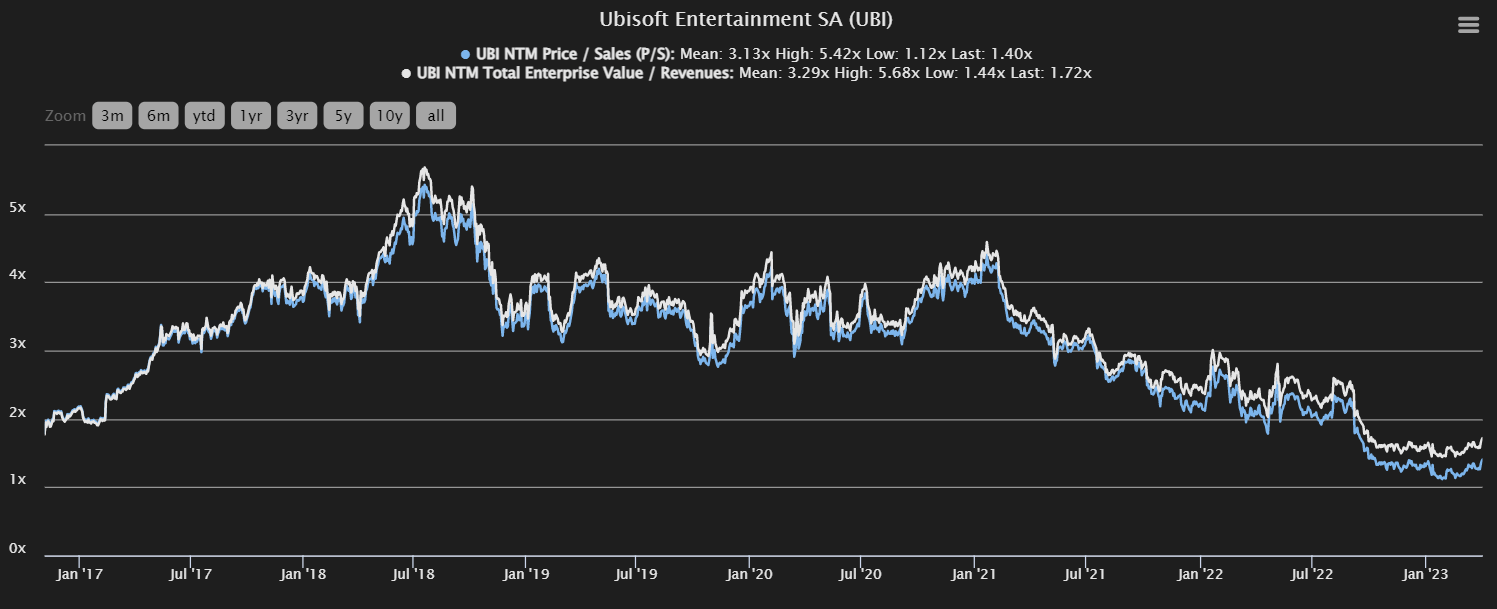

Ubisoft isn't the highest-quality gaming business out there, because a revenue dollar in Ubisoft does not equate to a revenue dollar, or even increased revenue, in net income. I won't claim that negative RoE, RoA, and other return metrics are unheard of in this industry. The fact that Ubisoft is still in the 30-40th percent tile with a negative 6.29% RoE means that this is not uncommon. And we also need to consider that Ubisoft, at this time of writing, is being valued at a revenue multiple of less than 1.8x and a sales multiple of less than 1.5x. Looking at the 5-year historical mean, this is significantly below where the business is usually valued.

{kind=link}

What I am highlighting here is a few of the reasons why, despite all the negativity, you shouldn't be quick to necessarily count the company out here.

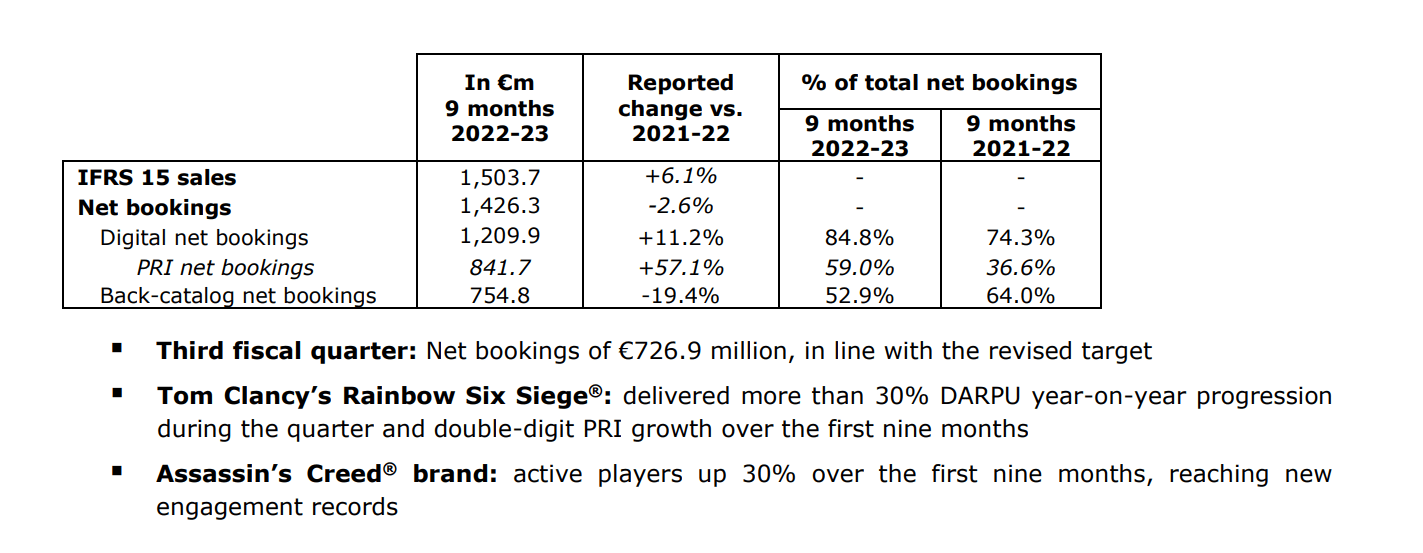

Because while Ubisoft may be in a turnaround, a turnaround it has been in for some time at this point, the numbers in terms of sales are still holding up strong. Take a look at the latest 3Q23 numbers, which at the very least showcase continued attraction for the company's titles, along with a confirmation of the 2022-2023 and 2023-2024 targets.

{kind=link}

The company also has a slew of new releases coming, including things like a new Assassins Creed, Mirage, Tom Clancy's Rainbow Six, and Avatar. The company is also showcasing its new "long-lasting live games", with Skull and Bones as an example - but that's where I as a gamer have to say that that particular game is absolute tosh - or seems like it, based on what I've seen. One of Ubisoft's problems has been an absolute lack of innovation for many of its core titles, with many of its new products seeming more like reskins of old ones or tired re-hashes compared to many excellent titles that have come out in the past 2 years.

Ubisoft needs to break this "slump" before a turnaround can be made real - and the recent set of company priorities do not give me faith. Here is what the Co-founder had to say as of late:

As we are focused on building on our strengths, we are prioritizing our efforts on big brands and long-lasting Live games. While the macro environment impacted the video game market and our Q3 results, our established franchises and Live games have performed solidly. In an intensely competitive environment for shooter games, Rainbow Six Siege has performed remarkably well. This momentum, seven years after the game’s release, is promising as we look to launch Rainbow Six Mobile next fiscal year. The Assassin’s Creed franchise reached new player engagement records over the past quarter, and we are excited to bring Assassin’s Creed Mirage to players in 2023-24.

(Source: Yves Guillemot, 3Q22)

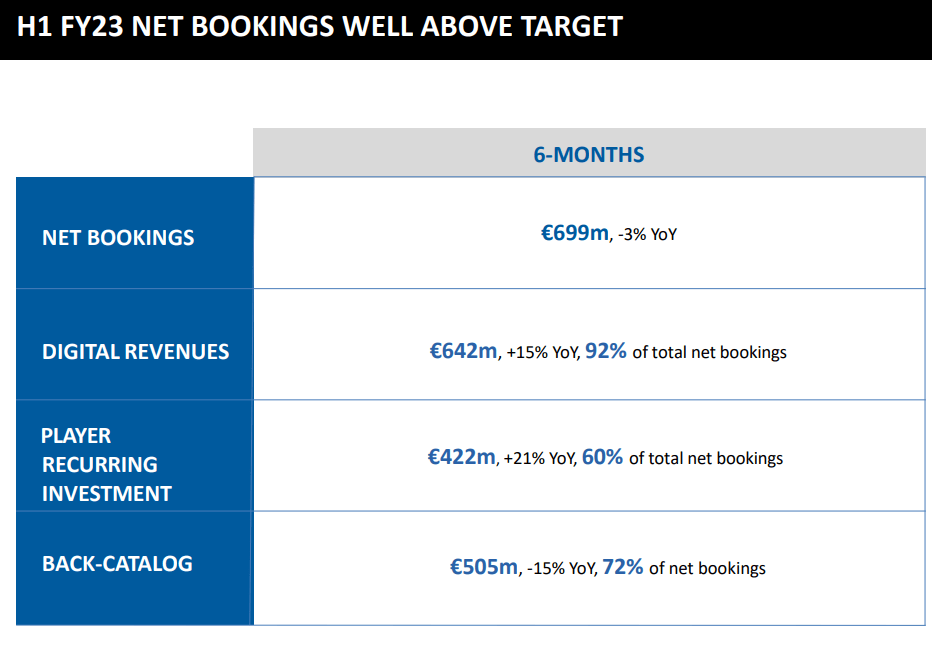

As a gamer myself, I probably am one of the harshest critics of this sort of company when investing. However, the company's focus on bookings, revenues, investment, and back-catalog tells me that the company's lack of focus on EBIT or net income showcases or highlights a problem.

{kind=link}

The fact is that the company's attractive IPs, including Assassin's Creed: Valhalla, have had more than 20M players, and bookings for other titles are up as well.

Then there is the M&A-related news for Ubisoft, with Tencent ( TCEHY ) looking to invest deeper into the company. I do not view this as a positive. The latest data from the Tencent deal implies a purchase price for Ubisoft (in terms of the stake) at around €38-€40/share when considering the specifics of the company structure of the major shareholders, the Guillemot family.

In the end, I continue to view Ubisoft as an attractive business from a pure valuation perspective. But I also acknowledge that there are significant worries and risks present in the thesis here - both related to sales, but also to other factors.

The fact that the company is in a turnaround and looking for direction is further confirmed by some of the moves the company is making. Canceling 7 announced titles in less than 12 months is not something done unless the company is looking to seriously turn things around. Part of the problem is cost, which needs to be reduced - but any time you're massively reducing costs in a gaming business, you're cutting staff - the creative and talented staff that's actually pushing your games. So even if the company manages its €200M savings targets, I would ask at what cost this comes in terms of game development?

Because while the latest games have been "okay" in terms of quality compared to what has been out there, they have not been blockbusters. I'm talking about comparing Assassin's Creed: Valhalla (Which I liked), with games like Elden Ring, Horizon Zero Dawn: Forbidden West, or God of War: Ragnarok. All of those games are better than Valhalla, and I don't think you'll find many enthused gamers who won't be able to see this perspective on things.

Look, I see a major problem in Ubisoft, as late as February of this year, saying that their major games ((AAA)) this year are going to be Skull and Bones, as well as The Crew Motorfest. In my mind, none of those titles will be able to compete with some of the major launches this year, either games that have come, or games that are about to.

So the trouble I see is with the company's ability to compete with product quality on a broader, global basis. I see Ubisoft as one of the "less appealing" games companies out there.

The positive part is, that the valuation definitely reflects this quite accurately.

Ubisoft Valuation - Almost ridiculously cheap

Ubisoft is one of the cheapest gaming publishers/designers currently available. I put it into interactive media and entertainment services. This includes comps like ATVI, NetEase (NTES), Nintendo, EA (EA), Take-Two (TTWO), and others. In this comp group, companies usually tend to trade at between 2.5-4x to revenues (6x+ for ATVI), over 10x to EBITDA, and only 3.76x for Ubisoft.

Some of these differences make sense. Consider for a moment that ATVI has a market cap of over $66B, while Ubisoft is at less than $3.4B. All of the peers I mentioned are not only larger than Ubisoft in terms of market cap and portfolio, but they're also more recently successful. And, more importantly, they're all profitable.

Ubisoft barely is, or isn't at all, depending on what year you look at.

The company is a business that desperately needs better results and a turnaround. The current plans include a significant savings program and focus on what the company refers to as a "live game". The problem is, these games have seen limited success in the long term, and it's not somewhere where Ubisoft has ever really excelled or produced critically-acclaimed products.

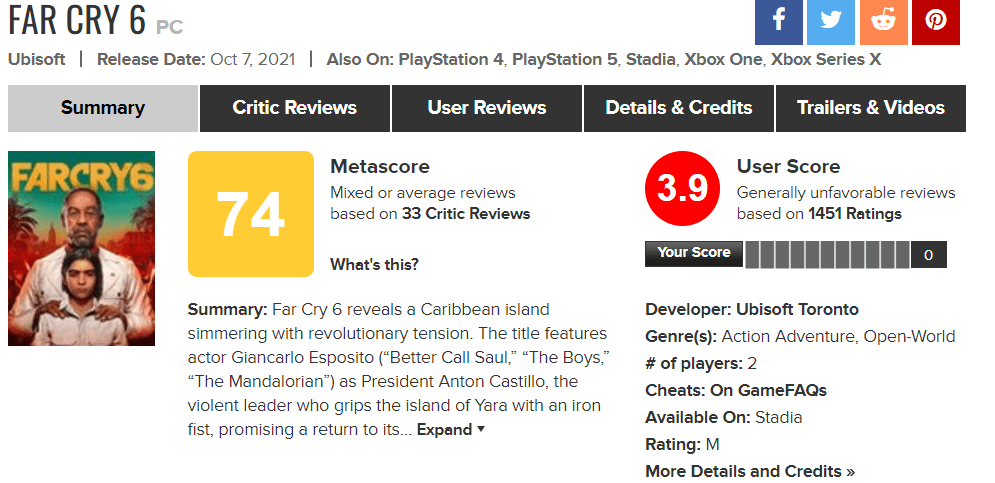

For that reason, I wouldn't view Ubisoft as a market leader, or even as a market-average company, but rather as an underperformer. I wouldn't pay more than a massive discount for an underperformer. The company's belief that its new titles, like Skull and Bones, will be outperformers, is something I would go very strongly against. The reason I'm sticking to my shares is that I see a long-term potential turnaround - but that is not related to Skull and Bones. Even the company's blockbuster IPs like Far Cry have been very lackluster. Take a look at the Metacritic Scores for the latest installment.

{kind=link}

For that reason, I significantly impair the company's valuation. Analysts are between €19 to €80 for the company's common share, traded in Paris, with an average of close to €41, down from an average of almost €60. Some analysts are still above €60.

Me, I'd price the company more like a distressed business based on its currently-negative trends and a pipeline that, to me, sees little in terms of being excited about.

The gaming space is an inherently risky area to be in. Never forget this. The more I read analysis by my colleagues, the more I realize that this is very hard to forecast unless you know your stuff in the space - because many failures these analysts have had are things I foresaw over 7 months before. I went in too early and underestimated the company and how far it would decline. My previous PT was just above €50/share, and this was a year back.

Things have grown worse than I expected since, and for that reason, I'm impairing it by another 20%. I'm now down to €40/share for the long term.

Doing any sort of forecast for Ubisoft is near impossible. Analysts can't be trusted - even with a 10-20% margin of error, their forecast accuracy is lower than 20%. You'd be mathematically safer betting on a coin toss - and even my own estimates should be taken with a grain of salt, because this company has really shown again and again that it doesn't deliver what its customers want - or rather, it lets it competitors deliver better products while underperforming.

For that reason, this is my current thesis on Ubisoft.

Thesis

- Ubisoft is, at least in theory, an attractive company with a good upside at the right price. However, due to what I would consider being mismanagement, the company's IP and pipeline don't really hold many products or games that I would consider likely to turn the currently unfavorable trends around.

- Ubisoft has a deep war chest, and I expect the company to eventually turn around. However, with the pipeline now updated and what'll happen in fiscal 2023-2024, it would further impair the company's valuation.

- I'm moving down 20%, and now consider the company a speculative "BUY" with a PT of €40 - no more.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I would call it qualitative, inherently, and cheap as well as with an upside, but I wouldn't call it well-run or paying a dividend. For that reason, I call Ubisoft a "speculative BUY".

For further details see:

Ubisoft: The Market Treats It Like Trash, I Say 'BUY'