UBS - UBS Group Q1 Earnings: Expected Weakness Shows How Resilient Business Is

2023-04-26 08:30:00 ET

Summary

- The management team at UBS Group announced financial results covering the first quarter of the company's 2023 fiscal year.

- The quarter saw a continued decrease in deposits, revenue, and profits, but the overall enterprise is quite resilient.

- In all, the UBS Group seems to offer investors a nice place to allocate their capital during these difficult times.

April 25th was a tough day for the market. But it was especially difficult for shareholders of banking giant UBS Group ( UBS ). After the company reported financial results for the first quarter of its 2023 fiscal year, shares took a step lower, dropping 4.7% for the day. A decline in revenue, combined with falling profits, aided in this regard. It didn't help that the company reported a decline in overall deposits quarter over quarter, likely driven by concerns about the banking sector in general. The good news for investors is that, in spite of these issues, the company does look rather robust from a fundamental perspective. Deposits have held up well in the grand scheme of things and, on a sequential basis, invested assets actually increased. Given these facts, combined with the rather attractive transaction involving it and Credit Suisse ( CS ) that still looks set to occur, I do believe that the company makes for a solid 'buy' candidate at this time.

UBS Group Q1 Earnings Results - Weakness across the board

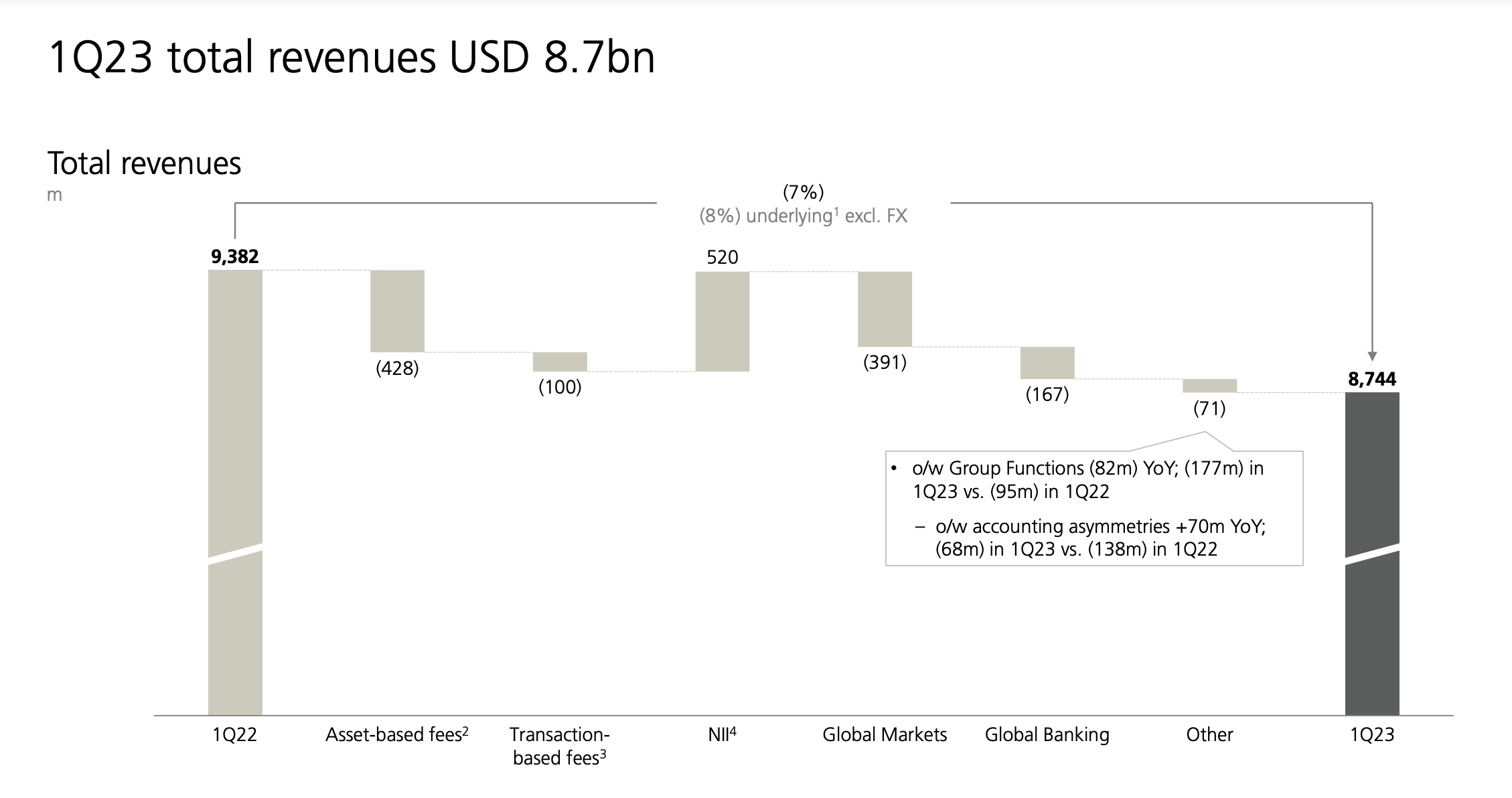

Year over year, the picture regarding UBS Group has definitely worsened. But then again, considering all that is transpiring in the banking sector, it would have been peculiar if the opposite had occurred. Consider revenue. Overall revenue for the company was $8.74 billion in the first quarter of its 2023 fiscal year. This represents a decline of 6.8% compared to the $9.38 billion in revenue reported the same quarter one year earlier. It was also below the $8.89 billion in revenue that analysts had forecasted .

{kind=link}

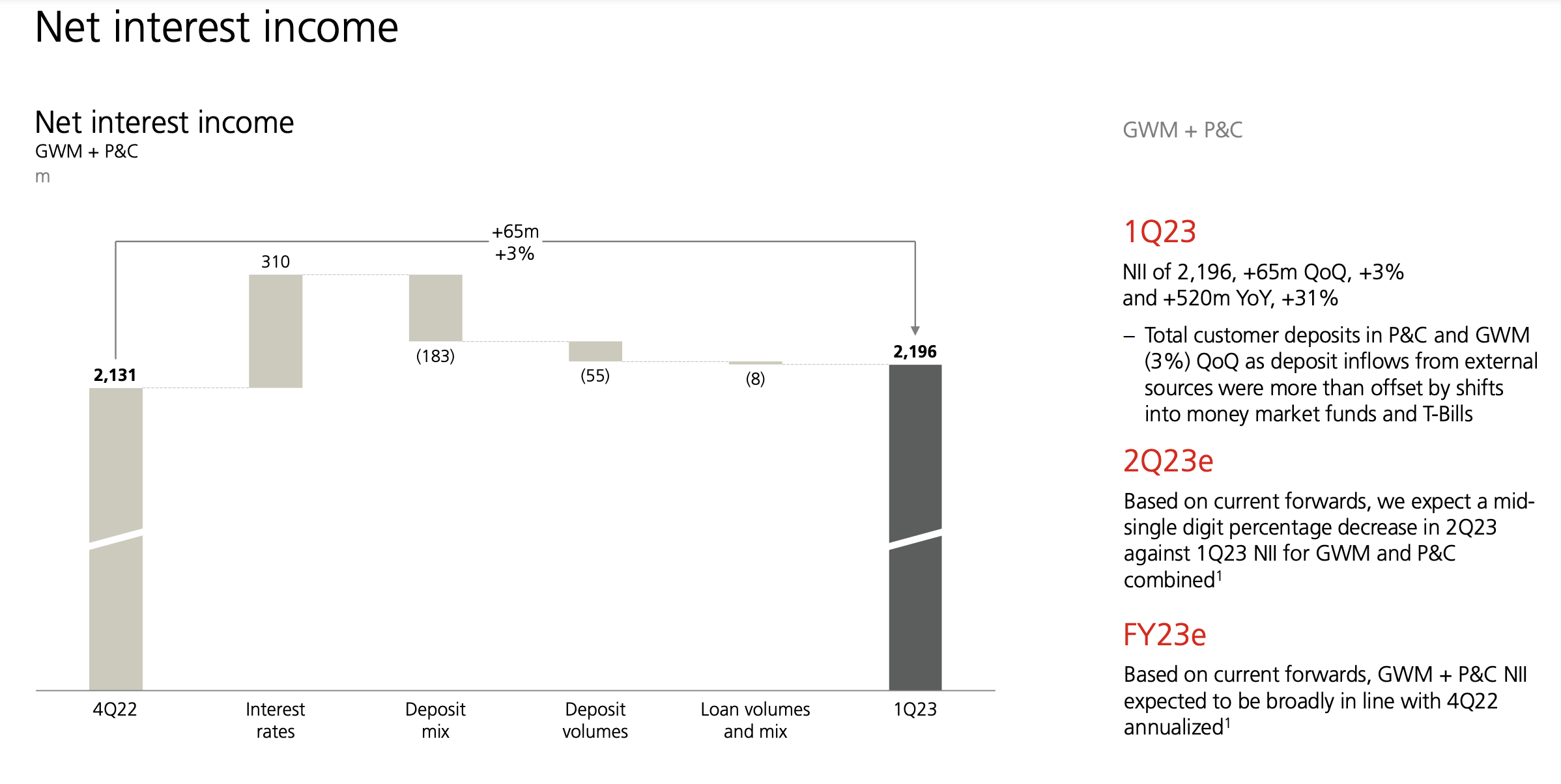

The only bright spot though the company experienced from a revenue perspective involved the net interest income it generates from its Global Wealth Management and Personal & Corporate Banking segments. Combined, net interest income from these units totaled nearly $2.20 billion. That was up nicely compared to the $1.68 billion reported the same quarter one year earlier. A rise in revenue associated with deposits, associated with higher interest rates, were helpful in pushing up net interest income under the Global Wealth Management segment. Higher deposit margins that were caused by rising interest rates, as well as higher loan revenues, pushed up the net interest income for the Personal & Corporate Banking segment.

{kind=link}

Outside of this, unfortunately, the company experienced weakness across the board. The Global Markets a side of the enterprise, for instance, saw a $391 million decline in revenue, while Global Banking was hit to the tune of $167 million. The biggest hit, however, came from asset-based fees. These plunged by $428 million year over year.

{kind=link}

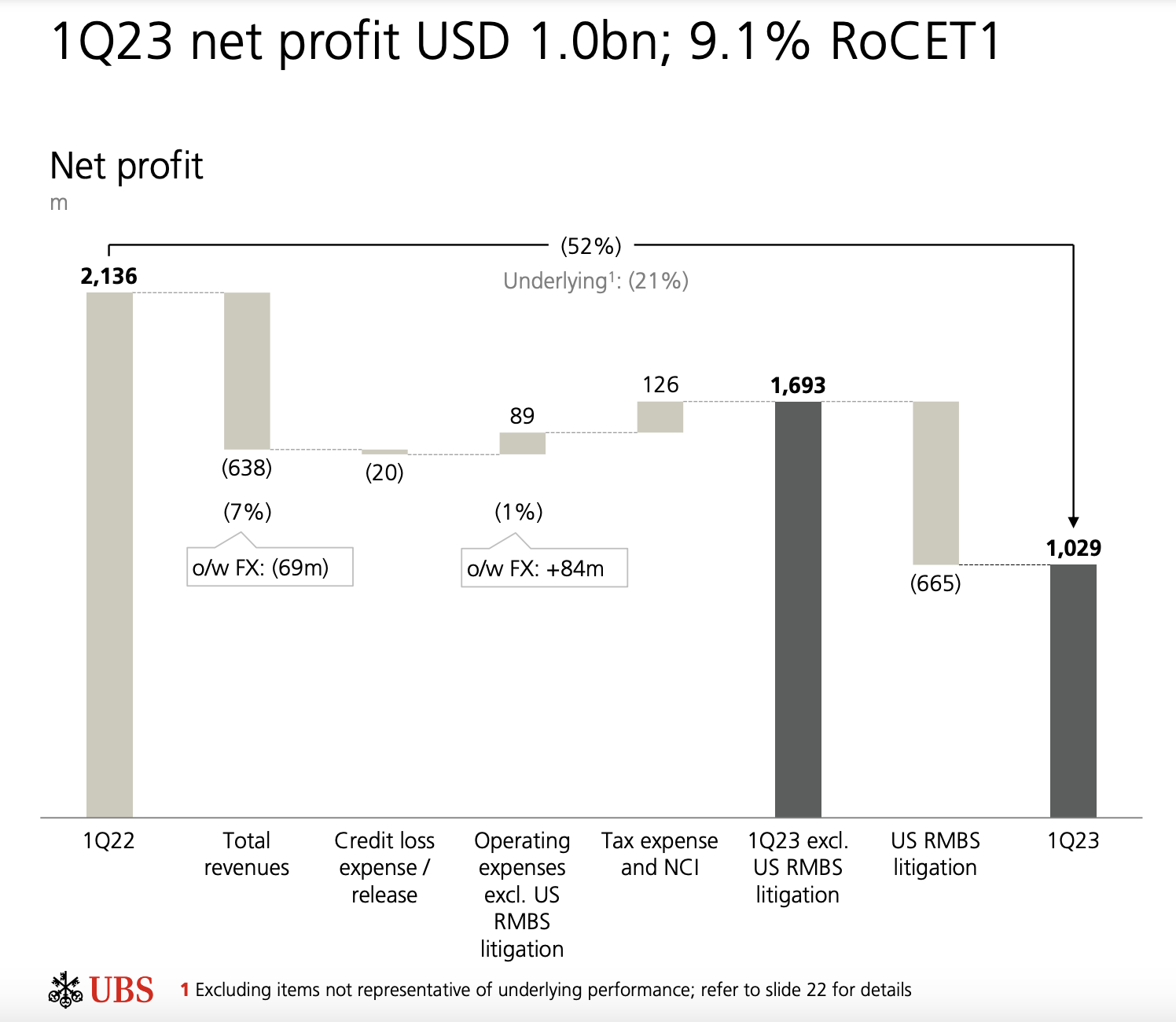

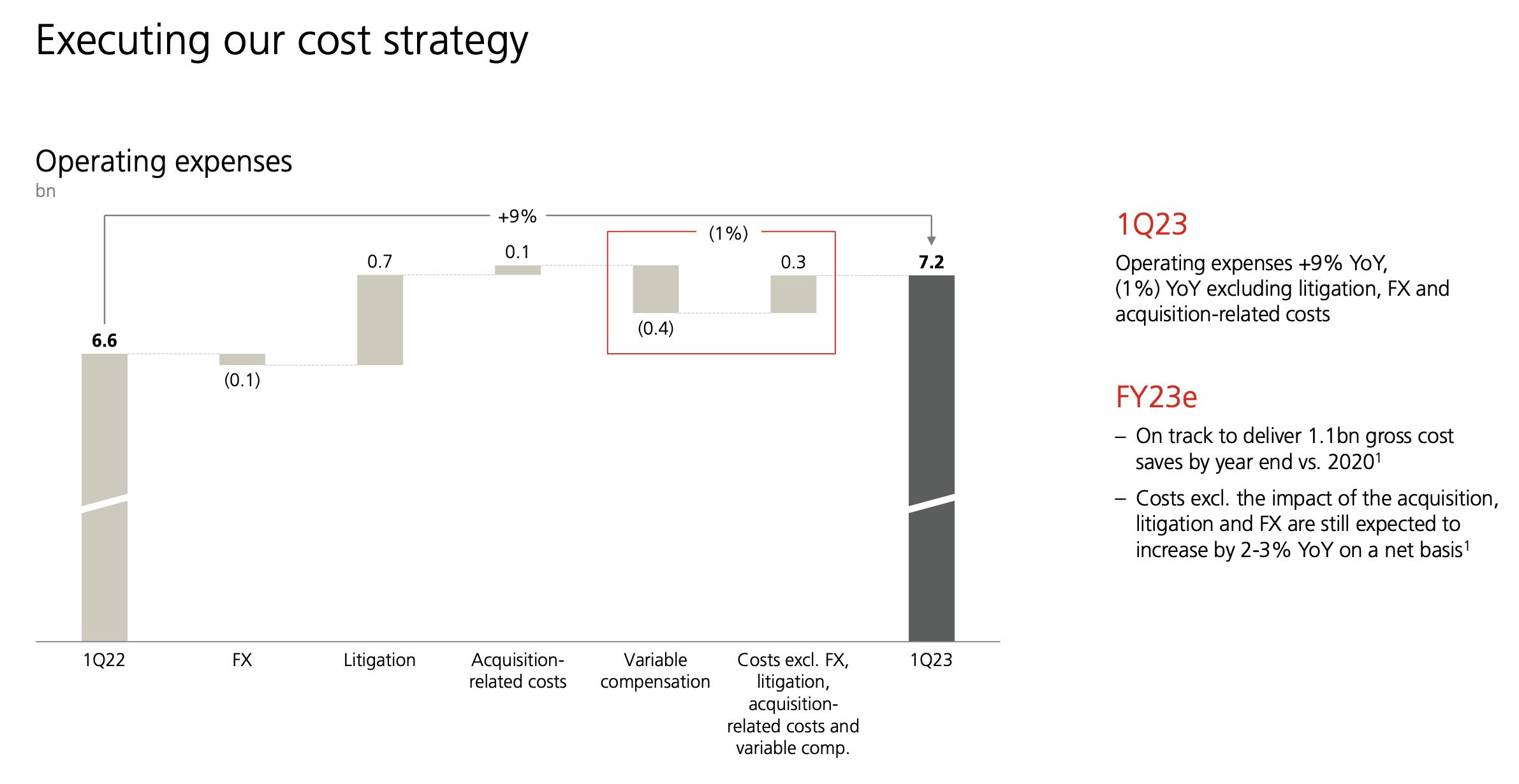

On the bottom line, the picture was also problematic. Net income for the company plunged from $2.14 billion to $1.03 billion. This took earnings per share from $0.61 to $0.32. While this looks awful, it is important to keep in mind that there were some one-time items in the picture that should not repeat themselves moving forward. Acquisition related costs impacted operating expenses by roughly $0.1 billion, while miscellaneous costs hit the company to the tune of $0.3 billion. But the biggest pain came from a $665 million litigation charge associated with the US residential mortgage-backed securities matter that the company has been dealing with. In addition to this, the company reduced variable compensation by roughly $0.4 billion year over year.

{kind=link}

{kind=link}

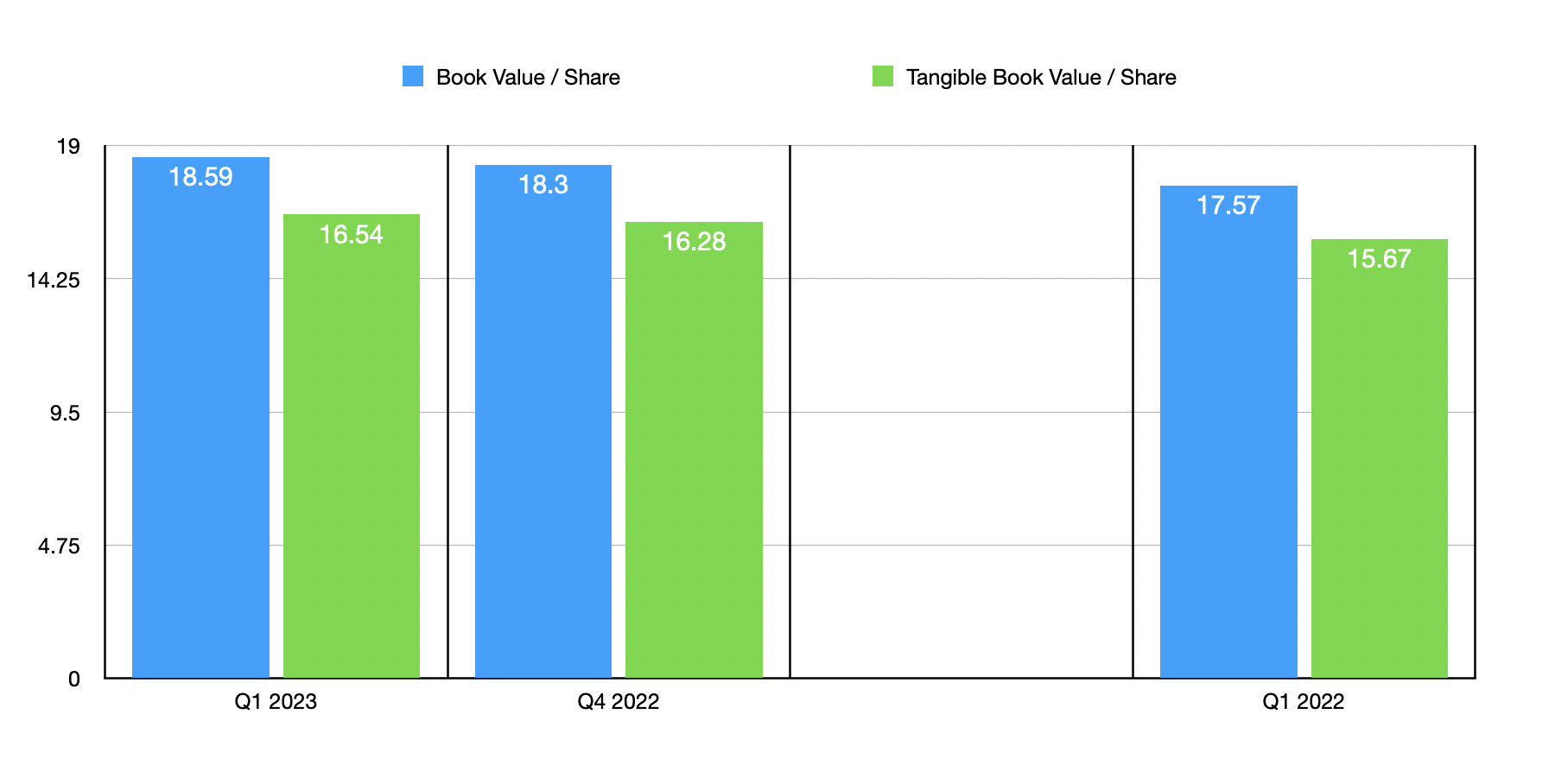

Despite the pain associated with net profits, the company did see improvements in key areas. For instance, book value per share for the company came in at $18.59. That was up nicely from the $18.30 per share reported only one quarter earlier and compared favorably to the $17.57 reported for the first quarter of 2022. As you can see in the chart below, tangible book value per share followed a similar trajectory. In addition to this, the company reported a rise in invested assets. This came in at $2.96 trillion for the quarter. Although this was down from the $3.15 trillion reported the same time last year, it was up nicely compared to the $3.82 trillion experience during the fourth quarter of last year.

{kind=link}

Outside of the earnings and revenue results experienced, the biggest pain for the company involved a decline in deposits. Overall deposits for the first quarter of the year were $505.58 billion. That represented a decline of $19.47 billion compared to the 525.05 billion seen one quarter earlier. This decline was driven by a plunge in the deposits under the Global Wealth Management portion of the company from $348.2 billion to $330.3 billion. One year ago, customer deposits were even higher at $372.3 billion. This decline in deposits was, according to management, largely driven by customers shifting their assets into money market funds and T-Bills as they seek for higher yields in this inflationary environment. Although it is worth noting that a bright spot was the Personal & Corporate Banking segment where deposits of $180.5 billion came in slightly higher than the $180 billion reported one quarter earlier and the $174.8 billion seen the same time last year.

{kind=link}

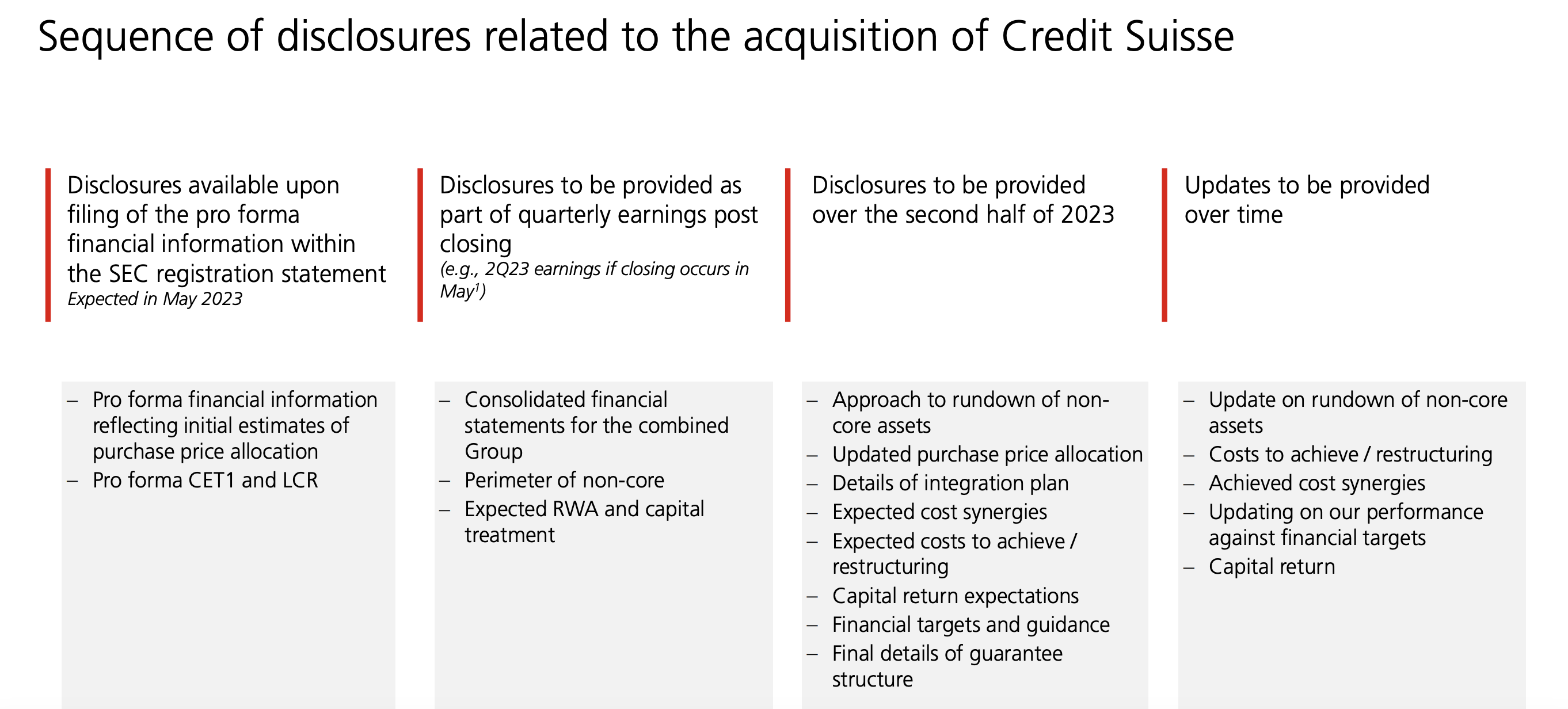

Of course, the big elephant in the room right now is the company's pending acquisition of Credit Suisse. This is likely very top of mind since the beleaguered bank reported the other day that asset outflows experienced during the first quarter of the year totaled $68.6 billion. Even as late as April 24th, the outflows had not yet shown signs of reversal, even though they did show signs of stability. Although I will not rehash the details of that transaction since I did write about it in great detail in another article , I do believe that UBS Group remains committed to the deal. Even in its investor presentation, the company talks about what it will look like once the merger is completed. For instance, it states that it will be the second largest wealth manager globally upon completion of the deal. And it will also be the third largest European asset manager, as well as the 11th largest global asset manager, after it absorbs its smaller rival. As of this moment, there is no evidence that the deal will fall through. In fact, the company even provided a rough timeline of what the picture should look like moving forward.

Takeaway

Based on all the data provided, I must say that UBS Group strikes me as a rather solid player in this environment. Yes, the firm did experience some weakness in some very important areas. But it would have taken a miracle for it not to in this environment. All things added together, the company strikes me as a quality player and a prospect that should continue to exhibit stability for the foreseeable future. And as such, I would argue that the company makes for a valid 'buy' candidate at this time.

For further details see:

UBS Group Q1 Earnings: Expected Weakness Shows How Resilient Business Is