UBS - UBS Swallows Credit Suisse: More Holes Than Cheese

2023-03-20 11:23:17 ET

Summary

- UBS finally bought Credit Suisse for arguably next to nothing.

- When considering that the Swiss regulator FINMA wrote off AT1 bonds, the purchase price is even lower.

- However, early projections by UBS prepare its shareholders for a tough period ahead, as the transaction will be EPS accretive only in 2027.

- While uncertainties are still huge, there are indications that UBS made a bargain purchase.

More holes than cheese

After a long stretch of scandals, missteps and capital destruction, what is left over from the old Credit Suisse ( CS ) is probably best compared to a piece of Swiss cheese, but with so many holes that you have to look hard for anything edible.

In fact, UBS ( UBS ) is getting its competitor right across the Zürich Paradeplatz close to nothing: While it will pay CHF 3B in an all-stock deal , it will get more than what had traded for north of CHF 8B as recently as a few days ago, since the repayment of the CS AT1 bonds will be eliminated – which means a whopping CHF 16B less to pay out for the future owner.

Moreover, there will be significant public liquidity support and some insurance-like loss coverage by the government: Both banks involved will have access to Emergency Liquidity Assistance of CHF 50B plus another CHF 100B of additional liquidity support provided by the Swiss central bank SNB. If I heard that right during the press conference, interest on the amounts drawn would apparently be only 1.5%.

To insure UBS against unforeseeable legal and financial risks, only the first CHF 5B of losses will be borne by UBS itself, the next CHF 9B will be shouldered by the government and any further losses will be shared equally by the new owner and the government.

This agreement highlights the enormous uncertainties hiding in this apparently great deal for UBS.

On the one hand it gets its former competitor's Swiss business (which, contrary to early speculation, won't be spun off due to competitive concerns) that was said to be worth around CHF 15B alone, plus an acceleration of its own asset management business, but on the other hand it will have to deal with all kinds of troubles hiding inside the acquired toxic investment banking division. As a reminder, within less than two months in 2021 this division was capable of accumulating a total of $15B exposure to two of the largest financial scandals in recent history: Greensill and Archegos. Will there be more of this kind? Who knows.

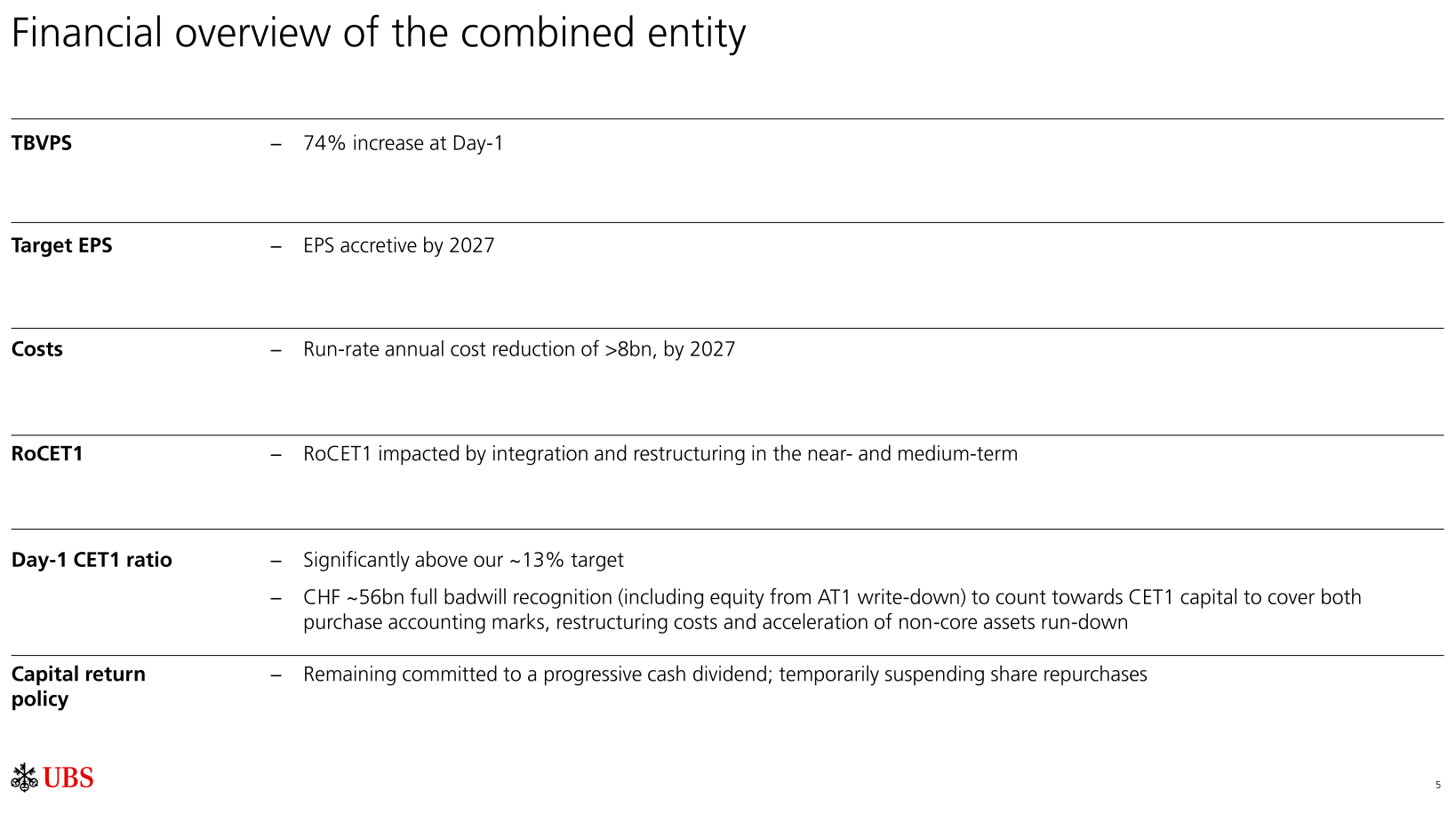

Shareholders will need to be patient, as first of all there will be costs to bear. Only in 2027 the new owner projects the first EPS accretion from the transaction.

Transaction overview (UBS presentation)

{kind=link}

Four years is a long time. The deal will likely bring a lot of distraction to management and employees, many of which will inevitably lose their jobs, as the new owner projects to save $8B of operating expenses by 2027. There will be dyssynergies, given that some clients which had spread their money over two different institutes will need to move some assets away from the merged entity. And there will inevitably be a series of bad news releases in my view.

Clearly, the goal of this deal was not to give a bargain to UBS, but to save the reputation of the Swiss banking system and economy. This was highlighted by the participation by none other than the Swiss President himself during the press conference presenting the transaction. Politicians were also scrambling to present the deal as a "private market solution", i.e. not a despicable "public bailout". This is true only if the "hidden skeleton" losses for UBS won't exceed the CHF 21B limit (CHF 16B of AT1 bonds erased today plus CHF 5B of own loss allowance). On the other hand, any other sort of transaction would have become far more costly to taxpayers: Injecting taxpayer money into Credit Suisse or letting it fail. While Swiss newspapers are already complaining in pretty bad terms about the current solution, I doubt the language would have been softer if one of the other two available solutions would have been chosen.

Why UBS might have made a bargain

Given this situation, UBS obviously entered the negotiations from a pretty strong position. I believe it knew perfectly well that any other solution than a merger would have had dramatic consequences for Switzerland as a whole and for the worldwide financial system. (It remains to be seen, though, whether the current solution will really save the ship).

The fact that it openly declined any interest in acquiring CS just a few days ago, might have been just posturing.

One detail probably shows how strong UBS' hand was: It can keep its former competitor's Swiss business. This would have been easy to spin off, but UBS managed to get a pass despite very justified competitive concerns. If the CS franchise was worth CHF 15B while having UBS as a competitor, it is certainly worth more now.

If we want to be optimistic on UBS, we can also consider that the 2027 profitability target could easily be a low-ball estimate together with the $8B cost efficiencies. Why would UBS tell the other folks involved the full synergy potential right away? Especially since cost savings involve a lot of job cuts, which are obviously not even in the interest of politicians. Only UBS can really know these figures and it would be terribly dumb to reveal its true estimates today. Just to make an example, UBS could cushion the impact of future negative news relating to the deal by announcing greater than expected cost efficiencies. And it could justify the necessity of further job cuts by pointing to additional risks and costs emerged in the meantime. So it is probably best to consider those profitability and synergy estimates not only as moving targets, but as politically useful targets which can be adapted to different situations.

If we want to be even more bullish, we can infer that the large state guarantees might just be in place to highlight potential risks to the public and CS shareholders to justify the low offer (actually UBS started by offering a third of the final tally). UBS could easily get away with a much lower cost. After all, the problems at CS were mainly liquidity and trust, leading to large capital outflows. Hence, a CHF 21B allowance for losses might abundantly cover the effective risk.

The suspension of share repurchases points into the same direction: It would not have been politically palatable to repurchase shares in this situation. At least apparently, UBS needs to keep large capital buffers. (But it won't suspend or cut its dividend and intends to keep its "progressive" dividend policy.)

The slide presentation includes an estimate of tangible book value accretion: On day one, the new UBS will enjoy a 74% increase of its TBVPS. While not all of this will be as profitable as the old UBS's tangible capital, it will certainly still earn a ton of money.

Overall, I tend to believe that UBS made a bargain purchase. Due to merger-related costs and some "skeletons" in CS's closet, it might suffer for some time, its ROE might go down for a few years, but overall it is quite hard to imagine that this deal turns out to be value-destructive for the acquirer.

But I admit that a lot of uncertainty remains, especially since we don't know if there will be other dominoes to fall and whether the capital markets will believe that this solution is really a solution. After all, people were withdrawing deposits from CS at breakneck speed until Friday. UBS credit default swaps are already rising . Nobody is out of the woods yet.

The issue with AT1 bonds

Finally, analysts were surprised to see AT1 bonds wiped out, while shareholders still get some money. Weren't these bonds supposed to be senior to equity? In this case, actually not, according to the term sheet they were at the mercy of FINMA's determinations. That said, the decision is not without risks. The loss of CHF 16B amounts to about 6% of the total amount of AT1 bonds outstanding from all European banks. There will certainly be some contagion: Part of these bonds might have been insured by other institutions, part might have been purchased by other banks, and – last, but not least – the overall market of AT1 bonds might be impacted, as investors will likely demand higher yields for these instruments going forward. And this will reduce profitability ratios for banks.

To buy or not to buy

So is UBS a buy? My hunch is yes. However, significant uncertainties remain related to the acquired liabilities and legal risks, but also to the overall stability of the global banking sector. If, one week from now, we are discussing yet another failing systemically relevant bank somewhere in the world, if U.S. regional banks continue to be under pressure, today's transaction might not bring much relief to share prices. UBS is down ~20% from its recent peak and trading for just 8x forward earnings with a ~3% dividend yield. It enjoys a ROE growing year after year and currently north of 13%, so it would be a buy on its own – in a stable environment. In the midst of a full-blown global banking crisis and after having taken over a "bad bank" probably not. So for me there is just not enough visibility to buy the stock.

For further details see:

UBS Swallows Credit Suisse: More Holes Than Cheese