UFPI - UFP Industries: An Antifragile Business Model Built For The Long-Term

2023-12-29 10:01:10 ET

Summary

- Due to short-term economic headwinds concerning the construction sector, UFPI trades at a discount to the market and its own history.

- UFP Industries has a long growth track record, a decentralized business model, and an attractive valuation.

- The company's structural advantages, strong management, and robust financial performance make it an attractive investment opportunity.

- Taking its net cash into account, UFPI trades at a 10% free cashflow yield, which is very attractive for a company of this quality.

Editor's note: Seeking Alpha is proud to welcome David Diranko as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

With a 30-year history as a public company, UFP Industries ( UFPI ) has a long growth track record with high returns on capital. This track record compounded shareholder value at 13.4% annually.

My investment thesis assumes that the experienced management team can use the same playbook to do "more of the same" and continue their past performance for a long period.

UFPI's decentralized business model, resilient balance sheet, and disciplined capital allocation provide plenty of room to grow in a fragmented market.

At a 10% free cash flow yield, the stock is attractively priced and I rate it as a buying opportunity.

Business and Market

UFPI is a US-based manufacturing company that operates a balanced business model through three main subsidiaries within the construction and industrial sector.

The first business unit is UFP Construction (UFPC). At its core, UFPC supplies homebuilders with site-built and factory-built homes but increasingly diversifies across other parts of the construction market.

The second business unit is UFP Retail Solutions (UFPR). Mr. Matthew Missad, CEO of UFPI, described UFPR in his Q3 2023 earnings call "as a value-added manufacturer, seller, and self-distributor, [...] [UFPR] provides solutions to the DIY consumer as well as the professional contractor".

The final business unit is UFP Packaging (UFPP), a leading US provider of industrial packaging. Operating in a fragmented market, the long-term ambition of UFPP is to become " the world's largest packaging company ".

Looking at revenue contribution, UFPR is the largest unit with 2022 net sales of $3.7B and $150M in operating profit. However, considering operating profit, UFPP is the most profitable unit with $2.4B in net sales and $340M in operating profit. UFPI's corporate strategy emphasizes balancing all three business units to navigate the cyclical nature of the construction market.

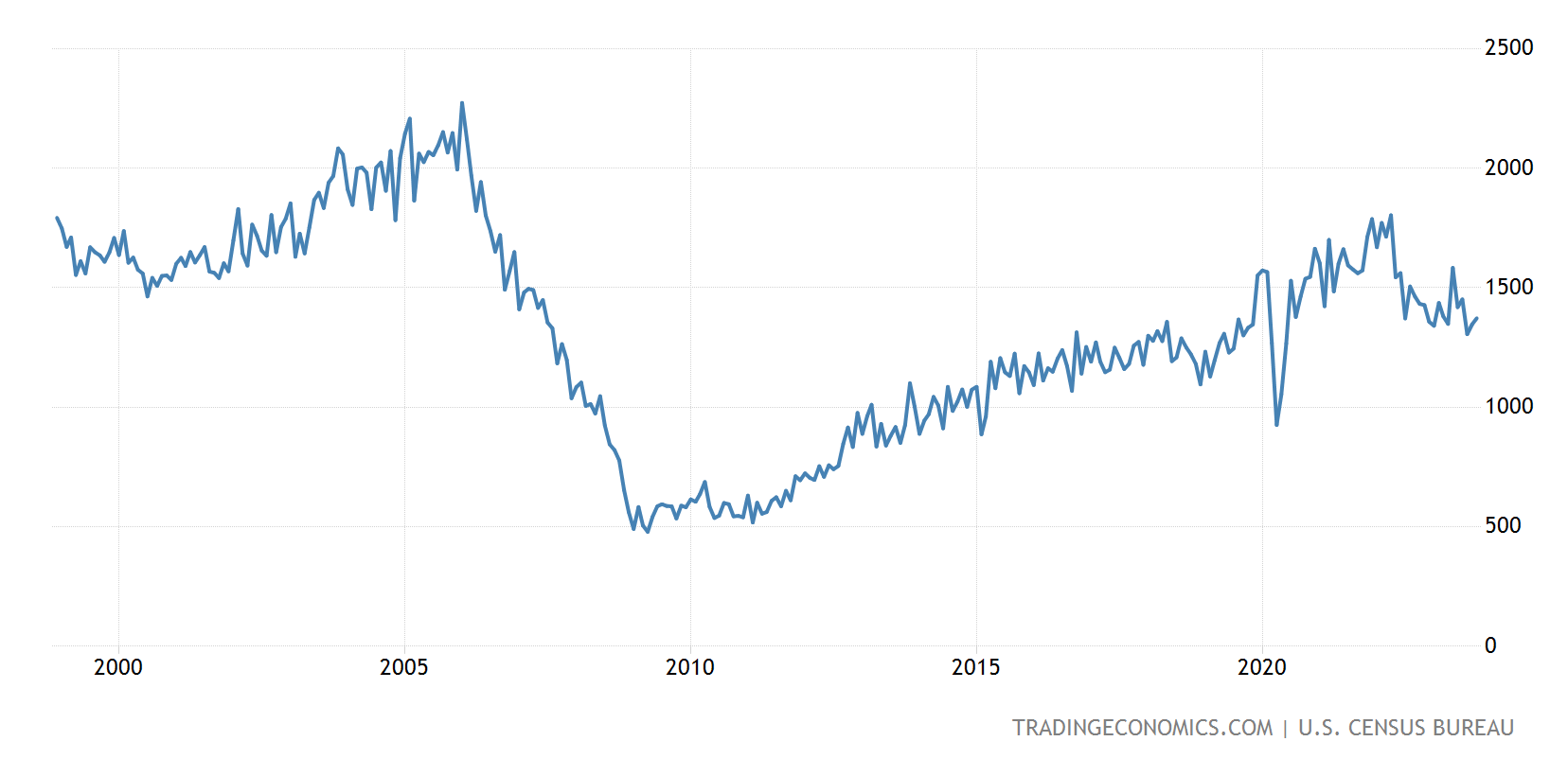

Although being highly cyclical, there are two major long-term developments within the construction market favorable to UFPI. First, beginning with the 2008 global financial crisis, the US has underbuilt new homes. The chart below shows US housing starts since 1998:

US housing starts since 1998 (Tradingeconomics.com)

{kind=link}

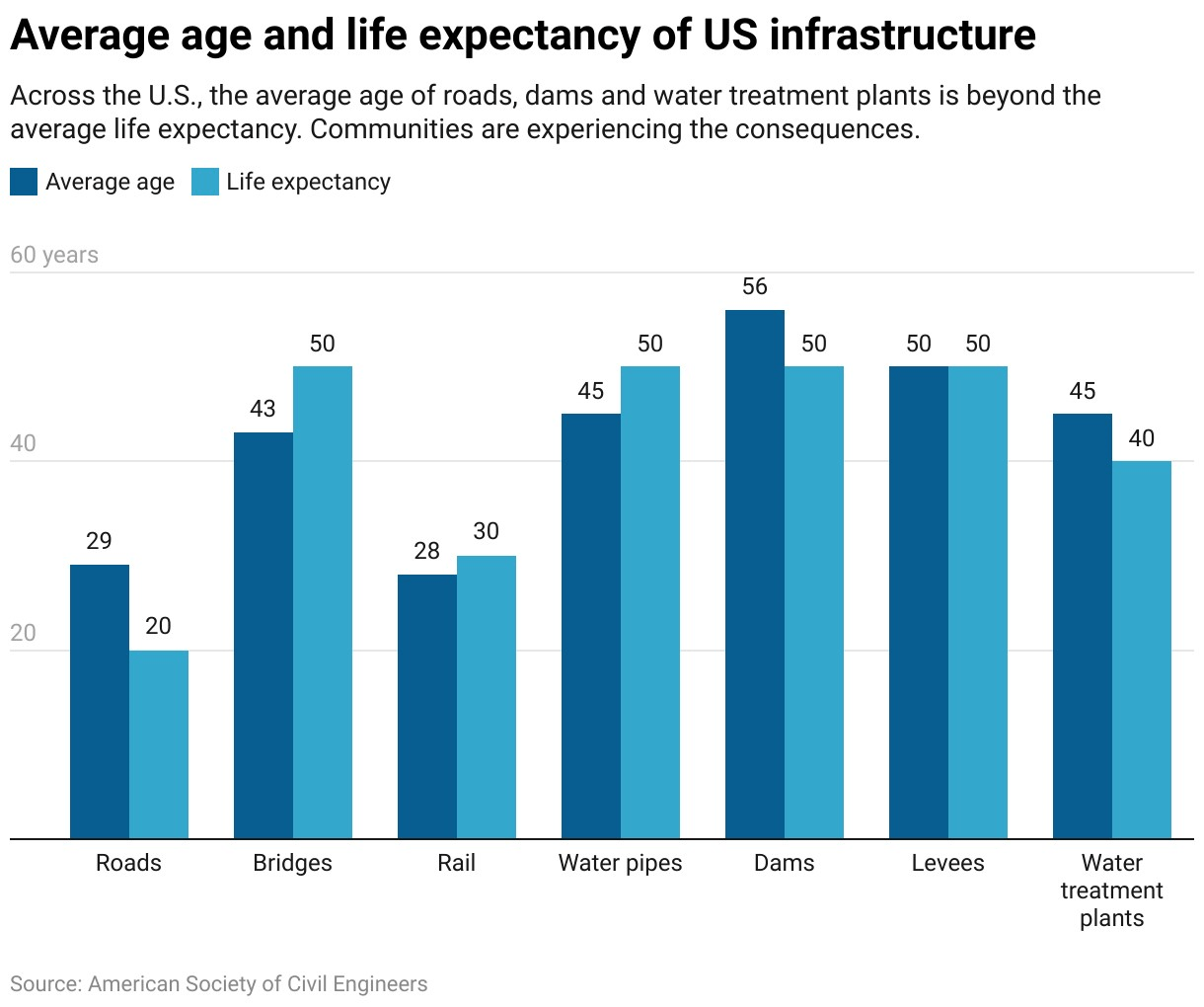

Second, the US government has underprioritized spending on public infrastructure. The following chart shows the average age of major parts of the US infrastructure:

Average age and life expectancy of US infrastructure (American Society of Civil Engineers)

{kind=link}

An acceleration in homebuilding activities combined with increased spending on public infrastructure provides long-term tailwinds to the core end markets of UFPI. On the contrary, rising interest rates raise mortgage rates and may slow the economy. Both factors have negative effects on homebuilding activities and represent a major downside to UFPI's business.

My investment thesis does not require favorable short-term macroeconomic developments as it centers around three long-term structural advantages of UFPI. Combined with the cyclicality and high fragmentation of UFPI's three core markets, I expect these structural advantages to result in a long runway for profitable growth and high returns on capital.

The first structural advantage of UFPI is its focus on value-added products with the additional internal target to generate 10% of annual revenues by new products. Over time, disciplined innovation shifts the product mix towards value-added products rather than commodity lumber. From 2013 to Q3 2023, the share of revenue from value-added products increased from 58% to 68%. This shift in the revenue mix comes at the benefit of gross margins expanding from 11.4% in 2013 to 18.6% in 2022.

Management

The second and third structural advantages are more about UFPI's organizational strengths than the construction market or its products. Hence, I will discuss these aspects within the management section.

The second structural advantage is UFPI's culture. UFPI fosters people development through its corporate business school , offering employees a two-year program to earn a Bachelor of Business Administration. The fully funded program equips UFPI employees with essential financial and management skills, preparing them for leadership roles. Furthermore, UFPI operates an innovation accelerator and a venture fund to drive entrepreneurship and innovation inside the company. The internal development program has already yielded results, evident in the average tenure of UFPI's 65 most senior leaders, which stands at 22.3 years.

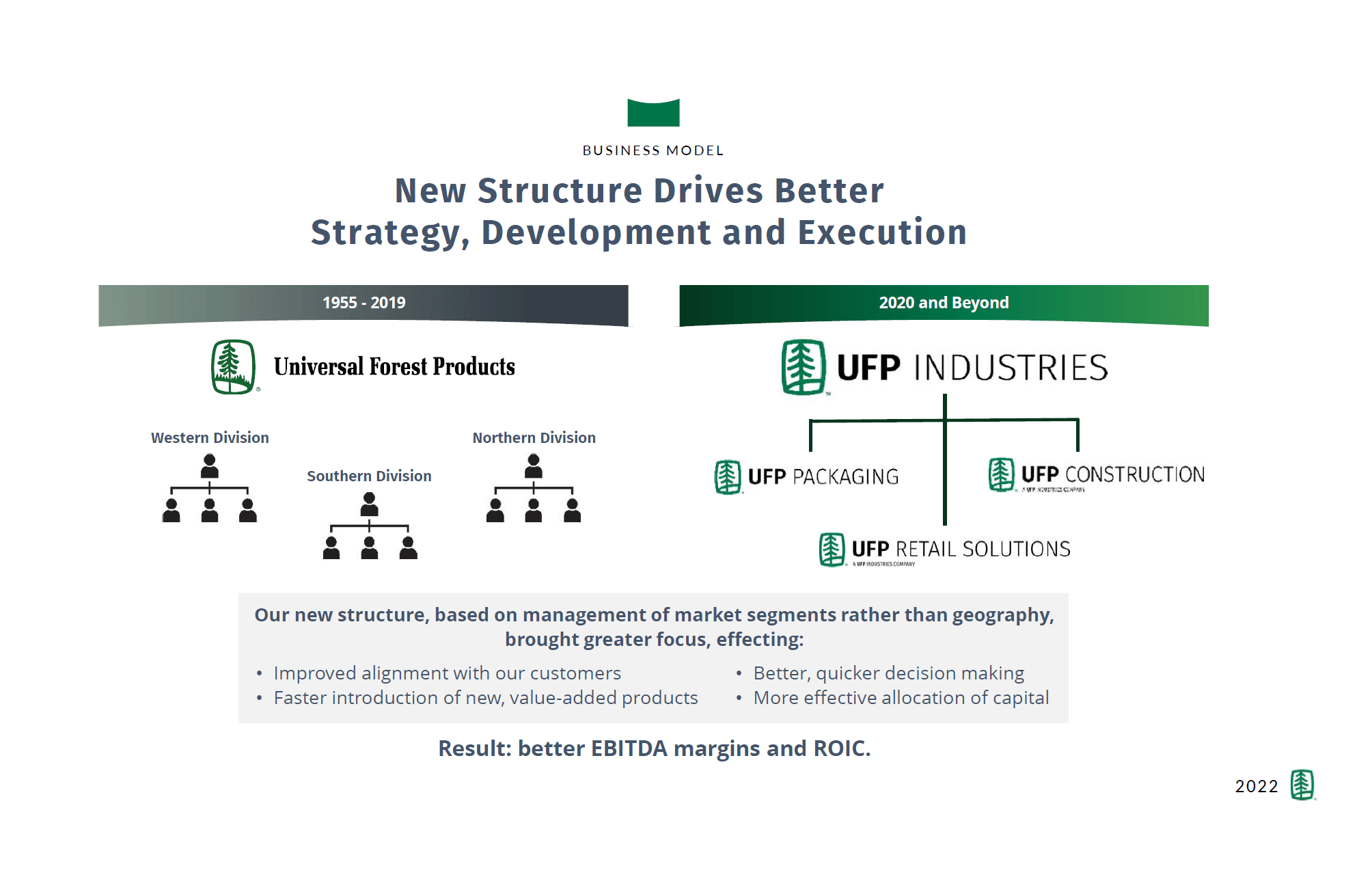

The third structural competitive advantage is UFPI's hard-to-replicate organizational structure. The structure consists of a balanced business model within a decentralized structure, supported by a strong balance sheet. Though in development for several years, UFPI's organizational structure underwent acceleration through corporate restructuring in 2020. As of 2020, UFPI reorganized its business units, transitioning from geographical to market segment-based organization, as outlined on the following slide:

UFPI organizational structure (Q4 2022 earnings call presentation UFPI)

{kind=link}

Organizing the business units by markets leverages operational efficiencies through consolidation and sharing of best practices. Additionally, it reduces unnecessary operational overhead while driving product innovation and decision-making, as well as customer servicing. These operational efficiencies led to increasing operating margins from 5.5% in 2019 to 9.8% in 2022. Additionally, UFPI adopted a decentralized business model, where each of their 222 operations is a profit center, managed by people who are required to own stock, and are compensated on a combination of pre-bonus operating profit and return on investment. This policy ensures strong alignment between management and shareholders, resulting in high insider ownership. As of the annual proxy statement from March 2023, the executive board holds 3.55% of the shares outstanding, with Mr. Missad alone owning approximately 0.9%. Additionally, the business boasts a robust balance sheet with $682M in net cash.

In my mental model, UFPI's organizational structure exhibits characteristics of what Nassim Taleb refers to as "antifragility" . Antifragility describes the properties of a system to benefit from chaos and adversity. Maintaining antifragility may limit upside during favorable periods but empowers the system or company to thrive in challenging times, where others may struggle.

Concluding the discussion on management, I want to highlight the high level of integrity in UFPI's management. With only five CEOs in its 68-year history, UFPI demonstrates a strong commitment to stable leadership . The current CEO, Mr. Missad, joined UFPI full-time 38 years ago, underscoring the company's enduring corporate governance. Additionally, he openly acknowledges the limits of his circle of competence. Concerning the state of the US economy in his Q1 2023 earnings call , he quoted Machine Gun Kelly: "All I know is I don't know nothing. People talk and they don't say nothing."

Downside Risk

The primary risk is a significant downturn in the US construction market, akin to the 2008 recession. This could severely affect UFPI's cash flows and, consequently, its stock performance.

Financials

Building on the robust balance sheet, it's noteworthy that UFPI, with its balanced business model, has never incurred losses in its 30-year history as a public company. The synergy of UFPI's three structural advantages contributes to consistently high returns on capital. From 2019 to 2022, the ROIC has climbed from 12.7% to 26.4%. While 2022 may represent a cyclical peak, the company's internal hurdle rate of 20% suggests a sustainable ROIC level.

Despite UFPI's recent impressive financial results its main downside potential is the cyclicality of the construction industry. While a cyclical downtrend could severely impact UFPI's financials in the short-term, I claim that it is insignificant to UFPI's long-term performance and may even be beneficial.

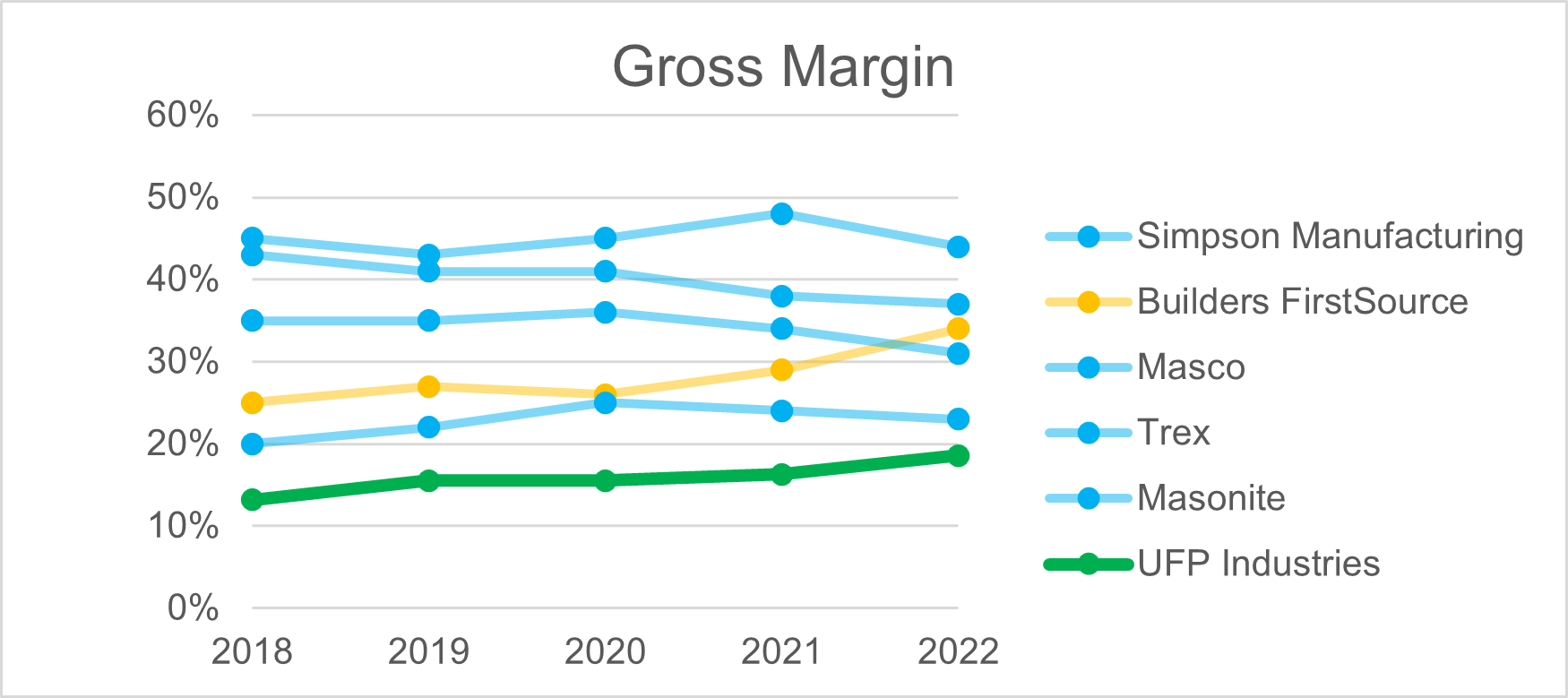

To verify my hypothesis, I benchmarked UFPI's performance since 2018 against a basket of companies operating in similar markets:

- Simpson Manufacturing ( SSD )

- Builders FirstSource ( BLDR )

- Masco ( MAS )

- Trex ( TREX )

- Masonite ( DOOR )

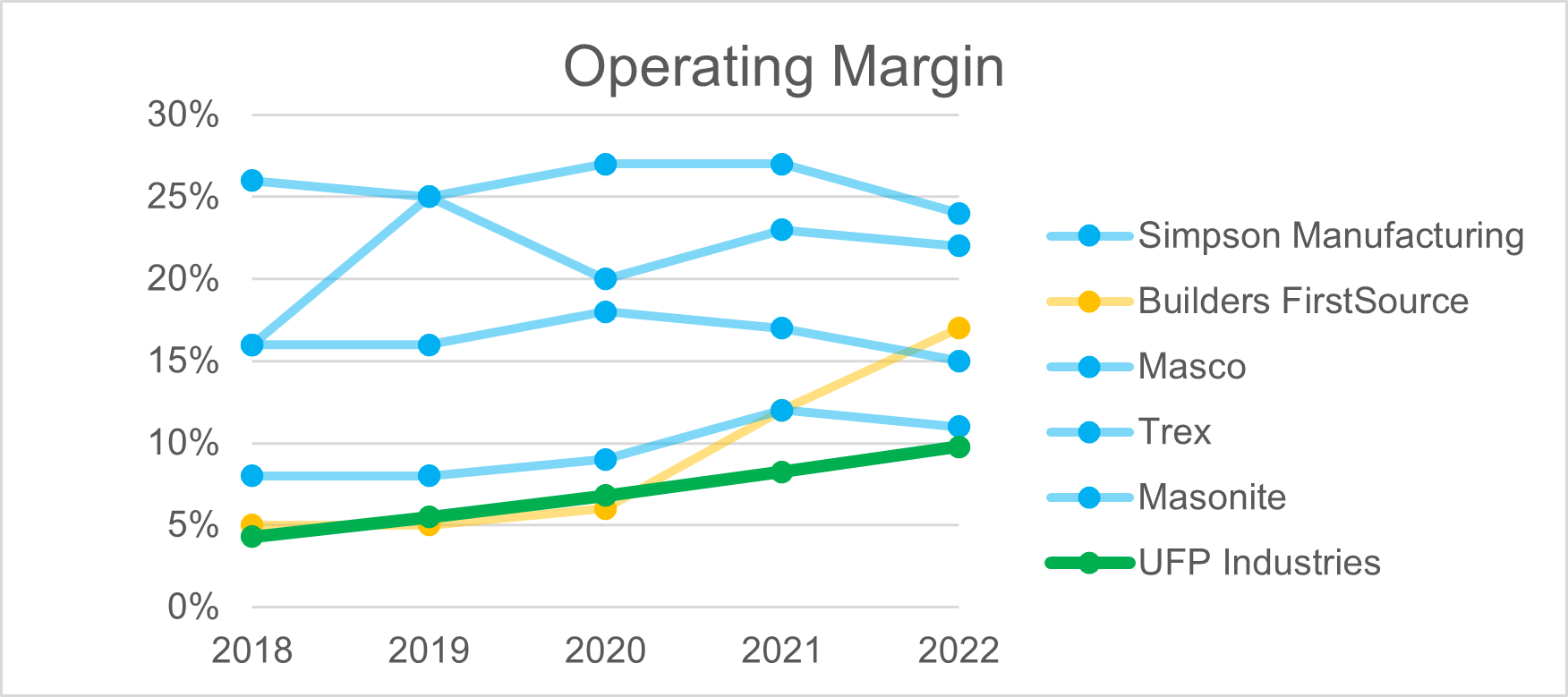

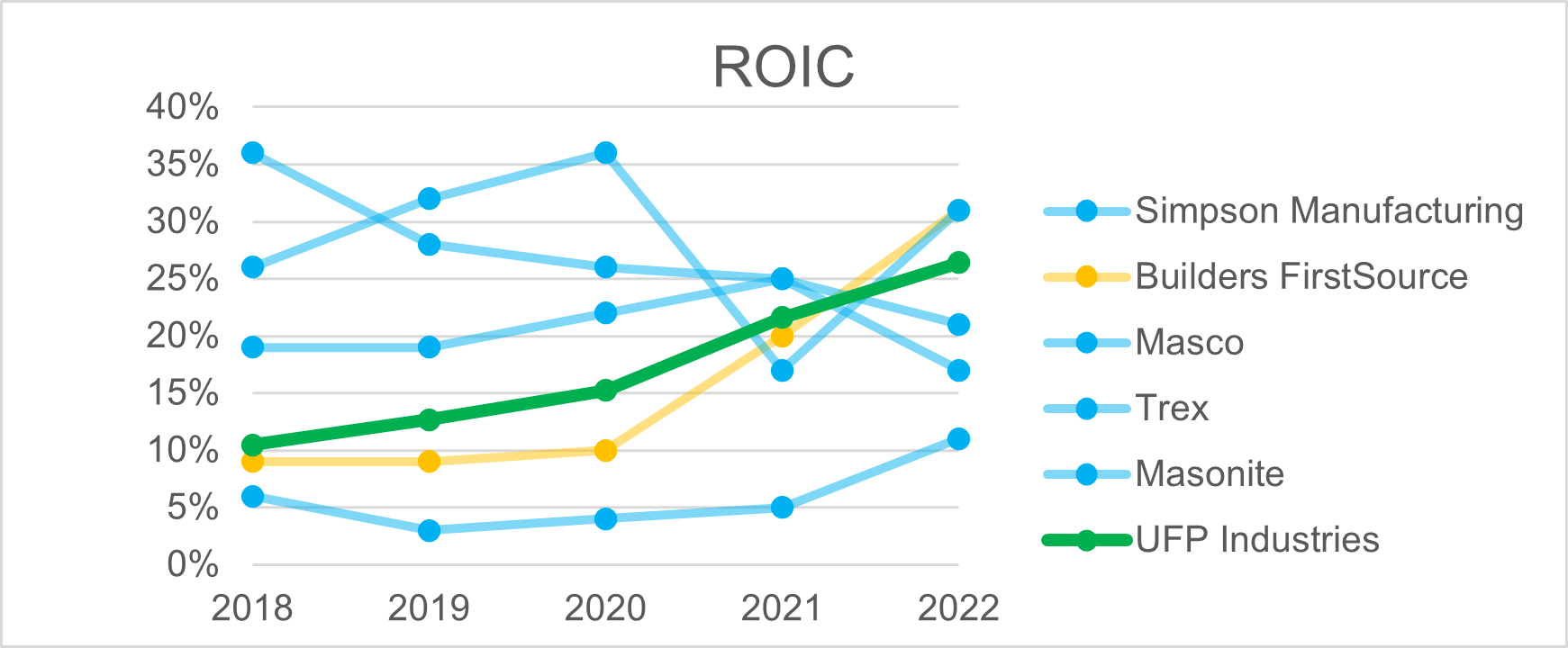

As key performance indicators (KPI), I assessed ROIC, gross margins, and operating margins. The trends in these KPIs are summarized in the charts below:

Gross margin development of UFPI and its peers (Created by Author) Operating margin development of UFPI and its peers (Created by Author) ROIC development of UFPI and its peers (Created by Author)

{kind=link}

{kind=link}

{kind=link}

Despite UFPI's peers initially having higher gross and operating margins, it's evident that the corporate restructuring in 2020 significantly elevated UFPI's margins, contrasting with the stagnant or slightly decreasing margins of most competitors. UFPI's robust margin development also led to an improved ROIC, surpassing most peers over the same period.

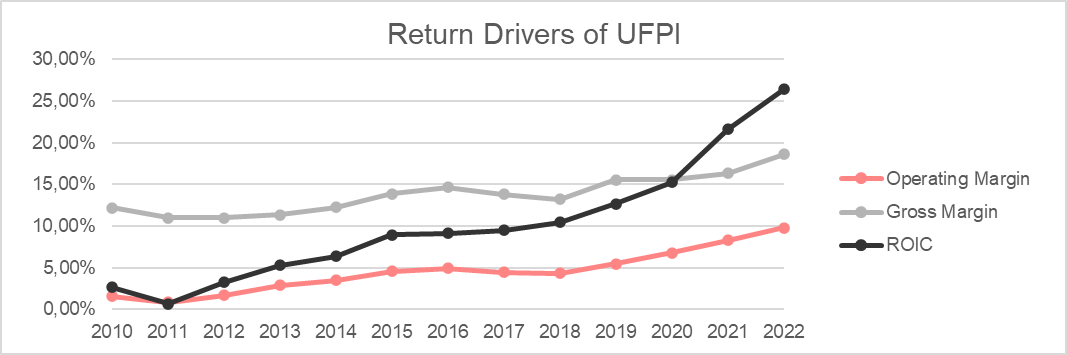

Given that only one of UFPI's peers, Builders FirstSource, exhibits a similarly positive financial trajectory, I conclude that a cyclical upturn cannot be the primary factor explaining UFPI's recent strong performance. In my assessment, it is the outcome of the antifragile business model combined with a disciplined approach to capital allocation. While I extensively discussed UFPI's business model, I'd like to spend some words on capital allocation. Illustrated in the chart below, UFPI's management team has adeptly allocated capital over the past decade, steadily enhancing the ROIC from 3.2% in 2012 to 26.4% in 2022.

Return drivers of UFPI (Created by Author)

{kind=link}

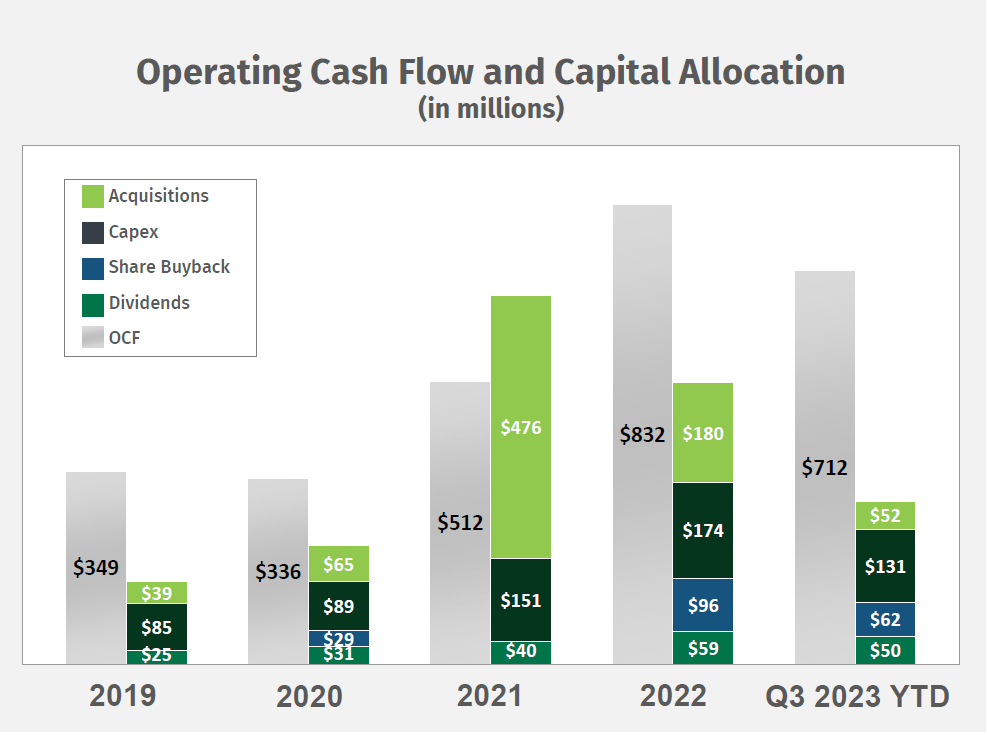

This track record stems from a disciplined capital allocation approach comprising three pillars, CAPEX, acquisitions and return of capital to shareholders, as illustrated in the slide below.

UFPI's capital allocation (Q3 2023 earnings call presentation of UFPI)

{kind=link}

CAPEX activities are focussed on four key areas, expansion of manufacturing capacity, geographic expansion, achieving efficiencies e.g. through automation and increasing transportation capacity to transform this function from a cost center to a profit center.

The second pillar involves acquisitions. Between 2012 and the end of 2022, UFPI acquired 50 businesses for approximately $1.1B, with the acquired companies generating total revenues of around $2.4B. Although the company does not disclose specific EBITDA numbers, assuming the disclosed internal target EBITDA margin of 10%, UFPI paid an average of 4.6x EBITDA. Upon request, the company confirmed a target range of 5-6x EBITDA for acquisitions, with allowances for high-potential opportunities.

For both pillars, encompassing CAPEX and acquisitions, the company maintains a ROIC hurdle rate of 20%, significantly surpassing its cost of capital of 10%.

If acquisition targets and internal opportunities fall short of the required ROIC level, UFPI employs its third pillar by returning cash flows to shareholders through dividends and share buybacks.

Valuation

As of December 6th, 2023, UFPI's shares trade at $115.9, valuing the equity at $7.2B and a 2022 free cash flow yield of 8.1%. The 2022 EV/EBIT is 7.3. Considering UFPI's accumulated net cash of $682M on the balance sheet and management's track record of capital allocation yielding returns above their 20% hurdle rate, I view the excess cash as an asset capable of generating an additional $136.4M in free cash flow within the foreseeable future. This extra cash flow raises the yield from 8.1% to my 10% hurdle rate.

As of the current writing, FY 2023 is not concluded, so my valuation is based on the FY2022 numbers. UFPI anticipates a revenue decline of about 10% and net earnings decline of 20% for FY2023, attributed to fluctuations in lumber prices and a slowdown in economic activity in the US. However, stability in operating cash flow and free cash flow is expected due to reductions in working capital.

To triangulate UFPI's value and derive a conservative estimate, I employed three approaches. First, I utilize an estimate for a sustainable ROE and an achievable growth rate, determining a conservative future internal rates of return ( IRR ) based on the resulting shareholder yield plus the growth rate. The second approach replicates the method but replaces ROE with ROIC. Finally, I employ a three-scenario DCF to value UFPI's equity, incorporating one pessimistic, one conservative, and one optimistic scenario for each method. The expected IRRs from all three approaches are summarized as follows:

| pessimistic |

| conservative |

| optimistic |

| ROE IRR |

| 8.1% |

| 12.3% |

| 19.5% |

| ROIC IRR |

| 8.1% |

| 11.8% |

| 19.5% |

| DCF IRR |

| 7.9% |

| 9.6% |

| 13.1% |

(source: Author's calculations)

In the ROE-based IRR analysis for the pessimistic scenario, I aligned the growth rate with the long-term inflation rate of 2%. In the conservative case, I anticipated management achieving its long-term targets of a 5-7% growth rate in units, plus a 1-3% price increase in line with long-term inflation expectations, resulting in an 8% growth rate. For the optimistic case, I assumed UFPI would replicate its compounded annual revenue growth from 2012 to 2022 at 16.7%. I considered three ROE values-11.0%, 18.7%, and 26.9%-to cover a range from pessimistic to optimistic.

For the ROIC-based IRR assessment, I utilized the same estimates as in the ROE-based approach, substituting ROE with ROIC.

My third valuation method employs a three-scenario DCF model. In this approach, I project UFPI's cash flows through one pessimistic, one conservative, and one optimistic scenario. For each scenario, I determine a fair price based on the company's cost of capital and calculate an expected IRR considering the current stock price. Across all scenarios, I apply a terminal growth rate of 2%, reflecting the long-term median ROIC for capital goods companies at 11%. UFPI's reported cost of capital is 10%, which I consider reasonable.

For the first scenario, I simulated a deep recession similar to the great financial crisis. Drawing reasonable assumptions, I used UFPI's financial performance from 2008-2011 as a proxy. UFPI would take two years until 2027 to recover to 2022 levels of revenue and profitability. Subsequently, management achieves their annual growth target of 8% at their 20% ROIC hurdle rate for five years. From 2027 to 2032, UFPI declines to its terminal state of 2% growth at the long-term industry median ROIC of 11%. I consider this scenario an extreme exaggeration, given UFPI's improved position compared to over a decade ago and the absence of excess in the US homebuilding market today. Nonetheless, in this scenario, I calculated a fair value of the stock at $89.45, representing a 23% discount to the current share price. The expected IRR given the current share price is 7.9%.

The second scenario envisions a mild recession in 2024, from which UFPI fully rebounds by 2026. Subsequently, management achieves their long-term target of 8% annual growth at a 20% ROIC for six years before entering a 5-year secular decline ending in 2032 with a 2% growth rate at an 11% ROIC. In this scenario, I calculated a fair value of the stock at $110.82, representing a 4% discount to the current share price. The expected IRR given the current share price is 9.6%.

The third scenario mirrors the second, except UFPI's management sustains their long-term target of 8% growth at a 20% ROIC for five additional years before entering secular decline in 2037. This scenario underscores the potential for long-term profitability. With just five more years of consistent execution, the fair value of the stock surges to $173.33, indicating a 50% increase over the current share price. The corresponding expected IRR, given the current share price, is 13.1%.

Conclusion

UFPI offers a highly asymmetric opportunity, with robust downside protection at approximately 80% of the current share price and substantial upside potential if the company maintains its successful track record. The antifragile business model positions UFPI to benefit from the construction cycle. Given these factors, I assign a higher probability to the upside potential than the downside, which leads to my buy rating for UFPI. In the event of a downside, the current 10% free cash flow yield provides a comfortable margin of safety.

Looking ahead, I'll monitor three key developments to support my investment thesis. If one or more of them is permanently impaired, I sell out of my position:

1. Does management sustain its disciplined approach to capital allocation?

2. Can the company continue its shift to value-added products, maintaining or expanding margins?

3. Does UFPI validate my antifragility assumption by thriving through the next downcycle?

For further details see:

UFP Industries: An Antifragile Business Model Built For The Long-Term