UFPI - UFP Industries: Improving Growth Prospects But Priced In

2023-12-27 07:32:01 ET

Summary

- UFP Industries, Inc. is expected to see an upward trend in revenues starting the back half of 2024, driven by potential rate cuts and improved demand conditions.

- The company's margins are currently under pressure due to lower volumes, but they are expected to improve as end-market demand recovers.

- However, these improving growth prospects already seem to be priced in with the stock trading at a premium to its historical valuation multiple.

Investment Thesis

While UFP Industries, Inc. (UFPI) faces near-term headwinds due to the high interest rate environment, the company's revenues should see improvement in 2024, especially in the 2H FY24, due to the high probability of multiple rate cuts next year, which should result in improved demand conditions. Further, the company is focusing on adding capacity to its Deckorators product line in the Retail Solutions segment and is pursuing large projects in the Packaging segment, which bodes well for its sales growth in FY24. In addition, the long-term tailwinds from higher homeowner equity levels and over a decade of underbuilding of new homes post the great recession of 2008 should benefit the company's repair and remodel (R&R) and new construction sales, respectively. Besides organic growth, the company has a healthy balance sheet and is well-placed to do M&As.

While there is some near-term pressure on margins due to lower volumes, as end-market demand improves and volume recovers towards the latter half of FY24, the company's margins should also see an improvement. Further, the margin should benefit from the cost-saving initiatives and a higher mix of value-added products in the long term.

While I like the company's improving growth prospects, I can't say the same regarding its valuation, which is higher than its historical averages. So, I would prefer to wait for a better entry point and have a neutral rating on the UFPI stock.

Revenue Analysis and Outlook

After seeing strong growth in FY21 and FY22, benefiting from higher lumber prices and accretive acquisitions, UFPI's sales turned negative in recent quarters. In the third quarter of 2023, the company posted a 21% Y/Y decline in net sales to $1.827 billion, caused by a 12% decline in average selling price and a 9% decline in organic unit sales. The Y/Y decrease in selling price was driven by lower lumber prices and a competitive pricing environment in certain business units.

In the Retail segment, net sales declined 16% Y/Y due to a 9% reduction in selling prices and a 7% decline in organic unit sales. The selling prices of variable-priced products declined due to lower lumber prices. Unit sales to independent retailers which, according to the company, are closely correlated with new housing starts, declined by ~22% Y/Y, while unit sales to big box customers, which are closely correlated with repair and remodel activity, grew by ~1% Y/Y.

The Packaging segment's net sales decreased 23% Y/Y due to a 16% decrease in selling prices and a 9% lower organic unit sales. This decrease was partially offset by a 2% contribution from Advantage Labels & Packaging (Advantage), Titan Corrugated (Titan), and All Boxed Up (ABU) acquisitions.

In the Construction segment, net sales declined 25% Y/Y driven by a 12% decline in selling prices and a 13% decline in organic unit sales. Organic unit sales declined 15% in site-built construction and 8% in factory-built housing businesses due to weaker housing demand brought on by higher interest rates. Organic unit sales declined 1% Y/Y in the concrete forming business and 27% Y/Y in the commercial construction, primarily due to a decline in market demand.

UFPI's Historical Revenue Growth (Company Data, GS Analytics Research)

Looking forward, while there are some near-term challenges due to the high interest rate environment, there is a light at the end of the tunnel given the expectations around interest rate cuts starting next year.

The company has good exposure to the construction market (primarily residential single-family, multi-family, and factory-built housing), and the company's UFP construction segment accounts for ~30% of its revenues. A good deal of the company's sales to independent retailers/distributors in UFP Retail Solutions is also linked to new home construction. UFP Retail Solutions accounts for ~41% of the company revenues and out of this ~64% is to Big Box retailers while 36% is to independent retailers/distributors and others.

The new residential market is sensitive to interest rates, and the upcoming interest rate cycle reversal in the latter part of FY24 should result in a good demand recovery. This market has solid long-term fundamentals and the demand-supply situation is favorable following over a decade of underbuilding of new homes after the great housing recession of 2008. While the extraordinarily high interest rate environment has caused a slowdown in this market, I believe it should see a swift recovery once the interest rate cycle turns.

The company's sales to big box retailers - Home Depot ( HD ) and Lowe's ( LOW ) - which account for approximately a quarter of its total sales, have performed well. While the sales were down Y/Y primarily due to lower lumber prices, the unit volumes sold to big box retailers were up Y/Y last quarter. This is interesting as the home retailers reported that their volumes (transaction comps) were down low to mid-single digits last quarter, indicating that UFPI is outperforming the broader repair and remodel category. I expect this outperformance to continue and with inflation slowly moderating, there is a good chance of improvement in consumer confidence as FY24 progresses, which should help demand. The long-term fundamentals of repair and remodel markets are also good, with homeowner equity levels at healthy levels. Homeowner equity is usually positively correlated with home improvement spending.

The company is also gaining good traction for its Deckorators product line and is adding capacity, which should aid long-term growth for this product line.

Finally, in the Packaging business, the company is seeing some pressure due to a general economic slowdown as a result of high interest rates and an inflationary environment. However, with inflationary headwinds slowly easing and a reversal in interest rate cycle expected next year, this segment should see a pick-up in demand as FY24 progresses. The company is also pursuing some larger projects in the packaging segment. Management expects some of those projects to start benefitting sales starting Q1 FY24 and then meaningfully add to sales towards late FY24.

So, overall I believe we are near the bottom and the company's organic sales should start improving next year, especially towards the back half of 2024, and then improve in the following years as end markets become more favorable with interest rates turning lower and inflation returning to normalized levels.

In addition, the company ended the last quarter with cash and cash equivalent of $957 mn and a net cash position of $682 mn. The company's healthy balance sheet should also help it pursue inorganic growth opportunities in the coming years.

Margin Analysis and Outlook

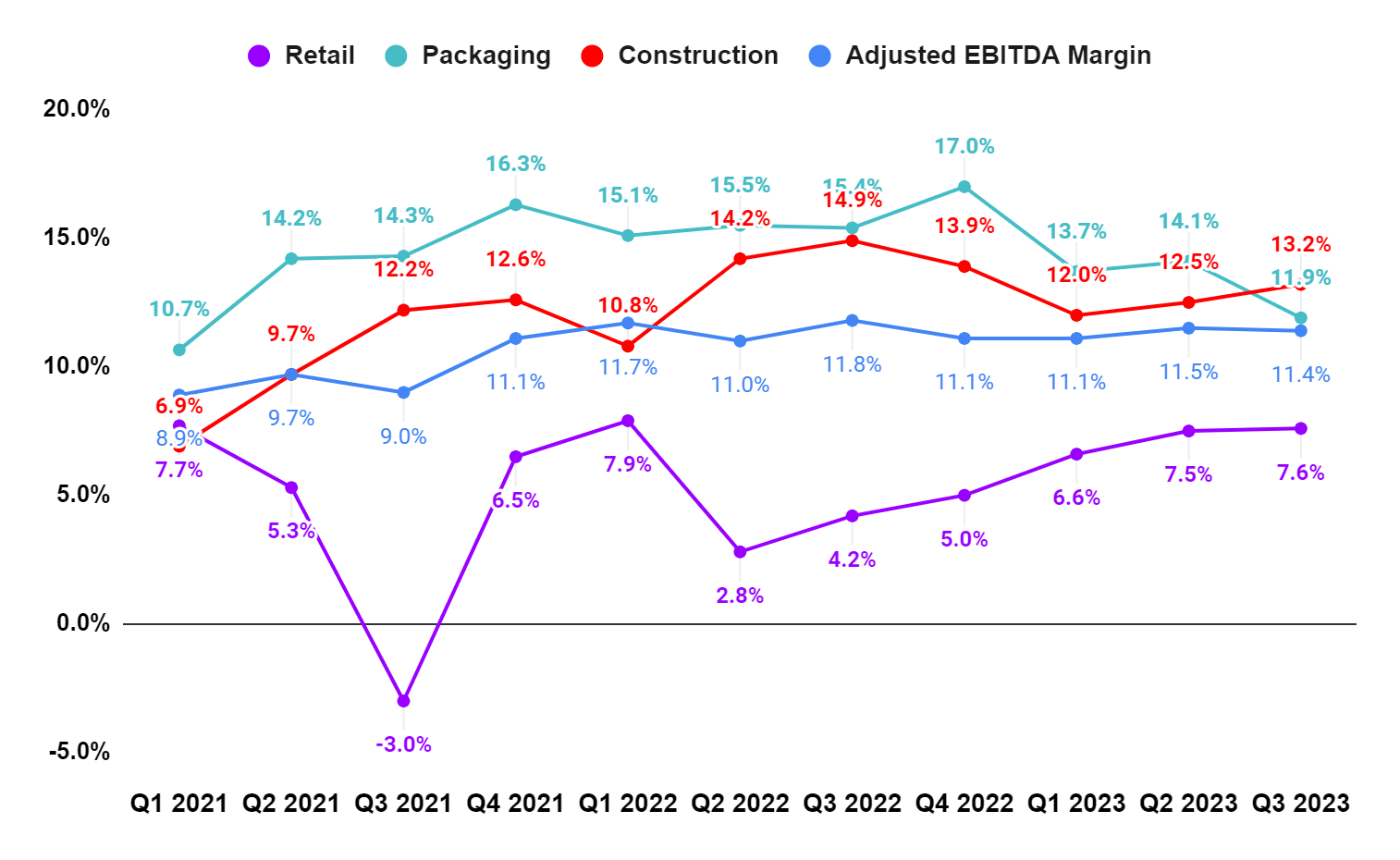

In Q3 2023, the Retail segment's adjusted EBITDA margin improved by 340 bps Y/Y attributed to easy comparisons versus 2022 when margins were negatively impacted by a significant decrease in lumber prices in a short duration of time. However, in the Packaging segment, the adjusted EBITDA margin declined by 350 bps Y/Y due to competitive price pressure and lower volumes while in the Construction segment, the adjusted EBITDA margin declined by 170 bps Y/Y due to more normalized market pricing and lower volume brought on by the decline in housing starts and production of manufactured homes.

Overall, the margin decline in the Packaging and Construction segments more than offset the margin growth in the Retail segment and resulted in a 40 bps Y/Y decline in consolidated adjusted EBITDA margin to 11.4%.

UFPI's Segment-Wise Adjusted EBITDA Margin (Company Data, GS Analytics Research)

{kind=link}

While lower volumes are expected to continue impacting margins in the near term, especially in construction and packaging businesses, I believe an eventual recovery in demand due to end-market improvement towards the back half of FY24 should result in margin improvement in the medium to long term.

The company is also implementing structural cost-saving initiatives like consolidating product manufacturing, rationalizing capacity, and using automation to drive productivity, which should help margins in the long run. In addition, the company's focus on launching new products with higher margins and increased value-added products should also help margin mix in the long run. Overall, I am optimistic about the company's margin growth prospects in the medium to long term.

Valuation and Conclusion

UFPI is currently trading at a 15.88x FY24 consensus EPS estimate of $7.93 and a 14.28x FY25 consensus EPS estimate of $8.83. The company is trading at a premium to its 5-year average forward P/E of 12.35x.

While the company's fundamentals appear to be near the bottom and I expect to see a recovery in the business starting the back half of FY24, the valuation seems to be already pricing in this improvement, with even the company's FY25 P/E above its historical average.

The company has good medium to long-term growth prospects benefiting from a potential reversal in the interest rate cycle in FY24 resulting in improved market demand, long-term tailwinds in the new construction and repair and remodel markets, inorganic growth opportunities from M&As, productivity gains, and an increased mix of higher margin value-added products. However, these growth prospects have already been factored into the current valuation. So, I would prefer to wait on the sidelines for a more attractive entry point. Hence, I have a neutral rating on the UFPI stock.

For further details see:

UFP Industries: Improving Growth Prospects But Priced In