LVMHF - Ulta Beauty: Now Is The Time To Buy

2023-09-04 12:14:22 ET

Summary

- Ulta Beauty's stock has remained relatively flat over the past year, but its fundamentals have consistently improved.

- The global beauty market is expected to grow, particularly in e-commerce sales, which could benefit Ulta.

- Both the Bear- and Base-Case Discounted Cash Flow Analysis suggest that the company could be undervalued right now.

Ulta Beauty ( ULTA ) is pretty much flat over the last year:

In the same time frame, the fundamentals however increased constantly.

This poses the question, if the company is currently at a suitable entry point to enter a position. To answer this question, we first take a look at the market with the predicted annual growth rates, then summarize the main points of Ulta in a SWOT-Analysis and finally valuate the company using a Discounted Cash Flow Analysis for the Bear and Base Case.

The Business

The American beauty retailer chain Ulta Beauty sells cosmetics, skincare, fragrance, bath and body items, haircare equipment, and salon services. Since its founding in 1990, the business has expanded to rank among the biggest beauty shops in the country.

In an effort to give a one-stop shopping experience for anything beauty-related, Ulta Beauty frequently carries a wide selection of goods from both luxury and drugstore brands. Their loyalty program, called Ultamate Rewards, is well-known for its points system, which enables consumers to collect points for purchases that can be used for discounts on subsequent purchases. They frequently conduct deals and promotions.

Additionally, Ulta frequently works with celebrities and beauty influencers to produce unique items and collections. They frequently provide cosmetic treatments including makeovers, skincare advice, and hair salon services in-store.

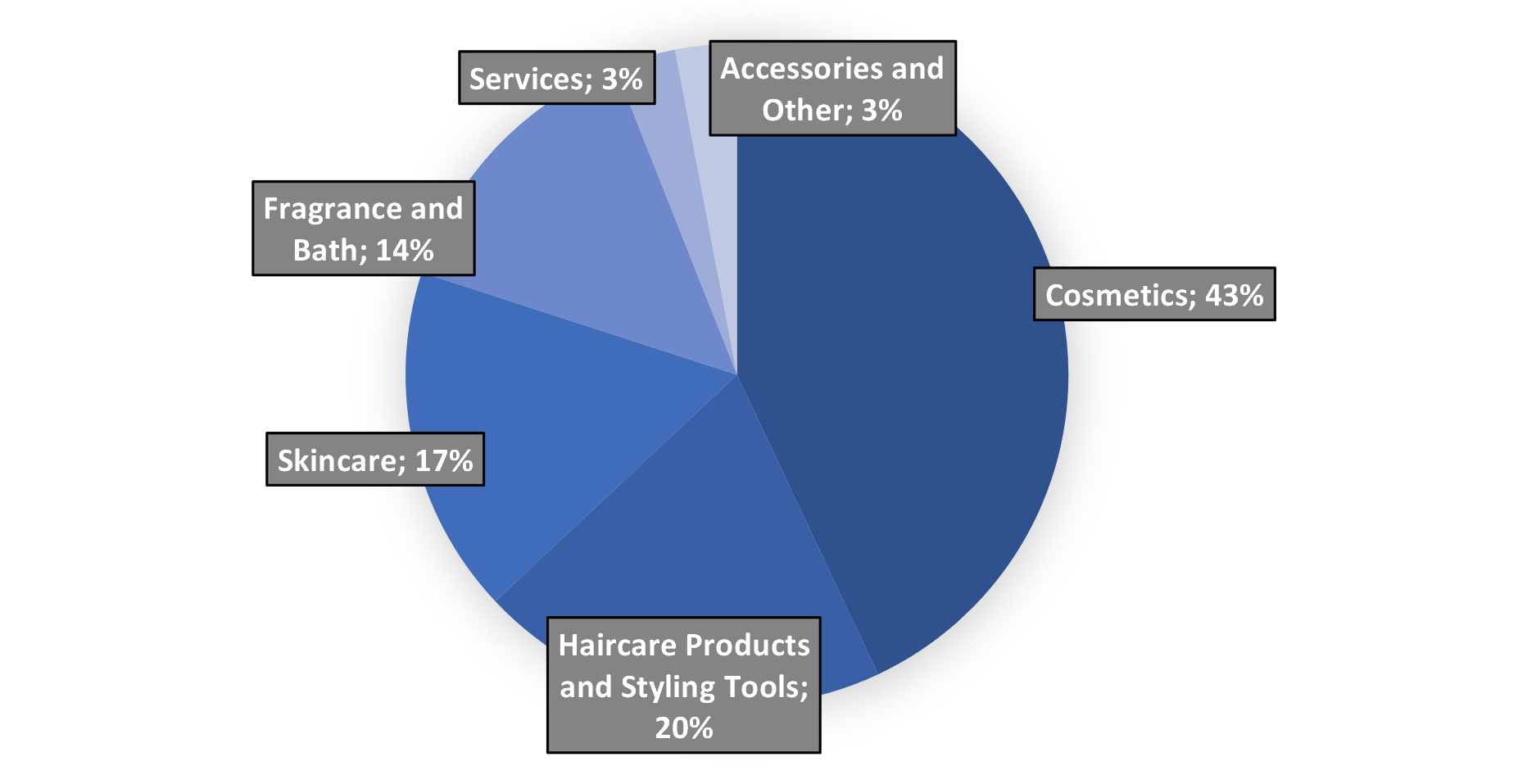

Their current business is segmented like this:

Ulta's Business (marketscreener.com)

{kind=link}

Ulta declared its earnings on August 24th. Net sales increased around 10% to $2.5 billion for Q2 2023. The most important metric - in my opinion - the comparable sales were increased by 8%, this change was composed of a 9% increase in transactions and a 1% decrease in average tickets. This seems like a very solid development for the company considering the current macroeconomic situation.

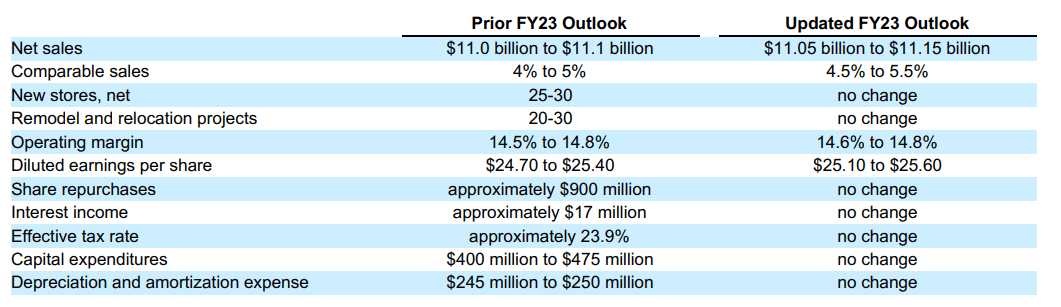

The company also gave a new (slightly improved) outlook for 2023:

{kind=link}

Furthermore, the CEO, David Kimbell, had the following comment to the whole beauty market: "The beauty category has continued to deliver healthy growth, as consumers maintain their post-pandemic routines and expand their definition of beauty."

The Market

Speaking of the beauty market, let's jump into expected growth rates and TAMs for this segment.

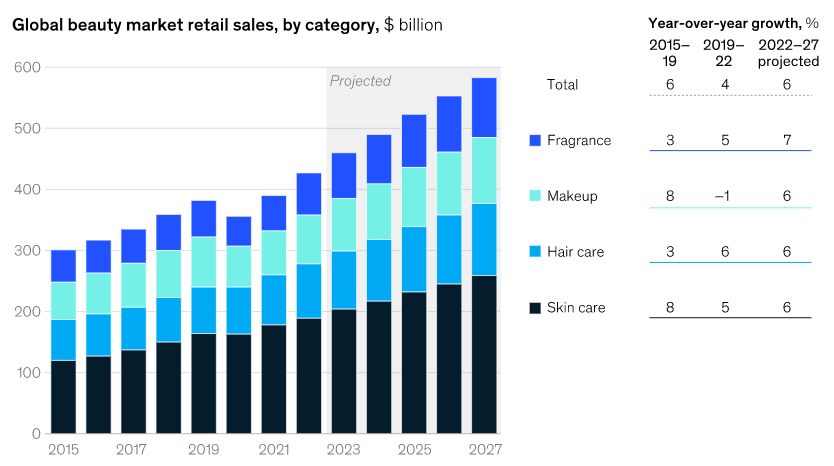

The total global beauty market is expected to grow around 6% p.a. until 2027. This is composed of 7% p.a. growth in fragrance, 6% p.a. in makeup, 6% p.a. in hair care and 6% p.a. in skin care.

Global Beauty Market by Category (mckinsey.com/industries/retail/our-insights/the-beauty-market-in-2023-a-special-state-of-fashion-report)

{kind=link}

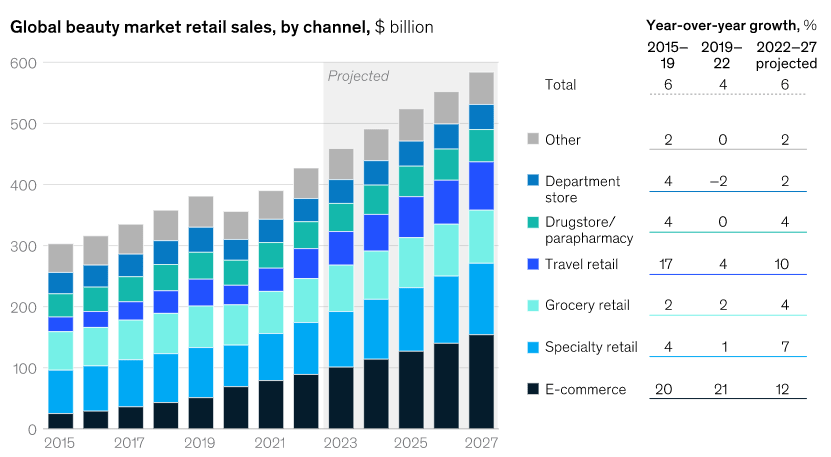

Within this growth, especially the e-commerce sales channel - with a CAGR of 12% until 2027 - is expected to grow fast.

Global Beauty Market by Channel (www.mckinsey.com/industries/retail/our-insights/the-beauty-market-in-2023-a-special-state-of-fashion-report)

{kind=link}

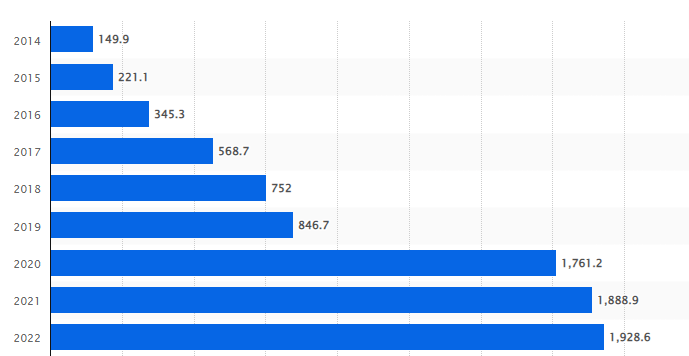

This trend could be beneficial for Ulta, as the company is increasingly expanding its e-commerce sales. As of 2022, around 19% of all sales were generated through the e-commerce business.

E-commerce net sales of ulta.com from 2014 to 2023 (statista.com/forecasts/1383720/ulta-revenue-development-ecommercedb)

{kind=link}

Another tailwind that Ulta currently has is the fact that the Generation Z is high valuating brands, that place a strong emphasis on social and ethical ideals including sustainability, diversity, and inclusion as well as product efficacy and transparency. These customers are seeking for businesses that promote a feeling of larger community, have a compelling narrative that goes beyond just selling items, and have a genuine and approachable brand image. Ulta is acting very transparent here .

Because of this and many other aspects, Ulta is currently the Top Beauty Destination in the US for teens. The company even managed to increase its lead over Sephora ( LVMHF ), Walmart ( WMT ), Target ( TGT ) and Amazon ( AMZN ) in the last years, as currently 41% of teens state that Ulta is their #1 beauty destination vs. 38% in 2019.

Top Beauty Destinations for Teens 2019 (www.pipersandler.com/news/piper-jaffray-completes-38th-semi-annual-generation-z-survey-9500-us-teens)

Top Beauty Destinations for Teens 2023 (www.pipersandler.com/news/piper-jaffray-completes-38th-semi-annual-generation-z-survey-9500-us-teens)

I believe that the beauty market in general is a very promising market to invest in. Especially that Ulta, the market leader for teen-beauty products in the US, is positioned very well to capitalize from the growing market.

SWOT Analysis

Strengths

Wide Range of Products and Services

The firm provides cosmetics, perfumes, skincare items, and salon services, giving customers a " one-stop-shop " " experience. As a result, the consumer base is more varied and the average transaction size rises.

Exclusive Brands and Partnerships

Ulta stands itself from rivals because of collaborations and distinct product ranges. These collaborations frequently involve high-end brand alliances, exclusive product releases, and celebrity product endorsements.

Omnichannel Strategy

The seamless integration of in-store and online shopping experiences by Ulta Beauty makes it simpler for customers to browse, purchase, and receive items.

Strong Loyalty Program

The well-regarded loyalty program "Ultamate Rewards" helps customers stay with the company and spend more money. Currently, the program has more than 40 million members , and a sizable portion of transactions take place through it.

Weaknesses

Heavy Reliance on the U.S. Market

Due to its focus on the US market , Ulta is particularly susceptible to market fluctuations and changes in customer tastes.

Supply Chain Concerns

Global disruptions like pandemics or trade wars might have an effect on the supply chain, which would then have an influence on the availability of goods.

Price Sensitivity

Because many customers think Ulta's items are pricey, the firm is susceptible to economic downturns when customers reduce their discretionary spending. But this could be argued for all Consumer Discretionary stocks.

Opportunities

International Expansion

Ulta has a chance to expand outside of the United States thanks to the expanding global beauty and cosmetics sector.

E-commerce Growth

Ulta might increase its focus on mobile apps and online purchasing to increase its portion of the expanding e-commerce sector.

Diversification

With the inclusion of natural and organic cosmetics, men's grooming, and more skincare categories, Ulta has the chance to expand its product selection and meet the demands of more customers.

Sustainable and Ethical Products

Ulta has the chance to diversify its product offering because of rising customer interest in eco-friendly and cruelty-free goods.

Threats

Competition

Sephora, Amazon, and drugstore chains are just a few of the major competitors fighting for market share in the fiercely competitive beauty retail sector.

Changing Consumer Preferences

The beauty industry's trends change quickly. If Ulta doesn't change, its products may become outdated or less desirable.

Economic Downturns

Discretionary expenditure on cosmetics and salon services is quite susceptible to changes in the economy.

Theft

Theft is currently a big problem for Ulta. According to Dave Kimbell, the CEO of Ulta, the company is experiencing a higher level of theft in the recent months. While this is definitely decreasing profits, the problem is slowly stabilizing according to Reuters .

Valuation

Ulta is currently trading at a P/E ratio of 16.7, this seems very cheap when we take a look at the company's 10 years average rate. The average here however includes the very high ratios of the company during the Covid 19 crisis.

When we take a more "ordinary" time frame, we can see that a more suitable average P/E would be around 21.

So even with a corrected/conservative P/E ratio, the company looks attractively valued on this side.

To get another angle at Ulta's valuation, we compare the company to two major peers: LVMH ((LVMHF)) and Bath & Body Works ( BBWI )

I'm aware that these companies can't be compared 1 to 1, but I nevertheless think that we get a good understanding of Ulta's valuation if we compare these companies.

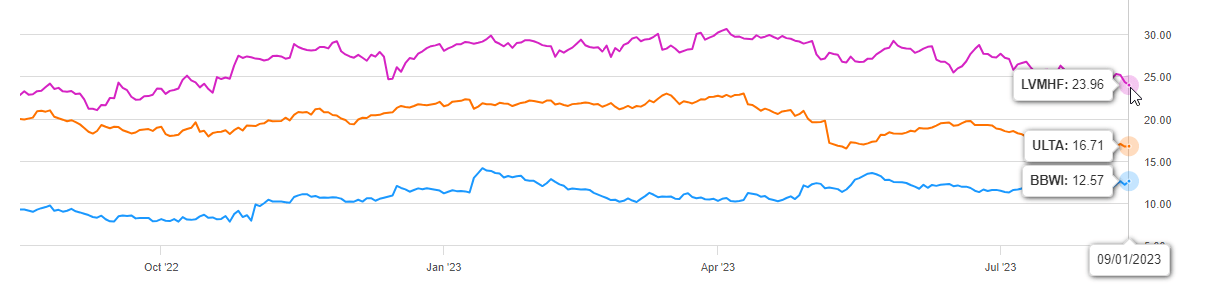

If we take a look at the current TTM GAAP P/E ratio of the three, it becomes apparent that LVMH is currently trading the highest with ULTA being at the lower end and slightly above BBWI.

P/E GAAP ULTA vs LVMH vs BBWI (seekingalpha.com)

{kind=link}

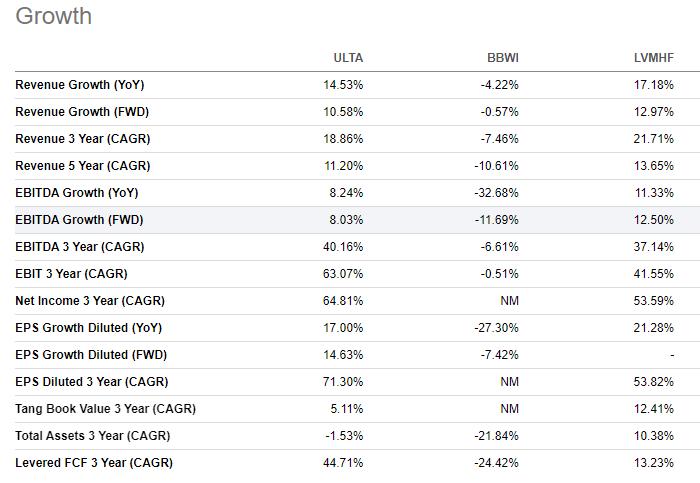

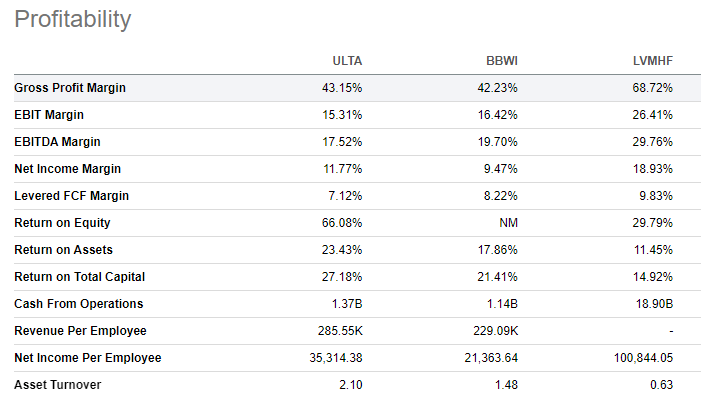

If we compare the growth and profitability metrics of the three, the P/E differences however seem to be justified, as LVMH is growing more rapidly than both and even achieves higher margins on the way. This is doable for LVMH due to their high focus on luxurious goods .

Growth Metrics ULTA vs LVMH vs BBWI (seekingalpha.com) Profitability Metrics ULTA vs LVMH vs BBWI (seekingalpha.com)

{kind=link}

{kind=link}

Discounted Cash Flow Analysis

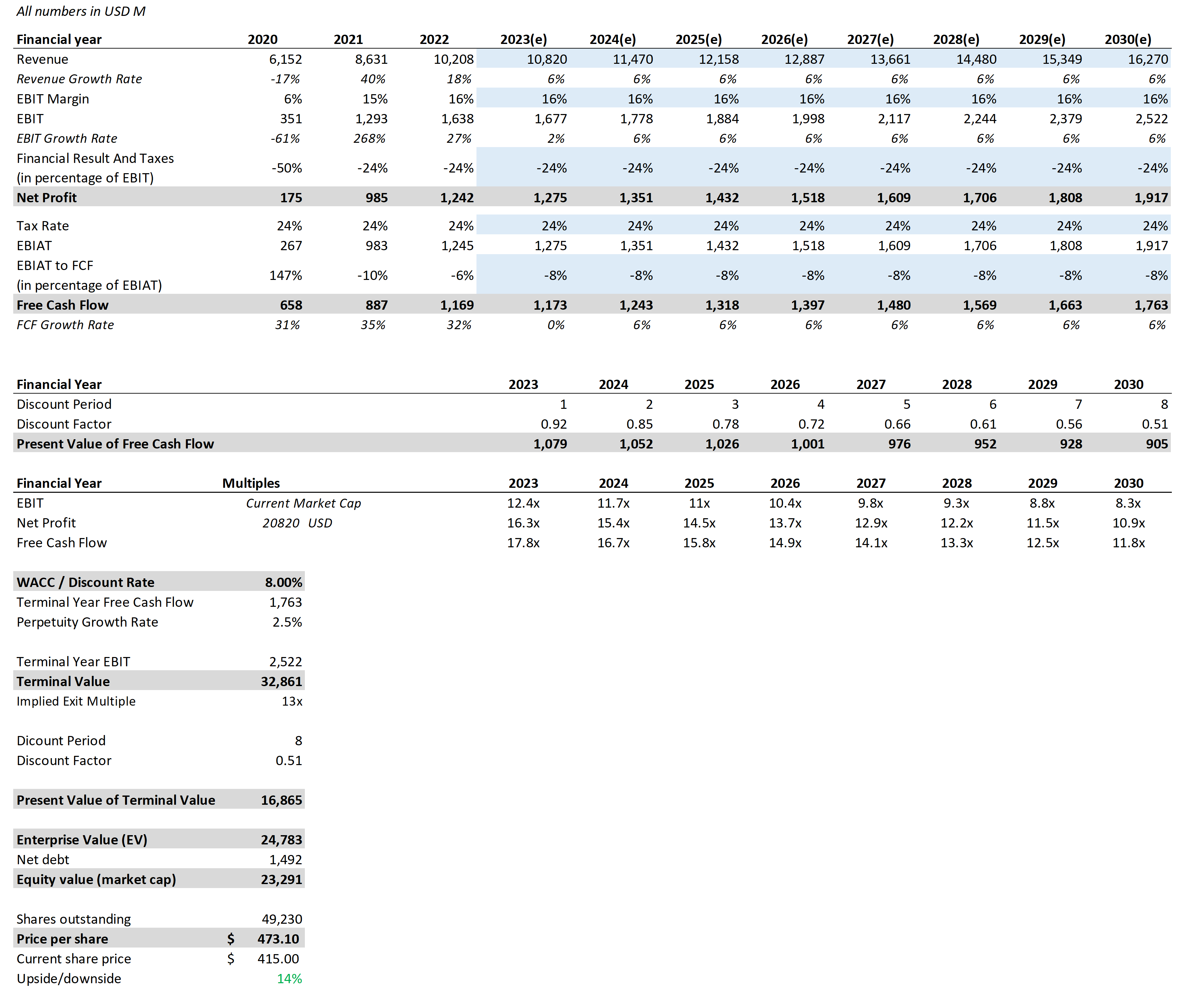

To evaluate the company independently from any peers and to finally answer the question, if the company is currently at a good valuation right now, I conducted two different Discounted Cash Flow Analyses: The Bear- and Base-Case. The blue cells in the DCF are the major assumptions I took to evaluate the company.

Bear-Case

- Revenue: For the Bear-Case, I assumed a revenue growth rate of 6% for the next years. Note that this is well below Ulta's historical ten-year growth rate of 15% and analysts' expectations for the company.

- EBIT Margin: For the EBIT margin, I used the average of the last 2 years and anticipated that it would stay flat at 16% for the next 8 years. I didn't use 2020 in the average, as the 6% achieved there seems like an outlier:

- Financial Result And Taxes: Here I also averaged out the last two years and therefore used -24% to calculate the Net Profit for the years 2023 to 2030.

- Tax Rate: For the tax rate, I used 24%, as this was the tax rate for the last three years.

- Free Cash Flow: I calculated the EBIAT using the aforementioned tax rate and then attempted to estimate an appropriate EBIAT to FCF ratio. I here again averaged out the last two years and used -8% to calculate Ulta's future Cash Flow.

- WACC: Ulta's WACC is currently at 7.5% , to make some room for errors and have a margin of safety I assumed a WACC of 8% for our DCF.

- Perpetuity Growth Rate: The perpetuity growth rate assumed for the analysis is a conservative 2.5%.

Discounted Cash Flow Analysis Ulta - Bear (seekingalpha.com; own assumptions)

{kind=link}

With these pretty conservative assumptions, we get a target price of ~$473, suggesting that even in the Bear-Case the company could be undervalued by 14%.

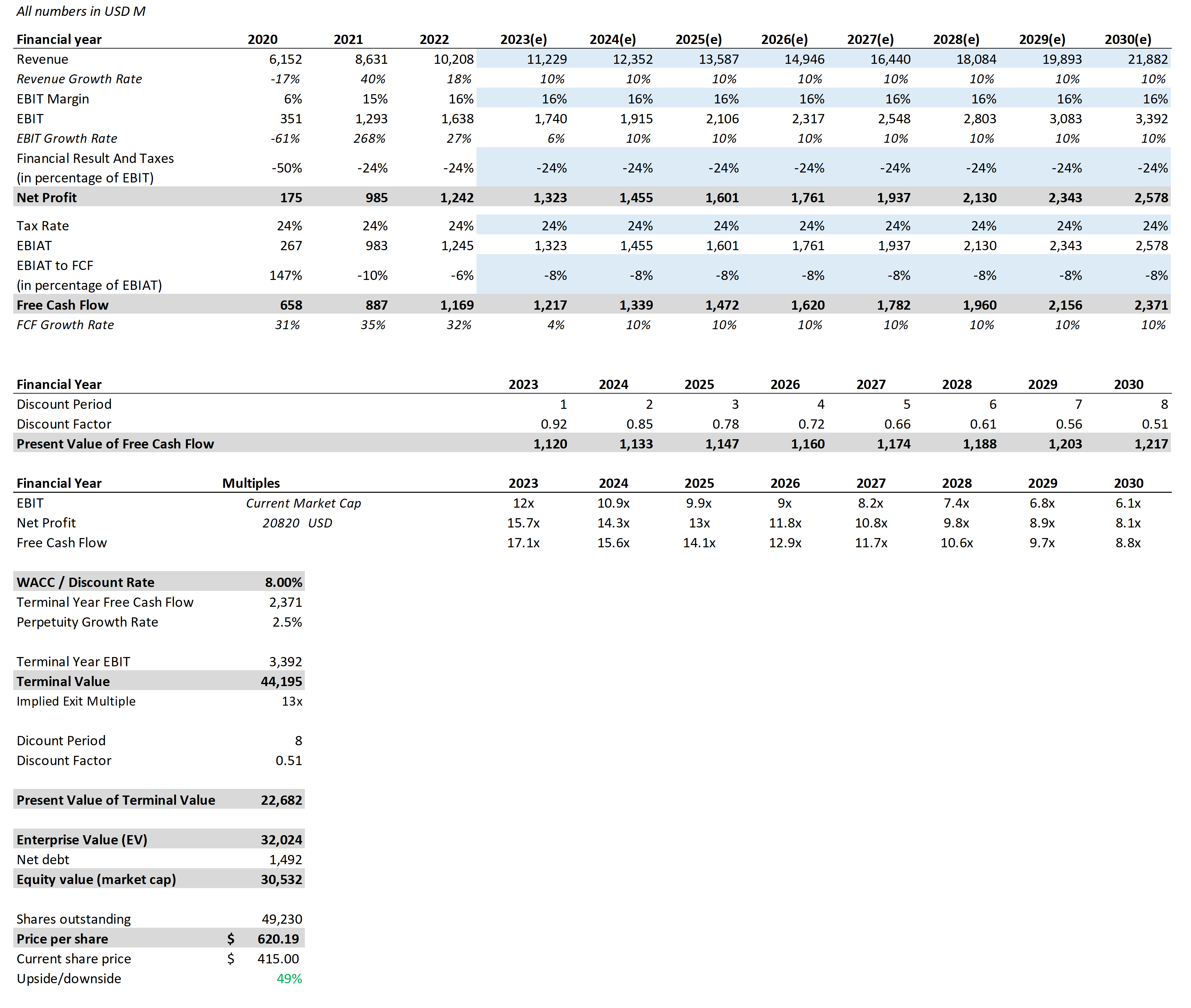

Base-Case

For the Base-Case, I let most of the metrics the same. I just assumed that the company will grow at a revenue CAGR of 10% until 2030. This is still lower than the company's five-year growth rate of 11%, but seems reasonable.

Discounted Cash Flow Analysis Ulta - Base (seekingalpha.com; own assumptions)

{kind=link}

With these more optimistic anticipations, we get a target price of ~$620, suggesting that the company could even be undervalued by almost 50%.

Risks To Consider

Of course, there are risks to this thesis that have to be considered. If one or more of the above-mentioned Threats and Weaknesses come into play or aren't addressed properly by management, the fundamentals and therefore our valuation might decline.

Especially the rising theft in retail is a big risk to consider. This is a 'macro' trend that is currently impacting a lot of the retail stores in the US. This is especially worrying as ULTA itself isn't capable of tackling the problem, but is reliant on the whole society and retailers to overcome this issue. This could in turn negatively impact the margins of Ulta.

Furthermore changing consumer preferences are a big risk for me. As mentioned around 40% of US teens currently named Ulta as their number one beauty destination. However with TikTok and Social Media preferences of young customers can shift very quickly and often unpredictable, which in turn could have a negative impact on Ulta's market share.

Conclusion

The beauty industry in general is, in my opinion, a very promising segment to invest in. Ulta offers here a very compelling opportunity, with its high standing among teens - a very important age group for beauty - and its high focus on e-commerce and its 'omnichannel' approach. All this while currently being at a very nice valuation range of an undervaluation between 14% and 50%. Considering all this, I currently rate the company as a 'Strong Buy' with a price target of $550.

For further details see:

Ulta Beauty: Now Is The Time To Buy