ELF - Ulta Is Solid But There Are More Attractive Beauty Stocks Out There

Summary

- Ulta should post strong FQ4 results, powered by a strong beauty category.

- The company still has some growth levers but has become a more mature retailer.

- COTY and ELF look more attractive, in my view.

Ulta Beauty ( ULTA ) should post strong FQ4 results on the back of a very good beauty category backdrop. However, the stock looks appropriately priced at current levels, and I think there are better investment options in the beauty space at the moment.

Company Profile

ULTA is the largest beauty retailer in the U.S. selling cosmetics, fragrance, skin care products, hair care products, and salon services. The company has over 1,300 stores in all 50 states. It also sells its products through its e-commerce website.

The retailer sells both prestige and mass-market beauty products, offering a variety of price points across its stores. In total, it stocks over 25,000 products from more than 600 beauty brands. It also has its own private-label brand.

Approximately 43% of its sales come from cosmetics, while haircare represents 20% of sales. Skincare and fragrance make up 17% and 14% of sales, respectively.

ULTA has one of the strongest loyalty programs in retail, boasting ~39 million members. An astonishing ~95% of sales coming from loyalty members.

Opportunities

One of ULTA's growth drivers is the continued introduction of new products and brands. The company says, historically, new products have averaged 20% to 30% of its sales. ULTA has done a great job of continually finding and adding hot new brands.

In this vein, it's been particularly focused on promoting the skincare and fragrance categories. On its fiscal Q3 earnings call , CEO Dave Kimbell said:

"Turning to the performance of our core categories, starting with our fastest-growing category, skincare. Beauty enthusiasts are maintaining their skincare routines with a focus on science-backed and dermatologist-recommended products. Guests are engaging with newer brands, like Drunk Elephant, Super Goop and Good Molecules, while new products from established brands like the Ordinary Hero Cosmetics and the Roche-Posay also contributed to sales growth.

"To drive discovery and support guest education, this quarter, we introduced our Skincare We Love All in all stores. This curated presentation highlights exciting brands and best-selling items across key categories. The fragrance and bath category delivered another impressive quarter, as Gen Z guests engaged with the category, leveraging multiple fragrances to express themselves. Recently launched Ulta Beauty exclusive Billie Eilish, as well as Nescens from Burberry, Gucci and Victor and Ralph drove meaningful sales growth. While our monthly fragrance crush program drove engagement with established brands including Versace and Jimmy Choo. In addition, the category benefited from strong guest engagement with our holiday fragrance gift sets, which were available earlier this year."

In many ways, ULTA actually helps drive a new brand's popularity, so it is often the go-to partner for new, up-and-coming brands. This is a powerful position to be in for the company.

Store expansion and lease optimization are another opportunities for ULTA. The company thinks it can reach 1,500-1,700 stores in the U.S. It has identified over 100 DMAs where it already has high market share where it thinks it can leverage its brand and further penetrate white space, and another nearly 50 DMA where it has a lower market share but high profitability it can go after.

Building stores-within-stores within Target ( TGT ) is also a nice opportunity. TGT tends to have a slightly more upscale customer base, so ULTA being able to offer some more prestige products beyond TGT's mass cosmetic offerings should be a win-win for both companies. In addition, while not in its near-term plans, international expansion is also on ULTA's radar.

The company also has a bunch of lease renewals coming up through 2024. Given the retail leasing marketplace, ULTA should be able to reduce rent expenses, improve the look of its stores, and/or find better locations.

As a more mature retailer, optimizing its infrastructure, e-commerce abilities, and improving its supply chain are other areas where ULTA can continue to improve. In recent years, the company has also improved its CRM capabilities to help better understand and target its customers. Digital initiatives such as virtual makeup try on, personalized shopping, and product finders can also continue to drive the user experience and thus growth.

Risks

The economy and a cautious consumer are on the minds of most retailers, as inflation remains elevated, reducing consumer buying power and discretionary income. However, the sales of cosmetics have traditionally been strong during these periods, even during recessions. Often referred to as the " lipstick index ," the phrase was coined by Estée Lauder's ( EL ) Leonard Lauder who noticed that during economic downturns, the sales of affordable little luxuries like cosmetics rose.

The lipstick index or not, it will be interesting to see if there is any trade-down effect. Cosmetic companies e.l.f. Beauty ( ELF ) and Coty ( COTY ) both saw strong sales in their mass brands. While a trade-down into mass could hurt ULTA's sales, it is fortunate enough to offer both prestige brands and mass brands, as well as what it calls masstige, which is what is in the middle.

Another risk ULTA faces is high expectations. The company has put up strong numbers over the past year, and the stock has performed very well over the last few years. At this point, expectations appear to be very high that this will continue.

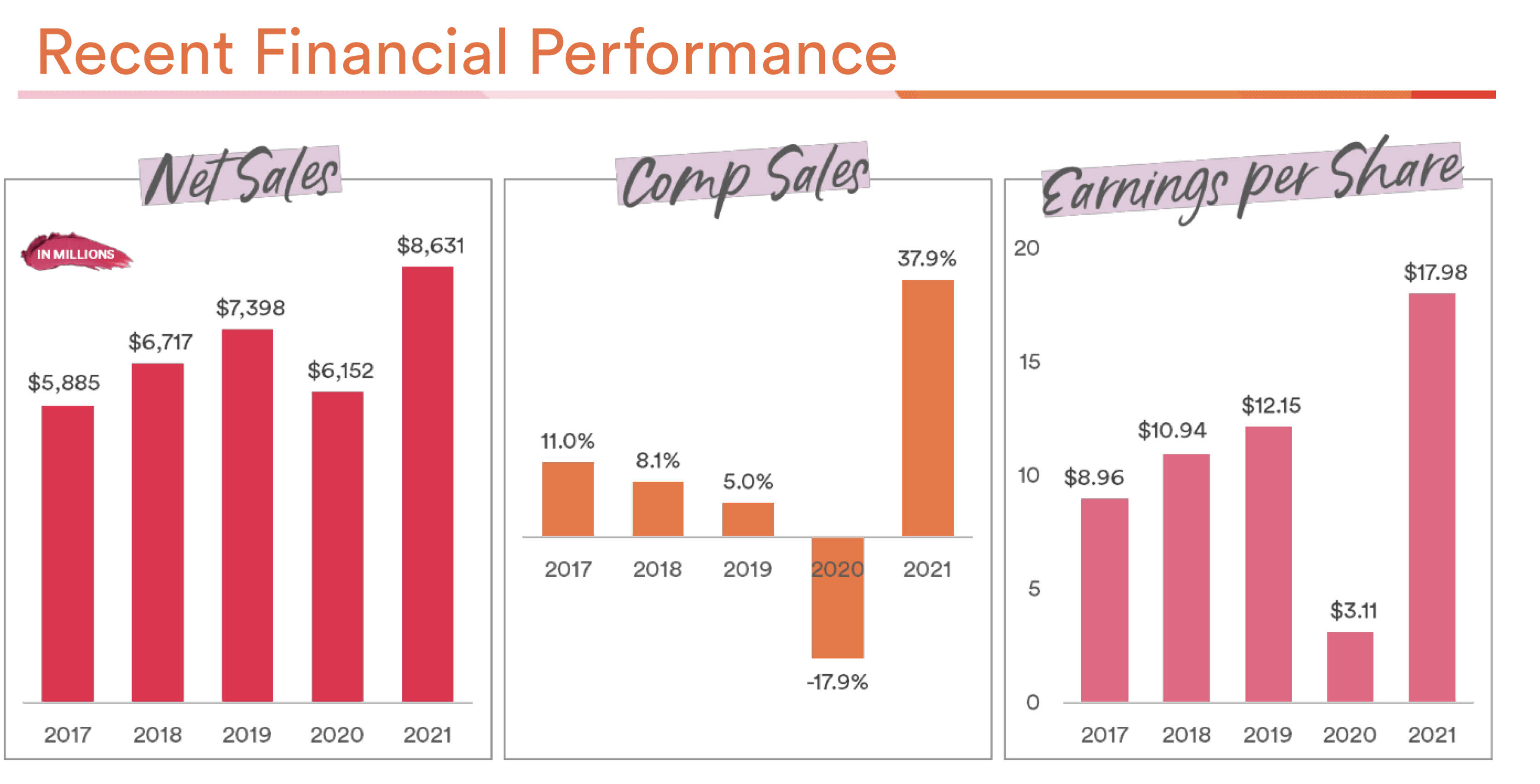

Seeking Alpha Company Presentation

{kind=link}

{kind=link}

Valuation

ULTA trades around 15x the FY2024 (ending January) consensus EBITDA of $1.86 billion and 14x the FY2025 consensus of $1.94 million.

It trades at a forward P/E of 21x the FY24 consensus of $24.20. Based on 2025 analyst estimates of $26.12, it trades at just under 20x.

Comparatively, cosmetic company EL is valued at ~21x fiscal '24 EBITDA (ending June) and ELF is valued at 30x FY'24 EBITDA (ending March).

However, ULTA is a retailer not a brand, and retailers typically trade at lower multiples than thriving brands, as brands can have more staying power and the ability to grow through increased distribution and international expansion. Retailers often trade under 12x EBITDA and under 15x forward PE.

{kind=link}

Conclusion

ULTA's stock has been a juggernaut, and with strong commentary from the likes of ELF and COTY, as well as L'Oréal with regard to North America, I expect the retailer to post strong Q4 results when it reports later this month. Beauty has been one of the strongest retail categories out there, with both strength in cosmetics as well as fragrance.

A 15x EV/EBITDA multiple for a more mature retailer does feel a bit high, although I think it is an appropriate valuation given ULTA's defensive nature and the strong current beauty market. However, within the beauty space, I do prefer COTY as a turnaround story and ELF as a growth story .

If I owned ULTA I'd continue to hold the stock, but I would not be a new buyer at current levels.

For further details see:

Ulta Is Solid, But There Are More Attractive Beauty Stocks Out There