MREO - Ultragenyx: Market Expectations Revised Lower Awaiting Clinical Trial Catalysts (Rating Downgrade)

2023-08-30 16:15:16 ET

Summary

- Ultragenyx Pharmaceutical Inc. shares have declined following Q2 numbers and a broader selloff in the healthcare sector.

- The company continues to show growth in product sales and progress in its clinical programs for setrusumab.

- Further catalysts are needed to see RARE sell higher in my view, and investors are chasing quality compounders in this current market.

- On this basis, revise to hold, while awaiting further trial readouts.

Investment updates

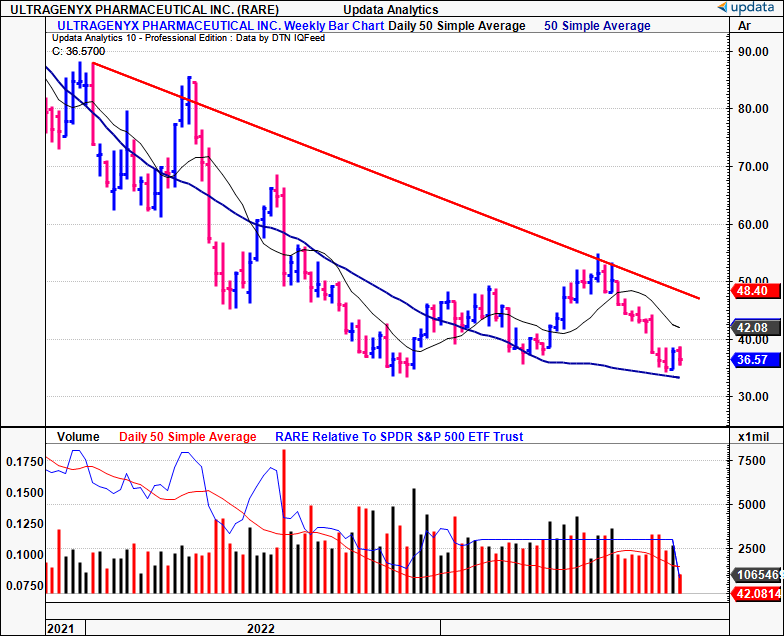

Since the last publication, shares of Ultragenyx Pharmaceutical Inc. (RARE) have failed to catch a bid and pushed further to the downside. I rated RARE a speculative buy in February, and after a short snapback rally, it sold off quickly following its Q2 numbers and amid the broad selloff in the healthcare basket.

Critically, the firm continues its growth in product sales and has made strides in its clinical programs for setrusumab, which shouldn't be overlooked. However, the market is looking for robust fundamentals and economic characteristics, and with a multitude of selective opportunities in our coverage universe, I revise RARE to a hold, awaiting a broader set of catalysts in either 1) fundamentals, 2) setrusumab trial updates, and/or 3) valuation re-ratings. Net-net, reiterate hold.

Figure 1. RARE weekly price evolution, 2021–date

{kind=link}

Critical facts to revised thesis

Overview of basic operations

RARE—as it says in the ticker name—is in the business of commercializing treatments for ultra-rare diseases. An 'ultra-rare' disease is one that has extremely low prevalence, considered usually <1 in every 50,000 persons. The corollary to this is a lack of sufficient treatment research programs to treat such conditions. Here's where RARE enters the market.

A brief rundown of the company's products and their indications follows:

- Crysvita approved in the U.S., the EU, and select regions for addressing X-linked hypophosphatemia ("XLH") in adult and pediatric patients aged one year and above. Crysvita has extended indication to treating hypophosphatemia in tumor-induced osteomalacia ("TIO"). Crysvita is also the company's main breadwinner.

- Mepsevii is a pioneering treatment for mucopolysaccharidosis VII ("MPS VII"), also known as Sly syndrome . It has U.S. and EU approval.

- Dojolvi, which is approved in the U.S. and select regions to alleviate the impact of long-chain fatty acid oxidation disorders ("LC-FAOD") in pediatrics and adults.

- Evkeeza; indicated in the treatment of homozygous familial hypercholesterolemia ("HoFH") in the U.S. and the European Economic Area ("EEA").

Distribution of its approved products is conducted through a concentrated network of distributors. The company books revenue from "named patient" sales in specific countries. This involves estimating transaction prices, including constrained variables, and things like discounts and returns. Essentially, the more units it sells, the more money it makes.

Q2 FY'23 insights

RARE put up Q2 sales of $108mm , up 21% YoY. It generated this on OpEx of $256mm, with an R&D investment of $165mm baked into this number. I'd also point out that the OpEx figures incorporate non-cash stock-based compensation amounting to $35mm, along with a one-time milestone payment of $9mm to Mereo BioPharma ( MREO ) for the phase 3 Orbit study, initiated during the quarter (this is discussed later). Net loss for Q2 came to $160mm or $2.25 per share.

The divisional breakdown of RARE's Q2 top-line is as follows:

- Crysvita's clipped Q2 revenues of $83mm. To disaggregate this further—North America ("NA") accounted for $61mm, Latin America ("LatAm") produced $16mm, and it saw $6mm from European royalties.

- Dojolvi printed revenues of $16mm, up 22% YoY, driven by demand-pull in NA.

- Mepsevii sales—now in their 6th year—were flat sequentially at $8mm. Management did mention new patients in Brazil and growing demand evidenced by the pace of its U.S. order growth.

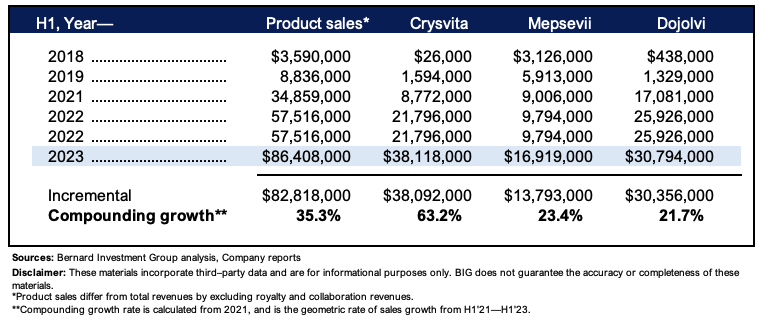

Figure 2 depicts the company's product growth from H1 FY'18—H1 FY'23. No royalty or collaboration revenues are included, just tangible product sales. This captures both pricing and demand effects. Further, Evkeeza product sales are excluded, given there's no comps period before 2023. The compounding growth rates are shown from 2021–2023.

Critically, the firm has added another $82mm in H1 revenues from 2018 to date. The bulk of contribution has stemmed from its Crysvita business, closely followed by Dojolvi sales. Since 2021, it has compounded its revenue clip at 35% geometrically, led by a 63% compounding growth rate in Crysvita.

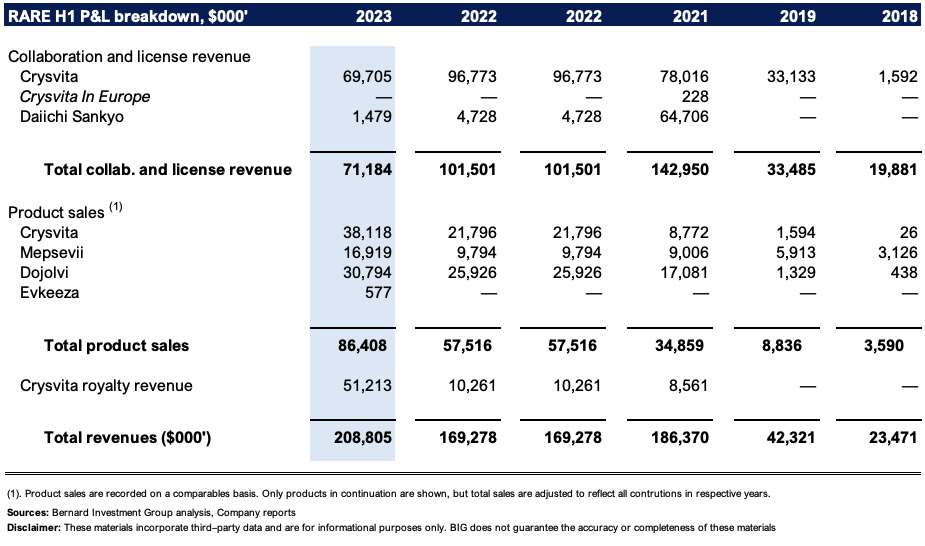

These are commendable growth percentages that indicate heavy uptake of the label. Over the entire testing period, YoY revenue growth has been persistent, and serves as a solid base going forward. Meanwhile, Figure 3 consolidates the company's top-line growth drivers, and separates all sources of income, including collaboration and licensing revenue, product sales, and royalty revenues on Crysvita

Figure 2.

{kind=link}

Figure 3.

{kind=link}

Given the upsides for Crysvita management reaffirmed its FY'23 guidance for the segment and calls for $325mm—$340mm for the year. Hence, it needs another $181mm in sales at the back end of the year, indicating it expects momentum to ratchet up in H2. This covers LatAm and Turkey, but also baked in cash and non-cash royalties from NA and the EU.

It also reaffirmed total sales guidance of $425mm—$450mm, calling for ~24% growth at the top at the upper end of range.

Recent clinical developments

In the last publication I shared our deep dive into the company's setrusumab [UX143] compound that looks to provide a medical breakthrough in 'brittle bone disease', a condition known as osteogenesis imperfecta ("OI"). This is a collaboration with MREO, as mentioned earlier. From the February report: "[OI] is a genetic disorder distinguished by the patient's predisposition to fractures. It results from a deficiency in collagen type I—a crucial component of bone cellular matrix. The insufficient collagen deposits lead to reduced cancellous and cortical bone density [cortical thickness, stiffness], resulting in bones that fracture easily with minimal trauma, sometimes even spontaneously".

At the time, RARE was dosing patients in its phase 2/3 pivotal study, "Orbit". Moving to the present day, the phase 2 dose-finding segment of the pivotal orbit study looks to have yielded meaningful results in my opinion. First, a statistical increase in serum P1NP levels was observed. P1NP is an indicator of bone formation. Patients exhibited a meaningful bone-building effect within 3 months of receiving setrusumab treatment, resulting in a ~10% change in lumbar bone mineral density.

Key baseline metrics further underscore the achievement. Patients in the 20mg cohort started with an average Z-score of negative 2.12—indicating severely compromised bone density. Over the duration of treatment, this score improved by 0.65 points, correlating to a 33% improvement in mineral deficit.

In July, it began patient dosing initiated for two phase 3 studies. The first explores setrusumab's effect on clinical fracture rates in patients aged 5–25 (i.e., a 'physically active' population). The second compares setrusumab against IV bisphosphonate therapy for annualized total fracture incidence in patients aged 2–5 years. Hence, you're looking at setrusumab potentially gaining indication across the entire spectrum of 'at risk' patients in pediatrics and the young adult population. This could be a major tailwind if it successfully navigates through the phase 3 arm.

Beyond numbers, tangible improvements in bone health were observed—fewer fractures, reduced bone pain, and so forth. As it continues the phase 2 arm, it will record fracture occurrences/reoccurrences to examine setrusumab's longer-term impact on bone density and, therefore, fractures. Ultimately, the end goal is to prevent fractures from occurring in the OI populous. There are high risks in obtaining bone fractures with minimal external force. For you and I, accidentally bumping the side of a table or hitting our knee on the door results in nothing more than a curse and a gentle rub better. For OI patients, it could be the difference in staying out of a plaster cast. So I'd urge investors to pay very close attention to the updates here, the next of which are planned for its Analyst Day in October, coinciding with the American Society for Bone and Mineral Research ("ASBMR") annual conference.

Valuation and conclusion

Lack of profitability and ongoing clinical trials make it difficult to accurately value the company on a confidence basis. Still, the stock sells at ~6x forward sales; 52% premium to the sector. Aside from forward sales projections, what else could support this premium? What is the market saying, for example?

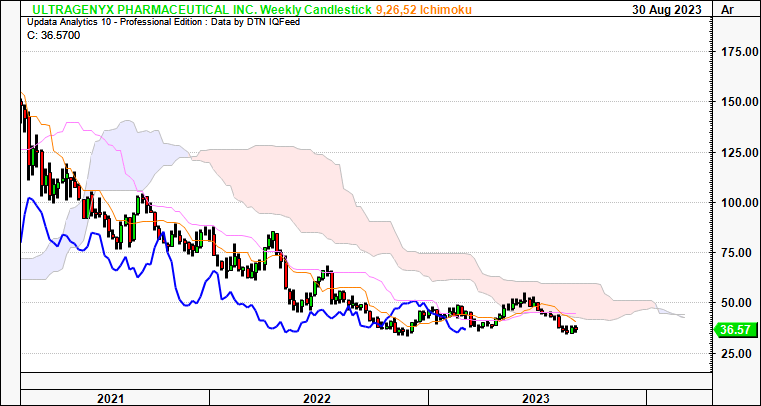

On the charts, the price structure is neutral in my view. The weekly cloud chart, that shows trend action at a simple glance, supports this notion. Both the price line and lagging line (in blue) are below the cloud, with the distance gapping as I write. You'd expect a cross above the cloud to suggest RARE was catching a bid. The weekly chart looks to the coming months. Hence, I am neutral on RARE over the medium term based on this data.

Figure 4.

{kind=link}

We also have further downsides to $32/share on the point and figure studies below. These charts remove the noise of time and give a cleaner view of trend action by removing short-term volatilities. It has eyed the moves from $57 down to $45, then $38, close to where RARE sells today. Hence, $32 might be the next objective to watch out for.

Figure 5.

Data: Updata

In short, despite multiple inflection points on its setrusumab pipeline, and growing sales in its core business, it remains to be seen what level of value RARE can produce for shareholders in the medium-term. The stock returns are basically all event-driven at the moment, centered on how it can mine its pipeline of clinical assets to drive business growth. I had rated RARE a speculative buy in February, and after a rally from $45 to ~$50, the market's expectations have narrowed in based on the latest price structure. Hence, with multiple selective opportunities available elsewhere in our coverage universe, I revise RARE to a hold.

For further details see:

Ultragenyx: Market Expectations Revised Lower, Awaiting Clinical Trial Catalysts (Rating Downgrade)