RARE - Ultragenyx Pharmaceuticals: Downward Trajectory Likely To Continue

Summary

- Ultragenyx has built a remunerative, albeit not yet profitable, business around treating patients with orphan and ultra-orphan diseases.

- The problem from an investor's viewpoint is its outsized expense profile.

- Ultragenyx has an impressive pipeline and strong liquidity.

This is my first look at Ultragenyx Pharmaceuticals ( RARE ), a little biotech with a long name and an active business. Its specific niche of orphan and ultra-orphan diseases presents extra challenges for the company and its shareholders as I will hereafter discuss.

Ultragenyx has significant reliable revenue streams

The initial challenge presented by Ultragenyx is to wrap one's head around its area of specialization. The following excerpt from the company profile describing its therapies is illustrative:

- Crysvita (burosumab), an antibody targeting fibroblast growth factor 23 for the treatment of X-linked hypophosphatemia, as well as tumor-induced osteomalacia;

- Mepsevii [VESTRONIDASE ALFA], an enzyme replacement therapy for the treatment of children and adults with Mucopolysaccharidosis VII [Sly Syndrome] and;

- Dojolvi [UX007/TRIHEPTANOIN] for treating long-chain fatty acid oxidation disorders [LC-FAOD]...

The FDA first approved Mepsevii in 11/2017. Less than 100 cases have been reported in the United States; worldwide prevalence is estimated at ~1:250,000 births. The FDA awarded it with a Rare Pediatric Disease Priority Review Voucher [PRV], which it promptly sold to Novartis ( NVS ) for $130 million.

Shortly thereafter, Crysvita was first approved by the FDA in 04/2018 to treat X-linked hypophosphatemia [XLH]. XLH is a rare ( prevalence ~1:20,000) inherited form of rickets for which vitamin D therapy is ineffective. In its latest 10-Q it estimates that there are ~48,000 patients with XLH in the developed world.

Later in 06/2022, the FDA approved Crysvita to treat tumor-induced osteomalacia [TIO]. TIO is exceptionally rare. One article notes that ~1,000 cases of TIO have been reported worldwide. Its extreme rarity contributes to the likelihood of misdiagnosis.

The FDA approved Dojolvi in treatment of LC-FAOD in 06/2020. Ultragenyx estimates that it afflicts between 2,000-3,500 people in the US.

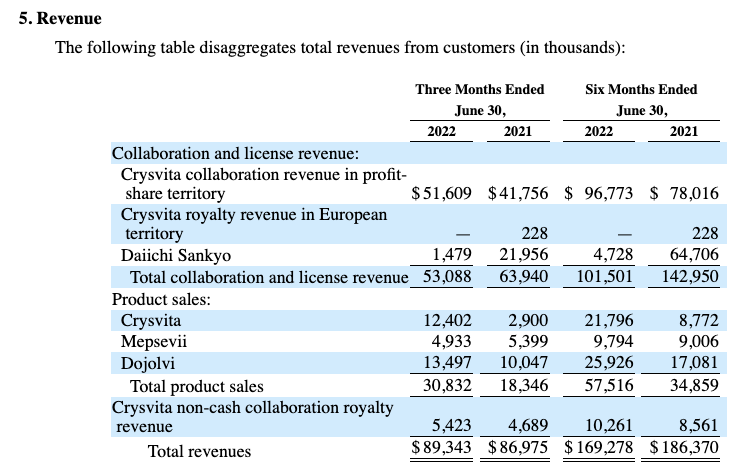

Ultragenyx's Q2, 2022 10-Q lists the following disaggregated revenues during its 3 and 6 month periods ending 06/30/2021 and 2022:

{kind=link}

Ultragenyx's interest in Crysvita (KRN23) arose out of a 2013 collaboration with Kyowa Hakko Kirin Co., Ltd. (KYKOY) for it to develop and commercialize KRN23. At the time Kyowa Hakko Kirin was completing a Phase 1/2 study in adults with XLH in the US and Canada.

During its Q2, 2022 earnings call (the "Call"), CCO Harris advised that Crysvita revenues to date gave it confidence to guide for full year 2022 Crysvita revenues of $250 to $260 million in Ultragenyx territories. He further confirmed prior guidance for $55 to $65 million in Dojolvi revenues. He offered no Mepsevii guidance.

Ultragenyx expenses far outstrip its revenues.

Ultragenyx's balance between its revenue from customers and its operating expenses is sadly askew. Its quarterly expenses are shown below:

seekingalpha.com seekingalpha.com

{kind=link}

{kind=link}

Just a glance shows how its nice quarterly revenues of ~$89 million discussed above are totally overmatched by operating expenses of ~$231 million. All three categories of expenses shot up in Q2, 2022 compared to Q2, 2021, cost of sales by ~164%, R&D by ~36%, SG&A by ~28%. In the aggregate expenses were up by ~36%.

One cannot go to the grocery store without lamenting about inflation; the problem seems to have hit Ultragenyx with extra force. CFO Dier's presentation during the Call provides helpful color on the expected shape of future expenses, although she does not provide an expense guidance.

She noted:

... 2022 is a peak burn year for us as we have initiated multiple late-stage clinical programs in-licensed Evkeeza [Evinacumab-dgnb] completed the acquisition of [GeneTx] and are completing the build-out of our gene therapy manufacturing facility.

In 2023, we don't anticipate additional one-time events of this nature or large capital expenditures and we anticipate SG&A will decrease compared to 2022 as we transition US and Canadian commercialization responsibilities for Crysvita to KKC.

We will continue to invest in our clinical and preclinical programs as discussed, and the overall net effect across the company then will be a decrease in net cash burn.

The referenced Evkeeza in-license refers to its 01/2022 deal with Regeneron (REGN) to clinically develop, commercialize and distribute Evkeeza (evinacumab-dgnb) ex-US. The deal called for $30 million upfront with $63 million in milestones.

The GeneTx acquisition refers to Ultragenyx's 07/2022 $75 million upfront exercise of its option to acquire its partner GeneTx; GeneTx had just reported encouraging interim data from its open-label, dose-escalating Phase 1/2 study of GTX-102 for the treatment of Angelman syndrome [AS].

During the Call there were a variety of questions showing great interest in the AS program. CEO Kakkis minced no words in expressing support for this program. He stated that Ultragenyx was "all in" on it. He enthused that:

...the excellent data we've seen to date in Phase I/II study. It's rare to see a significant improvement in development function as we have seen recently. This is something I haven't seen in 30 years of drug development.

Ultragenyx has a big pipeline and strong liquidity with which to build it.

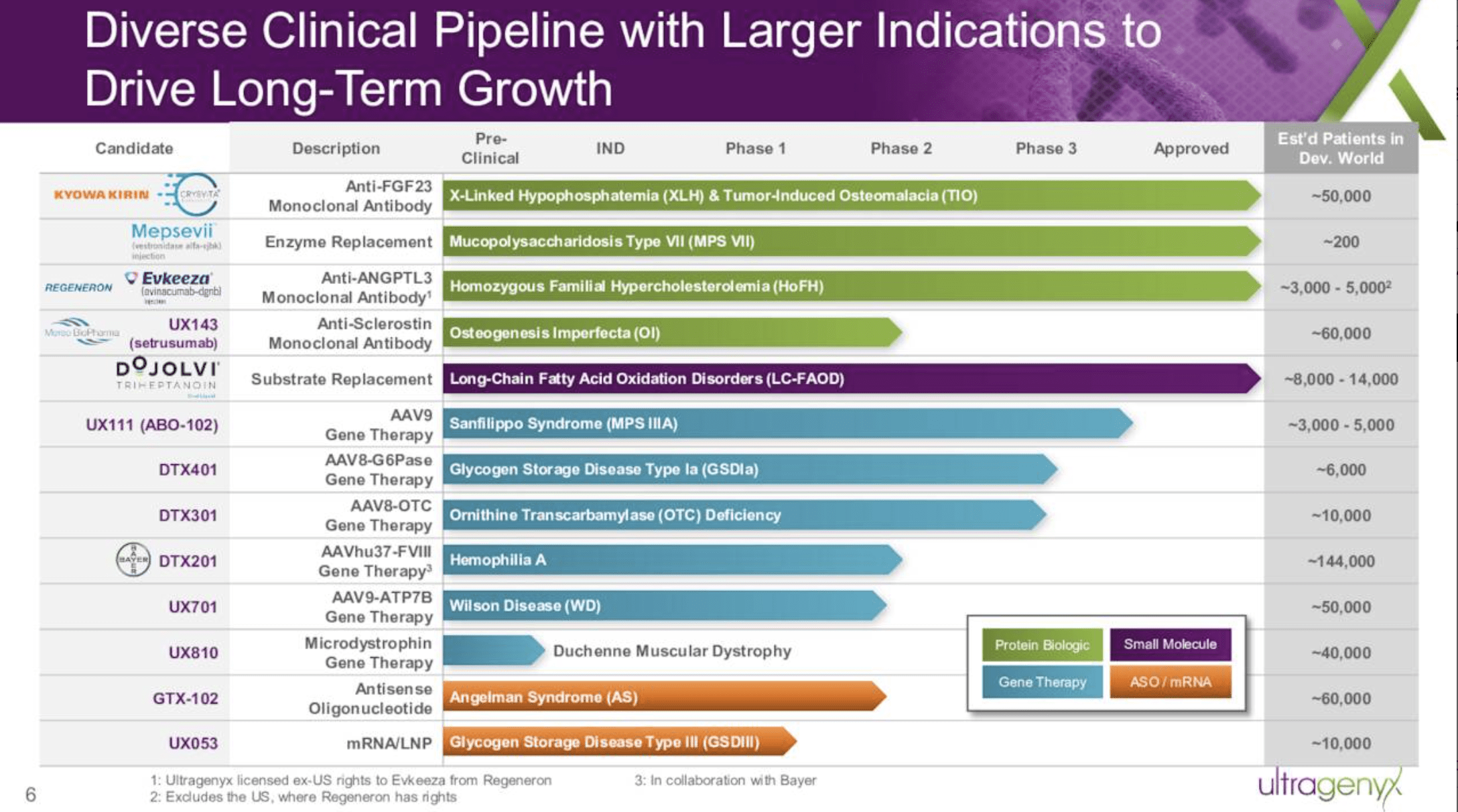

Ultragenyx lists its programs in its Q2, 2022 earnings presentation as follows:

{kind=link}

Its four late stage molecules include its setrusumab (UX143), UX111 (ABO-102), DTX401 and DTX301. Setrusumab is in two studies with estimated study completion dates in 2026, so it may take a while for it to be a revenue factor. DTX301 is also a study whose completion dates suggest that it is more likely to be a mid rather than near term revenue factor.

With 04/2023 estimated primary completion and 04/2024 estimated study completion date for its Phase 3 , DTX401 has prospects for being a nearer term factor. As for UX111, during the Call CEO Kakkis held out the prospect that an early filing was possible "based on convincing biomarker data".

Ultragenyx's clinical milestone slide (below) from its Q2, 2022 presentation shows no clear near term revenue opportunities:

{kind=link}

As for liquidity with which to develop its extensive pipeline, CFO Dier reported as follows during the Call:

We ended the quarter with approximately $706 million in cash, cash equivalents and marketable securities. Subsequent to the end of the quarter, in July we raised $500 million in non-equity dilutive capital in non-equity dilutive capital transactions with OMERS Capital Markets for the sale of a portion of our North America Crysvita royalty.

...We are well capitalized with over $1 billion in the bank and we are making operating decisions to stage spend on our development programs and slowing headcount growth in order to manage our burn.

Conclusion

Ultragenyx appears to be a well-run biotech with a viable plan and proven expertise in its chosen niche of therapies for rare and ultra-rare diseases. Its chart below illustrates its current lagging appeal to investors:

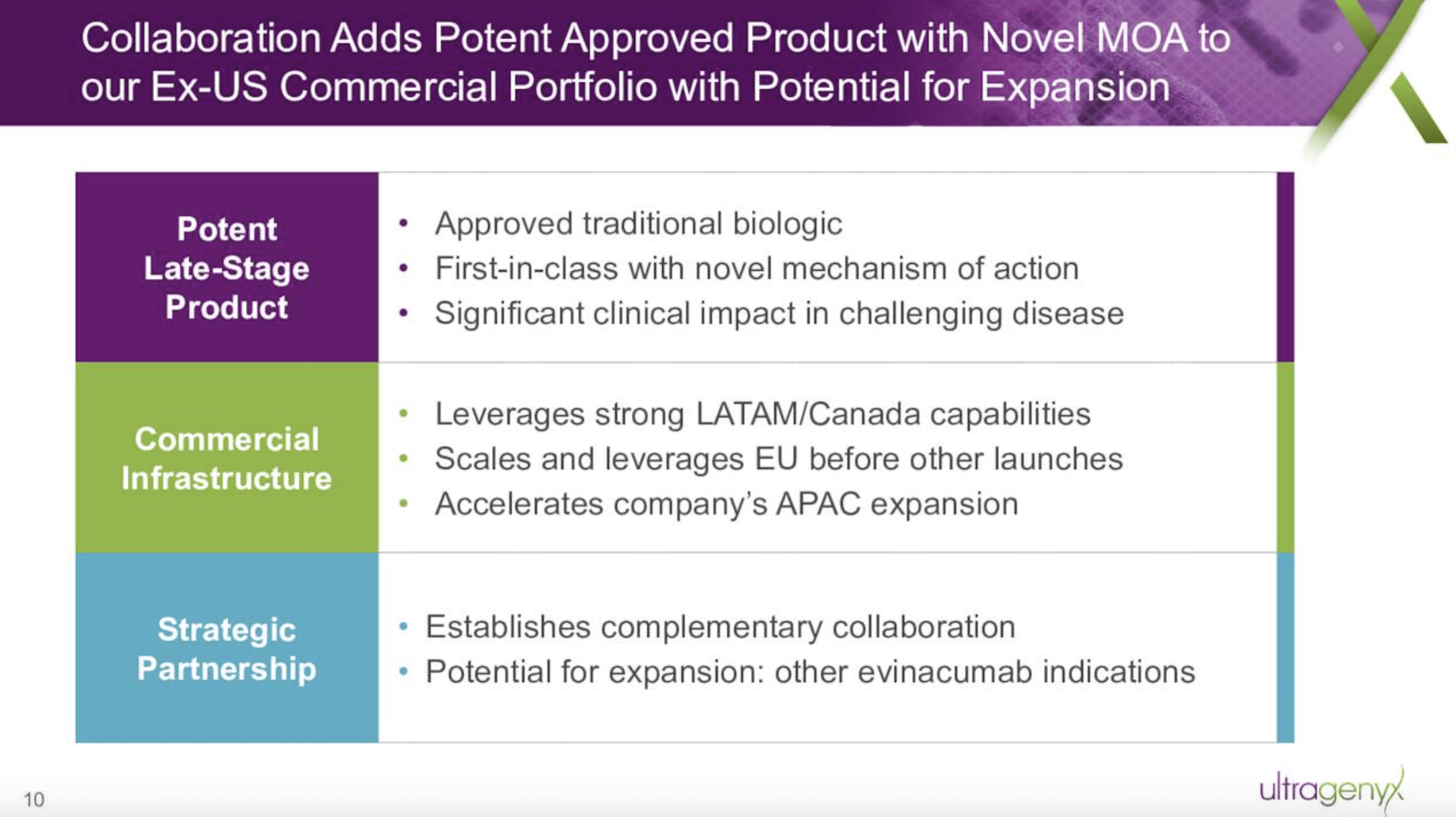

In order for Ultragenyx to power higher it requires fuel. For Ultragenyx the most potent fuel is new approvals. Its pipeline has no current compelling catalysts. The one molecule which looks to provide new revenue opportunities is its ex-US rights to Evkeeza. The slide below from Ultragenyx's Q2, 2022 earnings deck gives some idea of the opportunity here:

{kind=link}

Frustratingly Ultragenyx barely mentions Evkeeza during the Call; certainly it offers no Evkeeza revenue guidance. It's hard to anticipate that Evkeeza can spark sufficient revenues ex-US to make a difference for Ultragenyx anytime soon.

Accordingly, I see Ultragenyx as likely generating lackluster trading over the next few years. In a tough market, I expect its trajectory will continue to continue its downbeat trajectory.

For further details see:

Ultragenyx Pharmaceuticals: Downward Trajectory Likely To Continue