UMH - UMH Properties: Growth With A Margin Of Safety

2024-01-01 21:54:40 ET

Summary

- UMH Properties owns and operates manufactured home communities, leasing homesites and homes to residents.

- There are multiple factors that support the REIT's overall attractiveness, despite my concerns about the safety of its dividend.

- Among them is the current stock price that reflects an adequate discount to NAV and it, therefore, represents a potentially good investment opportunity.

UMH Properties, Inc. ( UMH ), incorporated in 1968 and headquartered in Freehold, NJ, owns and operates manufactured home communities. It mainly leases manufactured homesites and homes to residents.

Even though the dividend doesn't seem as safe as I'd have it, the REIT has a very long history, a great enough portfolio, conservative financing, adequate liquidity, well-laddered maturities, and the price reflects a good discount to NAV.

Portfolio

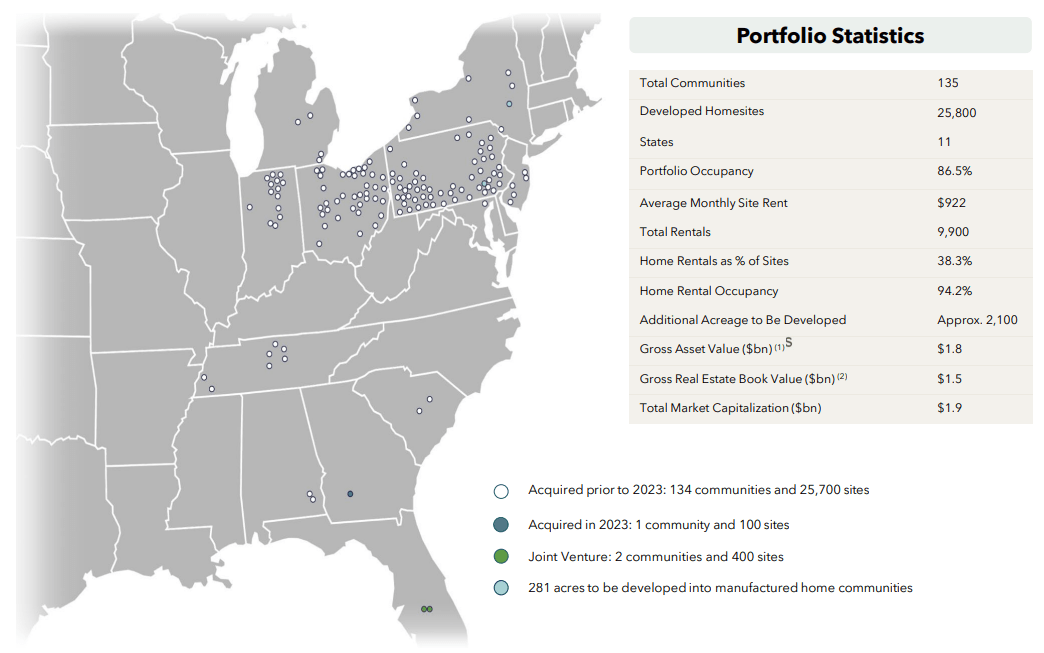

As of September 30, UMH had 135 manufactured home communities in its portfolio, which consisted of ~25,800 developed homesites, located in Alabama, Georgia, Indiana, Maryland, Michigan, New Jersey, New York, Ohio, Pennsylvania, South Carolina, and Tennessee. Additionally, it owns an ownership interest in two communities located in Florida, which it also operates.

{kind=link}

Truth be told, the portfolio is very concentrated, as is obvious in the image above. But I think that this is alleviated to some degree by the great number of homesites that the REIT leases.

Performance

Looking at the long-term historical operating performance, it looks like the company has been growing at a slow but steady rate. In the last decade, in particular, its revenue has been increasing exponentially, with FFO following at a slower pace and operating income more erratically:

Transitioning to more recent results, the occupancy rate as of the end of September was 94.2%, depicting decent efficiency in the use of the REIT's assets.

Additionally, significant growth is reflected in the latest quarterly figures when annualized and compared to the corresponding average annual ones of the last 3 fiscal years:

| Rental Revenue Growth |

| 22.17% |

| Cash NOI Growth |

| 23.92% |

| AFFO Growth |

| 47.52% |

Now, even though the price performance has been very erratic, it has followed the expansion represented in the operating performance of UMH:

Leverage

As for its leverage, about half of its assets are financed with long-term debt, a level it slowly reached throughout the decades. Liquidity also looks adequate, with a debt-to-EBITDA ratio of 8.4x and interest coverage at 1.18 times.

Additionally, 79% of the REIT's debt carries a fixed interest rate. Speaking of which, its cost of debt is also attractive as the weighted average interest rate of its mortgages, loans, and bonds is 4.71%. Moreover, there is no immediate threat to profitability from potentially higher interest expenses as there is no maturity in 2024 and the 3 years after involve small amounts coming due relative to the ~$966 million of mortgages, loans, and bonds outstanding.

Investor Presentation

Dividend & Valuation

UMH currently pays a quarterly dividend of $0.21 per share which implies a 5.48% forward yield. Although the yield is fairly attractive, the dividend is not ideal for a dividend-focused portfolio.

First, the 96.83% payout ratio based on AFFO is concerning and though the REIT has been paying a dividend for 33 years, it has only recently started increasing it after it cut it in 2008 (and very conservatively at that).

{kind=link}

Regardless, the 7.2% implied cap rate the shares are trading at seems a bit high to me today. Back when I was covering Sun Communities ( SUI ), I was more pessimistic about cap rates in general and I thought that such a large cap rate premium over residential assets made sense at the time (around 7%). But if residential properties can fetch sub-5% in the near term, I think that 6% for manufactured homesites/homes is less conservative than 7% but more reasonable. We should also consider that UMH uses a 5% cap rate to calculate the value of some of its assets in its latest investor presentation.

Therefore, assuming a 6% cap rate, UMH is selling at a 23.1% discount to NAV ($19.92), which reflects a 30.04% upside. Additionally, the price has recently gone much higher than the present NAV, but unfortunately began falling about the time the Fed started raising the rate in 2022:

Risks

REITs are fairly predictable and aren't usually speculative vehicles, but there are always some risks involved. The first is related to the dividend; again, it might not be a great fit for a dividend portfolio because the payment record doesn't suggest decent future dividend growth and the high payout ratio makes this even more unlikely. The company may cut the dividend again and if you buy the stock just for it, you might have to realize a loss to get out of your position to reallocate your funds accordingly.

Additionally, the REIT's portfolio is not as diversified as some investors would prefer to hedge risks that come from changes in population, unemployment rates, and rent prices. If you're looking for exposure to manufactured homes but greater diversification, then Sun Communities offers that both geographically and based on asset type, but I don't think it's as attractive as UMH.

Last, asset values fluctuate all the time, which makes NAV calculations not an exact science. I believe that 6% is conservative considering that the company uses 5% to value its assets today, but you can only assume what the market for manufactured homesites/homes is going to be in the future and sometimes you can be wrong.

Verdict

All in all, I believe that the REIT is a buy at its current price. I don't love the dividend yield, nor the high payout ratio, but the operating performance has been great and the discount to NAV is attractive.

What's your take? Do you own UMH or intend to? Why or why not? Let me know below and I'll get back to you as soon as I can. Thank you for reading!

For further details see:

UMH Properties: Growth With A Margin Of Safety