UMH - UMH Properties Is Cheap Enough After 40% Drop

Summary

- UMH Properties has a large and growing portfolio of manufactured housing communities.

- It's set to benefit from its large land bank and heightened demand for affordable housing.

- The large drop in price over the past 12 months gives value investors an opportunity to layer into the stock.

Manufactured housing is one of the best kept secrets in real estate. That's because they operate like Apartment REITs, but benefit from stickier tenant relationships, due to ownership of the underlying land, resulting in a more assured revenue stream and lower operating costs for the landlord.

This brings me to UMH Properties ( UMH ), which as seen below, has seen significant pressure on its share price, falling by 40% over the past 12 months. At the current price of $16.10, UMH is far closer to its 52-week low than its 52-week high of $27.44. This article highlights why now may be an opportune time to layer into this value dividend stock.

{kind=link}

Why UMH?

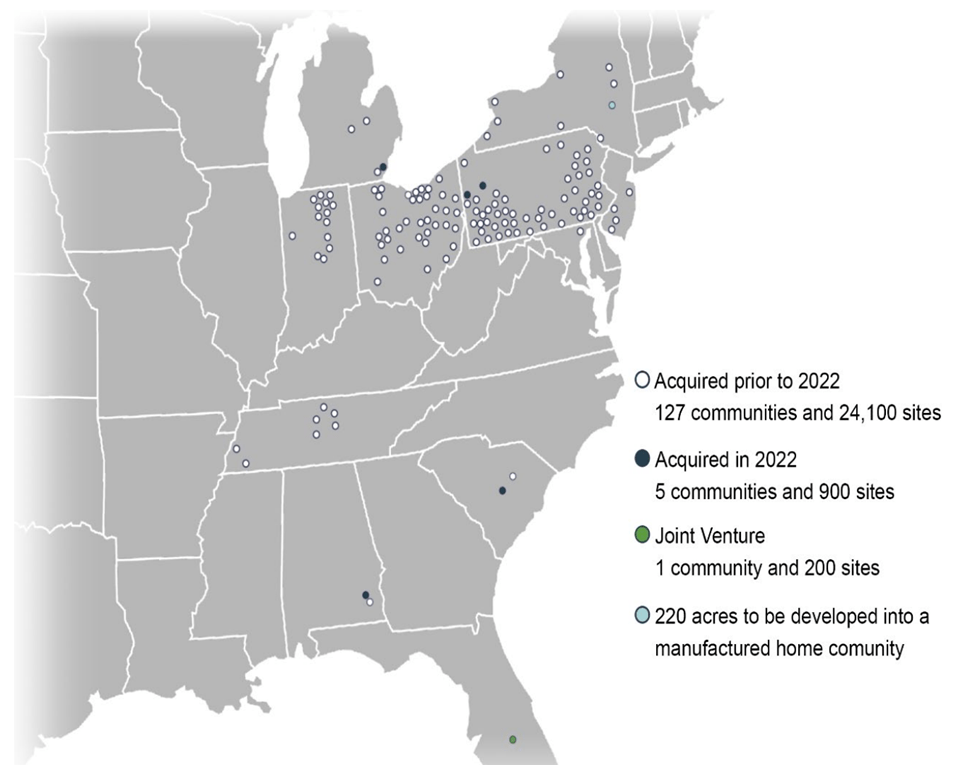

UMH Properties is a growing manufactured housing REIT that's been around since 1968 (since 1985 as a public company). At present, it has 132 communities containing 25K developed home sites, representing an increase of 5 communities totaling 900 sites from a year ago.

UMH's locations are primarily clustered around Pennsylvania and Ohio, near the energy producing regions of the Marcellus and Utica shale formations, home to one of the largest sources of natural gas in the world. This results in efficient scale, as having properties clustered results in lower property management overhead.

{kind=link}

UMH is seeing respectable growth, with rental income rising by 7% YoY during the third quarter. In the current era of rising rates, home affordability is as important as ever, and UMH is seeing the benefits of that. This is reflected by its sales of manufactured homes growing by a robust 16% YoY and 29% sequentially.

It's worth noting that normalized FFO per share did decline by $0.02 per share, to $0.21. This was due to opportunistic equity raises done at the end of 2021 and beginning of 2022, which would not have been possible at current prices. This enabled UMH to redeem $247 million worth of 6.75% Series C Preferred Stock, and had UMH received a full quarter's worth of benefit, management estimates FFO per share would have been $0.02 higher.

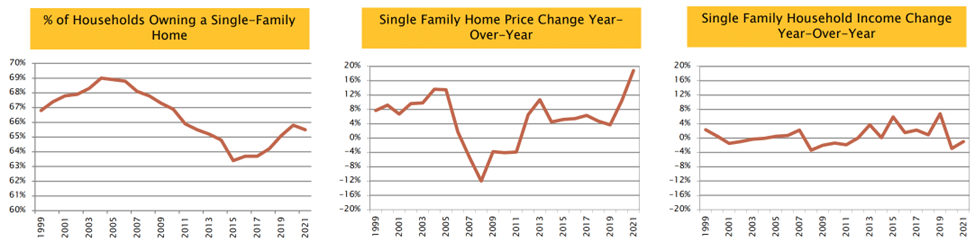

Looking ahead, UMH has plenty of growth runway due to its substantial landbank, comprised of 3,600 vacant lots to fill, and nearly 1,900 vacant acres on which to build 7,600 future lots. As shown below, the percentage of households owning a single family home remains well below the peak in 2005, with the upward momentum in recent years derailed by higher interest rates.

{kind=link}

While higher rates are a headwind for traditional single family home sales, it bodes well for manufactured housing providers such as UMH due to their affordability. This was highlighted by management during the last conference call :

Historically elevated home prices continue to drive strong demand for manufactured homes in our communities. Our nation continues to experience a shortage of affordable housing, and that shortage is only going to intensify as new housing units do not address the affordable end of the housing market.

The deceleration of residential home sales is likely to reduce single-family home starts by 100,000 units or more. The manufactured housing industry can help bridge the housing shortfall by developing 500 communities containing 200 sites annually or 100,000 new units.

UMH has spent decades providing affordable housing by acquiring communities with needed capital improvements and deferred maintenance and informing them into first-class communities that our residents are proud to call home. This business plan has allowed us to provide over 25,000 affordable housing sites to the nation.

One item that could use some improvement is the somewhat leveraged balance sheet, with a net debt to EBITDA ratio of 7.3x. While this is due to the growing nature of the portfolio, I would like to see improvement in this metric.

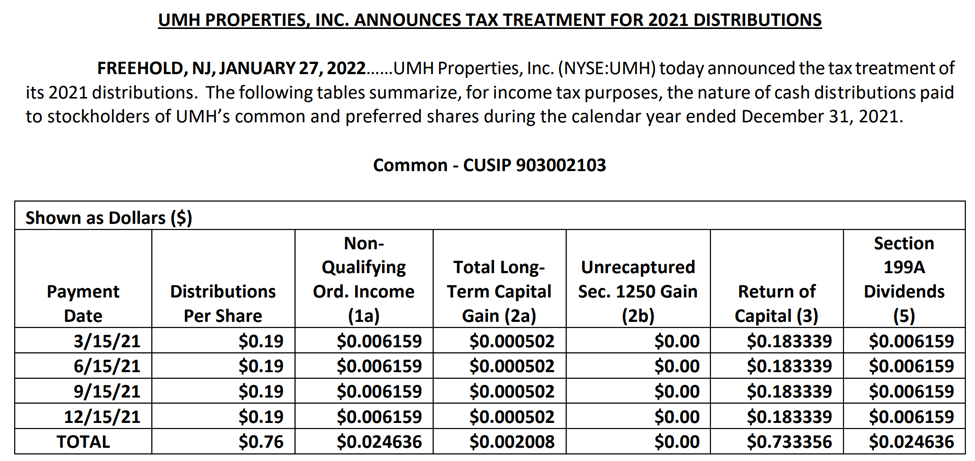

Nonetheless, I see value in the stock and the 5% dividend yield. Notably, the vast majority of the dividend in 2021 was treated as a return of capital, as shown below. This was obviously an advantage for investors last year from a tax perspective.

{kind=link}

Tax advantaged return of capital is due to a stream of new home development, which triggers depreciation, as highlighted by fellow SA contributor Ross Bowler in a recent article :

When we asked UMH CFO, Anna Chew, what accommodates the high return of capital ratio, she responded that it was application of depreciation and amortization allowances. If you look at recent community purchases in South Carolina and Michigan , you might perceive that UMH is an acquisitive growth company. When they buy and redevelop manufactured housing communities, UMH follows on with installation of hundreds of new homes for their rental program. These new home purchases create an extended stream of depreciation and amortization.

Turning to valuation, UMH doesn't scream cheap at the current price of $16.10 with a forward P/FFO of 20.8. However, analysts are projecting robust growth over the next 2 years, as shown below, as development projects come online. Analysts also have a consensus Strong Buy rating with an average price target of $21.44 , implying potentially very strong total returns from current levels.

{kind=link}

Investor Takeaway

UMH offers an attractive dividend yield of 5% and analysts project strong growth over the next two years. While UMH's balance sheet is somewhat leveraged, management has done a good job of using their capital to turn around formerly distressed communities into quality housing options for residents. Admittedly, UMH is not a sleep well at night stock, but I find value in the current price for potentially strong long-term returns.

For further details see:

UMH Properties Is Cheap Enough After 40% Drop